Global Plywood Floor Market

Market Size in USD Billion

USD

10.35 Billion

USD

20.69 Billion

2025

2033

USD

10.35 Billion

USD

20.69 Billion

2025

2033

| 2026 - 2033 | |

| USD 10.35 Billion | |

| USD 20.69 Billion | |

| % | |

|

Plywood Floor Market Overview

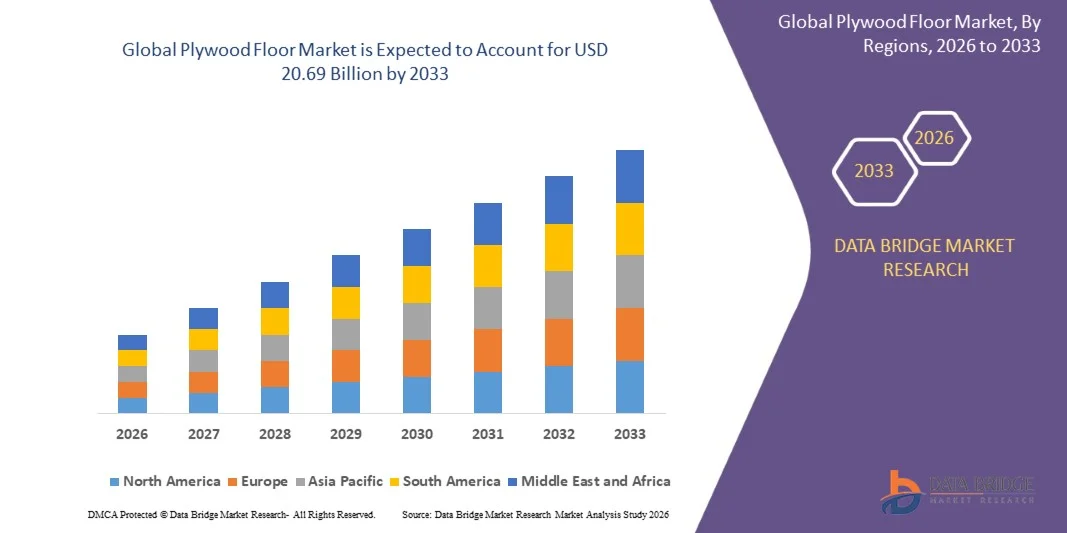

The Plywood Floor Market was valued at USD 10.35 billion in 2025 and is projected to reach USD 20.69 billion by 2033, growing at a CAGR of 9.05% from 2026 to 2033. The Plywood Floor Market is experiencing steady growth driven by rising demand for durable, cost-effective, and aesthetically appealing flooring solutions across residential, commercial, and industrial construction sectors. Increasing urbanization, rapid infrastructure development, and growing renovation activities in both developed and emerging economies are significantly supporting market expansion. In addition, plywood flooring is gaining popularity due to its strength, ease of installation, and versatility compared to traditional solid wood flooring, making it a preferred choice in modern construction projects.

The growing trend toward sustainable and eco-friendly building materials is further accelerating market demand, as plywood flooring is often manufactured using engineered wood that optimizes raw material usage and reduces waste. Rising investments in real estate, hospitality, and retail infrastructure are also contributing to increased adoption of plywood flooring systems. In addition, advancements in surface finishing technologies, water-resistant coatings, and laminated plywood variants are enhancing product durability and expanding application scope across high-moisture and high-traffic environments.

Key Market Trends & Insights

- North America dominated the Plywood Floor Market with the largest revenue share of 34.12% in 2025, supported by strong construction activity, high adoption of engineered wood flooring solutions, and increasing demand for durable and cost-effective flooring materials in residential and commercial projects.

- The Hardwood segment led the market with a 52.46% share in 2025, driven by superior durability, premium appearance, and strong preference in high-end residential and commercial construction projects.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.6% from 2026 to 2033, fueled by rapid urbanization, rising infrastructure development, increasing disposable incomes, and expanding residential construction activities in China, India, and Southeast Asia.

- BWR Grade plywood is the fastest-growing grade segment, projected to register a CAGR of 7.3%, supported by rising demand for moisture-resistant and durable flooring solutions in residential and commercial applications.

- The Residential segment dominates the end-user category with a 48.91% revenue share in 2025, driven by growing housing construction, renovation activities, and increasing preference for aesthetic and durable flooring materials.

- The 8mm–18mm thickness segment accounts for the largest market share of 49.37% in 2025, owing to its balanced strength, durability, and suitability for both residential and commercial flooring applications.

- The Distributors/Retailers channel holds the dominant position with a 61.28% share in 2025, supported by strong retail networks, easy product availability, and increasing consumer preference for offline material inspection before purchase.

- The Fire Resistant Grade segment is the fastest-growing grade category, projected to grow at a CAGR of 6.9%, driven by increasing building safety regulations and rising demand for enhanced fire protection in modern construction projects.

Market Size & Forecast

- Global Market Value (2025): USD 10.35 Billion

- Expected Market Value (2033): USD 20.69 Billion

- Forecast CAGR (2026–2033): 9.05%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Plywood Floor Market Segmentation

|

Attributes |

Plywood Floor Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Mohawk Industries (U.S.) |

|

Market Opportunities |

· Rising Demand for Sustainable and Engineered Wood Flooring Solutions · Expansion of Residential Construction and Urban Housing Projects · Growth in Renovation and Replacement Activities in Developed Economies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Plywood Floor Market Trends

Trend: Growing Demand for Sustainable, Durable, and Engineered Plywood Flooring Solutions

The Plywood Floor Market is witnessing strong growth driven by increasing demand for sustainable, cost-effective, and high-durability flooring solutions across residential and commercial construction projects. Developers and homeowners are increasingly shifting toward engineered wood flooring due to its dimensional stability, moisture resistance, and long lifecycle compared to traditional solid wood. Rising urbanization and expansion of multi-story residential buildings are significantly boosting adoption, particularly in densely populated cities across Asia-Pacific and North America. For instance, according to FAO forestry and construction material trends, engineered wood demand has been consistently rising due to global sustainability initiatives and reduced hardwood availability. In addition, green building certifications such as LEED and BREEAM are encouraging the use of low-emission plywood flooring materials. Manufacturers such as Tarkett and Kronospan are increasingly focusing on eco-certified flooring products with reduced formaldehyde emissions. Growth in renovation activities across Europe and North America is further strengthening demand for aesthetic and easy-to-install flooring solutions.

Plywood Floor Market Dynamics

Key Market Driver: Rising Residential Construction and Urban Infrastructure Development

The rapid expansion of residential construction, smart city projects, and urban infrastructure development is a major driver of the Plywood Floor Market. Increasing housing demand due to urban migration is fueling large-scale apartment and residential complex developments across emerging economies such as India, China, Indonesia, and Brazil. According to World Bank urbanization data, more than 55% of the global population now resides in urban areas, and this is expected to reach nearly 68% by 2050, significantly boosting construction material demand. Plywood flooring is widely preferred due to its affordability, ease of installation, and compatibility with modern interior designs. For example, in India’s Pradhan Mantri Awas Yojana (PMAY) housing scheme, millions of urban housing units have indirectly supported demand for engineered wood and plywood-based flooring materials. In addition, rising disposable income levels are enabling consumers to invest in premium flooring upgrades in residential spaces, further strengthening market growth globally.

Key Restraint/Challenge: Volatility in Raw Material Prices and Supply Chain Constraints

A major challenge in the Plywood Floor Market is the fluctuation in raw material prices, particularly timber and wood-based adhesives. The cost of raw wood is highly dependent on forestry regulations, environmental restrictions, and seasonal availability, which creates pricing instability for manufacturers. For instance, according to industry supply chain reports from 2023–2024, global timber prices experienced fluctuations of over 15–20% in certain regions due to supply disruptions and export restrictions in key producing countries. In addition, logistics challenges, deforestation regulations, and import-export barriers further increase production costs. Smaller manufacturers face difficulties in maintaining stable margins due to rising transportation and compliance costs. In emerging markets, inconsistent supply chains and lack of standardized raw material quality also impact production efficiency and product consistency, limiting broader market adoption.

Key Market Opportunity: Expansion of Green Building Projects and Premium Interior Renovation Demand

The increasing adoption of green building standards and sustainable construction practices presents a significant opportunity for the Plywood Floor Market. Governments across Europe, North America, and Asia-Pacific are promoting energy-efficient and eco-friendly construction materials through regulatory frameworks and incentive programs. For example, the U.S. Green Building Council (USGBC) has reported steady growth in LEED-certified projects globally, driving demand for certified wood flooring materials. In addition, rising consumer interest in premium interior design and home renovation is boosting demand for engineered plywood flooring in urban housing and commercial spaces such as hotels, offices, and retail centers. Companies like Mohawk Industries and Shaw Industries are expanding their engineered wood flooring portfolios to capture this growing demand. Furthermore, advancements in surface coating technologies, water-resistant plywood, and fire-retardant grades are opening new application areas, enhancing long-term growth potential for the market globally.

Plywood Floor Market Scope

The Plywood Floor market is segmented on the basis of wood type, grade, thickness, sales channel, and end-users.

- By Wood Type

On the basis of wood type, the Plywood Floor Market is segmented into Softwood and Hardwood. The Hardwood segment dominated the market with a 52.46% share in 2025, owing to its superior durability, high load-bearing capacity, and premium aesthetic appeal in residential and commercial flooring applications. Strong adoption in luxury housing, commercial interiors, and hospitality projects is further supporting segment leadership. Increasing demand for long-lasting and visually appealing flooring solutions is also driving growth. Hardwood plywood offers better resistance to wear and moisture, making it suitable for high-traffic areas. Rising urban construction activities across developed economies are further strengthening demand. Manufacturers are focusing on engineered hardwood solutions to improve sustainability and performance. Softwood plywood is widely used in cost-sensitive projects due to its affordability and ease of availability. It is gaining traction in mass housing and budget construction projects. Growing renovation activities are also supporting Softwood adoption. However, Hardwood remains the preferred choice in premium applications. Overall, Hardwood continues to dominate due to its superior quality and performance characteristics.

The Softwood segment is projected to register the fastest growth at a CAGR of 6.8% from 2026 to 2033, driven by rising demand for cost-effective flooring materials in emerging economies. Increasing residential construction in Asia-Pacific and Latin America is boosting adoption. Rapid urbanization and affordable housing initiatives are further supporting segment expansion. Manufacturers are improving softwood treatment technologies to enhance durability and resistance. Expanding low-cost housing projects are increasing usage in budget segments. Growing preference for lightweight and easy-to-install flooring materials is also supporting demand. Infrastructure development projects are further driving consumption. Availability of raw materials at lower cost is enhancing market penetration. Rising renovation activities in developing regions are accelerating adoption. Strong demand from price-sensitive consumers is fueling growth. Overall, Softwood is emerging as the fastest-growing segment due to affordability and scalability.

- By Grade

On the basis of grade, the market is segmented into MR Grade, BWR Grade, Fire Resistant Grade, BWP Grade, and Structural Grade. The BWR Grade segment dominated the market with a 34.18% share in 2025, owing to its strong water resistance, durability, and suitability for residential and semi-commercial flooring applications. High demand in humid and coastal regions is a key growth driver. Increasing use in modern housing projects is further strengthening segment leadership. BWR plywood offers a balance between cost and performance, making it widely preferred. Growing urban residential construction is significantly boosting demand. Manufacturers are enhancing moisture-resistant coatings to improve product life. Rising renovation activities are also supporting adoption. Structural Grade plywood is widely used in heavy-duty applications such as industrial flooring and infrastructure projects. Fire Resistant Grade is gaining traction due to increasing building safety regulations. MR Grade is preferred in dry indoor environments due to affordability. BWP Grade is used in premium waterproof applications. Overall, BWR Grade remains the most widely adopted category due to balanced performance and cost efficiency.

The Fire Resistant Grade segment is projected to register the fastest growth at a CAGR of 7.3% from 2026 to 2033, driven by increasing enforcement of fire safety regulations in modern construction. Rising demand from commercial buildings, hospitals, and high-rise infrastructure is supporting adoption. Governments across Europe, North America, and Asia-Pacific are mandating fire-safe construction materials. Growing awareness regarding building safety standards is further accelerating demand. Fire-resistant plywood offers enhanced protection and reduced risk in emergencies. Increasing investments in smart city infrastructure are boosting usage. Manufacturers are innovating with advanced fire-retardant chemical treatments. Rising insurance and compliance requirements are also supporting adoption. Expansion of commercial real estate is further driving demand. Strong regulatory push is accelerating market penetration. Overall, Fire Resistant Grade is emerging as the fastest-growing segment due to safety compliance needs.

- By Thickness

On the basis of thickness, the market is segmented into < 8mm, 8mm – 18mm, and > 18mm plywood flooring. The 8mm–18mm segment dominated the market with a 49.37% share in 2025, owing to its balanced strength, durability, and versatility in residential and commercial flooring applications. High demand in modern construction projects is a key growth driver. This thickness range offers optimal load-bearing capacity and ease of installation. Increasing use in urban housing and commercial interiors is supporting segment leadership. It is widely preferred for both new construction and renovation projects. Manufacturers are focusing on improving structural stability and moisture resistance. Rising infrastructure development is further boosting adoption. The < 8mm segment is mainly used in lightweight applications and decorative flooring. The > 18mm segment is used in heavy-duty industrial and commercial flooring. Growing construction activities in emerging economies are increasing overall demand. However, 8mm–18mm remains the most widely used category due to its versatility.

The > 18mm segment is projected to register the fastest growth at a CAGR of 6.9% from 2026 to 2033, driven by rising demand for high-strength flooring in industrial and commercial applications. Increasing infrastructure projects such as warehouses, factories, and logistics centers are boosting adoption. Growing need for high load-bearing capacity flooring is supporting segment expansion. Rising investments in commercial real estate are further driving demand. Enhanced durability and long lifecycle performance are key advantages. Manufacturers are improving thickness optimization for heavy-duty use. Expansion of industrialization in emerging markets is accelerating growth. Strong demand from construction contractors is supporting adoption. Increasing focus on long-term flooring solutions is further boosting usage. Overall, industrial and infrastructure growth is fueling this segment’s rapid expansion.

- By Sales Channel

On the basis of sales channel, the market is segmented into Direct Sales and Distributors/Retailers. The Distributors/Retailers segment dominated the market with a 61.28% share in 2025, owing to strong distribution networks and easy product availability across urban and semi-urban regions. Retail channels allow customers to physically evaluate product quality before purchase. Expanding construction supply chains are further supporting segment leadership. Increasing demand from small contractors and homeowners is boosting retail sales. Manufacturers prefer distributors for wider market reach and cost efficiency. Strong presence of hardware stores and building material outlets is enhancing accessibility. Rising renovation activities are further supporting retail dominance. Direct Sales is mainly used for bulk procurement in large construction projects. Growing infrastructure development is increasing direct procurement from manufacturers. However, retailers remain the dominant channel due to mass-market accessibility. E-commerce platforms are also gradually contributing to retail growth. Overall, Distributors/Retailers continue to lead due to strong market penetration.

The Direct Sales segment is projected to register the fastest growth at a CAGR of 6.7% from 2026 to 2033, driven by increasing large-scale construction and infrastructure projects. Growing demand from real estate developers and contractors is supporting adoption. Direct procurement ensures cost efficiency and bulk pricing advantages. Rising urban infrastructure projects are boosting institutional purchases. Manufacturers are strengthening B2B sales channels for better margins. Increasing smart city and housing projects are further accelerating growth. Digital procurement platforms are improving direct sales efficiency. Strong demand from commercial builders is supporting expansion. Reduced intermediary costs are encouraging direct transactions. Overall, infrastructure development is fueling rapid growth in this segment.

- By End-Users

On the basis of end-users, the market is segmented into Commercial, Residential, New Construction, and Replacement. The Residential segment dominated the market with a 48.91% share in 2025, owing to strong housing demand and increasing urban population growth. Rising preference for aesthetic and durable flooring solutions is a key driver. Expanding apartment and housing projects are boosting adoption. Increasing disposable income is encouraging home renovation activities. Growing nuclear families are further supporting residential flooring demand. Manufacturers are focusing on stylish and durable plywood flooring solutions. Strong urbanization trends are reinforcing segment leadership. The New Construction segment is widely used in large infrastructure and housing projects. Replacement demand is increasing due to renovation of aging buildings. Commercial applications are growing in offices, retail, and hospitality sectors. However, residential usage remains the largest contributor due to mass housing demand.

The Commercial segment is projected to register the fastest growth at a CAGR of 7.2% from 2026 to 2033, driven by rapid expansion of offices, retail spaces, and hospitality infrastructure. Increasing investment in commercial real estate is boosting flooring demand. Growing focus on aesthetic and durable interiors is supporting adoption. Rising tourism and hospitality development is further accelerating growth. Expansion of corporate infrastructure in emerging economies is driving demand. Manufacturers are offering premium-grade plywood flooring for commercial applications. Increasing renovation of commercial buildings is supporting replacement demand. Strong urban economic development is boosting usage. Demand for long-lasting flooring solutions is increasing in high-traffic areas. Overall, commercial expansion is fueling strong growth in this segment.

Plywood Floor Market Regional Analysis

North America dominated the Plywood Floor market and accounted for the largest revenue share of 34.12% in 2025, supported by strong construction activity, high adoption of engineered wood flooring solutions, and increasing demand for durable and cost-effective flooring materials in residential and commercial projects. The region also benefits from rapid urban renovation trends, strong presence of leading flooring manufacturers, and growing preference for sustainable and low-maintenance flooring materials. Rising investments in residential housing projects and commercial infrastructure further strengthen North America’s leadership position in the global market. Increasing focus on premium interior design and modern flooring aesthetics continues to support market expansion across the region.

U.S. Plywood Floor Market Insight

The U.S. Plywood Floor market is witnessing strong growth due to rising residential construction activities, home renovation trends, and expanding commercial infrastructure development. Increasing demand for engineered wood flooring in apartments, offices, and retail spaces is driving market expansion. The country’s strong real estate sector, coupled with high consumer preference for durable and aesthetic flooring solutions, is further boosting adoption. Additionally, growing awareness regarding sustainable building materials and green construction practices is accelerating demand for eco-friendly plywood flooring products.

Europe Plywood Floor Market Insight

The Europe Plywood Floor market remains a major contributor to global revenue, driven by stringent environmental regulations, strong construction standards, and high adoption of engineered wood flooring. Increasing focus on sustainable and certified wood products is supporting market expansion across residential and commercial sectors. The region also benefits from strong renovation and remodeling activities, particularly in aging infrastructure. Rising demand for premium interior finishes in commercial buildings, hotels, and offices is further enhancing market growth across Europe.

U.K. Plywood Floor Market Insight

The U.K. Plywood Floor market is experiencing steady growth, supported by increasing housing renovation activities, rising demand for modern interior design solutions, and strong adoption of engineered wood flooring. Growing investments in residential redevelopment projects and commercial real estate upgrades are further driving demand. Additionally, consumer preference for cost-effective yet durable flooring solutions is supporting market expansion. The rising trend of sustainable construction practices is also contributing to increased adoption of plywood flooring products in the U.K.

Germany Plywood Floor Market Insight

The Germany Plywood Floor market is expanding steadily due to strong industrial base, advanced construction technologies, and increasing demand for high-quality engineered flooring solutions. The country’s focus on energy-efficient and sustainable building materials is supporting market growth. Rising renovation of residential properties and modernization of commercial infrastructure are further boosting demand. Additionally, Germany’s emphasis on durability, precision engineering, and eco-friendly construction standards is strengthening plywood floor adoption.

Asia-Pacific Plywood Floor Market Insight

The Asia-Pacific Plywood Floor market is expected to witness rapid growth, driven by increasing urbanization, expanding residential construction, and rising infrastructure development across countries such as China, India, and Southeast Asia. Growing middle-class population, rising disposable incomes, and increasing demand for affordable housing are supporting market expansion. Additionally, strong growth in commercial construction projects and rapid urban migration are further accelerating plywood flooring adoption across the region.

Japan Plywood Floor Market Insight

The Japan Plywood Floor market is witnessing consistent growth due to rising residential renovation activities, compact housing trends, and strong demand for durable and space-efficient flooring solutions. Increasing preference for high-quality interior finishes in urban homes is driving adoption. The country’s focus on earthquake-resistant and lightweight construction materials is also supporting plywood flooring demand. Additionally, technological advancements in engineered wood products are further strengthening market growth in Japan.

China Plywood Floor Market Insight

The China Plywood Floor market is growing rapidly, driven by large-scale urbanization, massive residential construction projects, and expanding commercial infrastructure development. Strong government support for housing development and urban renewal projects is significantly boosting demand. Increasing adoption of engineered wood flooring in modern apartments and commercial spaces is further accelerating market growth. Additionally, rising environmental awareness and demand for cost-effective construction materials are positioning China as one of the fastest-growing markets globally.

Plywood Floor Market Share

The Plywood Floor industry is primarily led by well-established companies, including:

- Mohawk Industries (U.S.)

- Shaw Industries Group, Inc. (U.S.)

- Mannington Mills, Inc. (U.S.)

- Armstrong Flooring, Inc. (U.S.)

- Gerflor Group (France)

- Forbo Flooring Systems (Switzerland)

- Tarkett S.A. (France)

- Kährs Group (Sweden)

- Bauwerk Group (Switzerland)

- Unilin Technologies (Belgium)

- Boen (Norway)

- Greenply Industries Limited (India)

- Century Plyboards (India) Ltd. (India)

- Shandong Shengxiang Wood Industry Co., Ltd. (China)

- Anhui Conch Cement Company (China)

- Välinge Innovation AB (Sweden)

- Plycem USA LLC (U.S.)

- Ekornes ASA (Norway)

- Haro (Hamberger Flooring GmbH & Co. KG) (Germany)

- BerryAlloc (Belgium)

- Kronospan Limited (Austria)

- EGGER Group (Austria)

- West Fraser Timber Co. Ltd. (Canada)

- Interfor Corporation (Canada)

- Weyerhaeuser Company (U.S.)

- Roseburg Forest Products (U.S.)

- Georgia-Pacific LLC (U.S.)

- Sonae Arauco (Portugal)

- Swiss Krono Group (Switzerland)

- Metsa Group (Finland)

- UPM-Kymmene Corporation (Finland)

- Daiken Corporation (Japan)

- Sumitomo Forestry Co., Ltd. (Japan)

- Jaya Tiasa Holdings Berhad (Malaysia)

- Greenlam Industries Limited (India)

Latest Developments in Plywood Floor Market

- In March 2021, Mohawk Industries (U.S.), one of the world’s largest flooring manufacturers, expanded its engineered wood flooring portfolio under its “TecWood” and “SolidTech” ranges, focusing on enhanced water resistance and scratch durability. The company emphasized the growing demand for hybrid wood flooring solutions suitable for high-moisture residential environments such as kitchens and basements. This expansion aligned with increasing consumer preference for durable and low-maintenance flooring materials in North America and Europe, strengthening Mohawk’s position in the global wood flooring market

- In June 2022, Tarkett (France), a leading global flooring solutions provider, announced increased investment in circular economy-based flooring production, including engineered wood and plywood-core flooring systems. The initiative focused on reducing carbon footprint through recycled wood content and low-emission adhesives. Tarkett’s sustainability-driven approach supported growing regulatory pressure in Europe for eco-certified construction materials, reinforcing demand for sustainable plywood-based flooring across commercial and residential sectors

- In February 2023, Shaw Industries (U.S.), a Berkshire Hathaway company, launched upgraded engineered hardwood flooring collections featuring improved moisture resistance and digital surface technology. The new flooring systems were designed to enhance dimensional stability using advanced plywood core structures. This development reflected rising demand for premium engineered wood flooring in residential renovation projects across the U.S., particularly in high-traffic urban housing environments

- In September 2023, Kährs Group (Sweden), a major European wood flooring manufacturer, introduced next-generation engineered wood flooring with enhanced waterproof and wear-resistant properties. The product line incorporated multi-layer plywood core construction and advanced surface sealing technology. This launch was aligned with increasing demand in Europe for sustainable, long-life flooring solutions in both residential and hospitality sectors, especially in Germany, Sweden, and the U.K.

- In January 2024, Mohawk Industries (U.S.) expanded its production capacity for engineered wood flooring in North America to meet rising demand driven by housing renovation and new residential construction. The expansion included improved plywood-based core structures and digital manufacturing upgrades to enhance production efficiency. This move came amid strong growth in the U.S. housing market and increasing consumer shift toward engineered flooring over solid hardwood due to cost and durability advantages

- In August 2024, Kronospan (Austria), a major wood-based panel manufacturer, announced advancements in high-density plywood and engineered wood substrates used in flooring applications. The company focused on improving moisture resistance and structural strength for use in flooring and interior construction. This development supported increasing global demand for engineered plywood flooring in modular construction and prefabricated housing systems

- In March 2025, Unilin Technologies (Belgium), known for flooring innovation, introduced next-generation click-lock engineered wood flooring systems designed for faster installation and improved durability. The innovation leveraged advanced plywood core technology combined with enhanced locking mechanisms. This launch addressed growing demand for DIY-friendly flooring solutions in Europe and North America, particularly in the renovation and remodeling segment

- In October 2025, global flooring manufacturers collectively accelerated adoption of low-emission and formaldehyde-free plywood flooring materials in response to stricter environmental regulations in Europe and North America. Companies such as Tarkett, Mohawk, and Shaw Industries expanded eco-certified product lines to comply with green building standards such as LEED and BREEAM. This shift reflects strong market movement toward sustainable construction materials and increased demand for environmentally safe plywood-based flooring systems

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.