Global Phosphor Screen Market

Market Size in USD Billion

USD

3.67 Billion

USD

4.79 Billion

2024

2032

USD

3.67 Billion

USD

4.79 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.67 Billion | |

| USD 4.79 Billion | |

| % | |

|

Phosphor Screen Market Size

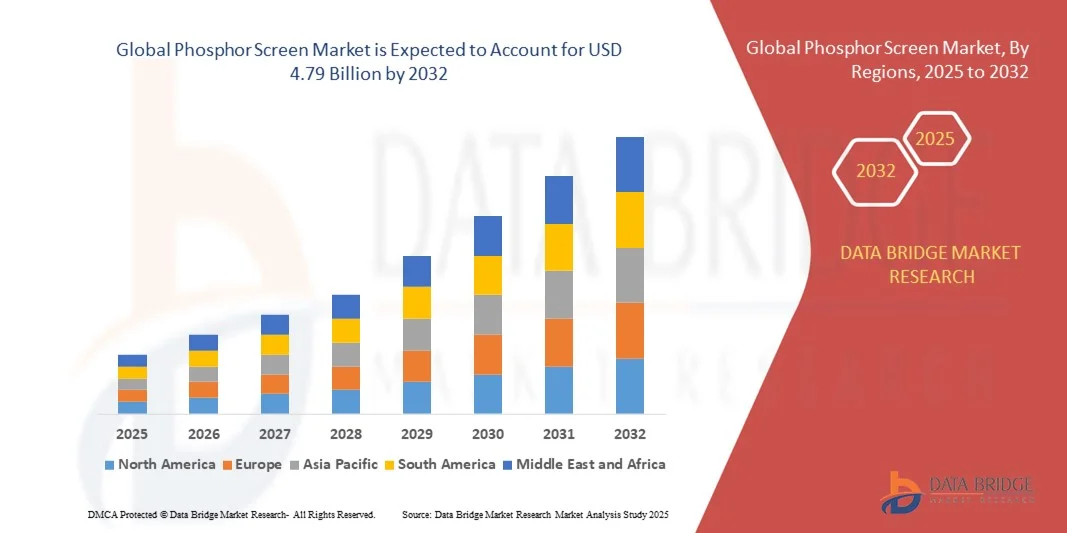

- The global phosphor screen market size was valued at USD 3.67 billion in 2024 and is expected to reach USD 4.79 billion by 2032, at a CAGR of 3.40% during the forecast period

- The market growth is largely fuelled by the increasing demand for advanced imaging technologies in healthcare, industrial inspection, and scientific research applications

- Rising investments in medical diagnostics, such as X-ray and computed radiography systems, are boosting the adoption of phosphor screens due to their superior image clarity and sensitivity

Phosphor Screen Market Analysis

- The global phosphor screen market is witnessing steady growth, driven by the expanding use of digital imaging systems across sectors such as healthcare, non-destructive testing, and security screening

- The market is shifting towards the adoption of energy-efficient and high-performance screens that provide enhanced image contrast and durability

- North America dominated the phosphor screen market with the largest revenue share in 2024, driven by strong demand for advanced imaging technologies in healthcare, industrial testing, and research applications. The region’s well-established infrastructure for medical diagnostics and non-destructive testing continues to support the widespread adoption of phosphor screens.

- Asia-Pacific region is expected to witness the highest growth rate in the global phosphor screen market, driven by technological innovation, expanding diagnostic imaging applications, and a surge in demand for high-resolution, low-exposure imaging solutions

- The short decay segment held the largest market revenue share in 2024, driven by its extensive use in medical imaging, non-destructive testing, and high-speed data acquisition applications that require rapid image response and reduced motion blur. Short decay phosphor screens provide enhanced temporal resolution and clarity, making them suitable for dynamic imaging systems and real-time analysis

Report Scope and Phosphor Screen Market Segmentation

|

Attributes |

Phosphor Screen Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Phosphor Screen Market Trends

Advancements In Digital Imaging And Radiography Technology

- The growing shift toward digital imaging and radiography is reshaping the phosphor screen market, as these screens play a crucial role in converting X-rays into visible light for image formation. The increasing demand for high-resolution and low-exposure imaging is encouraging the adoption of advanced phosphor screens across healthcare, industrial, and scientific applications. This trend is driven by the rising need for accuracy, faster image processing, and reduced radiation risks, particularly in diagnostic and non-destructive testing environments

- The integration of phosphor screens with digital detectors and imaging systems is accelerating in hospitals, research labs, and non-destructive testing facilities. Their ability to deliver sharper images with enhanced contrast has made them essential for early disease diagnosis, quality inspection, and analytical applications in material sciences. Furthermore, the transition from traditional film-based systems to digital platforms is increasing workflow efficiency and reducing maintenance costs

- The growing emphasis on eco-friendly and energy-efficient imaging systems is also promoting the development of new phosphor materials that reduce noise and enhance performance. Manufacturers are investing heavily in R&D to improve the efficiency, durability, and sensitivity of these screens, leading to broader use in both medical and industrial radiography. These advancements are also enabling the design of compact imaging systems for portable and field-based diagnostic applications

- For instance, in 2024, several imaging technology firms introduced rare-earth phosphor-based screens that improved luminescence efficiency by over 20%, significantly enhancing image clarity in low-dose X-ray systems. These innovations are helping healthcare providers achieve more accurate diagnostics while minimizing patient exposure. In addition, industrial users have reported improved throughput and inspection precision, boosting productivity across key sectors

- While technological advancements are enhancing market potential, continued innovation, material optimization, and cost-effectiveness remain critical to maintaining competitiveness and meeting the increasing demand across emerging sectors such as security screening and advanced microscopy. The evolution of hybrid imaging technologies and AI-driven image enhancement is expected to further expand market opportunities in the coming years

Phosphor Screen Market Dynamics

Driver

Rising Demand For High-Resolution Imaging In Healthcare And Industrial Applications

- The increasing need for superior imaging quality in both medical diagnostics and industrial inspection is a major driver for the phosphor screen market. These screens enable precise visualization in applications such as mammography, dental imaging, and non-destructive testing (NDT), where accuracy and clarity are critical. The shift toward digital and low-dose imaging modalities continues to strengthen the market’s technological landscape

- The expansion of global healthcare infrastructure, along with the rising number of imaging centers and diagnostic laboratories, is fueling phosphor screen adoption. Hospitals and clinics are increasingly upgrading to digital radiography systems that incorporate advanced phosphor materials to achieve higher contrast and faster image processing. This modernization drive is supported by government healthcare initiatives and growing investments in radiology equipment

- In industrial sectors, the growing use of X-ray inspection in aerospace, manufacturing, and electronics to detect defects and ensure product reliability further supports market demand. Companies are seeking high-sensitivity screens that can deliver consistent performance under varying conditions, helping reduce downtime and improve product quality assurance. The demand for compact, portable NDT systems is also contributing to the increased adoption of lightweight phosphor screens

- For instance, in 2023, several industrial equipment manufacturers integrated next-generation phosphor screens into their NDT systems, enabling faster inspection cycles and improved detection accuracy, particularly in automotive and aerospace components. These integrations also reduced operational costs by enhancing system efficiency and lifespan

- While rising demand continues to drive growth, ensuring cost efficiency, durability, and compatibility with evolving imaging platforms will be essential for long-term market expansion. Strategic collaborations and continual advancements in screen coatings are expected to improve adoption rates across multiple industries

Restraint/Challenge

High Production Cost And Limited Availability Of Advanced Phosphor Materials

- The production of phosphor screens involves complex material synthesis processes and the use of rare-earth elements, which significantly increases manufacturing costs. This cost structure limits affordability and scalability, especially for smaller imaging centers and research institutions. Furthermore, high initial setup and maintenance expenses often discourage adoption in developing regions

- Limited availability and fluctuating prices of raw materials such as gadolinium and terbium, which are crucial for high-performance phosphor coatings, also pose supply chain challenges. These constraints affect production stability and hinder the ability of manufacturers to meet growing global demand. The dependence on limited mining sources for these materials further intensifies market volatility

- In addition, the lack of standardized testing and performance benchmarks for phosphor materials across different applications often leads to inconsistency in product quality. This creates barriers for end-users seeking reliable and reproducible imaging results. Manufacturers must focus on establishing quality standards and improving cross-industry material uniformity

- For instance, in 2024, several imaging component suppliers reported production slowdowns due to shortages in rare-earth materials, leading to delayed deliveries and increased costs for medical device manufacturers. These disruptions also impacted large-scale industrial projects dependent on high-precision imaging

- Addressing these challenges will require strategic partnerships, advancements in material science, and investment in sustainable alternatives to ensure a stable supply and reduce overall production costs for long-term market viability. Industry players are exploring recycling methods and synthetic substitutes to lower dependency on rare-earth sources and stabilize production

Phosphor Screen Market Scope

The market is segmented on the basis of decay and end user.

- By Decay

On the basis of decay, the phosphor screen market is segmented into short decay and long decay. The short decay segment held the largest market revenue share in 2024, driven by its extensive use in medical imaging, non-destructive testing, and high-speed data acquisition applications that require rapid image response and reduced motion blur. Short decay phosphor screens provide enhanced temporal resolution and clarity, making them suitable for dynamic imaging systems and real-time analysis.

The long decay segment is expected to witness the fastest growth rate from 2025 to 2032, owing to its increasing adoption in scientific research, radiation monitoring, and display calibration where prolonged afterglow and signal retention are beneficial. Long decay screens are also gaining traction in applications demanding sustained visibility, such as dosimetry and phosphorescent display panels.

- By End User

On the basis of end user, the phosphor screen market is segmented into consumer electronics, healthcare electronics, telecommunication, scientific equipment manufacturing, research and academia, and others. The healthcare electronics segment held the largest market share in 2024, driven by the rising use of phosphor screens in digital radiography, mammography, and dental imaging systems. The growing focus on advanced diagnostic imaging and improved patient safety has boosted demand for high-resolution, low-dose phosphor materials.

The scientific equipment manufacturing segment is expected to witness the fastest growth rate from 2025 to 2032, supported by the expanding use of phosphor screens in laboratory instruments, spectroscopy, and material characterization systems. The increasing investments in R&D and the growing need for precision imaging in experimental physics and applied sciences are further driving segmental growth.

Phosphor Screen Market Regional Analysis

- North America dominated the phosphor screen market with the largest revenue share in 2024, driven by strong demand for advanced imaging technologies in healthcare, industrial testing, and research applications. The region’s well-established infrastructure for medical diagnostics and non-destructive testing continues to support the widespread adoption of phosphor screens.

- The increasing shift toward digital imaging, coupled with the presence of leading technology developers, further enhances innovation and product performance. In addition, rising investments in medical imaging and material sciences research are contributing to the growth of phosphor screen utilization across the region.

- The combination of strong R&D capabilities, high spending on technological upgrades, and a focus on quality imaging standards positions North America as a global hub for phosphor screen production and application.

U.S. Phosphor Screen Market Insight

The U.S. phosphor screen market held the largest revenue share in 2024 within North America, supported by the expanding use of imaging technologies in healthcare and industrial inspection. The presence of key manufacturers and research institutions drives continuous product innovation, enhancing imaging efficiency and accuracy. The growing adoption of digital radiography and non-destructive testing systems is fueling demand for high-sensitivity phosphor screens across medical and manufacturing sectors. Moreover, increasing investments in advanced medical diagnostics and material testing are further strengthening market growth in the U.S.

Europe Phosphor Screen Market Insight

The Europe phosphor screen market is expected to witness substantial growth from 2025 to 2032, propelled by advancements in healthcare imaging, scientific research, and industrial inspection systems. The region’s strong focus on safety regulations and quality standards in manufacturing processes supports the demand for precise and reliable imaging solutions. Furthermore, the integration of digital technologies and ongoing R&D initiatives in academic and industrial laboratories are enhancing the adoption of innovative phosphor screen materials.

U.K. Phosphor Screen Market Insight

The U.K. phosphor screen market is projected to register notable growth from 2025 to 2032, driven by increasing investments in medical imaging, life sciences research, and industrial testing. The country’s emphasis on digital transformation in healthcare and expanding infrastructure for diagnostic imaging are key contributors to market expansion. Moreover, growing collaborations between universities, research organizations, and imaging solution providers are fostering innovation in phosphor material development and imaging accuracy.

Germany Phosphor Screen Market Insight

The Germany phosphor screen market is expected to witness significant growth from 2025 to 2032, supported by the country’s strong manufacturing base and technological leadership in precision imaging. The rising need for advanced diagnostic systems and high-resolution non-destructive testing in automotive and aerospace industries is stimulating demand. In addition, Germany’s focus on sustainable material innovation and energy-efficient imaging systems aligns with its industrial and environmental objectives, promoting long-term market development.

Asia-Pacific Phosphor Screen Market Insight

The Asia-Pacific phosphor screen market is anticipated to record the fastest growth rate from 2025 to 2032, fuelled by expanding healthcare infrastructure, increasing industrialization, and advancements in imaging technologies in countries such as China, Japan, and India. The growing adoption of digital imaging for both medical and industrial applications is enhancing the use of phosphor screens across the region. Furthermore, cost-effective production capabilities and the presence of emerging local manufacturers are making Asia-Pacific a key contributor to global supply.

Japan Phosphor Screen Market Insight

The Japan phosphor screen market is expected to experience strong growth from 2025 to 2032, driven by the country’s technological innovation, strong research base, and demand for high-performance imaging systems. The extensive use of phosphor screens in healthcare imaging, electronics testing, and microscopy reflects Japan’s focus on precision and efficiency. In addition, continuous R&D in material science and imaging technologies is helping local manufacturers improve screen brightness, durability, and resolution for specialized applications.

China Phosphor Screen Market Insight

The China phosphor screen market accounted for the largest revenue share in the Asia-Pacific region in 2024, attributed to the nation’s rapid industrial growth, increasing healthcare investments, and large-scale adoption of digital imaging systems. China’s expanding manufacturing base and availability of cost-efficient production have strengthened its position as a global supplier of phosphor screens. Moreover, the government’s focus on technological advancement and infrastructure modernization continues to drive innovation and market growth across medical, industrial, and scientific domains.

Phosphor Screen Market Share

The Phosphor Screen industry is primarily led by well-established companies, including:

• GENERAL ELECTRIC COMPANY (U.S.)

• GIDS GmbH (Germany)

• Kimball Physics (U.S.)

• Phosphor Technology Ltd (U.K.)

• ProxiVision GmbH (Germany)

• Dr. Gassler Electron Devices (Germany)

• Hamamatsu Photonics K.K. (Japan)

• Apixia Inc (U.S.)

• AGFA Healthcare (Belgium)

• Scintacor (U.K.)

• Koninklijke Philips N.V. (Netherlands)

• 3Disc (U.S.)

• Kavo Dental (Germany)

• Stanford Computer Optics, Inc (U.S.)

• Hangzhou Kinghigh Technology Co., Ltd. (China)

• Durr NDT GmbH & Co. KG (Germany)

• Konica Minolta Business Solutions India Private Limited (India)

• Telecast Technology Corporation (China)

• NICHIA CORPORATION (Japan)

• Aimil Ltd (India)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Phosphor Screen Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Phosphor Screen Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Phosphor Screen Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.