Global Photovoltaic Pv Inverter Market

Market Size in USD Billion

USD

16.78 Billion

USD

27.46 Billion

2025

2033

USD

16.78 Billion

USD

27.46 Billion

2025

2033

| 2026 - 2033 | |

| USD 16.78 Billion | |

| USD 27.46 Billion | |

| % | |

|

Photovoltaic (PV) Inverter Market Overview

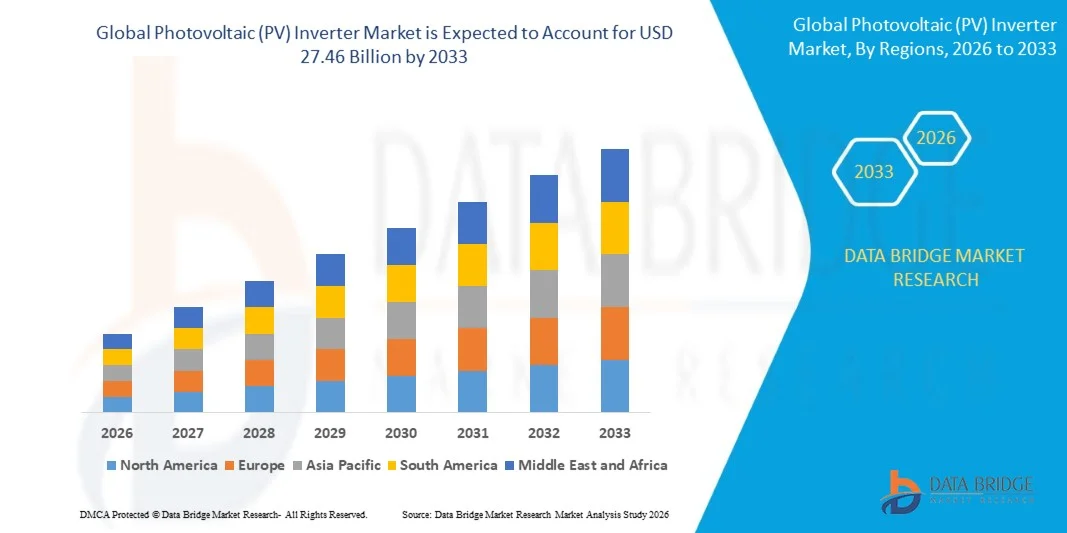

The Photovoltaic (PV) Inverter Market was valued at USD 16.78 Billion in 2025 and is projected to reach USD 27.46 Billion by 2033, growing at a CAGR of 6.35% from 2026 to 2033. The market is experiencing consistent growth driven by rapid growth in solar photovoltaic installations, increasing deployment of utility-scale solar projects, and rising adoption of distributed rooftop solar systems across residential and commercial sectors. Continuous advancements in inverter efficiency, smart grid integration, and hybrid energy storage compatibility are further accelerating market growth across global renewable energy ecosystems.

The increasing global focus on decarbonization, energy security, and transition toward renewable energy sources is significantly driving demand for PV inverters. Governments across major economies are implementing supportive policies, subsidies, and net metering frameworks that are encouraging large-scale solar adoption. In addition, rising electricity demand, declining solar installation costs, and growing integration of battery storage systems with solar PV infrastructure are further strengthening the adoption of advanced inverter technologies worldwide.

Key Market Trends & Insights

- Asia-Pacific dominated the Photovoltaic (PV) Inverter Market with the largest revenue share of 44.59% in 2025, supported by large-scale solar capacity additions, strong government renewable energy targets, and extensive deployment of utility-scale and rooftop PV systems

- The segment led the market with a 72.5% share in 2025, driven by widespread integration of solar systems into national electricity grids and large utility-scale installations

- North America is expected to be the fastest-growing region at a CAGR of 12.64% from 2026 to 2033, fueled by large-scale utility solar expansion, rising residential rooftop solar adoption, and increasing investments in clean energy infrastructure

- Above 110,000 W is the fastest-growing nominal output power type, projected to register a CAGR of 17.3% from 2026 to 2033, supported by large-scale utility solar farms requiring ultra-high-capacity power conversion systems

- The three phase segment dominated the power glass category with a 58.4% revenue share in 2025, led by extensive use in commercial, industrial, and utility-scale solar installations requiring higher power handling capacity

- Utility accounted for 46.8% of the market in 2025, preferred by large-scale solar farm installations and strong grid modernization programs across major economies

- The micro segment is the fastest-growing product category, with a CAGR of 16.1% from 2026 to 2033, driven by rising adoption in residential rooftop solar systems requiring panel-level optimization

Market Size & Forecast

- Global Market Value (2025): USD 16.78 Billion

- Expected Market Value (2033): USD 27.46 Billion

- Forecast CAGR (2026–2033): 6.35%

- Leading Region in 2025: Asia-Pacific

- Fastest Growing Region: North America

Report Scope and Photovoltaic (PV) Inverter Market Segmentation

|

Attributes |

Photovoltaic (PV) Inverter Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· ABB (Switzerland) · Schneider Electric (France) · Siemens (Germany) · Mitsubishi Electric Corporation (Japan) · General Electric (U.S.) · Omron Corporation (Japan) · SMA Solar Technology AG (Germany) · Delta Energy Systems Inc. (Taiwan) · Enphase Energy, Inc. (U.S.) · SolarEdge Technologies Inc. (Israel) · Huawei Technologies Co., Ltd. (China) · Kstar New Energy Co. Ltd (China) · ENF Ltd. (U.K.) · Sungrow (China) |

|

Market Opportunities |

· Expansion of Residential Rooftop Solar Adoption · Integration of Energy Storage with PV Inverter Systems · Growth Opportunities in Emerging Renewable Energy Markets |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Photovoltaic (PV) Inverter Market Trends

Trend: Increasing Adoption of Smart and Hybrid PV Inverters

Global PV inverter systems are increasingly shifting toward smart, AI-enabled, and hybrid configurations that integrate solar generation with battery storage and grid management capabilities. These advanced inverters improve energy efficiency, enable real-time monitoring, and support bidirectional power flow, making them essential for modern distributed energy systems. Growing deployment of rooftop solar and virtual power plant models is further accelerating adoption across residential and commercial segments.

For instance, Enphase Energy has expanded its IQ8 microinverter platform integrated with energy storage solutions, enabling grid-forming capabilities and improved residential energy independence across major solar markets.

Photovoltaic (PV) Inverter Market Dynamics

Key Market Driver: Rising Global Demand for Utility-Scale Solar Installations

The increasing deployment of large-scale solar farms is significantly driving demand for high-capacity PV inverters capable of efficient power conversion and grid integration. Utility-scale projects require advanced central and string inverters that ensure stable output, high efficiency, and compatibility with national grid systems. Strong government-backed solar auctions and renewable energy targets across major economies are further accelerating installations.

Companies such as Sungrow and Huawei Digital Power are widely supplying high-capacity inverters for large solar parks across China, the Middle East, and Europe, supporting rapid expansion of utility-scale solar infrastructure.

Key Restraint/Challenge: Grid Integration and Stability Constraints in High Solar Penetration Markets

Increasing penetration of solar PV into national grids is creating challenges related to voltage fluctuations, intermittency, and grid stability, particularly in regions with limited grid modernization. Existing transmission infrastructure in many markets is not fully equipped to handle variable solar output, requiring advanced inverter-based grid support functions. This is increasing complexity for utilities and slowing deployment in certain high-penetration regions.

For instance, grid operators in Germany have implemented stricter technical requirements for PV inverters to provide reactive power control and frequency support, reflecting the operational challenges of maintaining grid stability under high solar integration levels.

Key Market Opportunity: Integration of Energy Storage with PV Inverter Systems

The growing combination of solar PV systems with battery energy storage is creating strong opportunities for hybrid inverter solutions that enable seamless energy management and backup power capabilities. These integrated systems enhance self-consumption, improve grid reliability, and support peak load management across residential, commercial, and utility applications. Declining battery costs and supportive regulatory frameworks are further accelerating adoption of solar-plus-storage configurations.

Companies such as Tesla, SolarEdge Technologies, and SMA Solar Technology are actively expanding hybrid inverter portfolios integrated with storage systems, enabling advanced energy optimization and supporting the transition toward decentralized renewable energy ecosystems.

Photovoltaic (PV) Inverter Market Scope

The Photovoltaic (PV) Inverter market is segmented on the basis of application, connectivity, product, power glass, nominal output voltage, and nominal output power.

- By Application

On the basis of application, the Photovoltaic (PV) Inverter Market is segmented into residential, commercial, industrial, and utility. The Utility segment dominated the market with the largest share of 46.8% in 2025, driven by large-scale solar farm installations and strong grid modernization programs across major economies. Utilities increasingly deploy high-capacity PV inverters to manage fluctuating solar output and ensure grid stability under high renewable penetration. Expanding investments in centralized solar projects and government-backed clean energy auctions further strengthen segment dominance. Continuous demand for efficient power conversion in large solar parks reinforces its leading position.

The Residential segment is projected to register the fastest growth at a CAGR of 14.2% from 2026 to 2033, driven by rising rooftop solar adoption and increasing consumer focus on energy independence. Falling PV system costs and supportive net metering policies are encouraging household-level solar deployment across both developed and emerging regions. Growing awareness of electricity cost savings and backup power benefits is accelerating adoption in urban and semi-urban areas. Expanding incentive schemes for distributed solar generation further boost residential inverter demand across global markets.

- By Connectivity

On the basis of connectivity, the global PV Inverter market is segmented into standalone and on-grid systems. The On-Grid segment dominated the market with a share of 72.5% in 2025, driven by widespread integration of solar systems into national electricity grids and large utility-scale installations. Grid-tied inverters enable efficient energy export, net metering benefits, and optimized power distribution, making them highly preferred for commercial and utility applications. Rapid expansion of grid-connected solar farms across Asia-Pacific and Europe further strengthens dominance. Increasing grid infrastructure upgrades to accommodate renewable penetration supports long-term growth.

The Standalone segment is projected to register the fastest growth at a CAGR of 13.6% from 2026 to 2033, driven by rising demand for off-grid solar systems in remote and rural areas. These systems provide reliable electricity access in regions with limited or unstable grid infrastructure. Growing deployment of solar-powered microgrids for rural electrification and industrial backup applications is accelerating adoption. Declining battery storage costs and improvements in hybrid inverter efficiency further support segment expansion across emerging economies.

- By Product

On the basis of product, the global PV Inverter market is segmented into micro, string, and central inverters. The String Inverter segment dominated the market with a share of 41.3% in 2025, driven by its cost-effectiveness, ease of installation, and high efficiency in residential and commercial rooftop systems. String inverters offer flexible system design and are well-suited for distributed solar installations. Strong adoption across small and mid-scale solar projects further reinforces dominance. Increasing demand for modular and scalable solar solutions supports continued segment leadership.

The Micro Inverter segment is projected to register the fastest growth at a CAGR of 16.1% from 2026 to 2033, driven by rising adoption in residential rooftop solar systems requiring panel-level optimization. Micro inverters improve energy yield by minimizing shading losses and enabling real-time monitoring at the module level. Expanding smart home integration and growing preference for high-efficiency solar systems further accelerate demand. Continuous technological advancements in compact and high-reliability inverter design support rapid segment growth.

- By Power Class

On the basis of power class, the global PV Inverter market is segmented into single phase and three phase systems. The Three Phase segment dominated the market with a share of 58.4% in 2025, driven by extensive use in commercial, industrial, and utility-scale solar installations requiring higher power handling capacity. Three phase inverters ensure better load balancing, higher efficiency, and stable grid integration for large systems. Increasing deployment of industrial solar projects and utility-scale plants further strengthens dominance. Growing demand for high-capacity renewable energy infrastructure supports long-term market expansion.

The Single Phase segment is projected to register the fastest growth at a CAGR of 12.9% from 2026 to 2033, driven by rising residential solar adoption and small-scale commercial installations. These inverters are widely used in rooftop solar systems due to their lower cost and simpler installation process. Expanding urban housing solar programs and supportive government incentives further boost demand. Continuous improvements in compact inverter efficiency and safety features enhance adoption across residential users.

- By Nominal Output Voltage

On the basis of nominal output voltage, the PV Inverter market is segmented into 230 V, 230 - 400 V, 400 - 600 V, and above 600 V. The 230 - 400 V segment dominated the market with a share of 39.7% in 2025, driven by its widespread suitability for residential and commercial solar systems connected to standard distribution networks. This voltage range offers optimal efficiency and compatibility with most grid standards globally. Strong deployment in rooftop solar installations across urban areas reinforces dominance. Increasing adoption of decentralized solar systems further supports segment leadership.

The Above 600 V segment is projected to register the fastest growth at a CAGR of 15.4% from 2026 to 2033, driven by rising deployment of utility-scale solar farms requiring high-voltage power transmission for reduced energy losses. High-voltage inverters improve system efficiency and enable long-distance power evacuation from large solar parks. Expanding grid-scale renewable projects and cross-border energy trade initiatives further accelerate adoption. Advancements in high-voltage semiconductor technologies are enhancing performance and reliability.

- By Nominal Output Power

On the basis of nominal output power, the PV Inverter market is segmented into 300 W, 300 - 3,000 W, 3,000 - 33,000 W, 33,000 - 110,000 W, and above 110,000 W. The 3,000 - 33,000 W segment dominated the market with a share of 37.9% in 2025, driven by its extensive use in commercial rooftops and small industrial solar installations. This power range provides an optimal balance between efficiency, cost, and scalability for mid-sized projects. Strong adoption across commercial buildings and institutional solar systems further strengthens dominance. Growing demand for distributed generation systems supports sustained leadership.

The Above 110,000 W segment is projected to register the fastest growth at a CAGR of 17.3% from 2026 to 2033, driven by large-scale utility solar farms requiring ultra-high-capacity power conversion systems. These inverters are essential for maximizing efficiency in gigawatt-scale solar projects. Increasing global investment in utility-scale renewable energy infrastructure further accelerates adoption. Continuous technological advancements in high-power conversion and thermal management systems are enhancing reliability and performance.

Photovoltaic (PV) Inverter Market Regional Analysis

Asia-Pacific dominated the Photovoltaic (PV) Inverter market and accounted for the largest revenue share of 44.59% in 2025, supported by large-scale solar capacity additions, strong government renewable energy targets, and extensive deployment of utility-scale and rooftop PV systems. The region benefits from rapidly expanding electricity demand, favorable solar irradiation conditions, and cost-efficient manufacturing ecosystems for power electronics. Increasing investments in grid modernization, rising adoption of distributed solar systems, and strong policy support for carbon neutrality goals are accelerating regional market expansion.

China Photovoltaic (PV) Inverter Market Insight

China held the largest share in the Asia-Pacific Photovoltaic (PV) Inverter market in 2025, driven by its dominant position in global solar installations and strong domestic manufacturing capabilities for inverters and semiconductor components. The country has an extensive utility-scale solar farm network supported by aggressive renewable energy targets and large state-backed investments. Strong integration of solar power into national grid infrastructure and rapid deployment of high-capacity central and string inverters are further supporting growth. In addition, continuous export of Photovoltaic (PV) inverters to Europe, the Middle East, and emerging markets is reinforcing China’s leadership in the global inverter supply chain.

India Photovoltaic (PV) Inverter Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, driven by ambitious renewable capacity targets, rising utility-scale solar park development, and increasing rooftop solar adoption under government incentive programs. Expanding electrification needs, high solar potential, and declining system costs are significantly accelerating Photovoltaic (PV) inverter deployment across residential, commercial, and industrial segments. Strong policy initiatives such as solar auctions and net metering frameworks are further supporting market expansion. In addition, growing investments from global and domestic players in solar infrastructure are reinforcing long-term growth momentum.

Europe Photovoltaic (PV) Inverter Market Insight

The Europe Photovoltaic (PV) Inverter market is expanding steadily, supported by aggressive decarbonization targets, strong renewable energy mandates, and rising replacement demand for aging power infrastructure. Increasing adoption of distributed solar systems across residential and commercial sectors is strengthening demand for string and micro inverters. The region also benefits from strong technological innovation in smart inverters, grid-interactive systems, and energy management solutions. In addition, supportive policies for energy independence and reduction of fossil fuel reliance are accelerating market penetration across major European economies.

Germany Photovoltaic (PV) Inverter Market Insight

Germany accounted for the largest share in the Europe Photovoltaic (PV) Inverter market in 2025, driven by its well-established solar ecosystem, high rooftop solar penetration, and strong focus on energy transition policies. The country has extensive deployment of residential and commercial Photovoltaic (PV) systems integrated with advanced inverter technologies for grid stability and self-consumption optimization. Strong demand for smart energy systems, battery-integrated inverters, and energy-efficient solutions further reinforces market growth. In addition, robust manufacturing and R&D capabilities in power electronics are supporting Germany’s leadership position in the regional market.

U.K. Photovoltaic (PV) Inverter Market Insight

The U.K. market is supported by increasing investments in rooftop solar installations, commercial solar projects, and smart grid development initiatives. Rising energy prices and growing consumer preference for energy independence are driving adoption of Photovoltaic (PV) systems equipped with advanced inverters. The country is also witnessing increasing deployment of micro and string inverters in residential applications due to ease of installation and monitoring capabilities. In addition, supportive government policies for low-carbon energy transition are further contributing to market expansion.

North America PV Inverter Market Insight

North America is projected to grow at the fastest CAGR of 13.8% from 2026 to 2033, driven by large-scale utility solar expansion, rising residential rooftop solar adoption, and increasing investments in clean energy infrastructure. Strong demand for advanced grid-supporting inverters with smart monitoring and energy storage integration is significantly supporting market growth. Technological advancements in hybrid inverter systems and favorable tax incentives are further accelerating adoption. In addition, increasing corporate sustainability commitments and renewable procurement programs are boosting regional demand.

U.S. PV Inverter Market Insight

The U.S. accounted for the largest share in the North America PV Inverter market in 2025, supported by extensive utility-scale solar development, strong rooftop solar penetration, and growing deployment of energy storage-integrated inverter systems. Federal and state-level incentives such as tax credits and renewable portfolio standards are significantly driving installations. The country also benefits from strong participation of leading inverter manufacturers and technology providers. In addition, increasing focus on grid resilience and distributed energy generation is reinforcing the U.S. leadership position in the regional market.

Photovoltaic (PV) Inverter Market Share

The Photovoltaic (PV) Inverter industry is primarily led by well-established companies, including:

- ABB (Switzerland)

- Schneider Electric (France)

- Siemens (Germany)

- Mitsubishi Electric Corporation (Japan)

- General Electric (U.S.)

- Omron Corporation (Japan)

- SMA Solar Technology AG (Germany)

- Delta Energy Systems Inc. (Taiwan)

- Enphase Energy, Inc. (U.S.)

- SolarEdge Technologies Inc. (Israel)

- Huawei Technologies Co., Ltd. (China)

- Kstar New Energy Co. Ltd (China)

- ENF Ltd. (U.K.)

- Sungrow (China)

Latest Developments in Photovoltaic (PV) Inverter Market

- In December 2024, SolarEdge Technologies undertook major restructuring, including workforce reductions, which reflects the ongoing correction in residential solar demand across the U.S. and Europe. This development is impacting the PV inverter market by intensifying competition among key players and pushing companies toward higher-margin utility-scale and storage-integrated solutions. It is also accelerating the shift from residential-heavy revenue models to diversified energy management portfolios

- In November 2024, SMA Solar Technology strengthened its focus on hybrid inverter systems and grid-support solutions integrated with battery storage applications. This development is reshaping the PV inverter market by increasing demand for advanced inverters capable of supporting grid stability and decentralized energy networks. It is further encouraging adoption of virtual power plant models and enhancing the role of inverters in energy trading and storage optimization

- In October 2024, Huawei Digital Power (FusionSolar) upgraded its residential and commercial PV inverter portfolio with enhanced efficiency, AI-based monitoring, and improved safety features. This development is influencing the market by increasing competition in smart inverter technologies and accelerating the transition toward intelligent, digitally connected solar systems. It is also strengthening demand for high-performance distributed energy solutions in urban and semi-urban installations

- In September 2024, Sungrow Power Supply expanded its global manufacturing capacity, including increased production capabilities in Europe, to support rising utility-scale solar demand. This development is impacting the PV inverter market by improving supply chain resilience and reducing lead times for large solar projects. It is also reinforcing Sungrow’s competitiveness in the central and string inverter segments, particularly in utility-scale installations

- In August 2024, Enphase Energy expanded deployment of its IQ8 microinverter platform along with its IQ Battery 5P system across key residential solar markets. This development is driving the PV inverter market toward deeper integration of solar-plus-storage systems, enabling higher energy independence and grid-forming capabilities. It is also strengthening the shift toward modular, panel-level power electronics in residential solar applications

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Photovoltaic Pv Inverter Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Photovoltaic Pv Inverter Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Photovoltaic Pv Inverter Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.