Global Phocomelia Market

Market Size in USD Billion

USD

1.56 Billion

USD

2.30 Billion

2024

2032

USD

1.56 Billion

USD

2.30 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.56 Billion | |

| USD 2.30 Billion | |

| % | |

|

Phocomelia Market Size

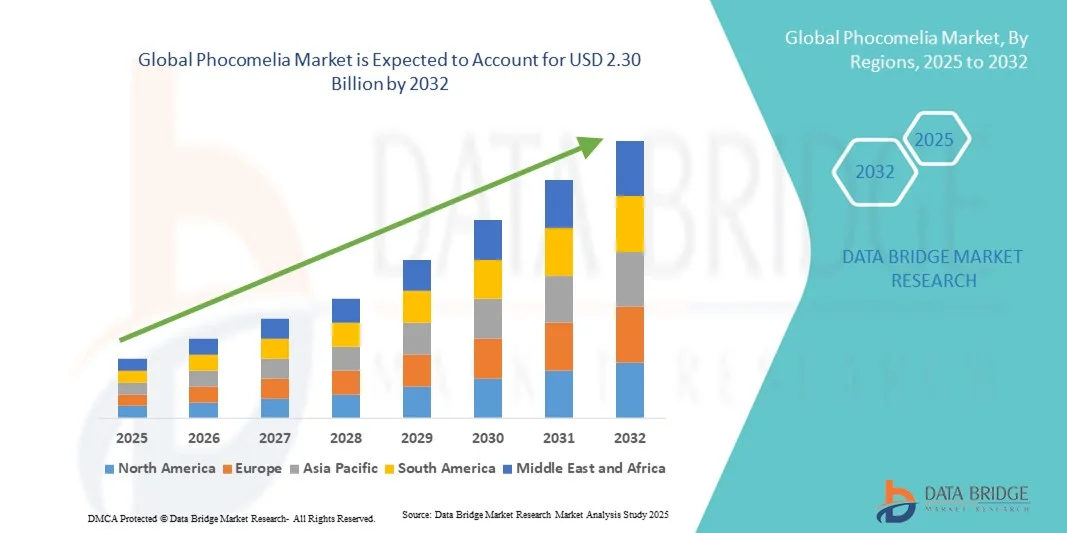

- The global phocomelia market size was valued at USD 1.56 billion in 2024 and is expected to reach USD 2.30 billion by 2032, at a CAGR of 5.00% during the forecast period

- The market growth is largely fueled by the growing awareness and advancements in diagnostic technologies and prenatal screening, leading to earlier detection and better management of congenital limb malformation disorders such as Phocomelia

- Furthermore, increasing research initiatives focused on genetic studies, along with rising investments in regenerative medicine and prosthetic innovation, are driving the development of advanced therapeutic and supportive care solutions for individuals affected by Phocomelia. These converging factors are accelerating the adoption of Phocomelia treatment and management solutions, thereby significantly boosting the industry’s growth

Phocomelia Market Analysis

- The Phocomelia market is witnessing significant growth driven by advancements in genetic testing, prenatal diagnostics, and improved access to early screening programs that help identify congenital limb reduction disorders at earlier stages. Increasing awareness among healthcare professionals and expecting parents regarding genetic abnormalities and teratogenic exposures is further contributing to market expansion

- The growing focus on research into gene therapy, stem cell treatment, and advanced prosthetic technologies is fueling innovation in the management of Phocomelia. Furthermore, collaborations between research institutions, biotechnology firms, and healthcare providers are enhancing therapeutic development and patient care outcomes

- North America dominated the phocomelia market with the largest revenue share of 41.6% in 2024, attributed to strong healthcare infrastructure, advanced genetic research facilities, and government support for rare disease treatment and early detection initiatives. The U.S. has shown notable progress in clinical studies and patient support programs, enhancing diagnosis and management rates

- Asia-Pacific is projected to be the fastest-growing region in the phocomelia market during the forecast period, driven by increasing investments in healthcare modernization, growing awareness of congenital disorders, and the availability of cost-effective diagnostic solutions in countries such as India, China, and Japan

- The Prosthetics and Therapy segment dominated the largest revenue share of 62.1% in 2024, driven by rising global adoption of advanced prosthetic limbs and physical therapy solutions

Report Scope and Phocomelia Market Segmentation

|

Attributes |

Phocomelia Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Phocomelia Market Trends

Advancements in Prenatal Screening and Gene Therapy Research

- A significant and accelerating trend in the global phocomelia market is the advancement of prenatal genetic screening technologies and the growing focus on gene therapy research to understand and potentially manage congenital limb malformations. These innovations are revolutionizing early diagnosis and the approach to treatment, enabling clinicians to detect abnormalities like phocomelia at an early fetal stage

- For instance, in March 2024, researchers at the University of Oxford reported progress in using CRISPR-Cas9 gene-editing tools to study the role of ESR1 and HOX gene mutations associated with phocomelia-like phenotypes. Similarly, the expansion of next-generation sequencing (NGS)-based prenatal panels has allowed healthcare providers to identify rare genetic syndromes more efficiently, improving early counseling and management strategies

- Moreover, the integration of AI-powered diagnostic imaging is improving the precision of detecting limb abnormalities through ultrasound and MRI. Companies are investing in machine learning algorithms that enhance fetal anomaly recognition and assist in clinical decision-making. This trend toward early detection and molecular-level understanding is shaping the future of congenital disorder management and offering promising insights for long-term therapeutic development

- The combination of gene-based research, digital diagnostic tools, and awareness programs about congenital malformation risks is creating a more proactive global healthcare ecosystem for addressing rare disorders such as phocomelia

Phocomelia Market Dynamics

Driver

Rising Awareness and Advancements in Genetic Research for Congenital Limb Disorders

- The growing global focus on rare disease awareness, coupled with advancements in molecular genetics and fetal imaging technologies, is a key driver for the Phocomelia market. Increased medical understanding of limb development abnormalities has encouraged research collaborations and funding initiatives aimed at identifying the underlying causes and potential preventive approaches.

- For instance, in April 2023, the National Institutes of Health (NIH) launched a multi-year study under its Rare Diseases Clinical Research Network (RDCRN) to investigate limb malformation syndromes, including phocomelia, to support novel diagnostic and treatment pathways

- Furthermore, improvements in prenatal care, genetic counseling, and public awareness programs about teratogenic risks—such as exposure to thalidomide or harmful environmental factors—are driving early diagnosis and intervention. The availability of advanced 3D/4D ultrasound technologies and genetic marker testing also enhances detection accuracy, improving the management of affected pregnancies

- As healthcare systems continue to prioritize early detection and multidisciplinary research collaborations, the overall demand for improved diagnostic and therapeutic tools in congenital limb disorders like phocomelia is projected to increase steadily

Restraint/Challenge

Limited Treatment Availability and High Research Costs

- Despite advances in diagnostics, the lack of curative treatments for phocomelia remains a major challenge restraining market growth. Most existing approaches focus on symptom management, including orthopedic surgeries, prosthetic integration, and rehabilitation therapies, rather than genetic correction or prevention

- For instance, in December 2024, a report by Rare Diseases Europe (EURORDIS) highlighted that over 80% of congenital malformation disorders, including phocomelia, still lack disease-specific therapeutic solutions, emphasizing the need for increased research investment and international collaboration

- In addition, high costs associated with rare disease research—spanning clinical trials, genetic testing, and regulatory approvals—pose financial barriers, especially in low- and middle-income regions. The limited patient pool further complicates the process of conducting large-scale studies and obtaining commercial viability for potential therapies

- Moreover, ethical considerations in fetal intervention and gene-editing therapies create regulatory complexities, slowing down innovation. Addressing these challenges through targeted funding programs, policy support, and technological innovation in genetic medicine will be crucial for advancing the Phocomelia market in the coming years

Phocomelia Market Scope

The market is segmented on the basis of mutations, symptoms, treatment, causes, end-users, and distribution channel.

- By Mutations

On the basis of mutations, the Phocomelia market is segmented into Inherited Mutations and Spontaneous Genetic Mutations. The Inherited Mutations segment dominated the market with the largest revenue share of 58.6% in 2024, driven by the genetic transmission of defective genes across generations. Families with a history of genetic disorders often show recurring cases of Phocomelia, emphasizing the importance of genetic counseling and early detection. Advances in prenatal testing, such as amniocentesis and next-generation sequencing, have improved early diagnosis of inherited mutations. Moreover, increased awareness and healthcare spending in developed nations continue to support early screening initiatives. Genetic registries and population studies have further strengthened the ability to track hereditary transmission, supporting research funding. Rising awareness among expecting parents about hereditary risk factors also contributes to this segment’s dominance. The increasing availability of specialized diagnostic tools in hospitals and clinics has made it easier to identify inherited cases during early gestation.

The Spontaneous Genetic Mutations segment is expected to witness the fastest CAGR of 9.8% from 2025 to 2032, primarily due to rising exposure to mutagenic agents and environmental pollutants. Random mutations occurring during fetal development often result from external factors such as radiation exposure, chemical contact, or maternal drug intake. The growing global prevalence of spontaneous mutation-related birth defects highlights the role of preventive healthcare measures. Research advancements in genetic mapping and mutation tracking are expected to strengthen diagnostic capabilities for sporadic cases. In addition, the use of CRISPR and other gene-editing tools for identifying mutation origins has accelerated scientific studies. Environmental awareness programs and maternal care initiatives are also projected to contribute to early prevention. The growing investment in prenatal genetics research is further supporting the faster growth of this segment.

- By Symptoms

On the basis of symptoms, the Phocomelia market is segmented into Shortened or Missing Limbs, Shorter Neck Length, Mental Deficiencies, Vomiting, Migraines, Malformation of the Uterus, Urethra, Kidney, or Heart, and Problems with Blood Clotting. The Shortened or Missing Limbs segment dominated the largest market revenue share of 45.4% in 2024, as limb malformation is the most visible and commonly diagnosed symptom of Phocomelia. The high prevalence of limb-related deformities among affected infants drives strong demand for prosthetic and surgical interventions. Increasing accessibility to orthotic technologies, including 3D-printed prosthetics, is enhancing treatment efficiency and recovery rates. The rising number of specialized rehabilitation centers catering to limb deformities also supports market expansion. Government healthcare initiatives promoting early diagnosis and limb correction surgeries further strengthen segment dominance. Increased awareness of congenital limb defects through national programs and digital health platforms is also driving detection rates. The rising integration of physiotherapy and assistive devices in post-surgical care is a major supporting trend.

The Malformation of the Uterus, Urethra, Kidney, or Heart segment is projected to witness the fastest CAGR of 10.6% from 2025 to 2032, due to rising diagnostic precision in internal organ malformations linked to Phocomelia. The increased use of prenatal imaging and genetic analysis enables early detection of associated visceral anomalies. Growing awareness about multi-organ complications during gestation, especially in women with high-risk pregnancies, is fueling medical intervention rates. Healthcare providers are emphasizing integrated approaches for managing both external and internal malformations simultaneously. Research investments focusing on congenital organ deformities are expanding, improving postnatal survival rates. The integration of advanced pediatric surgical units and neonatal intensive care facilities has boosted treatment efficiency. Increased patient education regarding congenital organ complications and available therapies is further accelerating growth in this segment.

- By Treatment

On the basis of treatment, the Phocomelia market is segmented into Prosthetics and Therapy and Surgery. The Prosthetics and Therapy segment dominated the largest revenue share of 62.1% in 2024, driven by rising global adoption of advanced prosthetic limbs and physical therapy solutions. Innovations in lightweight, AI-enabled prosthetics are enhancing mobility and quality of life for patients. The availability of customized 3D-printed limb replacements has made prosthetics more accessible and affordable. Rehabilitation centers and occupational therapy programs are increasingly focusing on long-term functional recovery. Growing support from insurance providers for prosthetic coverage further accelerates adoption. The segment’s growth is also supported by rising government initiatives for disability inclusion and physical rehabilitation. The collaboration between medical device companies and hospitals has improved prosthetic customization standards. Rising awareness among caregivers and patients about the benefits of physiotherapy and mobility training contributes to segment strength.

The Surgery segment is expected to witness the fastest CAGR of 9.9% from 2025 to 2032, driven by increasing success rates of corrective and reconstructive procedures. Technological advancements in microsurgery and tissue regeneration techniques are transforming clinical outcomes. The integration of robotic-assisted surgery is improving precision and reducing recovery times. Pediatric and orthopedic surgeons are increasingly specializing in congenital limb correction. Rising investments in healthcare infrastructure and neonatal surgery units have improved access to advanced surgical interventions. Global collaborations in pediatric surgery training programs are also enhancing clinical expertise. Increased patient awareness and accessibility of post-operative care services further promote growth. As healthcare systems expand access to complex reconstructive surgeries, the demand for early intervention continues to rise.

- By Causes

On the basis of causes, the Phocomelia market is segmented into Maternal Intake of Thalidomide, Alcohol or Cocaine, Gestational Diabetes, X-Ray Radiation, and Blood Flow Problems. The Maternal Intake of Thalidomide segment dominated the market with a revenue share of 41.7% in 2024, attributed to the historical prevalence of thalidomide-induced birth defects. Although its use has declined, the residual impact on genetic counseling, risk awareness, and regulatory frameworks remains strong. The segment’s dominance is supported by ongoing medical studies linking thalidomide exposure to severe congenital limb deformities. Awareness campaigns have been established to prevent recurrence through stricter drug usage monitoring. The persistence of thalidomide-related cases in developing countries where regulations are less stringent continues to influence market share. Medical training programs also emphasize identifying early teratogenic exposure symptoms. The lessons learned from thalidomide have led to significant pharmaceutical reforms and enhanced preclinical testing standards worldwide.

The Gestational Diabetes segment is expected to witness the fastest CAGR of 10.2% from 2025 to 2032, driven by rising diabetes prevalence among pregnant women globally. Elevated glucose levels during pregnancy increase the risk of congenital deformities, including Phocomelia. Early screening and blood glucose monitoring during prenatal care are becoming routine practices, improving early diagnosis. Increased public awareness of maternal metabolic health is encouraging preventive interventions. Medical device innovations for continuous glucose monitoring are enhancing pregnancy management. Health organizations worldwide are prioritizing maternal wellness through nutritional and exercise programs. Collaboration between endocrinologists and obstetricians is leading to better fetal outcomes. As urban lifestyles and obesity rates rise, the link between gestational diabetes and congenital deformities continues to drive medical research and awareness.

- By End-Users

On the basis of end-users, the Phocomelia market is segmented into Clinics, Hospitals, Diagnostic Centres, Home Healthcare, and Others. The Hospitals segment dominated the largest market revenue share of 49.8% in 2024, due to the availability of multidisciplinary medical teams and advanced infrastructure for diagnosis and treatment. Hospitals are often the first point of care for congenital deformity cases, offering integrated surgical and rehabilitative services. The rising prevalence of complex birth defects requiring specialized neonatal care supports segment dominance. Technological advancements such as robotic-assisted surgery and precision diagnostics are increasingly utilized in hospital settings. Growing patient preference for comprehensive treatment facilities and reimbursement coverage also contributes to growth. Expanding hospital networks in emerging economies and government funding for pediatric care units further strengthen this segment.

The Diagnostic Centres segment is expected to witness the fastest CAGR of 9.7% from 2025 to 2032, driven by the rising demand for early detection and genetic screening. Increased use of non-invasive prenatal testing (NIPT) and advanced imaging techniques enhances diagnostic precision. Growing awareness about the importance of early identification of congenital anomalies supports rapid growth. The collaboration between diagnostic labs and genetic counseling services provides patients with early intervention options. Technological innovations such as AI-based image recognition for fetal abnormalities are improving outcomes. Diagnostic centres also play a crucial role in monitoring maternal exposure to harmful agents. The segment benefits from government support for expanding prenatal testing coverage and private sector investments in diagnostic infrastructure.

- By Distribution Channel

On the basis of distribution channel, the Phocomelia market is segmented into Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy. The Hospital Pharmacy segment dominated the market with a revenue share of 54.2% in 2024, supported by the direct supply of essential medicines, surgical aids, and post-operative care drugs. Hospitals maintain close coordination between physicians and pharmacists for prescribing specialized treatments. The presence of in-house pharmacies ensures immediate availability of antibiotics, pain management drugs, and prosthetic support products. Hospital pharmacies also play a key role in managing thalidomide-related risk by monitoring prescriptions. The segment’s dominance is reinforced by patient reliance on hospital-based treatment channels for congenital conditions. Growing emphasis on integrated patient care systems within hospitals further strengthens this trend.

The Online Pharmacy segment is projected to witness the fastest CAGR of 11.1% from 2025 to 2032, driven by increasing digitalization of healthcare delivery. Online pharmacies enable convenient access to prosthetic maintenance supplies, prescribed drugs, and rehabilitation materials. Rising e-commerce penetration and improved logistics systems are accelerating product delivery for patients in remote areas. The growing popularity of telehealth and e-prescription models supports this segment’s expansion. Online platforms also provide better price transparency and offer educational content on congenital disorders. The COVID-19 pandemic further accelerated the adoption of online pharmacy services for chronic and congenital treatments. Increasing collaboration between online platforms and healthcare providers continues to drive this segment’s strong growth trajectory.

Phocomelia Market Regional Analysis

- North America dominated the phocomelia market with the largest revenue share of 41.6% in 2024, attributed to its strong healthcare infrastructure, advanced genetic research facilities, and robust government initiatives supporting rare disease detection and treatment

- The region’s commitment to precision medicine and early genetic screening programs has significantly improved diagnostic accuracy and patient care outcomes for congenital limb disorders. Ongoing collaborations between clinical research institutions and biotechnology companies are also accelerating the development of targeted therapies and diagnostic advancements

- Moreover, supportive regulatory frameworks and funding from organizations such as the National Institutes of Health (NIH) and U.S. Food and Drug Administration (FDA) for rare disease studies further bolster market expansion

U.S. Phocomelia Market Insight

The U.S. phocomelia market captured the largest revenue share in 2024 within North America, driven by advancements in genomics research, robust healthcare expenditure, and growing awareness of congenital malformations. The country has witnessed rapid progress in prenatal genetic testing and molecular diagnostics, with several academic research centers and hospitals integrating next-generation sequencing (NGS) and AI-assisted imaging into prenatal care. Furthermore, the availability of specialized rehabilitation programs, prosthetic technologies, and government-backed patient assistance initiatives contributes to improved management outcomes. The ongoing push for rare disease registries and increased funding for gene therapy research is expected to sustain U.S. market growth over the coming years.

Europe Phocomelia Market Insight

The Europe phocomelia market is projected to grow at a substantial CAGR during the forecast period, primarily driven by the region’s stringent healthcare quality standards, robust rare disease policies, and active participation in international genetic research collaborations. Increasing investments in genomic medicine and prenatal diagnostics are strengthening the region’s capacity to detect and manage congenital disorders like phocomelia at earlier stages. Public awareness campaigns and support from organizations such as EURORDIS (Rare Diseases Europe) are further facilitating early diagnosis and patient advocacy. The region also benefits from a well-structured healthcare reimbursement system that encourages adoption of advanced testing and prosthetic solutions.

U.K. Phocomelia Market Insight

The U.K. phocomelia market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by the country’s expanding focus on genetic health research and early intervention for congenital anomalies. Initiatives such as the Genomics England Project and the 100,000 Genomes Project have strengthened the U.K.’s diagnostic capabilities in rare genetic disorders. In addition, government-funded programs emphasizing prenatal screening and patient counseling are enhancing disease awareness and detection. Increased collaboration between academic researchers, healthcare providers, and biotechnology firms is expected to further drive innovation in diagnosis and therapeutic support.

Germany Phocomelia Market Insight

The Germany phocomelia market is expected to expand at a considerable CAGR throughout the forecast period, propelled by the country’s advanced biomedical research infrastructure, technological innovation, and emphasis on ethical genetic practices. Germany’s strong focus on clinical research and patient safety standards supports extensive studies on congenital disorders and their genetic origins. In addition, high adoption of precision diagnostics, along with the availability of advanced prosthetic technologies and rehabilitation centers, contributes to improved patient outcomes. Government incentives promoting rare disease research and partnerships between universities and biotech firms further enhance market growth prospects.

Asia-Pacific Phocomelia Market Insight

The Asia-Pacific phocomelia market is poised to grow at the fastest CAGR during the forecast period from 2025 to 2032, driven by increasing healthcare investments, rapid urbanization, and growing awareness of congenital disorders. Countries such as India, China, and Japan are investing heavily in medical genetics research, diagnostic laboratory infrastructure, and prenatal screening programs. Government-led initiatives to improve maternal and child health, along with improved accessibility to affordable genetic testing, are boosting early diagnosis rates. Furthermore, local manufacturing capabilities and cross-border research collaborations are enhancing regional affordability and expanding patient reach.

Japan Phocomelia Market Insight

The Japan phocomelia market is gaining significant traction due to the country’s technological sophistication in medical imaging, genetics, and rehabilitation care. Japan’s strong emphasis on innovation and healthcare automation is leading to better early detection and patient support programs for congenital disorders. Furthermore, the country’s rapidly aging population is driving investments in advanced prosthetic technologies and orthopedic care. Research collaborations between universities and medical institutions are also fostering genomic studies to better understand the causes and inheritance patterns of phocomelia.

China Phocomelia Market Insight

The China phocomelia market accounted for the largest market revenue share within Asia-Pacific in 2024, fueled by rapid advancements in genomics, growing healthcare infrastructure, and national initiatives promoting rare disease research. The expansion of genetic counseling centers, coupled with government-backed newborn screening programs, has accelerated early identification of congenital malformations. China’s large population base, combined with rising healthcare spending and local biotech innovation, positions it as a critical growth hub for diagnostic and therapeutic solutions in the phocomelia market. Increasing academic research and technology partnerships with international institutions further enhance its long-term growth trajectory.

Phocomelia Market Share

The Phocomelia industry is primarily led by well-established companies, including:

• Pfizer Inc. (U.S.)

• GlaxoSmithKline plc (U.K.)

• Novartis AG (Switzerland)

• Johnson & Johnson Services, Inc. (U.S.)

• F. Hoffmann-La Roche Ltd (Switzerland)

• Merck & Co., Inc. (U.S.)

• Sanofi S.A. (France)

• Bayer AG (Germany)

• Teva Pharmaceutical Industries Ltd. (Israel)

• Cipla Ltd. (India)

• Sun Pharmaceutical Industries Ltd. (India)

• AstraZeneca plc (U.K.)

• Lilly (U.S.)

• AbbVie Inc. (U.S.)

• Takeda Pharmaceutical Company Limited (Japan)

• Bristol Myers Squibb (U.S.)

• Dr. Reddy’s Laboratories Ltd. (India)

• Amgen Inc. (U.S.)

• Viatris Inc. (U.S.)

• Biocon Limited (India)

Latest Developments in Global Phocomelia Market

- In August 2021, U.S. regulatory records showed a significant modification to the THALOMID (thalidomide) REMS program which updated program materials and requirements — a regulatory action that reinforced pregnancy-prevention controls for thalidomide and related phthalimide drugs and therefore directly affects the global risk-management environment for therapies linked to phocomelia risk

- In March 2023, the U.S. FDA issued an approval letter for a supplemental application related to THALOMID that included updates to the product’s REMS documentation and implementation details; this letter reaffirmed strict distribution controls and reinforced pregnancy prevention and pharmacovigilance measures that continue to shape clinical use and public-health surveillance for teratogenic exposures linked to phocomelia

- In June 2023, the clinical resource StatPearls released an updated Phocomelia review (last updated June 12, 2023) summarizing contemporary epidemiology, etiologies (including thalidomide exposure and genetic causes), diagnostic pathways, and multidisciplinary management — a consolidation that has been widely used by clinicians for current best-practice guidance and teaching

- In July 2023, multiple news and clinical outreach initiatives documenting 3D-printed pediatric prosthetic deliveries (for example, student-and-NGO led programs delivering low-cost custom prostheses to children abroad) drew attention to the rapid practical adoption of low-cost, rapid-turnaround 3D printing solutions for limb replacement and rehabilitation in children with congenital limb defects — a development that accelerated interest and investment in affordable prosthetic options for phocomelia patients globally

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.