Global Point Of Care Ultrasound Device Market

Market Size in USD Billion

USD

2.61 Billion

USD

4.16 Billion

2024

2032

USD

2.61 Billion

USD

4.16 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.61 Billion | |

| USD 4.16 Billion | |

| % | |

|

Point-of-Care-Ultrasound Device Market Size

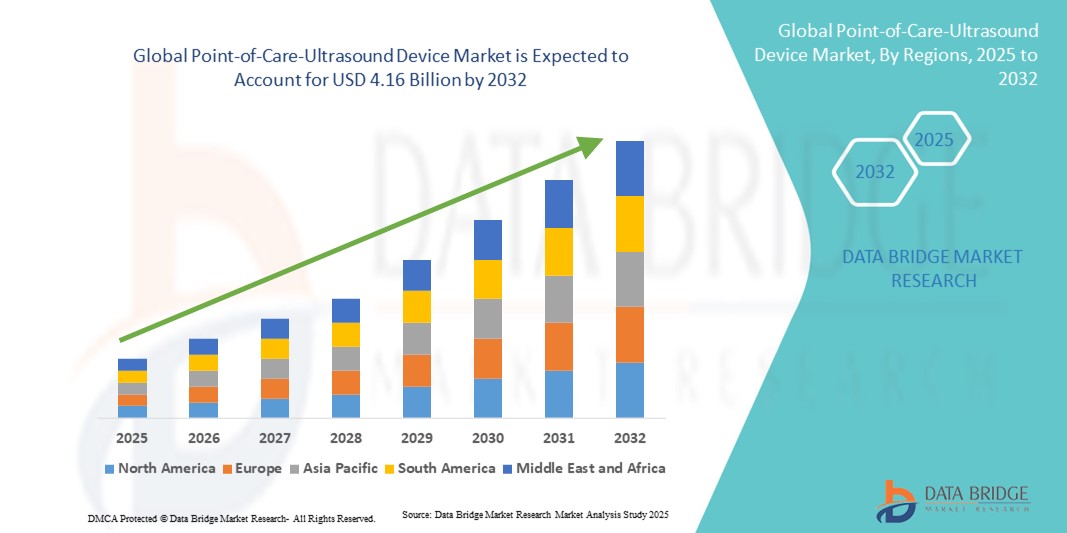

- The global point-of-care-ultrasound device market size was valued at USD 2.61 billion in 2024 and is expected to reach USD 4.16 billion by 2032, at a CAGR of 6.00% during the forecast period

- The market growth is largely fueled by the increasing adoption of portable and handheld ultrasound devices, technological advancements in imaging quality, AI integration, and wireless connectivity, which are enabling faster and more accurate bedside diagnostics across clinical settings

- Furthermore, rising demand from hospitals, emergency care units, and diagnostic centers for user-friendly, real-time imaging solutions is establishing POCUS devices as a preferred diagnostic tool. These converging factors are accelerating the uptake of point-of-care ultrasound solutions, thereby significantly boosting the industry’s growth

Point-of-Care-Ultrasound Device Market Analysis

- Point-of-care ultrasound (POCUS) devices, providing portable, real-time imaging at the patient bedside, are increasingly essential tools in modern healthcare settings across hospitals, clinics, and emergency care units due to their rapid diagnostic capabilities, ease of use, and integration with digital health systems

- The rising adoption of POCUS devices is primarily fueled by growing demand for quick, non-invasive diagnostic solutions, technological advancements such as AI-assisted imaging and wireless connectivity, and the increasing need for point-of-care diagnostics in both developed and emerging healthcare markets

- North America dominated the POCUS device market with the largest revenue share of 39.5% in 2024, driven by advanced healthcare infrastructure, high adoption of innovative medical technologies, and a strong presence of leading device manufacturers, with the U.S. showing significant growth in handheld and compact device adoption, particularly in emergency medicine, cardiology, and critical care settings

- Asia-Pacific is expected to be the fastest-growing region in the POCUS device market during the forecast period due to expanding healthcare access, increasing investment in medical infrastructure, and rising awareness about point-of-care diagnostic benefits

- Handheld segment dominated the point-of-care-ultrasound device market with a market share of 44.6% in 2024, driven by its portability, ease of integration into diverse clinical workflows, and ability to provide rapid, bedside diagnostic imaging without the need for dedicated imaging rooms

Report Scope and Point-of-Care-Ultrasound Device Market Segmentation

|

Attributes |

Point-of-Care-Ultrasound Device Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Point-of-Care-Ultrasound Device Market Trends

Enhanced Diagnostic Efficiency Through AI and Wireless Integration

- A significant and accelerating trend in the global POCUS device market is the integration of artificial intelligence (AI) and wireless connectivity, enabling faster image acquisition, real-time analysis, and remote consultations. This fusion of technologies is significantly improving workflow efficiency and diagnostic accuracy in clinical settings

- For instance, Butterfly iQ+ and Philips Lumify devices leverage AI-powered image interpretation to assist clinicians in detecting abnormalities quickly, while wireless connectivity allows seamless transfer of imaging data to electronic health records (EHRs) or remote specialists for consultation

- AI integration in POCUS devices facilitates features such as automated measurements, anomaly detection, and decision-support recommendations, enhancing clinical confidence and reducing the need for multiple scans. Similarly, wireless-enabled devices allow physicians to perform bedside imaging without bulky equipment, improving patient throughput and convenience

- The seamless integration of POCUS devices with hospital information systems, telemedicine platforms, and mobile applications enables centralized management of imaging workflows, remote monitoring, and efficient sharing of diagnostic results across care teams

- This trend toward intelligent, connected, and portable ultrasound solutions is fundamentally transforming clinical expectations for point-of-care diagnostics. Consequently, companies such as GE Healthcare and Butterfly Network are developing AI-assisted and cloud-connected POCUS systems with advanced analytics and remote monitoring capabilities

- The demand for POCUS devices offering AI-driven analysis and wireless connectivity is growing rapidly across hospitals, emergency care units, and specialty clinics, as healthcare providers increasingly prioritize rapid, accurate, and patient-centric diagnostic solutions

Point-of-Care-Ultrasound Device Market Dynamics

Driver

Growing Demand Due to Rapid Diagnostics and Portable Imaging Needs

- The increasing need for immediate bedside diagnostics, coupled with the growing adoption of portable ultrasound devices, is a significant driver for the heightened demand for POCUS systems

- For instance, in March 2024, Philips Lumify introduced new enhancements to its handheld ultrasound solutions, integrating AI-powered imaging and mobile app connectivity, aimed at improving point-of-care diagnostics in emergency and outpatient settings

- As healthcare providers seek to reduce patient wait times, optimize workflow, and enhance decision-making, POCUS devices offer real-time imaging, automated measurements, and improved accuracy compared to traditional imaging approaches

- Furthermore, the growing prevalence of chronic diseases, emergency care requirements, and prehospital diagnostic needs is increasing the reliance on portable ultrasound devices, making POCUS an essential tool for hospitals, ambulatory care centers, and mobile clinics

- The convenience of compact form factors, wireless data transfer, and rapid deployment in diverse clinical scenarios is propelling the adoption of POCUS devices globally, supported by increasing awareness and training among healthcare professionals

Restraint/Challenge

High Device Cost and Regulatory Hurdles

- Concerns regarding high acquisition costs, complex regulatory approvals, and reimbursement limitations pose significant challenges to broader market penetration. Advanced POCUS devices, particularly those with AI capabilities and integrated telemedicine features, often come with premium pricing, limiting adoption in cost-sensitive markets

- For instance, while devices such as Butterfly iQ+ have made handheld ultrasound more affordable, premium solutions with advanced imaging and analytics remain relatively expensive, particularly for smaller clinics and emerging markets

- Regulatory compliance and stringent certification requirements for medical devices, including ultrasound systems, can delay product launches and market entry. Companies such as GE Healthcare and Siemens Healthineers focus on meeting FDA, CE, and other regional approvals while emphasizing robust device safety and performance to build trust among healthcare providers

- In addition, ensuring proper training for clinicians and technicians is critical to maximize device utility and avoid diagnostic errors, which can be a barrier in regions with limited skilled personnel

- Overcoming these challenges through cost-effective solutions, flexible financing models, enhanced regulatory support, and training programs will be vital for sustained POCUS market growth

Point-of-Care-Ultrasound Device Market Scope

The market is segmented on the basis of type, portability, application, and end user.

- By Type

On the basis of type, the point-of-care-ultrasound device market is segmented into diagnostic and therapeutic devices. The diagnostic segment dominated the market with the largest revenue share of 61.3% in 2024, driven by the widespread use of ultrasound imaging for rapid bedside assessments in emergency medicine, cardiology, obstetrics, and general clinical examinations. Diagnostic POCUS devices are highly preferred by hospitals and clinics because they provide real-time imaging, automated measurements, and AI-assisted interpretation, improving clinical decision-making and patient outcomes. The strong demand is also fueled by the ease of integration into digital health records and telemedicine platforms, which facilitates remote consultation and efficient workflow management. Furthermore, diagnostic devices are available in a variety of form factors—handheld, cart-based, and portable which increases their adoption across multiple care settings.

The therapeutic segment is expected to witness the fastest growth rate of 8.1% CAGR from 2025 to 2032, driven by the rising use of ultrasound-guided minimally invasive procedures, regional anesthesia, and focused drug delivery systems. Therapeutic POCUS devices allow clinicians to perform precision procedures with reduced risk and improved outcomes, making them increasingly valuable in surgical, cardiology, and oncology departments. The trend toward personalized treatment, coupled with technological advancements such as AI-assisted targeting, is boosting adoption in both developed and emerging healthcare markets.

- By Portability

On the basis of portability, the point-of-care-ultrasound device market is segmented into trolley/cart-based and compact/handheld devices. The compact/handheld segment dominated the market with a revenue share of 44.6% in 2024, driven by the increasing demand for portable, bedside imaging solutions that allow rapid diagnostics in emergency rooms, outpatient clinics, and remote healthcare settings. Handheld POCUS devices, such as Butterfly iQ+ and Philips Lumify, provide clinicians with high-quality imaging in a compact form factor, enabling flexibility, portability, and convenience compared to bulkier cart-based systems. The dominance of this segment is further supported by integration with AI-powered imaging, mobile applications, and wireless connectivity, which facilitates seamless data transfer, real-time analysis, and remote consultations. Handheld devices are increasingly preferred for point-of-care use in critical care, cardiology, and obstetrics, as well as in resource-limited settings and home healthcare.

The trolley/cart-based segment is expected to witness the fastest CAGR of 10.2% from 2025 to 2032, driven by their superior imaging quality, support for multiple probes, and advanced features such as Doppler imaging and multi-organ scanning. Cart-based systems remain essential for high-volume hospitals and diagnostic centers that require comprehensive and robust ultrasound capabilities. The combination of advanced technology, durability, and multi-functionality is accelerating adoption in emergency departments, ICUs, and surgical units globally.

- By Application

On the basis of application, the point-of-care-ultrasound device market is segmented into emergency medicine, cardiology, obstetrics and gynecology, oncology, surgery, urology, vascular surgery, musculoskeletal, and others. The emergency medicine segment dominated the market with the largest share of 29.4% in 2024, driven by the need for rapid, bedside imaging to triage patients and support critical care decision-making. POCUS devices provide real-time diagnostic information, allowing emergency physicians to assess trauma, cardiac function, and internal bleeding quickly. The growing adoption of POCUS in prehospital care and ambulances further strengthens this segment.

The cardiology segment is expected to witness the fastest CAGR of 9.3% from 2025 to 2032, driven by increasing use of handheld and compact devices for rapid cardiac assessments, echocardiography, and monitoring of heart failure patients. AI-enabled POCUS devices are assisting cardiologists in detecting arrhythmias, structural abnormalities, and ventricular dysfunction, improving early diagnosis and intervention. Rising cardiovascular disease prevalence and the need for efficient outpatient cardiac monitoring are contributing to the accelerated adoption of POCUS in cardiology.

- By End User

On the basis of end user, the point-of-care-ultrasound device market is segmented into hospitals, diagnostic centers, research laboratories, clinics, ambulatory surgical centers, and others. The hospitals segment dominated the market with a revenue share of 65.1% in 2024, due to the high patient throughput, requirement for multiple imaging modalities, and the availability of skilled operators. Hospitals benefit from both trolley-based and handheld devices for diverse applications such as emergency diagnostics, inpatient monitoring, and surgical guidance, making them the largest end users of POCUS devices.

The clinics segment is expected to witness the fastest CAGR of 8.7% from 2025 to 2032, driven by rising outpatient care, telemedicine adoption, and increasing preference for point-of-care diagnostics in private healthcare facilities. Compact and handheld POCUS devices enable clinics to perform immediate assessments without referring patients to hospitals, reducing waiting times and improving patient satisfaction. Growing awareness among clinicians about the clinical and operational benefits of POCUS devices is further propelling growth in this segment.

Point-of-Care-Ultrasound Device Market Regional Analysis

- North America dominated the point-of-care-ultrasound device market with the largest revenue share of 39.5% in 2024, driven by advanced healthcare infrastructure, high adoption of innovative medical technologies, and a strong presence of leading device manufacturers

- Healthcare providers in the region highly value the portability, AI-assisted imaging, and wireless connectivity offered by handheld and compact POCUS devices, which enable quick assessments, real-time decision-making, and integration with electronic health records and telemedicine platforms

- This widespread adoption is further supported by high healthcare spending, a technologically inclined medical workforce, and strong presence of leading device manufacturers such as GE Healthcare, Philips, and Butterfly Network. The availability of skilled clinicians trained in POCUS usage and the focus on improving patient throughput and care efficiency establish these devices as essential tools in North American healthcare facilities

U.S. Point-of-Care-Ultrasound Device Market Insight

The U.S. point-of-care ultrasound device market captured the largest revenue share of 36% in 2024 within North America, driven by the high adoption of portable and handheld ultrasound devices in hospitals, emergency care units, and outpatient clinics. Healthcare providers are prioritizing rapid, bedside diagnostics to improve patient outcomes and operational efficiency. The growing trend of integrating AI-assisted imaging, wireless connectivity, and mobile applications enables real-time data sharing and telemedicine consultations, further propelling market growth. Moreover, increasing awareness of point-of-care diagnostics and the demand for compact, user-friendly devices support strong adoption across both urban and rural healthcare settings.

Europe Point-of-Care Ultrasound Device Market Insight

The Europe point-of-care ultrasound device market is projected to expand at a substantial CAGR throughout the forecast period, fueled by well-established healthcare systems, rising adoption of portable imaging solutions, and increasing awareness of the benefits of rapid bedside diagnostics. Hospitals, cardiology centers, and emergency departments are increasingly integrating compact ultrasound devices for real-time assessment, while regulatory support for advanced medical technologies promotes market growth. The trend of combining point-of-care ultrasound devices with telemedicine platforms and AI-driven analytics further enhances diagnostic accuracy and efficiency, supporting adoption across both residential healthcare clinics and large medical facilities.

U.K. Point-of-Care Ultrasound Device Market Insight

The U.K. point-of-care ultrasound device market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the need for rapid and accurate diagnostic tools in emergency medicine, cardiology, and outpatient care. Increasing prevalence of chronic diseases, rising investment in healthcare infrastructure, and growing awareness among clinicians about point-of-care ultrasound advantages are supporting market expansion. In addition, the integration of handheld devices with electronic health records and telemedicine systems facilitates seamless patient monitoring, further encouraging adoption in hospitals, clinics, and diagnostic centers.

Germany Point-of-Care Ultrasound Device Market Insight

The Germany point-of-care ultrasound device market is expected to expand at a considerable CAGR during the forecast period, fueled by high healthcare standards, strong technological infrastructure, and rising awareness of portable and AI-enabled ultrasound devices. Hospitals and specialty clinics are increasingly adopting compact and handheld point-of-care ultrasound systems for emergency diagnostics, cardiology, and obstetrics applications. The emphasis on innovation and precision medicine promotes the deployment of advanced imaging solutions, while robust training programs for healthcare professionals ensure effective utilization of point-of-care ultrasound devices across clinical settings.

Asia-Pacific Point-of-Care Ultrasound Device Market Insight

The Asia-Pacific point-of-care ultrasound device market is poised to grow at the fastest CAGR of 11% during the forecast period of 2025 to 2032, driven by increasing healthcare access, rapid urbanization, and rising investments in diagnostic infrastructure across countries such as China, Japan, and India. The growing adoption of portable and compact point-of-care ultrasound devices in emergency care, cardiology, and obstetrics is accelerating market penetration. Government initiatives to enhance healthcare accessibility, coupled with increasing awareness of point-of-care diagnostics and rising disposable incomes, are contributing to the fast uptake of point-of-care ultrasound devices in hospitals, clinics, and rural healthcare centers.

Japan Point-of-Care Ultrasound Device Market Insight

The Japan point-of-care ultrasound device market is gaining momentum due to the country’s high-tech healthcare ecosystem, rapid urbanization, and increasing demand for rapid diagnostic solutions. Handheld and AI-enabled point-of-care ultrasound devices are being integrated into hospitals, emergency units, and outpatient clinics to improve patient care and workflow efficiency. The trend toward connected devices and telemedicine platforms supports market expansion, while Japan’s aging population is driving demand for user-friendly, accurate, and portable diagnostic tools across both residential and commercial healthcare facilities.

India Point-of-Care Ultrasound Device Market Insight

The India point-of-care ultrasound device market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to expanding healthcare infrastructure, high adoption of digital health solutions, and rising awareness of point-of-care diagnostics. Hospitals, clinics, and emergency care units are increasingly using handheld ultrasound devices to provide rapid bedside imaging. Government initiatives to promote smart healthcare facilities, increasing affordability of compact point-of-care ultrasound devices, and strong local manufacturing capabilities are key factors driving growth. The trend toward portable, AI-assisted diagnostic tools is accelerating adoption across both urban and semi-urban regions in India.

Point-of-Care-Ultrasound Device Market Share

The Point-of-Care-Ultrasound Device industry is primarily led by well-established companies, including:

- EchoNous, Inc. (U.S.)

- Clarius Mobile Health Corp. (Canada)

- FUJIFILM Sonosite, Inc. (U.S.)

- GE HealthCare (U.S.)

- Butterfly Network, inc. (U.S.)

- Koninklijke Philips N.V., (Netherlands)

- Terason Division Teratech Corporation. (U.S.)

- Siemens Healthineers AG (Germany)

- TELEMED (Greece)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China)

- Samsung Medison Co., Ltd. (South Korea)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Hologic, Inc. (U.S.)

- Haifu Medical Technology Co., Ltd. (China)

- Esaote S.p.A. (Italy)

- Hitachi Healthcare Americas (U.S.)

- Analogic Corporation (U.S.)

- SonoScape Medical Corp. (China)

What are the Recent Developments in Global Point-of-Care-Ultrasound Device Market?

- In August 2025, Sonic Incytes Medical Corp announced that the U.S. Food and Drug Administration (FDA) granted 510(k) clearance for Velacur ONE, its point-of-care ultrasound elastography device. This device enables clinicians to assess liver stiffness at the bedside, aiding in the management of chronic liver diseases and improving patient care through non-invasive diagnostics

- In July 2025, MAUI Imaging, a medical startup, raised USD 14 million in Series D funding to advance its innovative ultrasound technology. The company's devices aim to visualize through typical barriers such as bone, gas, fat, surgical tools, and implants areas beyond the capabilities of traditional ultrasound. This advancement has the potential to enhance diagnostic imaging, particularly in challenging clinical scenarios

- In June 2025, Philips introduced the Flash 5100, a next-generation point-of-care ultrasound system designed for critical care environments. This system aims to provide rapid and accurate imaging in emergency rooms, intensive care units, and trauma wards, enhancing diagnostic capabilities at the bedside. The Flash 5100 integrates advanced imaging technology to support clinicians in making swift, informed decisions

- In June 2025, Vave Health launched the world's first wireless, handheld, whole-body ultrasound system with a single PZT transducer. This innovative device aims to make ultrasound technology more accessible and cost-effective, enabling comprehensive imaging in various clinical settings, including primary care and emergency medicine

- In September 2024, GE HealthCare unveiled the Venue Sprint, a compact ultrasound device combining portability with AI-enabled tools. Designed for emergency and critical care settings, the Venue Sprint offers enhanced imaging capabilities and real-time decision support, facilitating quick assessments in fast-paced environments

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.