Global Plastic Film Pouches Market

Market Size in USD Billion

USD

69.95 Billion

USD

101.39 Billion

2024

2032

USD

69.95 Billion

USD

101.39 Billion

2024

2032

| 2025 - 2032 | |

| USD 69.95 Billion | |

| USD 101.39 Billion | |

| % | |

|

Global Plastic Film Pouches Market Size

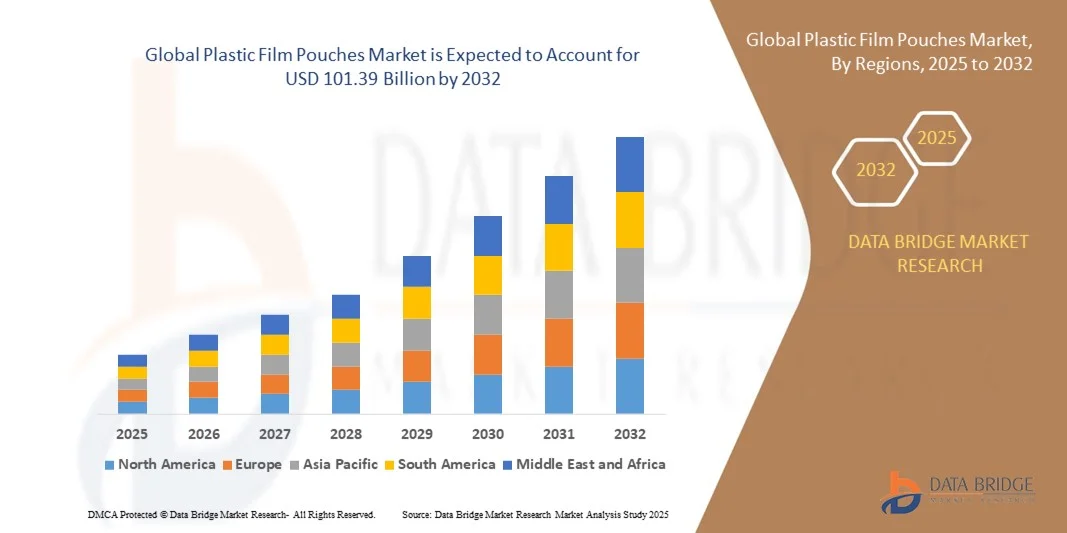

- The global Plastic Film Pouches Market size was valued at USD 69.95 billion in 2024 and is projected to reach USD 101.39 billion by 2032, growing at a CAGR of 4.75% during the forecast period.

- The market expansion is primarily driven by increasing demand for lightweight, cost-effective, and sustainable packaging solutions across food, beverage, personal care, and pharmaceutical sectors.

- Moreover, advancements in material science and flexible packaging technologies are enabling enhanced barrier protection, shelf life, and design versatility—key factors encouraging manufacturers to shift from rigid to flexible packaging, thereby propelling the growth of plastic film pouches globally.

Global Plastic Film Pouches Market Analysis

- Plastic film pouches, known for their lightweight, flexible, and cost-efficient packaging properties, are becoming essential across various industries including food, beverages, personal care, and pharmaceuticals, owing to their sustainability benefits and ease of customization.

- The surging demand for plastic film pouches is primarily driven by growing consumer preference for convenient, resealable, and portable packaging, along with rising environmental awareness prompting brands to adopt recyclable and eco-friendly materials.

- Asia-Pacific dominated the Global Plastic Film Pouches Market with the largest revenue share of 33.1% in 2024, supported by strong demand from the packaged food sector, advanced manufacturing technologies, and increasing adoption of sustainable packaging by major brands in the U.S. and Canada.

- Europe is expected to be the fastest growing region in the Global Plastic Film Pouches Market during the forecast period due to rapid urbanization, expanding middle-class population, and a booming e-commerce industry driving demand for flexible packaging.

- The polyethylene segment dominated the market with the largest revenue share of 36.5% in 2024, driven by its versatility, durability, and cost-effectiveness. It is widely used in food and beverage applications due to its strong moisture barrier and heat-sealing capabilities

Report Scope and Global Plastic Film Pouches Market Segmentation

|

Attributes |

Plastic Film Pouches Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Global Plastic Film Pouches Market Trends

Innovation in Sustainable Materials and Functional Design

- A significant and accelerating trend in the global Plastic Film Pouches Market is the continued innovation in sustainable materials and functional pouch designs, aimed at enhancing both environmental performance and end-user convenience. This focus on sustainability and usability is reshaping packaging strategies across multiple industries, particularly in food, beverage, and personal care sectors.

- For instance, major packaging providers are developing recyclable mono-material pouches and compostable films to replace traditional multi-layered structures. Companies such as Amcor and Mondi have launched recyclable stand-up pouches that meet recyclability standards while maintaining product protection and shelf appeal.

- These innovations also include functional enhancements such as resealable zippers, spouts, and easy-tear openings, which significantly improve consumer convenience. Furthermore, the use of high-barrier films preserves product freshness while reducing the need for additional protective layers, supporting efforts to reduce plastic waste.

- The integration of smart packaging features, such as QR codes and NFC tags, is also emerging—allowing brands to engage with consumers, track inventory, and provide authentication, further increasing the functional value of plastic film pouches.

- As environmental regulations tighten and consumer awareness of sustainability grows, brands are increasingly opting for pouches made from post-consumer recycled (PCR) content or bio-based plastics. This shift is driving the development of advanced pouch technologies that meet both performance and environmental criteria.

- The demand for plastic film pouches that combine sustainability with enhanced functionality is rising rapidly across global markets, as businesses respond to evolving consumer preferences and regulatory pressures, making innovation in pouch design and materials a key differentiator in the competitive landscape.

Global Plastic Film Pouches Market Dynamics

Driver

Growing Demand Driven by Sustainability and Convenience in Packaging

- The increasing global focus on sustainability, coupled with rising demand for convenient and user-friendly packaging, is a major driver for the growth of the Plastic Film Pouches Market.

- For instance, in March 2024, Amcor introduced new high-barrier recyclable pouch formats aimed at reducing environmental impact without compromising product integrity. Such innovations are expected to boost market growth as both consumers and regulatory bodies push for greener alternatives to traditional rigid plastics.

- Plastic film pouches offer advantages such as lightweight structure, reduced material usage, and space-efficient transportation, making them highly attractive for manufacturers and retailers. Their resealable closures, ease of use, and portability also enhance consumer appeal, particularly in the food and beverage sector.

- Moreover, the growing demand for on-the-go consumption and single-serve products is encouraging the adoption of flexible pouch packaging across various industries including healthcare, cosmetics, and pet food.

- As e-commerce continues to expand globally, brands are turning to durable, flexible pouches that protect products during shipping while maintaining a premium look and feel. This trend is particularly evident in Asia-Pacific and North America, where urbanization and rising disposable incomes are driving changes in consumer behavior and packaging preferences.

- The shift towards environmentally responsible packaging, combined with the need for practical and appealing product formats, is expected to continue fueling the growth of plastic film pouches across global markets.

Restraint/Challenge

Environmental Concerns and Recycling Infrastructure Limitations

- Despite the growing adoption of plastic film pouches, environmental concerns related to their recyclability and the lack of adequate recycling infrastructure remain significant challenges to market expansion.

- Multi-layer pouch structures, which often combine different materials for barrier protection, are difficult to recycle using standard processes. This complexity has led to increased scrutiny from environmental groups and consumers demanding more sustainable packaging solutions.

- For Instance, many municipal recycling programs are not equipped to handle flexible plastic packaging, resulting in low actual recycling rates despite claims of recyclability. This disconnect can undermine consumer confidence and brand credibility.

- While companies like Mondi and Dow are investing in recyclable and mono-material pouch solutions, the transition to widespread circular packaging systems requires significant infrastructure development, regulatory alignment, and consumer education.

- Additionally, the perception that flexible packaging contributes to plastic pollution in oceans and landfills can negatively impact brand image, particularly among environmentally conscious consumers.

- Overcoming these challenges will require greater collaboration between packaging companies, governments, and waste management stakeholders, along with continued innovation in materials and recycling technologies. Balancing performance, cost, and sustainability remains a critical hurdle for the long-term success of the plastic film pouches market.

Global Plastic Film Pouches Market Scope

The plastic film pouches market is segmented on the basis of plastic film type, pouches type, treatment type, pouch weight, sealer and application.

- By Plastic Film Type

On the basis of plastic film type, the Global Plastic Film Pouches Market is segmented into Polyethylene, Polypropylene, Poly Vinyl Chloride, Ethylene Vinyl Alcohol (EVOH), and Polyamide. The polyethylene segment dominated the market with the largest revenue share of 36.5% in 2024, driven by its versatility, durability, and cost-effectiveness. It is widely used in food and beverage applications due to its strong moisture barrier and heat-sealing capabilities. Polyethylene films are also compatible with various pouch formats and offer a balance of strength and flexibility for mass-market applications.

The Ethylene Vinyl Alcohol (EVOH) segment is expected to witness the fastest CAGR from 2025 to 2032. Its superior gas and oxygen barrier properties make it ideal for packaging perishable food and pharmaceuticals, helping to extend shelf life. Growing demand for high-performance, recyclable multilayer films further supports EVOH’s market growth, particularly in premium and sustainable packaging segments.

- By Pouches Type

On the basis of pouch type, the market is segmented into Stand-Up, Flat, and Rollstock. The stand-up pouch segment held the largest market revenue share in 2024 at 48.9%, driven by its self-standing design, resealable features, and attractive shelf presence. It is widely used in food, pet food, and personal care sectors, as it offers convenience and strong branding potential. These pouches are also valued for their space efficiency during storage and transportation.

The rollstock segment is expected to witness the fastest CAGR from 2025 to 2032, as it supports high-speed production and is ideal for form-fill-seal machinery. Rollstock films are cost-effective and customizable, making them suitable for large-scale food and healthcare manufacturers aiming to reduce material usage and increase production efficiency. Their flexibility and reduced waste output are also aligned with sustainability goals.

- By Treatment Type

On the basis of treatment type, the market is segmented into Standard, Aseptic, Retort, and Hot-Filled. The standard segment dominated the market in 2024 with a 41.6% revenue share, due to its broad application in dry goods, snacks, and everyday personal care products. Standard pouches offer cost-effective packaging and are compatible with both manual and automated filling lines, making them the default choice for many manufacturers in developing and mature markets alike.

The retort segment is projected to record the fastest growth during the forecast period, driven by rising demand for shelf-stable meals, pet foods, and convenience foods. Retort pouches are heat-resistant and can preserve food without refrigeration, making them increasingly popular for ready-to-eat applications. As consumer demand for portable and long-lasting meals rises, especially in Asia-Pacific, the retort category is expected to grow significantly.

- By Pouch Weight

On the basis of pouch weight, the market is segmented into Below 10 Grams, 10–20 Grams, 50–70 Grams, and More Than 70 Grams. The 10–20 grams segment dominated the market in 2024 with a 34.1% share, due to its widespread use in single-serve applications such as seasonings, personal care sachets, and travel-size items. These lightweight pouches are economical and ideal for sampling, particularly in emerging economies where affordability and portability are key consumer demands.

The 50–70 grams segment is anticipated to witness the highest CAGR from 2025 to 2032, driven by rising demand for portion-controlled ready meals, nutritional supplements, and high-end personal care products. These pouches offer ample space for branding and are increasingly favored for products aimed at urban, on-the-go consumers seeking convenience and premium experiences.

- By Sealer

On the basis of sealer type, the Global Plastic Film Pouches Market is segmented into Direct Heat Sealer and Vacuum Pouch Sealer. The direct heat sealer segment dominated the market in 2024 with a revenue share of 61.3%, driven by its ease of operation, lower cost, and broad usage in sealing polyethylene and laminated films. These sealers are popular in small- to mid-scale packaging operations across food, pharmaceuticals, and personal care industries.

The vacuum pouch sealer segment is forecasted to grow at the fastest CAGR from 2025 to 2032. With increasing demand for vacuum-packed perishable products, particularly meat, seafood, and prepared meals, vacuum sealing is gaining momentum. It enhances shelf life, maintains freshness, and is increasingly used by meal prep services and frozen food manufacturers catering to health-conscious consumers.

- By Application

On the basis of application, the market is segmented into Food, Beverages, Personal Care & Homecare, Healthcare, and Others. The food segment accounted for the largest revenue share in 2024 at 52.7%, due to the high consumption of packaged snacks, frozen foods, dairy, and convenience meals globally. Plastic film pouches are preferred in food packaging for their ability to preserve freshness, lightweight nature, and reduced material usage compared to rigid packaging.

The healthcare segment is projected to witness the fastest CAGR during the forecast period. Rising demand for sterile and tamper-evident packaging in pharmaceuticals, diagnostics, and medical devices is boosting adoption. As the global focus on hygiene, portability, and dosage control grows, healthcare companies are increasingly turning to flexible pouches for both consumer and institutional use.

Global Plastic Film Pouches Market Regional Analysis

- Asia-Pacific dominated the Global Plastic Film Pouches Market with the largest revenue share of 33.1% in 2024, driven by the region’s strong demand for flexible, lightweight, and sustainable packaging solutions across key industries such as food, beverages, and healthcare.

- Consumers and manufacturers in the region are increasingly adopting plastic film pouches due to their convenience, extended shelf life, and superior branding potential. In particular, the rising preference for ready-to-eat meals, frozen foods, and single-serve beverage options is accelerating pouch usage in the food and beverage sectors.

- The growth is further supported by high consumer awareness around sustainability, advancements in packaging technology, and the presence of major FMCG and healthcare companies. Regulatory initiatives encouraging recyclable and low-waste packaging formats have also contributed to the market’s momentum, making North America a key hub for innovation and adoption in plastic film pouch packaging.

U.S. Plastic Film Pouches Market Insight

The U.S. plastic film pouches market captured the largest revenue share of 81% in North America in 2024, driven by growing consumer preference for convenient, sustainable, and lightweight packaging solutions. The food and beverage sector, in particular, is witnessing high adoption of plastic film pouches due to their ability to extend product shelf life and offer resealable options. Additionally, the rise of e-commerce and on-the-go consumption patterns is fueling demand. Manufacturers are increasingly focusing on innovative pouch designs and sustainable materials to meet consumer expectations and regulatory guidelines. Furthermore, advancements in barrier technology and multi-layer films contribute to product freshness, driving widespread adoption in both commercial and retail sectors.

Europe Plastic Film Pouches Market Insight

The Europe plastic film pouches market is projected to grow at a substantial CAGR during the forecast period, driven by stringent environmental regulations and increasing demand for eco-friendly packaging. The food, beverage, and personal care sectors are rapidly shifting towards plastic film pouches due to their recyclability and lower carbon footprint compared to rigid packaging. Urbanization and the rise in single-person households are boosting demand for smaller, convenient pouch formats. Additionally, government initiatives supporting circular economy practices and consumer awareness about sustainable packaging further propel the market growth across residential and commercial applications.

U.K. Plastic Film Pouches Market Insight

The U.K. plastic film pouches market is expected to witness strong growth throughout the forecast period, supported by a rising trend in sustainable packaging and the expansion of the ready-to-eat food segment. Increasing consumer awareness regarding environmental impact is encouraging brands to adopt recyclable and biodegradable film pouches. The food and beverage industry leads adoption, with growing demand for single-serve and on-the-go packaging solutions. Additionally, advancements in pouch sealing technologies and barrier films enhance product safety and shelf life, attracting a broad range of applications from personal care to healthcare sectors.

Germany Plastic Film Pouches Market Insight

The Germany plastic film pouches market is set to expand significantly, driven by the country’s commitment to sustainability and innovation in packaging technology. With strict environmental regulations in place, manufacturers are adopting eco-friendly film materials such as biodegradable polyethylene and recyclable polypropylene. Germany’s strong food processing industry demands high-barrier pouches that maintain product freshness and safety. The personal care and healthcare segments also contribute to market growth, with increasing use of aseptic and retort pouch types. Consumer preference for minimalistic and recyclable packaging further boosts market penetration.

Asia-Pacific Plastic Film Pouches Market Insight

The Asia-Pacific plastic film pouches market is anticipated to grow at the fastest CAGR of 24% during the forecast period, fueled by rapid urbanization, rising disposable incomes, and expanding food and beverage industries in countries like China, India, and Japan. The shift towards convenient, lightweight, and affordable packaging solutions is accelerating demand. Government initiatives to reduce plastic waste and promote sustainable packaging are encouraging the adoption of advanced film technologies and recyclable pouches. Moreover, the region’s manufacturing capabilities and increasing export opportunities contribute to the expansion of plastic film pouch applications across various sectors, including personal care and healthcare.

Japan Plastic Film Pouches Market Insight

Japan’s plastic film pouches market is gaining traction due to the country’s advanced packaging technologies and consumer demand for high-quality, convenience-focused packaging solutions. The food and beverage sector leads the adoption of stand-up and retort pouches, favored for their shelf stability and ease of use. Japan’s aging population also drives demand for user-friendly packaging, including easy-open features and portion-controlled sizes. Additionally, Japan’s focus on sustainability encourages manufacturers to develop recyclable and biodegradable film materials, contributing to the steady growth of the market in both retail and industrial applications.

China Plastic Film Pouches Market Insight

China accounted for the largest market revenue share in Asia-Pacific in 2024, propelled by rapid urbanization, growing middle-class consumers, and increasing demand for packaged foods and beverages. The country’s plastic film pouch market benefits from a strong manufacturing base, enabling competitive pricing and innovation in pouch types and film compositions. The rise of e-commerce and convenience stores fuels demand for flexible, lightweight packaging. Additionally, government policies promoting environmentally friendly packaging and reduction of plastic waste are driving the adoption of recyclable and biodegradable film pouches, further accelerating market growth in China.

Global Plastic Film Pouches Market Share

The Plastic Film Pouches industry is primarily led by well-established companies, including:

• Amcor PLC (Australia)

• Jindal Poly Films Limited (India)

• Mitsubishi Chemical Corporation (Japan)

• Novolex (U.S.)

• RKW Group (Germany)

• Sealed Air Corporation (U.S.)

• Dow Inc. (U.S.)

• Toray Industries, Inc. (Japan)

• Toyobo Co., Ltd. (Japan)

• UFlex Limited (India)

• DuPont (U.S.)

• Berry Global Inc. (U.S.)

• Innovia Films (U.K.)

• Klöckner Pentaplast (Germany)

• SINOPEC SHANGHAI PETROCHEMICAL COMPANY LIMITED (China)

• Treofan Group (Germany)

• Vibac S.p.A. (Italy)

• POLYPLEX (India)

• Inteplast Group (U.S.)

• Exxon Mobil Corporation (U.S.)

What are the Recent Developments in Global Plastic Film Pouches Market?

- In April 2023, Amcor plc, a global leader in packaging solutions, launched an innovative range of recyclable plastic film pouches designed specifically for the food and beverage industry in South Africa. This initiative highlights Amcor’s commitment to sustainable packaging and addresses growing consumer demand for eco-friendly alternatives. By leveraging advanced film technologies and global expertise, Amcor aims to reduce environmental impact while maintaining product freshness, reinforcing its leadership position in the expanding global plastic film pouches market.

- In March 2023, Berry Global Group, Inc., a leading manufacturer of flexible packaging, introduced a new line of aseptic plastic film pouches tailored for the healthcare and personal care sectors. The product’s enhanced barrier properties and lightweight design improve product safety and ease of use, meeting stringent regulatory standards. This launch underscores Berry Global’s focus on innovation and its dedication to providing versatile packaging solutions that meet the evolving needs of sensitive product segments.

- In March 2023, Sealed Air Corporation successfully deployed a state-of-the-art plastic film pouch solution for the Bengaluru Food Processing Park, aimed at extending shelf life and reducing food waste. The initiative utilizes multi-layer barrier films combined with sustainable materials, demonstrating Sealed Air’s commitment to sustainable development and food security. This project reflects the growing importance of advanced plastic film pouch technologies in urban food supply chains and supports safer, more sustainable packaging practices.

- In February 2023, Winpak Ltd., a prominent flexible packaging company, announced a strategic partnership with a leading beverage manufacturer in North America to develop custom stand-up plastic film pouches with enhanced resealability features. This collaboration is designed to improve consumer convenience and product preservation, driving growth in the retail food and beverage sector. The initiative highlights Winpak’s dedication to innovation and customer-centric packaging solutions in the competitive plastic film pouches market.

- In January 2023, Mondi Group, a global packaging and paper company, unveiled its new hot-filled plastic film pouch product line at the PACK EXPO 2023. This range is designed to withstand high-temperature filling processes while ensuring product integrity and consumer safety. Mondi’s launch reflects its commitment to advancing packaging technology, offering manufacturers flexible and durable options that meet the demands of the food and beverage and personal care industries, thus strengthening its presence in the global plastic film pouches market.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Plastic Film Pouches Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Plastic Film Pouches Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Plastic Film Pouches Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.