Global Polychondritis Disease Treatment Market

Market Size in USD Million

USD

124.70 Million

USD

198.75 Million

2024

2032

USD

124.70 Million

USD

198.75 Million

2024

2032

| 2025 - 2032 | |

| USD 124.70 Million | |

| USD 198.75 Million | |

| % | |

|

Polychondritis Disease Treatment Market Size

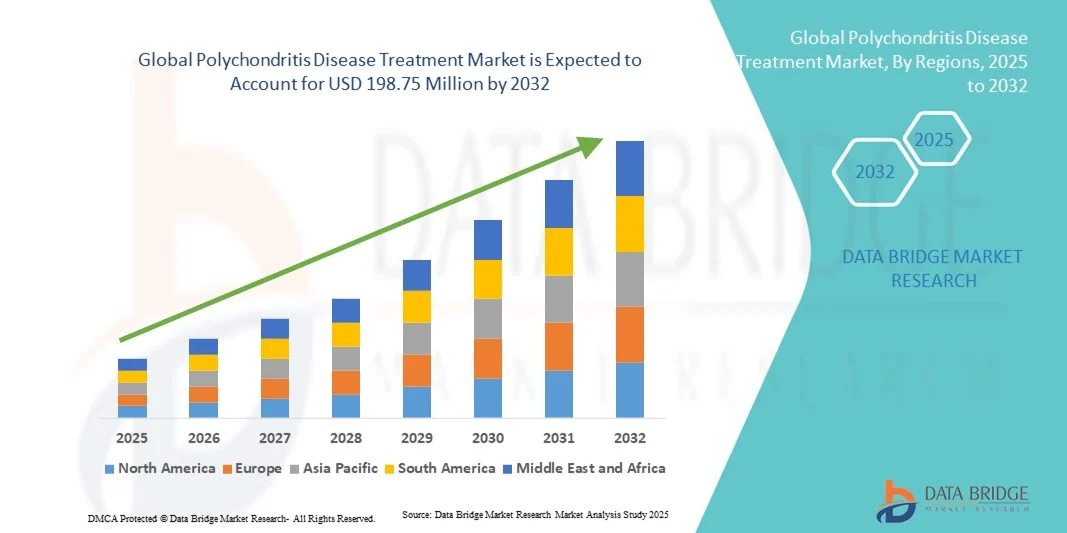

- The global polychondritis disease treatment market size was valued at USD 124.7 Million in 2024 and is expected to reach USD 198.75 Million by 2032, at a CAGR of 6.00% during the forecast period

- The market growth is largely fueled by the growing adoption of advanced therapeutic approaches and ongoing technological progress in drug development, gene therapy, and biologics aimed at managing inflammation and preventing cartilage degradation in patients with Polychondritis Disease

- Furthermore, increasing awareness about autoimmune disorders, rising investments in research and development by pharmaceutical companies, and growing demand for effective treatment options are driving the uptake of Polychondritis Disease Treatment solutions, thereby significantly boosting the industry's growth

Polychondritis Disease Treatment Market Analysis

- Polychondritis Disease Treatment, encompassing pharmacological and non-pharmacological approaches, is becoming increasingly important in managing chronic inflammation and preventing progressive cartilage damage in both mild and severe cases due to advancements in immunotherapy, biologics, and early diagnostic methods

- The rising demand for polychondritis disease treatment is primarily driven by increasing awareness of autoimmune disorders, expanding access to specialty healthcare services, and the growing availability of targeted therapies offering improved efficacy and fewer side effects compared to conventional corticosteroids

- North America dominated the polychondritis disease treatment market with the largest revenue share of 38.5% in 2024, supported by strong healthcare infrastructure, favorable reimbursement frameworks, and high prevalence of autoimmune and inflammatory diseases. The U.S. continues to lead regional growth due to increased clinical trials, rapid adoption of biologics, and active participation of major pharmaceutical companies in rare disease research

- Asia-Pacific is expected to be the fastest-growing region in the polychondritis disease Treatment market during the forecast period, with a projected CAGR of 9.8%, driven by improving diagnostic facilities, growing healthcare expenditure, and rising patient awareness in emerging economies such as China, India, and South Korea

- The oral segment dominated the market with a 52.8% revenue share in 2024, attributed to its ease of administration, patient convenience, and preference for non-invasive treatment routes

Report Scope and Polychondritis Disease Treatment Market Segmentation

|

Attributes |

Polychondritis Disease Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Polychondritis Disease Treatment Market Trends

Advancements in Biologic Therapies and Personalized Medicine

- A significant and accelerating trend in the global polychondritis disease treatment market is the increasing focus on biologic and targeted therapies, along with the adoption of personalized treatment strategies. These innovations are transforming disease management by addressing specific inflammatory pathways involved in cartilage damage and immune dysregulation

- For instance, ongoing clinical trials are evaluating TNF inhibitors, IL-6 blockers, and complement pathway inhibitors for refractory cases, offering new hope for patients unresponsive to conventional corticosteroids and immunosuppressants. Similarly, biologics targeting cytokine-mediated inflammation have shown encouraging outcomes in improving symptom control and reducing relapse frequency

- The integration of molecular diagnostics and genomic profiling allows clinicians to tailor therapy based on the patient’s genetic and immunologic profile, improving precision and long-term treatment outcomes. For example, novel biomarker-based approaches are being developed to predict disease flares and guide the optimal use of biologic agents

- The growing emphasis on early diagnosis and proactive disease management has led to the development of patient-specific treatment algorithms and multidisciplinary care models involving rheumatologists, otolaryngologists, and pulmonologists

- Furthermore, the emergence of advanced biologic delivery methods — such as subcutaneous injections and extended-release formulations — is enhancing treatment adherence and patient quality of life. The availability of compassionate-use programs and expanded-access clinical initiatives is also helping patients access novel therapies prior to formal market approval

- This trend toward more personalized, targeted, and biologically advanced therapy options is redefining the treatment landscape for autoimmune and inflammatory diseases such as Polychondritis. Consequently, several key pharmaceutical players are accelerating research into monoclonal antibodies and small-molecule immunomodulators to expand treatment options and improve long-term disease management

- The demand for novel biologic and targeted therapies is rapidly increasing worldwide as clinicians and patients shift away from long-term corticosteroid dependence toward safer, more effective, and individualized therapeutic regimens

Polychondritis Disease Treatment Market Dynamics

Driver

Rising Prevalence of Autoimmune Disorders and Increasing Research Initiatives

- The growing global burden of autoimmune and inflammatory diseases, along with greater recognition and diagnosis of Polychondritis, is a major factor driving market growth. Rising clinical awareness among healthcare professionals has improved early detection rates and accelerated referrals to specialty care centers

- For instance, in March 2024, the U.S. National Institutes of Health (NIH) expanded its Rare Diseases Clinical Research Network to include Polychondritis-focused studies aimed at investigating new immunomodulatory treatments. Such initiatives are expected to stimulate product development and enhance treatment availability

- The increasing research focus on understanding the genetic and molecular basis of the disease has led to the discovery of potential therapeutic targets, prompting drug development partnerships between biotechnology companies and academic institutions

- Furthermore, growing patient advocacy efforts and support organizations are promoting awareness campaigns and funding for rare disease research, contributing to market expansion. The rising use of advanced imaging, biomarkers, and next-generation sequencing technologies is improving diagnosis precision and supporting personalized care strategies

- Overall, the integration of innovative R&D, improved disease monitoring, and patient-focused clinical programs continues to propel the Polychondritis Disease Treatment market forward

Restraint/Challenge

Limited Treatment Options and High Costs of Advanced Therapies

- The lack of approved targeted therapies and the reliance on long-term corticosteroid and immunosuppressive regimens remain key challenges in the effective management of Polychondritis. Many patients experience partial or inconsistent responses to available treatments, necessitating ongoing research into safer and more durable therapeutic solutions

- For instance, although biologics show promising results, their high cost and limited insurance coverage make access challenging for many patients, particularly in developing regions. The absence of standardized treatment guidelines and variability in clinical presentation further complicate disease management

- The chronic nature of Polychondritis often requires long-term treatment, increasing both the economic and psychological burden on patients. Moreover, the rarity of the condition limits large-scale clinical trial participation, slowing drug development and regulatory approval

- Addressing these challenges requires collaborative efforts between governments, pharmaceutical companies, and patient organizations to improve affordability and availability of new treatments. Investment in orphan drug development programs and international clinical networks is essential to expedite research and broaden therapeutic options

- While innovation in biologics and molecular therapies continues, the market still faces barriers in pricing, distribution, and regulatory harmonization. Overcoming these issues through increased funding, global collaboration, and patient support frameworks will be critical for ensuring equitable access and sustainable market growth

Polychondritis Disease Treatment Market Scope

The market is segmented on the basis of drug class, symptoms, mode of administration, and distribution channel.

- By Drug Class

On the basis of drug class, the Polychondritis Disease Treatment market is segmented into corticosteroids, aspirin, dapsone, and others. The corticosteroid segment dominated the largest market revenue share of 46.7% in 2024, driven by its high effectiveness in suppressing inflammation and modulating immune response. Corticosteroids such as prednisone remain the gold standard for managing acute and relapsing symptoms of polychondritis, ensuring rapid relief and improved patient outcomes. Their proven therapeutic efficacy, affordability, and established clinical protocols strengthen their use across hospital and retail pharmacies. The segment also benefits from ongoing innovation in dosage optimization, tapering methods, and novel formulations with reduced side effects. The continued preference for corticosteroids as first-line therapy in mild to moderate cases ensures stable long-term demand across developed and emerging markets, reinforcing this segment’s dominance in global revenue contribution.

The dapsone segment is expected to witness the fastest CAGR of 8.6% from 2025 to 2032, driven by its growing clinical use in refractory and corticosteroid-resistant cases of polychondritis. Dapsone’s dual anti-inflammatory and immunomodulatory properties have positioned it as an emerging alternative in combination treatment protocols. Increasing physician awareness of its efficacy in chronic management and its ability to reduce corticosteroid dependency are key growth contributors. Ongoing research exploring dapsone’s mechanisms in autoimmune regulation is further enhancing its acceptance among healthcare providers. The rising availability of oral and low-dose dapsone formulations with better tolerability profiles also supports broader patient adoption, particularly in Asia-Pacific and Europe.

- By Symptoms

On the basis of symptoms, the Polychondritis Disease Treatment market is segmented into nasal chondritis, inflammation, heart valve abnormalities, and kidney inflammation and dysfunction. The inflammation segment accounted for the largest market revenue share of 41.5% in 2024, driven by the high prevalence of systemic and localized inflammatory manifestations in patients with relapsing polychondritis. Anti-inflammatory and corticosteroid-based regimens are the cornerstone of treatment, making this segment central to overall disease management. Widespread availability of therapeutic options, rapid symptom control, and consistent physician preference for inflammation-targeted therapy drive this dominance. The rise in autoimmune-triggered inflammatory cases further increases treatment demand globally. Advancements in targeted drug formulations and early diagnosis also contribute to the robust revenue performance of this segment in both outpatient and hospital settings.

The heart valve abnormalities segment is projected to register the fastest CAGR of 9.1% from 2025 to 2032, fueled by increasing awareness of cardiac involvement in chronic autoimmune disorders. The growing rate of diagnostic echocardiography and the availability of advanced interventional therapies have enhanced early detection and management of polychondritis-related valve complications. The introduction of biologics and immunotherapies targeting cardiovascular inflammation is improving long-term outcomes, leading to rising treatment uptake. Moreover, collaborative research between rheumatologists and cardiologists is expanding the scope of clinical intervention in this category, driving sustained market growth over the forecast period.

- By Mode of Administration

On the basis of mode of administration, the Polychondritis Disease Treatment market is segmented into injectables, oral, and others. The oral segment dominated the market with a 52.8% revenue share in 2024, attributed to its ease of administration, patient convenience, and preference for non-invasive treatment routes. Oral corticosteroids and immunomodulatory drugs are widely prescribed due to their cost-effectiveness, accessibility, and suitability for long-term disease management. The availability of multiple dosage forms and the flexibility in adjusting therapy according to symptom severity further support dominance. The strong global distribution network of oral medications through both retail and hospital pharmacies ensures continuous treatment availability. These factors collectively reinforce the leading position of the oral administration segment in the global market landscape.

The injectables segment is anticipated to witness the fastest CAGR of 8.9% from 2025 to 2032, driven by the rising adoption of biologics and monoclonal antibody therapies. Injectable formulations provide higher bioavailability and rapid therapeutic onset, making them ideal for severe or refractory cases. Increasing R&D investments in injectable biologics targeting inflammatory pathways are expanding clinical options for polychondritis patients. Hospitals and specialty clinics are increasingly preferring injectable drugs for personalized, high-efficacy treatment plans. Continuous technological improvements in delivery mechanisms, such as prefilled syringes and autoinjectors, further enhance convenience and compliance, boosting this segment’s growth trajectory through 2032.

- By Distribution Channel

On the basis of distribution channel, the Polychondritis Disease Treatment market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. The hospital pharmacy segment dominated the market with a 49.3% revenue share in 2024, supported by the central role hospitals play in the diagnosis and management of rare autoimmune disorders. These settings provide access to specialized physicians, advanced biologics, and emergency care facilities, ensuring comprehensive treatment for complex cases. Hospitals also benefit from direct partnerships with pharmaceutical manufacturers, improving the availability of high-cost biologics and injectables. Rising hospitalization rates for acute symptom management and the concentration of clinical expertise within tertiary care centers strengthen this segment’s dominance across key regions.

The online pharmacy segment is projected to witness the fastest CAGR of 10.2% from 2025 to 2032, fueled by the rapid digital transformation of healthcare and growing consumer preference for home-based medication delivery. The expansion of telemedicine and e-prescription systems has made online access to autoimmune drugs more seamless. Major e-pharmacy platforms are increasingly collaborating with licensed suppliers to ensure authenticity and compliance with regulatory standards. Rising awareness about chronic disease management and the convenience of subscription-based refill options are driving adoption. The integration of digital consultation services within online pharmacy networks further enhances patient engagement, contributing to sustained double-digit growth over the forecast period.

Polychondritis Disease Treatment Market Regional Analysis

- North America dominated the polychondritis disease treatment market with the largest revenue share of 38.5% in 2024, supported by strong healthcare infrastructure, favorable reimbursement frameworks, and a high prevalence of autoimmune and inflammatory diseases

- The region’s leadership is further reinforced by growing awareness of rare disease management, a surge in biologic therapy adoption, and the presence of major pharmaceutical

- And biotech companies conducting clinical trials and developing innovative treatment options for relapsing polychondritis

U.S. Polychondritis Disease Treatment Market Insight

The U.S. polychondritis disease treatment market captured the largest revenue share in 2024 within North America, driven by extensive research on biologics, gene therapies, and immunomodulators. The country’s strong clinical research network, combined with increased funding from both public and private organizations, supports faster development of advanced therapeutic options. The introduction of patient support programs and growing healthcare expenditure further propel the U.S. market, making it a key contributor to regional and global revenue growth.

Europe Polychondritis Disease Treatment Market Insight

The Europe polychondritis disease treatment market is projected to grow at a notable CAGR throughout the forecast period, primarily driven by government-backed healthcare initiatives, rising clinical research activities, and advancements in biologic drugs. Increasing collaboration between European research institutes and pharmaceutical companies for orphan drug development is significantly enhancing market expansion. Furthermore, patient registries and awareness programs across the EU are supporting early diagnosis and improving treatment accessibility.

U.K. Polychondritis Disease Treatment Market Insight

The U.K. polychondritis disease treatment market is expected to expand at a substantial CAGR during the forecast period, propelled by active participation in clinical trials, increasing availability of specialized autoimmune disease centers, and supportive regulatory policies for rare disease drug approvals. The NHS’s growing focus on integrating biologic therapies and digital diagnostic tools is also contributing to improved disease management outcomes across the country.

Germany Polychondritis Disease Treatment Market Insight

The polychondritis disease treatment market is expected to grow steadily during the forecast period, driven by a robust healthcare system, strong presence of global pharmaceutical companies, and an emphasis on research and development of biologic and targeted therapies. Germany’s commitment to improving rare disease infrastructure through national registries and hospital collaborations is also creating favorable conditions for market growth.

Asia-Pacific Polychondritis Disease Treatment Market Insight

The Asia-Pacific polychondritis disease treatment market is projected to witness the fastest CAGR of 9.8% from 2025 to 2032, fueled by improving diagnostic facilities, growing healthcare expenditure, and rising awareness about autoimmune disorders in emerging economies such as China, India, and South Korea. Increasing clinical collaborations with global pharmaceutical firms and government investments in rare disease management are significantly driving treatment accessibility and market expansion.

Japan Polychondritis Disease Treatment Market Insight

The Japan polychondritis disease treatment market is experiencing steady growth, supported by high healthcare standards, early adoption of biologic therapies, and the country’s strong focus on precision medicine. Japan’s ongoing advancements in genetic research and stem-cell-based therapies are expected to contribute to long-term market development and improved treatment efficacy.

China Polychondritis Disease Treatment Market Insight

The China polychondritis disease treatment market accounted for the largest revenue share in the Asia-Pacific region in 2024, attributed to rapidly expanding healthcare infrastructure, increasing public health awareness, and government initiatives promoting rare disease diagnosis and treatment. Growing domestic pharmaceutical production and clinical research collaborations are making advanced therapies more accessible, positioning China as a key emerging market in the global landscape.

Polychondritis Disease Treatment Market Share

The Polychondritis Disease Treatment industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Johnson & Johnson and its affiliates (U.S.)

- Novartis AG (Switzerland)

- GSK plc (U.K.)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- AbbVie Inc. (U.S.)

- AstraZeneca plc (U.K.)

- Bayer AG (Germany)

- Bristol Myers Squibb (U.S.)

- Merck & Co., Inc. (U.S.)

- Sanofi S.A. (France)

- Amgen Inc. (U.S.)

- Lilly (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Horizon Therapeutics plc (Ireland)

- CSL Behring (Australia)

- Astellas Pharma Inc. (Japan)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Biogen Inc. (U.S.)

Latest Developments in Global Polychondritis Disease Treatment Market

- In May 2023, French expert groups published practical national guidelines for the diagnosis and management of relapsing polychondritis, providing the first widely referenced country-level recommendations to standardize diagnosis, organ-specific assessment, and stepwise therapy (from corticosteroids to steroid-sparing immunosuppressants and biologics)

- In May 2024, a multicenter study published in Scientific Reports described long-term outcomes and real-world treatment patterns across referral centers, documenting near-universal glucocorticoid use, frequent adoption of adjunctive immunosuppressants and biologics, and substantial rates of organ-specific damage that emphasize the need for earlier targeted interventions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.