Global Pneumococcal Vaccine Market

Market Size in USD Billion

USD

9.28 Billion

USD

14.24 Billion

2025

2033

USD

9.28 Billion

USD

14.24 Billion

2025

2033

| 2026 - 2033 | |

| USD 9.28 Billion | |

| USD 14.24 Billion | |

| % | |

|

Pneumococcal Vaccine Market Size

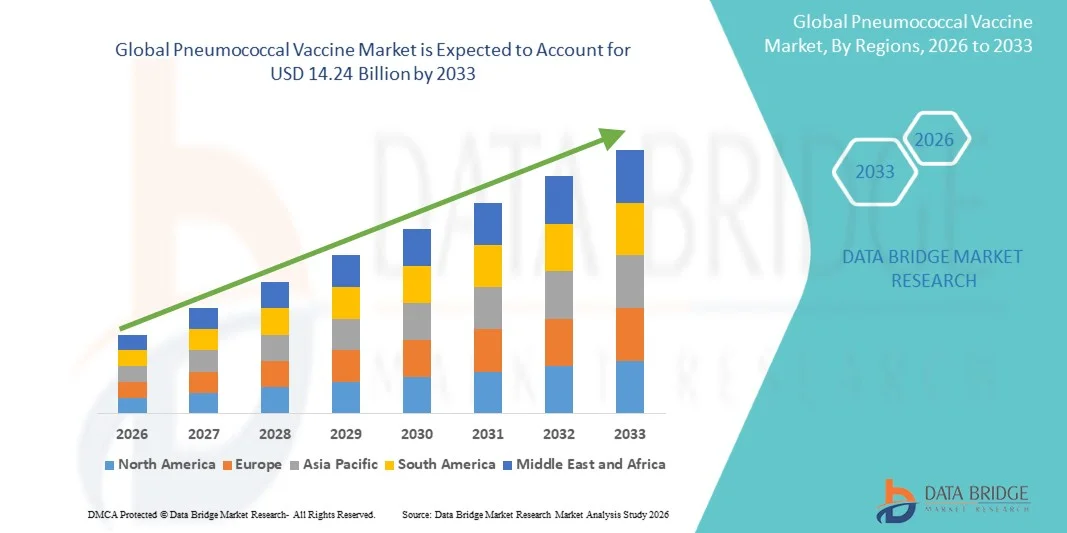

- The global pneumococcal vaccine market size was valued at USD 9.28 billion in 2025 and is expected to reach USD 14.24 billion by 2033, at a CAGR of 5.5% during the forecast period

- The market growth is largely driven by increasing prevalence of pneumococcal diseases, growing awareness regarding vaccination, and expanding immunization programs across both developed and emerging economies

- Furthermore, ongoing research and development for next-generation vaccines, along with government initiatives and public-private partnerships to enhance vaccine accessibility, are reinforcing the adoption of pneumococcal vaccines. These combined factors are propelling market demand, thereby significantly contributing to the industry's growth

Pneumococcal Vaccine Market Analysis

- Pneumococcal vaccines, providing protection against infections caused by Streptococcus pneumoniae, are becoming essential components of public health immunization programs worldwide, particularly for children, the elderly, and high-risk populations, due to their proven efficacy in preventing pneumonia, meningitis, and sepsis

- The rising demand for pneumococcal vaccines is primarily driven by increasing awareness about vaccine-preventable diseases, expanding national immunization programs, and growing government and NGO initiatives to improve vaccine coverage in both developed and developing countries

- North America dominated the pneumococcal vaccine market with the largest revenue share of 40.9% in 2025, supported by strong healthcare infrastructure, widespread awareness campaigns, and high vaccination rates, with the U.S. witnessing significant adoption through pediatric and adult immunization schedules and continuous innovation in conjugate vaccines by leading pharmaceutical companies

- Asia-Pacific is expected to be the fastest growing region in the pneumococcal vaccine market during the forecast period, driven by rising government vaccination initiatives, increasing healthcare accessibility, and growing awareness about preventive healthcare in emerging economies such as India and China

- Pneumococcal Conjugate Vaccine segment dominated the pneumococcal vaccine market with a market share of 61.5% in 2025, owing to their superior immunogenicity, broader serotype coverage, and inclusion in routine childhood immunization programs globally

Report Scope and Pneumococcal Vaccine Market Segmentation

|

Attributes |

Pneumococcal Vaccine Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Pneumococcal Vaccine Market Trends

“Increasing Adoption of Next-Generation Conjugate Vaccines”

- A significant and accelerating trend in the global pneumococcal vaccine market is the growing adoption of next-generation conjugate vaccines that cover more pneumococcal serotypes, improving protection across diverse populations

- For instance, the introduction of 20-valent pneumococcal conjugate vaccines by Pfizer allows broader immunization coverage, reducing the incidence of invasive pneumococcal diseases among children and older adults

- These advanced vaccines offer enhanced immunogenicity, longer-lasting immunity, and better protection against antibiotic-resistant strains, making them increasingly preferred in national immunization programs

- The incorporation of these vaccines into routine pediatric and adult immunization schedules is streamlining preventive healthcare strategies, reducing hospitalizations, and improving overall population health outcomes

- This trend towards more effective and broad-spectrum pneumococcal vaccines is reshaping public health policies and driving demand for vaccines that provide comprehensive protection against evolving pneumococcal strains

- The demand for next-generation conjugate vaccines is growing rapidly across both developed and developing regions, as governments and healthcare providers prioritize reducing the burden of pneumococcal diseases

- Advances in combination vaccines that integrate pneumococcal protection with other routine immunizations are enhancing patient compliance and expanding market opportunities

Pneumococcal Vaccine Market Dynamics

Driver

“Rising Incidence of Pneumococcal Diseases and Expanded Immunization Programs”

- The increasing prevalence of pneumococcal infections, especially among children under five, the elderly, and immunocompromised individuals, is a key driver boosting demand for vaccines globally

- For instance, WHO and CDC reports highlight high rates of pneumonia and meningitis in low- and middle-income countries, prompting expanded vaccination campaigns to prevent disease outbreaks

- Growing awareness among healthcare providers and parents regarding the severe consequences of pneumococcal infections is driving uptake of vaccines in routine immunization programs

- Furthermore, government and non-government initiatives supporting universal immunization schedules are making vaccines more accessible, particularly in underserved regions

- Continuous efforts to integrate pneumococcal vaccines into national immunization strategies and school-based programs are enhancing coverage rates and reducing disease burden

- Increasing funding from global health organizations, such as Gavi, the Vaccine Alliance, is facilitating procurement and distribution in developing regions, strengthening market growth

- Ongoing research to develop vaccines suitable for older adults and high-risk populations is expanding target demographics, creating new opportunities for market expansion

Restraint/Challenge

“High Vaccine Cost and Cold Chain Infrastructure Limitations”

- The relatively high cost of pneumococcal vaccines, especially next-generation conjugate formulations, poses a significant challenge to adoption in price-sensitive markets

- For instance, limited budgets in certain developing countries restrict large-scale procurement, delaying nationwide vaccination programs despite growing disease prevalence

- In addition, pneumococcal vaccines require strict cold chain management and temperature-controlled storage, which can be difficult to maintain in regions with inadequate infrastructure

- The complexity of logistics, including transportation and storage of vaccines in remote areas, can lead to reduced vaccine efficacy or wastage, hampering immunization efforts

- Overcoming these challenges through government subsidies, public-private partnerships, and investments in cold chain infrastructure will be critical for expanding global vaccine coverage

- Vaccine hesitancy due to misinformation and fear of side effects can reduce immunization rates, limiting market penetration in certain communities

- Regulatory hurdles for approval of new conjugate vaccines in multiple countries can delay market entry and slow adoption of innovative formulations

Pneumococcal Vaccine Market Scope

The market is segmented on the basis of vaccine type, product type, route of administration, end users, and distribution channel.

- By Vaccine Type

On the basis of vaccine type, the pneumococcal vaccine market is segmented into pneumococcal conjugate vaccines (PCV) and pneumococcal polysaccharide vaccines (PPSV). The pneumococcal conjugate vaccine segment dominated the market with the largest revenue share of 61.5% in 2025, driven by its superior immunogenicity, broader serotype coverage, and inclusion in routine childhood immunization programs globally. PCVs are preferred for pediatric populations and high-risk adults because they provide longer-lasting immunity and better protection against invasive pneumococcal diseases. In addition, government immunization initiatives in developed and developing countries are strongly promoting PCV adoption, increasing demand. The segment’s dominance is further reinforced by the availability of multiple vaccine options such as Prevnar 13 and Synflorix, which are widely recommended by healthcare authorities. PCVs are also supported by extensive clinical trial data and healthcare provider trust, making them the first choice in public health programs. The ongoing development of next-generation PCVs with higher serotype coverage continues to drive growth in this segment.

The pneumococcal polysaccharide vaccine segment is expected to witness the fastest growth rate during 2026–2033 due to its suitability for older adults and immunocompromised populations who require protection against a wide range of pneumococcal serotypes. PPSVs are often used as a booster following conjugate vaccine administration, expanding their adoption among high-risk populations. Rising awareness of adult immunization programs and government recommendations for PPSV vaccination in seniors are fueling growth. Increasing healthcare infrastructure and awareness campaigns in emerging economies also contribute to the rising uptake of PPSVs in non-pediatric populations. For instance, Pneumovax 23 is widely recommended for adults over 65 and patients with chronic illnesses. The growing aging population globally provides a larger target demographic for PPSVs, supporting sustained market growth.

- By Product Type

On the basis of product type, the market is segmented into Prevnar 13, Synflorix, Pneumovax 23, and others. Prevnar 13 dominated the market with the largest revenue share in 2025 due to its wide serotype coverage and established presence in national immunization schedules. It is heavily prescribed for infants, children, and adults at risk of pneumococcal infections, contributing to consistent market demand. Healthcare providers prefer Prevnar 13 for its strong efficacy data and robust clinical trial support. Brand recognition and availability through public health programs further strengthen its dominance in the market. Prevnar 13 also benefits from government funding and inclusion in routine pediatric programs, ensuring high adoption rates. Continuous research and reformulation efforts maintain its relevance and competitive advantage.

Pneumovax 23 is expected to witness the fastest growth during 2026–2033 as it is primarily targeted toward older adults and individuals with chronic conditions. Pneumovax 23 covers more serotypes than most conjugate vaccines, making it an essential option for adult immunization. Increasing aging populations in North America, Europe, and Asia-Pacific are driving adoption. Government and private healthcare campaigns recommending Pneumovax 23 for seniors and high-risk groups further contribute to market expansion. For instance, the CDC recommends Pneumovax 23 for adults aged 65 and older as part of routine immunization schedules. The growing prevalence of chronic diseases such as diabetes and heart disease also increases the target population for Pneumovax 23, supporting rapid segment growth.

- By Route of Administration

On the basis of route of administration, the market is segmented into intravenous, intramuscular, and subcutaneous. The intramuscular segment dominated the market in 2025, supported by its ease of administration in hospitals, clinics, and vaccination centers. Most pediatric and adult pneumococcal vaccines are administered intramuscularly, making it the preferred route in immunization programs. This method ensures optimal vaccine efficacy and patient compliance, particularly in large-scale vaccination drives. For instance, Prevnar 13 and Synflorix are both administered intramuscularly in routine programs. Intramuscular injections are also compatible with combination vaccines, further simplifying immunization schedules. The availability of trained healthcare personnel in most hospitals supports intramuscular administration at scale.

The subcutaneous segment is anticipated to witness the fastest growth during 2026–2033 due to its suitability for specific adult and high-risk populations. Subcutaneous administration allows flexibility in healthcare settings where intramuscular injection may not be feasible and is sometimes preferred for booster doses. For instance, Pneumovax 23 can be administered subcutaneously in certain adult vaccination protocols. Rising adoption in specialty clinics and increased awareness of alternative administration routes are contributing to its growth. This route also reduces injection site discomfort in some patients, enhancing compliance. Expanding vaccination programs in emerging economies are likely to adopt subcutaneous administration to reach broader populations efficiently.

- By End Users

On the basis of end users, the market is segmented into hospitals, specialty clinics, and others. Hospitals dominated the market in 2025, accounting for the largest revenue share, as they are primary vaccination centers for both routine immunizations and outbreak control. Hospitals have established cold chain infrastructure, trained personnel, and access to large patient volumes, facilitating high vaccine coverage. Large-scale government vaccination programs and hospital-based immunization campaigns further support market dominance. For instance, public hospitals in the U.S. and Europe provide free or subsidized pneumococcal vaccines to eligible populations. Hospitals also serve as key vaccination hubs during seasonal campaigns, increasing throughput. The strong presence of pediatric and adult immunization programs within hospitals maintains steady demand.

Specialty clinics are expected to witness the fastest growth from 2026 to 2033, driven by increased adult vaccination awareness and targeted campaigns for high-risk populations. Clinics provide focused care for seniors, immunocompromised individuals, and patients with chronic conditions, creating a growing demand for pneumococcal vaccines. For instance, private geriatrics and immunology clinics are increasingly offering Pneumovax 23 and booster doses. Expansion of private healthcare and specialized vaccination centers in urban and semi-urban regions is accelerating market penetration in this segment. Clinics also offer flexible scheduling and personalized follow-ups, increasing patient compliance. Collaboration with NGOs and insurance providers is further boosting adoption at specialty clinics.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into distribution partner companies, non-governmental organizations (NGOs), and others. Distribution partner companies dominated the market in 2025, due to their established networks for vaccine delivery, partnerships with hospitals, and logistics capabilities ensuring timely distribution of vaccines. They play a critical role in ensuring vaccine availability across developed and emerging economies, supporting both public and private healthcare providers. For instance, Pfizer and GSK work closely with distribution partners to supply vaccines globally. Efficient cold chain management and supply reliability strengthen this segment’s dominance. Strategic alliances with governments for public immunization programs further enhance market penetration. The robust distribution networks enable prompt response to outbreak situations, maintaining consistent demand.

NGOs are expected to witness the fastest growth during 2026–2033, as they facilitate vaccine distribution in rural and underserved regions where healthcare access is limited. Global health initiatives by organizations such as Gavi and UNICEF are expanding coverage and awareness, particularly in low- and middle-income countries. For instance, NGO-led campaigns in sub-Saharan Africa and Southeast Asia have successfully increased vaccine adoption among children. Increasing partnerships between NGOs, governments, and manufacturers are accelerating vaccine accessibility and adoption, driving growth in this segment. NGOs also support community education programs, which improve acceptance and compliance. Their involvement is critical in reaching remote populations and boosting overall market expansion.

Pneumococcal Vaccine Market Regional Analysis

- North America dominated the pneumococcal vaccine market with the largest revenue share of 40.9% in 2025, supported by strong healthcare infrastructure, widespread awareness campaigns, and high vaccination rates

- Consumers and healthcare providers in the region highly value the protection offered by pneumococcal vaccines against pneumonia, meningitis, and invasive pneumococcal diseases, particularly among children, older adults, and high-risk populations

- This widespread adoption is further supported by strong government initiatives, inclusion of vaccines in routine immunization schedules, and extensive public-private partnerships, establishing pneumococcal vaccines as a critical component of preventive healthcare across both pediatric and adult populations

U.S. Pneumococcal Vaccine Market Insight

The U.S. pneumococcal vaccine market captured the largest revenue share of 82% in 2025 within North America, fueled by well-established immunization programs and high awareness of vaccine-preventable diseases. Consumers and healthcare providers are increasingly prioritizing protection against pneumonia, meningitis, and invasive pneumococcal infections. The growing emphasis on pediatric and adult vaccination schedules, combined with strong recommendations from the CDC and other healthcare authorities, further propels the vaccine industry. Moreover, government initiatives, insurance coverage, and public-private partnerships are significantly contributing to market expansion. The increasing prevalence of chronic diseases and aging population also drives higher vaccine uptake across adults and seniors.

Europe Pneumococcal Vaccine Market Insight

The Europe pneumococcal vaccine market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by government immunization mandates and growing awareness of pneumococcal diseases. Increasing urbanization and the rising prevalence of at-risk populations, such as children and the elderly, are fostering vaccine adoption. European consumers and healthcare providers value vaccines for their proven efficacy, safety, and inclusion in national immunization schedules. The region is experiencing significant growth across public hospitals, private clinics, and specialty centers, with pneumococcal vaccines being increasingly incorporated into routine healthcare programs. Ongoing vaccination campaigns and reimbursement policies further strengthen market expansion.

U.K. Pneumococcal Vaccine Market Insight

The U.K. pneumococcal vaccine market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising awareness about preventive healthcare and adherence to NHS vaccination guidelines. Concerns regarding pneumonia, meningitis, and other pneumococcal infections are encouraging both healthcare providers and parents to follow recommended immunization schedules. The country’s robust healthcare infrastructure, combined with strong government vaccination initiatives and digital health campaigns, is expected to continue to stimulate market growth. In addition, the availability of both conjugate and polysaccharide vaccines for children and adults supports widespread adoption. The U.K. market also benefits from easy access to vaccines through clinics and pharmacies.

Germany Pneumococcal Vaccine Market Insight

The Germany pneumococcal vaccine market is expected to expand at a considerable CAGR during the forecast period, fueled by growing awareness of pneumococcal disease prevention and increasing vaccination coverage among vulnerable populations. Germany’s well-developed healthcare system, strong public health policies, and emphasis on preventive care promote vaccine adoption, particularly in children, older adults, and immunocompromised individuals. The integration of vaccines into routine pediatric and adult immunization schedules is also driving uptake. High public trust in vaccines and extensive government-supported campaigns further strengthen market growth. In addition, the growing prevalence of chronic diseases and aging population increases demand for adult pneumococcal vaccination.

Asia-Pacific Pneumococcal Vaccine Market Insight

The Asia-Pacific pneumococcal vaccine market is poised to grow at the fastest CAGR of 23% during the forecast period of 2026 to 2033, driven by increasing government initiatives for immunization and growing awareness of vaccine-preventable diseases. Rising urbanization, improving healthcare infrastructure, and higher disposable incomes in countries such as China, India, and Japan are fueling vaccine adoption. The region’s focus on child health and national immunization programs is increasing coverage rates. Moreover, the affordability and accessibility of vaccines are improving through domestic manufacturing and partnerships with global vaccine manufacturers. Expanding public and private healthcare facilities further support the growing demand for pneumococcal vaccines.

Japan Pneumococcal Vaccine Market Insight

The Japan pneumococcal vaccine market is gaining momentum due to the country’s focus on preventive healthcare, aging population, and strong immunization programs. Japanese healthcare providers emphasize vaccination for both children and seniors, increasing market demand. The adoption of pneumococcal vaccines is also driven by public awareness campaigns and government-supported vaccination initiatives. Integration of vaccination into routine check-ups and community health programs supports steady uptake. Moreover, the availability of conjugate and polysaccharide vaccines ensures protection across multiple age groups. Japan’s high healthcare standards and emphasis on disease prevention are boosting market growth across residential and clinical settings.

India Pneumococcal Vaccine Market Insight

The India pneumococcal vaccine market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rising government immunization initiatives, increasing awareness, and expanding healthcare access. India’s focus on child health programs, alongside growing adoption of adult vaccination, is driving market demand. The country is witnessing increased inclusion of vaccines in public and private healthcare programs, improving availability and coverage. Expanding urbanization, rising disposable incomes, and growing healthcare infrastructure further support market growth. Moreover, domestic vaccine manufacturing and affordability initiatives enhance accessibility to pneumococcal vaccines. Strong collaborations between global vaccine manufacturers and government programs are key factors propelling the market in India.

Pneumococcal Vaccine Market Share

The Pneumococcal Vaccine industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- GSK plc (U.K.)

- Serum Institute of India Pvt. Ltd. (India)

- Biological E. Limited (India)

- Yunnan Walvax Biotechnology Co., Ltd. (China)

- Sanofi (France)

- Astellas Pharma Inc. (Japan)

- Vaxcyte, Inc. (U.S.)

- Shenzhen Kangtai Biological Products Co., Ltd. (China)

- Panacea Biotec Ltd (India)

- Bharat Biotech International Ltd (India)

- Beijing Minhai Biotechnology Co., Ltd. (China)

- SK bioscience Co., Ltd. (South Korea)

- Biological E Ltd (India)

- Emergent BioSolutions Inc. (U.S.)

- Hualan Biological Engineering Inc. (China)

- NPO Petrovax Pharm LLC (Russia)

- PnuVax Incorporated (U.S.)

- CSL Limited (Australia)

What are the Recent Developments in Global Pneumococcal Vaccine Market?

- In March 2025, the European Commission (EC) granted regulatory approval for CAPVAXIVE® (Merck’s 21‑valent PCV) across the EU for adult immunization against invasive pneumococcal disease and pneumonia, enabling broader European access

- In January 2025, the Pan American Health Organization (PAHO), Argentina, Pfizer and Sinergium Biotech announced collaboration to drive local production of the 20‑valent pneumococcal vaccine (PCV20) for Latin America and the Caribbean, improving regional access at competitive pricing

- In October 2024, Pfizer supplied its one‑billionth pneumococcal conjugate vaccine dose through its partnership with Gavi, the Vaccine Alliance to vaccinate children in low‑income countries, marking a major milestone in global immunization outreach

- In June 2024, the FDA approved CAPVAXIVE™ (Merck’s 21‑valent pneumococcal conjugate vaccine) for active immunization to prevent invasive pneumococcal disease and pneumonia in adults 18 years and older, representing the most serotype‑inclusive adult pneumococcal vaccine to date

- In April 2023, the U.S. Food and Drug Administration (FDA) approved PREVNAR 20, Pfizer’s 20‑valent pneumococcal conjugate vaccine for the prevention of invasive pneumococcal disease and otitis media in infants, children and older populations, broadening protection beyond 13 serotypes

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.