Global Phenotypic Screening Market

Market Size in USD Billion

USD

2.68 Billion

USD

5.62 Billion

2025

2033

USD

2.68 Billion

USD

5.62 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.68 Billion | |

| USD 5.62 Billion | |

| % | |

|

Phenotypic Screening Market Overview

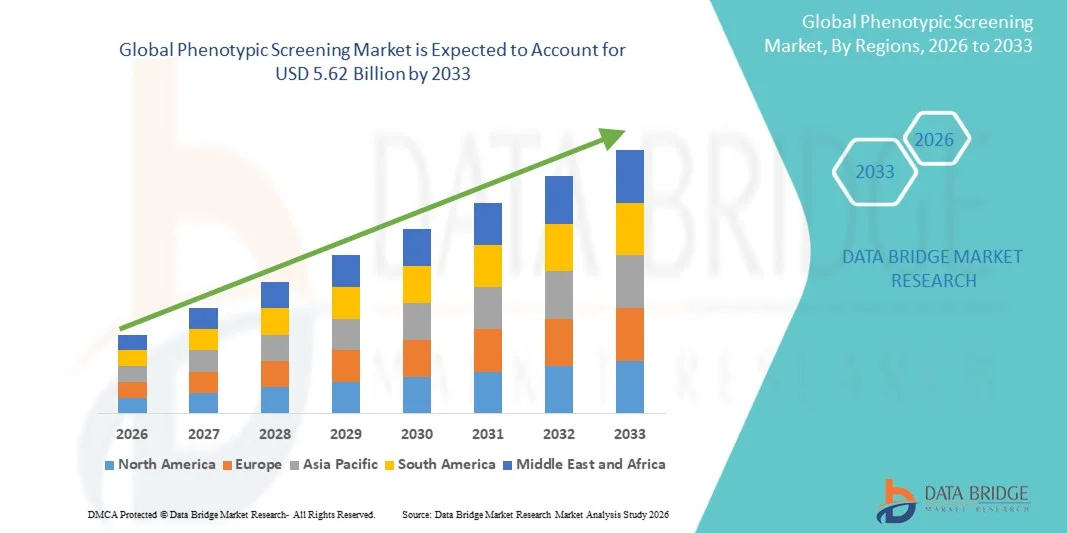

As per Data Bridge Market Research analysis The phenotypic screening market was valued at USD 2.68 billion in 2025 and is projected to reach USD 5.62 billion by 2033, growing at a CAGR of 9.70% from 2026 to 2033. The market is experiencing consistent growth driven by increasing demand for advanced drug discovery approaches, rising adoption of high-content screening technologies, and growing applications of phenotypic screening in pharmaceutical and biotechnology research. The market is expanding due to the shift from traditional target-based drug discovery toward phenotype-driven approaches that enable identification of novel drug candidates and therapeutic mechanisms.

The increasing investment in drug discovery and development activities, combined with advancements in automated imaging, artificial intelligence, and high-throughput screening platforms, is encouraging pharmaceutical companies, biotechnology companies, and contract research organizations to adopt phenotypic screening solutions. Cell-based assays, high-content screening, and automated analysis platforms are enhancing screening efficiency by providing comprehensive insights into cellular responses, disease mechanisms, and potential therapeutic targets.

Market Size & Forecast

- Global Market Value (2025): USD 2.68 Billion

- Expected Market Value (2033): USD 5.62 Billion

- Forecast CAGR (2026–2033): 9.70%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Key Market Trends & Insights

- North America dominated the phenotypic screening market with the largest revenue share of 38.9% in 2025, supported by strong pharmaceutical and biotechnology research activities, advanced drug discovery infrastructure, and increasing adoption of high-content screening technologies.

- The reagents & consumables segment led the market with a 42.3% share in 2025, driven by the recurring and essential requirement of consumable products across phenotypic screening workflows

- Asia Pacific is expected to be the fastest-growing region with a projected CAGR of 10.2% from 2026 to 2033, fueled by rapid biopharma sector expansion, increasing government investment in drug discovery infrastructure, and growth of outsourced CRO services in China, Japan, South Korea, and India

- Software is the fastest-growing product type, projected to register a CAGR of 11.4%, reflecting the surge in integration of artificial intelligence, machine learning, automated image analysis, and advanced data management platforms.

- The cell-based assays segment dominated the technology category with a 48.6% revenue share in 2025, led by the increasing adoption of cellular models for evaluating biological responses and identifying potential therapeutic compounds.

- Drug discovery accounted for 52.7% of the market, preferred by increasing adoption of phenotypic approaches for identifying novel therapeutic candidates and understanding disease mechanisms.

- The toxicology studies segment is the fastest-growing application category, with a CAGR of 9.1%, driven by increasing demand for early-stage safety evaluation and predictive toxicity assessment

Report Scope and Phenotypic Screening Market Segmentation

|

Attributes |

Phenotypic Screening Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Phenotypic Screening Market Trends

Trend: Integration of Artificial Intelligence and High-Content Screening Technologies

Pharmaceutical and biotechnology companies are increasingly adopting AI-enabled phenotypic screening platforms to accelerate compound identification, image analysis, and cellular response profiling. The integration of artificial intelligence with high-content screening enables automated interpretation of complex biological datasets, improving screening accuracy and reducing analysis time. Advanced imaging technologies combined with machine learning algorithms are supporting multiparametric analysis of cellular phenotypes, allowing researchers to identify novel therapeutic candidates and mechanisms of action more efficiently. For instance, in January 2024, Recursion introduced its Phenom foundation model, developed using high-throughput cellular imaging data and machine learning approaches to analyze cellular responses to chemical and genetic perturbations, demonstrating the growing role of AI-driven phenotypic screening in accelerating drug discovery.

The integration of AI, automated imaging, and advanced analytics is transforming phenotypic screening into a data-driven approach, creating opportunities for faster and more efficient drug discovery workflows.

Phenotypic Screening Market Dynamics

Key Market Driver: Rising Adoption of Phenotypic Screening in Drug Discovery and Development

The increasing demand for novel drug discovery approaches is driving the adoption of phenotypic screening technologies across pharmaceutical and biotechnology organizations. Unlike traditional target-based screening, phenotypic screening enables researchers to identify compounds based on observable biological effects, supporting the discovery of first-in-class therapies and new mechanisms of action. Growing investments in precision medicine, cell-based assays, and advanced disease models are further strengthening the role of phenotypic screening in early-stage drug development programs. For instance, in November 2023, Bayer and Recursion Pharmaceuticals expanded their research collaboration in precision oncology, leveraging Recursion’s artificial intelligence-guided drug discovery platform, which integrates biological and chemical data with machine learning approaches, including high-resolution imaging data, to accelerate identification of novel therapeutic candidates.

The growing need for efficient therapeutic discovery methods and mechanism-independent approaches is accelerating the adoption of phenotypic screening across the biopharmaceutical industry.

Key Restraint/Challenge: High Cost and Complexity of Phenotypic Screening Platforms

A significant challenge in the phenotypic screening market is the high investment required for advanced screening infrastructure, including automated imaging systems, high-content analysis platforms, specialized reagents, and data processing capabilities. The complexity of managing large-scale biological datasets and the requirement for skilled personnel increase operational costs, limiting adoption among smaller research organizations and institutions with restricted budgets. In addition, integration of artificial intelligence and advanced analytics tools requires significant computational resources and technical expertise. For instance, Thermo Fisher Scientific’s CellInsight™ High-Content Screening platforms integrate automated microscopy, image acquisition, and quantitative image analysis capabilities, enabling researchers to perform complex cellular assays and phenotypic profiling for drug discovery applications.

The high cost of equipment, data management requirements, and technical complexity remain major barriers limiting widespread adoption of advanced phenotypic screening solutions.

Key Market Opportunity: Expansion of Organoid Models and AI-Based Phenotypic Analysis

The growing adoption of advanced biological models, including patient-derived organoids and induced pluripotent stem cell (iPSC)-based systems, presents significant opportunities for the phenotypic screening market. These models provide more physiologically relevant disease environments compared with traditional two-dimensional cell cultures, improving predictive accuracy in drug discovery. The combination of organoid-based screening with artificial intelligence and automated image analysis is enabling researchers to evaluate complex biological responses and identify promising therapeutic candidates more effectively. For instance, in January 2025, Merck KGaA’s Life Science business acquired HUB Organoids Holding B.V., expanding its organoid technology portfolio to provide patient-derived organoid models and screening services that support more predictive drug discovery and development workflows.

The integration of organoid models, artificial intelligence, and automated phenotypic analysis is creating new growth opportunities by improving the accuracy and scalability of next-generation drug discovery platforms.

Phenotypic Screening Market Scope

The phenotypic screening market is segmented on the basis of product type, technology, application, and end-user.

- By Product Type

On the basis of product type, the phenotypic screening market is segmented into reagents & consumables, instruments, software, and services. The reagents & consumables segment dominated the market with a 42.3% share in 2025, owing to the recurring and essential requirement of consumable products across phenotypic screening workflows. This segment includes cell culture media, assay kits, fluorescent dyes, antibodies, transfection reagents, microplates, and biosensor substrates required for routine screening activities. Increasing adoption of cell-based assays, high-content screening, CRISPR functional screening, and 3D organoid-compatible formats is strengthening demand for specialized reagents and consumables. Pharmaceutical and biotechnology companies rely on continuous procurement of these products to support large-scale screening campaigns and compound evaluation studies. Growing expansion of laboratory infrastructure in emerging markets, including China, India, and South Korea, is further increasing consumable demand. The segment is expected to maintain its leading position due to the recurring nature of consumption and increasing screening throughput requirements.

The software segment is projected to register the fastest growth with a CAGR of 11.4% from 2026 to 2033, driven by increasing integration of artificial intelligence, machine learning, automated image analysis, and advanced data management platforms. Software solutions enable researchers to process and interpret large volumes of phenotypic datasets generated through high-content screening systems. Growing adoption of AI-powered image analysis tools is improving hit identification, cellular profiling, and mechanism-of-action analysis. Pharmaceutical companies and research organizations are increasingly implementing data-driven screening workflows to enhance discovery efficiency. Cloud-based platforms and integrated analytics solutions are further improving scalability and accessibility. Rising complexity of biological datasets is expected to accelerate demand for specialized phenotypic screening software solutions.

- By Technology

On the basis of technology, the phenotypic screening market is segmented into cell-based assays, biochemical assays, high-content screening, and others. The cell-based assays segment dominated the market with a 48.6% revenue share in 2025, supported by increasing adoption of cellular models for evaluating biological responses and identifying potential therapeutic compounds. Cell-based assays allow researchers to analyze complex cellular changes without requiring prior knowledge of specific molecular targets. These assays are widely utilized in early-stage drug discovery, disease modeling, toxicity evaluation, and mechanism-of-action studies. Increasing use of human-derived cell models, CRISPR-based approaches, and advanced cellular technologies is further supporting segment growth. Pharmaceutical and biotechnology companies are adopting cell-based screening methods to improve prediction of drug efficacy and safety outcomes. The ability to provide biologically relevant insights continues to drive the dominance of this technology segment.

The high-content screening segment is projected to witness the fastest growth with a CAGR of 11.1% from 2026 to 2033, driven by increasing demand for automated microscopy, multiparametric imaging, and advanced cellular analysis capabilities. High-content screening combines automated fluorescence microscopy with quantitative image analysis to evaluate multiple cellular parameters simultaneously. Increasing adoption of artificial intelligence and machine learning tools is improving image interpretation and screening efficiency. Pharmaceutical companies and CROs are investing in high-content platforms to support large-scale compound screening and complex disease modeling. Advancements in confocal imaging, automation, and miniaturized screening formats such as 384- and 1536-well plates are further accelerating adoption. Growing demand for detailed cellular profiling is expected to support continued expansion of high-content screening technologies.

- By Application

On the basis of application, the phenotypic screening market is segmented into drug discovery, toxicology studies, target validation, and others. The drug discovery segment dominated the market with a 52.7% share in 2025, driven by increasing adoption of phenotypic approaches for identifying novel therapeutic candidates and understanding disease mechanisms. Phenotypic screening enables evaluation of functional biological responses, allowing researchers to discover compounds without requiring predefined molecular targets. Increasing pharmaceutical R&D investment and growing demand for innovative drug discovery methods are supporting market expansion. These approaches are increasingly used for identifying first-in-class therapies and exploring complex disease pathways. The integration of high-content imaging, multi-omics analysis, and artificial intelligence is further enhancing drug discovery efficiency. Growing demand for predictive and mechanism-agnostic screening approaches continues to strengthen this segment’s leadership.

The toxicology studies segment is expected to register significant growth with a CAGR of 9.1% from 2026 to 2033, supported by increasing demand for early-stage safety evaluation and predictive toxicity assessment. Phenotypic screening enables researchers to identify cellular responses and adverse effects associated with drug candidates before clinical development. Growing regulatory emphasis on alternative testing approaches and reduction of animal-based testing is supporting adoption of advanced cellular screening models. Human-relevant cell systems are improving the accuracy of toxicity prediction compared with conventional methods. Pharmaceutical companies are increasingly incorporating phenotypic toxicity assessment into development pipelines to reduce late-stage failures. Rising focus on safer and more efficient drug development is expected to drive growth in this application segment.

- By End User

On the basis of end user, the phenotypic screening market is segmented into pharmaceutical & biotechnology companies, academic & research institutes, contract research organizations, and others. The pharmaceutical & biotechnology companies segment dominated the market with a 51.1% share in 2025, driven by increasing investment in drug discovery pipelines and adoption of advanced screening technologies. These companies extensively utilize phenotypic screening for compound identification, cellular response analysis, and therapeutic candidate evaluation. Growing demand for innovative medicines and increasing complexity of drug development programs are encouraging adoption of advanced screening platforms. Integration of automation, artificial intelligence, and high-content imaging technologies is improving research efficiency. Expansion of biotechnology research activities and precision medicine initiatives is further supporting demand. The segment remains the largest end-user category due to extensive involvement in pharmaceutical discovery and development activities.

The contract research organizations segment is projected to be the fastest-growing end-user segment with a CAGR of 10.4% from 2026 to 2033, driven by increasing outsourcing of drug discovery activities by pharmaceutical and biotechnology companies. CROs provide specialized phenotypic screening services, including assay development, compound profiling, and high-content screening capabilities. Outsourcing enables smaller biotechnology companies to access advanced screening infrastructure without significant capital investment. Increasing demand for cost-efficient research models is accelerating CRO adoption globally. Leading CROs are expanding screening facilities and investing in advanced technologies to support pharmaceutical clients. The growing preference for flexible research partnerships is expected to further strengthen CRO growth in the phenotypic screening market.

Phenotypic Screening Market Regional Analysis

North America dominated the phenotypic screening market with the largest revenue share of 38.9% in 2025, supported by strong pharmaceutical and biotechnology research activities, advanced drug discovery infrastructure, and increasing adoption of high-content screening technologies. The region benefits from the presence of major pharmaceutical companies, biotechnology firms, contract research organizations, and academic research institutions involved in advanced screening applications. Growing investments in artificial intelligence, automated imaging platforms, and precision medicine research are accelerating market development. Increasing adoption of cell-based assays, high-content screening systems, and advanced data analysis solutions is further strengthening regional growth. Rising focus on innovative drug discovery approaches, mechanism-of-action studies, and development of novel therapeutics continues to support North America's leading position in the global phenotypic screening market.

U.S. Phenotypic Screening Market Insight

The U.S. phenotypic screening market is witnessing strong growth due to the presence of leading pharmaceutical and biotechnology companies, advanced life science research infrastructure, and increasing adoption of AI-enabled drug discovery platforms. The country’s strong ecosystem of biomedical research organizations, contract research organizations, and technology providers is driving demand for high-content screening, cellular imaging, and automated phenotypic analysis solutions. Increasing investment in precision medicine, artificial intelligence, and next-generation biological models is further accelerating market adoption across pharmaceutical research applications. In January 2024, U.S.-based Recursion Pharmaceuticals introduced its Phenom foundation model, developed using large-scale biological imaging datasets to analyze cellular phenotypes through artificial intelligence. The platform demonstrates the growing integration of AI, high-content imaging, and automated phenotypic analysis technologies in U.S. drug discovery workflows, supporting increased adoption of advanced phenotypic screening solutions across pharmaceutical and biotechnology companies.

Europe Phenotypic Screening Market Insight

The Europe phenotypic screening market remains a significant contributor to global revenue, driven by strong pharmaceutical research capabilities, advanced biotechnology infrastructure, and increasing adoption of innovative drug discovery technologies. The presence of established life science companies, academic research institutions, and collaborative research networks is supporting regional expansion. Increasing focus on advanced cellular models, automated screening platforms, and next-generation biology approaches is strengthening adoption across European research organizations. In January 2025, Merck KGaA’s Life Science business completed the acquisition of HUB Organoids Holding B.V., expanding its next-generation biology portfolio with patient-derived organoid technologies that support advanced disease modeling and drug development research.

U.K. Phenotypic Screening Market Insight

The U.K. phenotypic screening market is experiencing steady growth, supported by strong academic research capabilities, biotechnology innovation, and increasing collaboration between research institutions and pharmaceutical companies. Growing adoption of advanced screening technologies, automated assay platforms, and translational research solutions is contributing to market development. Furthermore, government-supported life science initiatives and access to specialized drug discovery infrastructure are improving the adoption of phenotypic screening technologies across the country. The. U.K.-based Cellular Generation and Analysis Network and academic research groups have advanced high-content cellular analysis approaches, supporting image-based phenotypic profiling and cell-based screening research for disease modelling and therapeutic discovery.

Germany Phenotypic Screening Market Insight

The Germany phenotypic screening market is expanding steadily due to the country’s strong pharmaceutical industry, advanced biomedical research environment, and increasing investment in innovative drug discovery technologies. Pharmaceutical companies and research organizations are adopting phenotypic screening approaches for compound evaluation, disease modeling, and identification of therapeutic candidates. Continuous development of advanced biological models, automation technologies, and data-driven screening approaches is further supporting market growth in Germany. In January 2025, Merck KGaA’s Life Science business completed the acquisition of HUB Organoids Holding B.V., expanding its next-generation biology portfolio through access to patient-derived organoid technologies that support more predictive disease modeling and drug discovery research. Organoid models are increasingly used in phenotypic drug discovery workflows by improving biological relevance compared with conventional cell models.

Asia-Pacific Phenotypic Screening Market Insight

The Asia-Pacific phenotypic screening market is expected to witness rapid growth, driven by expanding pharmaceutical research activities, increasing biotechnology investments, and rising adoption of advanced drug discovery technologies in countries such as China, Japan, South Korea, and India. Growing research infrastructure, increasing outsourcing of pharmaceutical R&D activities, and development of biotechnology hubs are supporting regional market expansion. In addition, increasing adoption of artificial intelligence, high-content imaging, and advanced cellular models is accelerating phenotypic screening implementation across academic and commercial research sectors. Daiichi Sankyo (Japan) collaborated with LPIXEL to develop an AI-enabled phenotypic screening system that uses machine learning algorithms to analyze cellular images and support identification of potential drug candidates, demonstrating the increasing adoption of AI-driven phenotypic screening technologies in Asia-Pacific drug discovery research

Japan Phenotypic Screening Market Insight

The Japan phenotypic screening market is witnessing consistent growth due to strong pharmaceutical research capabilities, advanced biotechnology infrastructure, and increasing adoption of innovative screening methods. Pharmaceutical companies, research institutions, and technology organizations are increasingly utilizing cellular analysis, imaging technologies, and advanced biological models for drug discovery applications. Moreover, Japan’s focus on regenerative medicine, precision medicine, and life science innovation is contributing to broader adoption of phenotypic screening solutions. RIKEN’s Center for Integrative Medical Sciences conducts advanced biomedical research using large-scale biological data analysis and cellular research approaches to support understanding of disease mechanisms and therapeutic development.

China Phenotypic Screening Market Insight

The China phenotypic screening market is growing rapidly, driven by increasing pharmaceutical R&D investment, expansion of biotechnology companies, and rising government support for innovative drug development. Growing adoption of AI-enabled screening platforms, high-content imaging technologies, and automated analysis solutions across research organizations is significantly boosting market demand. In addition, increasing collaboration between biotechnology companies, academic institutions, and pharmaceutical organizations is strengthening China’s position as a rapidly developing market for phenotypic screening technologies. WuXi AppTec’s upgraded screening platform integrates high-content screening, cell-based assays, and advanced screening technologies to analyze cellular responses and accelerate molecular discovery, reflecting the increasing adoption of phenotypic screening approaches in China’s drug discovery ecosystem.

Phenotypic Screening Market Share

The phenotypic screening industry is primarily led by well-established companies, including:

- Merck KGaA (Germany)

- Thermo Fisher Scientific Inc. (U.S.)

- Revvity (U.S.)

- Agilent Technologies, Inc. (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Danaher (U.S.)

- BD (U.S.)

- Eppendorf SE (Germany)

- Sartorius AG (Germany)

- Promega Corporation (U.S.)

- Corning Incorporated (U.S.)

- Charles River Laboratories (U.S.)

- Eurofins Scientific SE (Luxembourg)

- Evotec SE (Germany)

- Recursion Pharmaceuticals (U.S.)

- QIAGEN (Netherlands)

- Molecular Devices, LLC (U.S.)

- Cytiva (U.S.)

- Lonza (Switzerland)

Latest Developments in Phenotypic Screening Market

- In January 2025, Merck KGaA’s Life Science business completed the acquisition of HUB Organoids Holding B.V. to expand its next-generation biology portfolio with advanced organoid technologies. The acquisition strengthens Merck’s capabilities in patient-derived organoid models, which are increasingly used in drug discovery research to improve disease modeling, biological relevance, and predictive evaluation of therapeutic candidates.

- In January 2025, Recursion Pharmaceuticals announced the availability of its Phenom foundation model, developed using large-scale biological imaging datasets to advance AI-powered phenomics research. The model applies artificial intelligence to analyze cellular images and identify complex biological patterns, supporting the development of computational approaches for drug discovery and phenotypic analysis

- In June 2023, Recursion Pharmaceuticals and NVIDIA announced a collaboration to accelerate AI-driven drug discovery by combining Recursion’s biological and chemical datasets with NVIDIA’s accelerated computing and artificial intelligence technologies. The collaboration supports the development of large-scale AI models for biology and chemistry, enabling faster analysis of complex biological data generated through advanced screening approaches

- In January 2022, FUJIFILM Cellular Dynamics and PhenoVista Biosciences announced a strategic alliance to improve the drug discovery process by combining induced pluripotent stem cell (iPSC) technologies with imaging-based phenotypic and high-content screening services. The collaboration enabled researchers to access human iPSC-derived differentiated cells for biologically relevant phenotypic assays, supporting improved disease modeling and identification of potential therapeutic candidates

- In October 2021, PerkinElmer launched its Signals Image Artist™ software, an advanced image analysis solution designed to support high-content screening workflows by enabling automated analysis and interpretation of complex cellular imaging data. The platform helps researchers extract quantitative biological insights from microscopy images, improving efficiency in cell-based screening and phenotypic analysis applications.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.