Global Pleurisy Disease Market

Market Size in USD Billion

USD

2.05 Billion

USD

3.29 Billion

2024

2032

USD

2.05 Billion

USD

3.29 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.05 Billion | |

| USD 3.29 Billion | |

| % | |

|

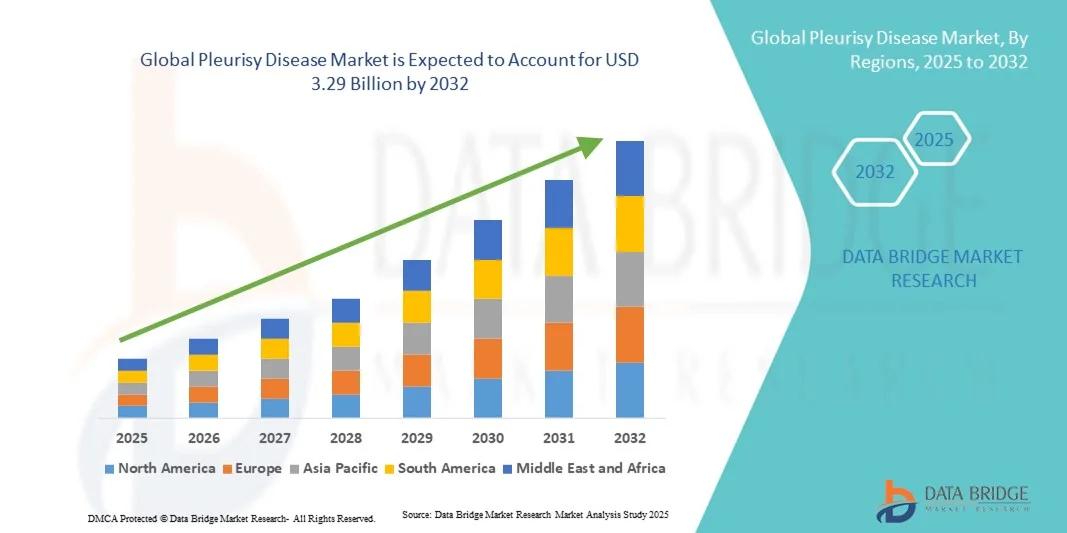

Pleurisy Disease Market Size

- The global pleurisy disease market size was valued at USD 2.05 billion in 2024 and is expected to reach USD 3.29 billion by 2032, at a CAGR of 6.10% during the forecast period

- The market growth is largely fueled by the rising prevalence of respiratory disorders, increasing awareness regarding pleural diseases, and advancements in diagnostic imaging and thoracentesis techniques, which have enhanced early detection and management of pleurisy

- Furthermore, the growing availability of effective treatment options such as anti-inflammatory drugs, antibiotics, and pleural drainage procedures, along with an increasing focus on improving respiratory health infrastructure globally, is accelerating the adoption of pleurisy disease management solutions, thereby significantly boosting the industry's growth

Pleurisy Disease Market Analysis

- Pleurisy disease, characterized by inflammation of the pleura surrounding the lungs, has become an important area of focus in the global respiratory health landscape due to the increasing incidence of lung infections, pneumonia, tuberculosis, and other pulmonary complications. The rising prevalence of chronic respiratory diseases and growing public health awareness are driving the demand for effective diagnosis and treatment options

- The escalating demand for pleurisy disease management solutions is primarily fueled by advancements in medical imaging, improved diagnostic accuracy, and the availability of targeted anti-inflammatory and antibiotic therapies. Increasing hospital admissions for respiratory conditions and the need for specialized care are further supporting market growth

- North America dominated the pleurisy disease market with the largest revenue share of 41.2% in 2024, driven by a well-established healthcare infrastructure, high diagnostic accuracy, and significant investments in respiratory disease research. The U.S. leads the regional market due to advanced treatment options, high disease awareness, and the presence of major pharmaceutical and biotechnology companies

- Asia-Pacific is expected to be the fastest-growing region in the pleurisy disease market during the forecast period, fueled by rising air pollution levels, increasing prevalence of lung infections, and growing healthcare access in emerging economies such as India and China. Government initiatives to strengthen respiratory care and rising investments in hospital infrastructure are further propelling market expansion

- The prescription segment held the largest revenue share of 68.3% in 2024, due to physician-supervised therapy for antibiotics, antifungals, and anticoagulants. Prescription drugs ensure correct dosing and reduce risks of resistance or side effects

Report Scope and Pleurisy Disease Market Segmentation

|

Attributes |

Pleurisy Disease Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Pfizer Inc. (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Pleurisy Disease Market Trends

Advancements in Diagnostic Imaging and AI Integration for Early Detection

- A significant and accelerating trend in the global pleurisy disease market is the integration of artificial intelligence (AI) and advanced imaging technologies such as high-resolution ultrasound, CT scans, and MRI for precise diagnosis and monitoring. These technologies are enhancing diagnostic accuracy and facilitating early detection of pleural inflammation and effusion

- For instance, AI-driven diagnostic tools can assist radiologists in identifying pleural thickening or effusion patterns, improving the accuracy of differential diagnosis between bacterial, viral, and tuberculous pleurisy

- Integration of AI in diagnostic imaging also enables predictive analysis by identifying subtle changes in pleural structures, aiding clinicians in initiating timely treatment interventions

- Furthermore, the adoption of digital pathology and automated image analysis supports efficient interpretation of pleural fluid cytology, minimizing human error and improving diagnostic turnaround time

- Healthcare institutions are increasingly adopting integrated electronic health record (EHR) systems that combine AI analytics with patient imaging data, supporting holistic care management. This trend is revolutionizing clinical workflows and improving patient outcomes

- As precision medicine continues to advance, the global pleurisy market is witnessing a shift towards personalized therapeutic approaches based on molecular profiling and advanced imaging diagnostics

Pleurisy Disease Market Dynamics

Driver

Rising Prevalence of Respiratory Infections and Improved Diagnostic Capabilities

- The increasing prevalence of respiratory infections such as pneumonia, tuberculosis, and viral infections leading to pleural inflammation is a major driver of the pleurisy disease market

- For instance, in March 2024, the World Health Organization (WHO) highlighted that pleural complications are among the most common comorbidities in patients suffering from advanced tuberculosis and bacterial pneumonia, driving diagnostic and treatment demand

- Advancements in diagnostic imaging, including ultrasound-guided thoracentesis and CT imaging, have significantly improved the identification and management of pleurisy

- Growing awareness among healthcare professionals about the importance of early diagnosis and the adoption of standardized diagnostic protocols are further driving market growth

- Moreover, the increasing global healthcare expenditure, coupled with government initiatives to enhance pulmonary care infrastructure, is accelerating the adoption of pleurisy treatment and diagnostic services

- The rising availability of minimally invasive procedures for fluid drainage and pleural biopsy also contributes to the market’s expansion, improving patient recovery outcomes and reducing hospitalization time

Restraint/Challenge

High Treatment Costs and Limited Access to Advanced Diagnostic Facilities in Low-Income Regions

- The high cost of advanced diagnostic procedures, such as MRI and CT-guided pleural biopsies, poses a challenge for patients in developing regions, limiting early detection and timely treatment

- In low-resource settings, limited access to specialized healthcare professionals and diagnostic equipment further restricts proper disease management

- For instance, many rural hospitals in Asia and Africa lack the infrastructure for real-time imaging or laboratory analysis of pleural fluid, leading to delayed or inaccurate diagnoses

- Another major challenge is the risk of misdiagnosis, as pleurisy symptoms often overlap with other thoracic diseases, including pulmonary embolism or malignancy, necessitating complex diagnostic evaluations

- High treatment costs associated with recurrent pleural effusions, combined with long-term antibiotic or anti-tubercular therapy, increase the financial burden on patients and healthcare systems

- In addition, the unavailability of affordable diagnostic reagents and advanced testing kits in emerging economies contributes to delayed diagnosis and underreporting of case

- The absence of standardized global treatment guidelines for pleurisy further complicates therapeutic decisions, leading to variations in patient outcomes

- Shortages of trained pulmonologists and thoracic specialists, particularly in remote regions, exacerbate diagnostic delays and limit access to optimal care

- Moreover, complications arising from untreated pleurisy, such as empyema or pleural fibrosis, often require costly surgical interventions like decortication or pleurectomy, making treatment financially unsustainable for many patients

- The lack of widespread awareness among patients about early pleurisy symptoms leads to delayed medical consultation, increasing the risk of disease progression and hospitalization costs

Pleurisy Disease Market Scope

The market is segmented on the basis of diagnostic type, treatment type, route of administration, end user, mode of purchase, and distribution channel.

- By Diagnostic Type

On the basis of diagnostic type, the Pleurisy Disease market is segmented into thoracentesis, video-assisted thoracic surgery (VATS), imaging devices, blood test, and others. The thoracentesis segment dominated the largest market revenue share of 38.9% in 2024, driven by its widespread use as a standard diagnostic and therapeutic procedure for pleural effusions. Thoracentesis provides rapid symptomatic relief while allowing collection of pleural fluid for analysis, making it the preferred choice among pulmonologists. Its minimal invasiveness, cost-effectiveness, and proven diagnostic accuracy enhance its adoption in hospitals and specialty clinics. The segment benefits from technological improvements in imaging-guided procedures that increase accuracy and safety. High prevalence of bacterial infections, tuberculosis, and cancer-related pleural effusions fuels demand. Thoracentesis is widely taught in medical training programs, supporting its standard-of-care status. Patient outcomes and satisfaction are higher due to quick relief from fluid buildup. Hospitals and diagnostic centers maintain specialized teams for procedure efficiency. Early detection through thoracentesis supports better treatment planning. Continuous research into safer needle and drainage systems further enhances adoption. Clinical guidelines endorse thoracentesis as first-line intervention. Its integration with imaging and laboratory analysis reinforces its dominance.

The video-assisted thoracic surgery (VATS) segment is projected to witness the fastest CAGR of 20.4% from 2025 to 2032, driven by rising adoption of minimally invasive techniques and improved patient outcomes. VATS provides direct visualization of the pleura, allowing precise biopsies and treatment of recurrent or complex effusions. Hospitals are increasingly investing in thoracoscopic equipment due to shorter hospital stays and faster recovery times. Advanced imaging systems and 3D visualization improve surgical accuracy and patient safety. VATS is preferred in cases where thoracentesis is inconclusive or ineffective. Surgeons favor VATS for its ability to combine diagnostic and therapeutic interventions in a single procedure. Awareness programs and training workshops are expanding the skilled workforce. Insurance coverage for minimally invasive procedures is improving in developed markets. VATS is gaining acceptance in emerging economies with urban hospital expansions. Patient preference for less invasive options drives adoption. Research into robotic-assisted thoracic surgery further supports segment growth. Integration with post-operative care programs enhances recovery and reduces complications. Multidisciplinary hospital teams adopt VATS as part of comprehensive pleurisy management.

- By Treatment Type

On the basis of treatment type, the Pleurisy Disease market is segmented into antibiotics, antifungals, blood thinners, nonsteroidal anti-inflammatory drugs (NSAIDs), and others. The antibiotics segment accounted for the largest market revenue share of 42.1% in 2024, driven by the high incidence of bacterial pleurisy and pneumonia-associated infections. Broad-spectrum antibiotics are often prescribed as first-line therapy. Rising bacterial resistance has led to newer combination antibiotic therapies with improved efficacy. Hospitals and specialty clinics rely on antibiotics for both inpatient and outpatient management. Clinical guidelines emphasize timely administration to prevent complications. Patient compliance is supported through oral formulations and supervised therapy. Pharmaceutical companies are focusing on better lung tissue penetration and faster-acting antibiotics. Insurance coverage ensures accessibility in key regions. Early treatment prevents hospitalizations and reduces long-term morbidity. Antibiotics are critical in managing community-acquired pneumonia cases. Awareness campaigns encourage early physician consultation. Repeat treatment and follow-up programs enhance continued demand. Antibiotics remain the backbone of pleurisy disease management globally.

The nonsteroidal anti-inflammatory drugs (NSAIDs) segment is projected to witness the fastest CAGR of 18.7% from 2025 to 2032, driven by their critical role in relieving pleuritic pain and inflammation. NSAIDs are widely prescribed for outpatient care and mild pleurisy cases. Advances in selective COX-2 inhibitors improve safety and reduce gastrointestinal side effects. Growing OTC availability supports patient self-management. Hospitals and clinics increasingly integrate NSAIDs with standard therapy for holistic symptom control. Pharmaceutical innovations provide controlled-release oral formulations for prolonged relief. Public awareness of symptom management promotes early adoption. Insurance and reimbursement policies support broader usage. Urban and semi-urban pharmacies ensure accessibility. Telemedicine prescriptions accelerate adoption in remote regions. Pediatric and adult populations benefit from tailored dosing. Combination therapies with antibiotics enhance patient outcomes. Increasing prevalence of chronic or recurrent pleurisy further drives segment growth.

- By Route of Administration

On the basis of route of administration, the Pleurisy Disease market is segmented into oral and parenteral routes. The oral segment dominated the largest market revenue share of 56.4% in 2024, supported by patient convenience, affordability, and wide availability of oral medications for antibiotics, anti-inflammatories, and antifungals. Oral administration is preferred for outpatient treatment and long-term management. Improved bioavailability and controlled-release formulations enhance efficacy. Widespread adoption in developing regions is supported by generic availability. Hospitals and clinics favor oral therapy for ease of dispensing and patient compliance. Oral drugs reduce hospital visits and improve adherence to treatment plans. Multidrug regimens are easier to manage with oral forms. Pharmaceutical advancements continue to enhance therapeutic effectiveness. Public health initiatives promote safe oral therapy practices. Education campaigns on dosing adherence strengthen market penetration. Oral administration facilitates home-based care, reducing healthcare burden.

The parenteral segment is expected to witness the fastest CAGR of 17.9% from 2025 to 2032, driven by rapid action in severe pleurisy cases requiring intravenous therapy. Injectable antibiotics and anti-inflammatories are essential for hospitalized patients with complicated infections or pleural effusions. Hospitals increasingly rely on parenteral formulations for acute management. Advancements in infusion technology improve safety and reduce side effects. Intensive care and specialized wards favor intravenous therapy for precise dosing. Increasing prevalence of severe pleurisy cases in aging populations supports growth. Combination parenteral therapies enhance clinical outcomes. Telemedicine and outpatient infusion services expand reach. Rapid hospital response protocols include parenteral administration. Continuous training of clinical staff improves procedural efficiency. High-risk cases such as immunocompromised patients benefit from parenteral treatment. Hospital supply chains strengthen availability and timely administration.

- By End User

On the basis of end user, the Pleurisy Disease market is segmented into hospitals, clinics, diagnostic laboratories, and others. The hospital segment accounted for the largest revenue share of 49.8% in 2024, due to availability of advanced diagnostic and therapeutic facilities, including thoracentesis, VATS, and IV therapy. Hospitals serve as primary centers for severe and moderate pleurisy management. Multidisciplinary care ensures optimal patient outcomes. Hospital protocols facilitate integration of diagnostics, treatment, and follow-up care. Urban and tertiary hospitals maintain specialized respiratory departments. Insurance coverage supports hospital-based care. Hospitals provide training programs for clinicians and nurses. Repeat hospital visits for severe cases reinforce revenue. Clinical guidelines prioritize hospital-based interventions. High patient trust and perceived quality of care boost hospital utilization. Research and clinical trials in hospitals further enhance service adoption.

The diagnostic laboratories segment is projected to witness the fastest CAGR of 19.5% from 2025 to 2032, driven by growing demand for pleural fluid analysis, cytology, and microbiological tests. Laboratories increasingly adopt molecular and biomarker-based diagnostics. Rapid turnaround times for lab tests enhance early diagnosis. Collaborative agreements with hospitals and clinics expand service coverage. Private lab networks are expanding in emerging regions. Integration with telemedicine platforms supports remote patient management. Standardization of laboratory practices ensures accuracy and reliability. Investment in high-throughput testing equipment accelerates adoption. Laboratories are crucial for personalized treatment planning. Government and NGO programs support expanded diagnostic access. Growing awareness among patients promotes lab-based testing. Advanced diagnostic platforms improve sensitivity and specificity. Clinical adoption of laboratory testing is increasing across urban and semi-urban regions.

- By Mode of Purchase

On the basis of mode of purchase, the Pleurisy Disease market is segmented into prescription and over-the-counter (OTC) drugs. The prescription segment held the largest revenue share of 68.3% in 2024, due to physician-supervised therapy for antibiotics, antifungals, and anticoagulants. Prescription drugs ensure correct dosing and reduce risks of resistance or side effects. Hospitals and clinics are major prescription sources. Prescription adherence programs improve outcomes. Strong regulatory frameworks support this segment. Telemedicine consultations increase prescription accessibility. Repeat prescriptions maintain steady demand. Clinical guidelines enforce prescription-based therapy for severe cases. Physician confidence and patient trust reinforce prescription dominance. Specialized medications for pleurisy are mostly prescription-only. Hospital pharmacies primarily drive distribution. Evidence-based protocols favor prescription adherence.

The over-the-counter (OTC) segment is expected to witness the fastest CAGR of 16.8% from 2025 to 2032, fueled by increasing availability of NSAIDs and analgesics for symptomatic relief. OTC medications support self-care for mild pleuritic pain. Urban pharmacies and online platforms improve accessibility. Awareness campaigns encourage early pain management. OTC adoption grows in areas with limited healthcare access. Consumer preference for quick relief supports segment growth. Integration with e-commerce platforms enhances convenience. Pediatric and adult-friendly formulations expand market reach. OTC sales benefit from brand recognition and trust. Telepharmacy services enable remote consultation and purchase. Subscription-based delivery models improve adherence. OTC segment growth is driven by rising disposable income and health consciousness.

- By Distribution Channel

On the basis of distribution channel, the Pleurisy Disease market is segmented into hospital pharmacies, retail pharmacies, online pharmacies, and others. The hospital pharmacies segment dominated with a share of 41.5% in 2024, supported by direct procurement of medications for inpatient care, critical therapies, and IV drugs. Hospitals ensure proper storage, dispensing, and patient counseling. Bulk procurement reduces cost per treatment. Integration with clinical workflows enhances adherence and outcomes. Hospitals provide both acute and chronic care for pleurisy patients. Training programs for staff improve safe drug administration. Repeat purchases and long-term treatment regimens maintain demand. Multidisciplinary hospital teams strengthen market presence. Insurance coverage supports hospital pharmacy utilization. Supply chain management ensures timely availability. Standardized procedures maintain quality and safety. Hospitals are primary points of sale for critical medications.

The online pharmacies segment is anticipated to record the fastest CAGR of 21.2% from 2025 to 2032, driven by increasing digitalization and e-commerce adoption in healthcare. Online platforms offer convenience, home delivery, and competitive pricing. Telemedicine integration with online pharmacies supports prescription fulfillment. Growing awareness and trust in digital health platforms expand adoption. Subscription and repeat delivery models improve adherence. Urban and semi-urban consumers increasingly prefer online options. OTC and prescription medications are both accessible online. Logistics improvements ensure timely delivery across regions. Online platforms expand reach in developing markets. Secure payment and data protection strengthen consumer confidence. Customer support and counseling services enhance usability. Partnerships with hospitals and clinics improve prescription verification. Online pharmacies capitalize on convenience, efficiency, and broad product range.

Pleurisy Disease Market Regional Analysis

- North America dominated the pleurisy disease market with the largest revenue share of 41.2% in 2024, driven by a well-established healthcare infrastructure, high diagnostic accuracy, and significant investments in respiratory disease research. The presence of advanced medical facilities and strong reimbursement frameworks enables timely diagnosis and effective treatment of pleurisy

- Continuous research on anti-inflammatory and antimicrobial therapies, coupled with advancements in imaging technologies such as CT scans and ultrasound-guided thoracentesis, further strengthens market growth

- High awareness among both healthcare professionals and patients regarding early detection and management of pleural disorders contributes to superior clinical outcomes

U.S. Pleurisy Disease Market Insight

The U.S. pleurisy disease market captured the largest revenue share within North America in 2024, owing to the country’s advanced healthcare ecosystem, adoption of innovative diagnostic technologies, and availability of targeted anti-inflammatory and antibiotic treatments. Strong government funding for respiratory research programs and the presence of leading pharmaceutical and biotechnology firms actively developing novel therapies drive market expansion. The rising incidence of bacterial and viral lung infections, combined with lifestyle-related respiratory complications, underscores the need for improved pleural care management. Moreover, the integration of digital health tools, telemedicine platforms, and AI-assisted diagnostic imaging is further enhancing patient outcomes and treatment efficiency across healthcare facilities in the U.S.

Europe Pleurisy Disease Market Insight

The Europe pleurisy disease market is projected to register steady growth during the forecast period, driven by improved diagnostic accuracy, expanding hospital networks, and growing awareness of pleural health management. Governments across the region are prioritizing early detection and prevention of respiratory conditions through funding programs and public health initiatives.

Countries such as Germany, France, and the U.K. are witnessing increased clinical adoption of advanced diagnostic procedures like pleural fluid cytology and thoracoscopy. In addition, collaborations between research institutions and pharmaceutical companies are accelerating the development of novel therapeutic agents and minimally invasive surgical interventions for pleural disorders.

U.K. Pleurisy Disease Market Insight

The U.K. pleurisy disease market is expected to grow at a noteworthy CAGR over the forecast period, supported by strong public healthcare infrastructure, high disease awareness, and government-backed initiatives focused on respiratory disease management. Increasing cases of lung infections, coupled with the growing elderly population, are fueling the need for timely and accurate pleurisy diagnosis. The National Health Service (NHS) is also emphasizing advancements in imaging and diagnostic efficiency, leading to enhanced patient outcomes.

Furthermore, ongoing clinical studies targeting pleural inflammation and fibrosis are expected to boost the adoption of innovative therapeutic regimens in the coming years.

Germany Pleurisy Disease Market Insight

The Germany pleurisy disease market is poised for significant growth during the forecast period, driven by the nation’s focus on advanced diagnostic research and investment in respiratory healthcare infrastructure. Germany’s strong presence of medical technology manufacturers and healthcare innovation centers supports the integration of high-precision diagnostic imaging and thoracic care. Moreover, the country’s emphasis on preventive healthcare and digital health adoption is enhancing patient monitoring and long-term disease management.

The increasing incidence of pleural effusion and tuberculosis-related pleurisy further strengthens the market potential for both pharmaceuticals and surgical treatments.

Asia-Pacific Pleurisy Disease Market Insight

The Asia-Pacific pleurisy disease market is anticipated to grow at the fastest CAGR during the forecast period (2025–2032), fueled by rising air pollution levels, increasing prevalence of lung infections, and growing healthcare access in emerging economies such as India and China. Government initiatives to strengthen respiratory care infrastructure, coupled with public health campaigns on tuberculosis and pneumonia awareness, are driving market growth. Rapid urbanization, expanding medical insurance coverage, and the establishment of new diagnostic centers are improving patient accessibility to pleural disease management. Furthermore, pharmaceutical collaborations and the production of affordable generic medications are enabling cost-effective treatment options for patients across the region.

Japan Pleurisy Disease Market Insight

The Japan pleurisy disease market is gaining traction due to the nation’s advanced healthcare system, early disease screening programs, and high public awareness of respiratory illnesses. Rising cases of pneumonia and lung infections among the aging population are increasing demand for specialized pleural care services. The integration of AI-based diagnostic imaging and the use of minimally invasive thoracic procedures are further driving market growth. In addition, the Japanese government’s focus on healthcare innovation and hospital digitalization supports the expansion of pleurisy treatment options in both public and private healthcare facilities.

China Pleurisy Disease Market Insight

The China pleurisy disease market accounted for the largest revenue share within the Asia-Pacific region in 2024, attributed to rapid healthcare modernization, government-led initiatives to combat respiratory diseases, and increased investments in hospital infrastructure. The nation’s expanding middle-class population, growing medical tourism, and availability of cost-effective treatment solutions contribute significantly to market expansion. China’s efforts toward enhancing tuberculosis and pneumonia management programs are improving diagnostic rates and early intervention. Furthermore, the rising adoption of advanced imaging systems, coupled with the presence of numerous domestic pharmaceutical manufacturers, is boosting the country’s dominance in the regional pleurisy disease market.

Pleurisy Disease Market Share

The Pleurisy Disease industry is primarily led by well-established companies, including:

• Pfizer Inc. (U.S.)

• GSK plc (U.K.)

• Novartis AG (Switzerland)

• Sanofi (France)

• AstraZeneca plc (U.K.)

• F. Hoffmann-La Roche Ltd. (Switzerland)

• Bayer AG (Germany)

• Merck & Co., Inc. (U.S.)

• Johnson & Johnson and affiliates (U.S.)

• Boehringer Ingelheim International GmbH (Germany)

• Teva Pharmaceutical Industries Ltd. (Israel)

• AbbVie Inc. (U.S.)

• Cipla Ltd. (India)

• Sun Pharmaceutical Industries Ltd. (India)

• Lupin Limited (India)

Latest Developments in Global Pleurisy Disease Market

- In May 2025, AstraZeneca showcased its latest research on a comprehensive portfolio and pipeline aimed at transforming respiratory diseases at the American Thoracic Society (ATS) 2025 conference. The presentation highlighted novel therapeutic approaches for pleurisy and other pleural disorders, emphasizing early detection and improved patient outcomes

- In February 2025, the U.S. FDA approved EMBLAVEO (aztreonam and avibactam) for the treatment of adults with complicated intra-abdominal infections, including hospital-acquired pneumonia and complicated urinary tract infections. This approval provides an additional option for managing pleural infections with limited or no treatment alternatives

- In December 2024, the FDA released its annual report detailing notable new drug approvals, highlighting actions likely to have a significant impact on patient care and public health, including drugs relevant to pleural and respiratory disease management

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.