Global Polycrystalline Solar Cell Multi Si Market

Market Size in USD Billion

USD

30.05 Billion

USD

42.73 Billion

2025

2033

USD

30.05 Billion

USD

42.73 Billion

2025

2033

| 2026 - 2033 | |

| USD 30.05 Billion | |

| USD 42.73 Billion | |

| % | |

|

Polycrystalline Solar Cell (Multi Si) Market Overview

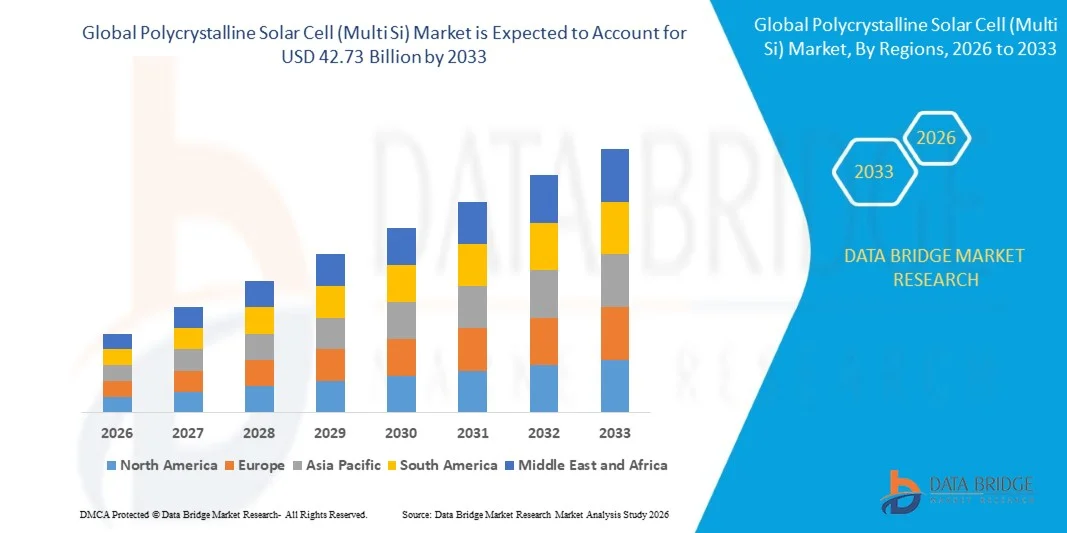

The global polycrystalline solar cell (Multi Si) market was valued at USD 30.05 billion in 2025 and is projected to reach USD 42.73 billion by 2033, growing at a CAGR of 4.50% from 2026 to 2033. The market is experiencing consistent growth driven by unmatched affordability, reliable life spans and government policies and initiatives.

Polycrystalline solar cell (Multi Si) market are generally cheaper to produce and casting process results in generation of minimal waste driving down the cost per watt. Though polycrystalline has lower conversion energy they generally have a 25 to 35 years of life span making it highly attractive for small scale projects, like rural electrification. Heavy focus on reducing carbon, and localized financial incentives (such as India's Production Linked Incentive scheme) are heavily subsidizing domestic manufacturing

Market Size & Forecast

- Market Value (2025): USD 30.05 Billion

- Expected Market Value (2033): USD 42.73 Billion

- Forecast CAGR (2026–2033): 4.50%

- Leading Region in 2025: Asia Pacific

- Fastest Growing Region: Middle East and Africa

Key Market Trends & Insights

- Asia Pacific dominated the global polycrystalline solar cell (Multi Si) market with the largest revenue share of 2% in 2025, supported by unparalleled manufacturing infrastructure and localized utility-scale installation wave.

- The grid connected segment dominated the market with an estimated 64% share in 2025, owing to the widespread deployment of utility-scale solar power plants and commercial rooftop photovoltaic systems connected to national electricity grids.

- The Middle East and Africa is expected to be the fastest-growing region at a CAGR of 20% from 2026 to 2033, fueled by rising urbanization, increasing training infrastructure investments, and growing adoption in China, India, and Japan.

- The commercial segment is expected to register the fastest CAGR of 7.12% from 2026 to 2033, driven by increasing rooftop solar adoption across office buildings, educational institutions, hospitals, shopping complexes, and industrial facilities.

- The ground-mount segment dominated the market with an estimated 69.48% share in 2025 due to its extensive use in utility-scale solar farms requiring higher generation capacity and superior operational efficiency.

Report Scope and Polycrystalline Solar Cell (Multi Si) Market Segmentation

|

Attributes |

Polycrystalline Solar Cell (Multi Si) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· LONGi Green Energy Technology Co., Ltd. (China) · Trina Solar Co., Ltd. (China) · JA Solar Technology Co., Ltd. (China) · JinkoSolar Holding Co., Ltd. (China) · Canadian Solar Inc. (Canada) · Risen Energy Co., Ltd. (China) · Astronergy (CHINT New Energy Technology Co., Ltd.) (China) · Talesun Solar Technologies Co., Ltd. (China) · GCL System Integration Technology Co., Ltd. (China) · Yingli Green Energy Holding Company Limited (China) · Hanwha Solutions Corporation (Qcells) (South Korea) · Adani Solar (India) · Waaree Energies Limited (India) · Vikram Solar Limited (India) · Tata Power Solar Systems Limited (India) · RenewSys India Pvt. Ltd. (India) · Premier Energies Limited (India) · REC Group (Singapore) · Sharp Corporation (Japan) · Neo Solar Power Corporation (Taiwan) · Motech Industries Inc. (Taiwan) |

|

Market Opportunities |

· Expansion of utility-scale solar projects in emerging economies · Growth of PV recycling and circular economy initiatives · Integration with bifacial and agrivoltaic installations |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Polycrystalline Solar Cell (Multi Si) Market Trends

Trend: Increasing Adoption of High-Efficiency Multi-Busbar and N-Type Polycrystalline Solar Cell Technologies

The global polycrystalline solar cell (multiSi) market is witnessing a gradual technological transition toward higher-efficiency cell architectures and improved manufacturing processes. Although monocrystalline technologies are gaining market share, polycrystalline solar cells continue to be widely deployed in cost-sensitive utility-scale projects and emerging markets due to their competitive pricing and proven performance. Manufacturers are increasingly adopting multi-busbar (MBB), half-cell, and advanced passivation technologies to improve module efficiency, reduce resistive losses, and enhance energy yield. In addition, growing demand for affordable photovoltaic solutions across developing economies is supporting continued investment in polycrystalline production capacity. For instance, in June 2024, the International Energy Agency reported that global renewable electricity capacity additions reached record levels in 2023, with solar PV accounting for approximately 75% of new renewable capacity additions worldwide, reinforcing continued demand for cost-effective solar technologies, including polycrystalline modules in price-sensitive markets. The continued adoption of advanced manufacturing technologies, coupled with sustained demand for affordable photovoltaic solutions in emerging economies, is expected to support the long-term relevance of the polycrystalline solar cell (multi Si) market. Although high-efficiency monocrystalline technologies are gaining market share, ongoing improvements in multi-Si cell performance and cost competitiveness will continue to drive deployment across utility-scale and commercial solar projects where affordability remains a key purchasing criterion.

Polycrystalline Solar Cell (Multi Si) Market Dynamics

Key Market Driver: Rising Utility-Scale Solar Installations in Emerging Economies

Rapid expansion of utility-scale solar power projects across Asia-Pacific, the Middle East, Africa, and Latin America is a major driver of the global polycrystalline solar cell (multi Si) market. Governments are investing heavily in renewable energy infrastructure to reduce carbon emissions, improve energy security, and achieve national clean energy targets. Polycrystalline solar cells continue to remain an attractive option for large-scale installations because they offer a favorable balance between cost and performance, particularly in projects where minimizing capital expenditure is a priority. Increasing electricity demand, supportive feed-in tariffs, renewable auctions, and declining photovoltaic manufacturing costs are further accelerating market growth. For instance, according to the International Renewable Energy Agency, global renewable power capacity increased by 585 GW in 2024, with solar photovoltaics contributing nearly 452 GW, accounting for more than three-quarters of all renewable capacity additions worldwide. This continued expansion of utility-scale solar projects is creating sustained demand for photovoltaic technologies, including polycrystalline solar cells. Growing government investments in renewable energy infrastructure and increasing deployment of utility-scale solar projects are expected to maintain steady demand for cost-effective polycrystalline solar cells, particularly across developing economies.

Key Restraint/Challenge: Rapid Shift Toward High-Efficiency Monocrystalline Technologies

One of the major challenges facing the global polycrystalline solar cell (multi Si) market is the rapid commercialization of high-efficiency monocrystalline technologies such as TOPCon, HJT, and back-contact solar cells. Continuous improvements in monocrystalline manufacturing processes have significantly reduced production costs while delivering higher conversion efficiencies than conventional polycrystalline cells. Consequently, many large solar developers are increasingly favoring monocrystalline modules to maximize energy generation and optimize land utilization. This technological transition is placing pricing pressure on polycrystalline manufacturers and reducing investment in new multi-Si production capacity. For instance, in May 2024, International Energy Agency reported that monocrystalline technologies now account for the overwhelming majority of newly installed photovoltaic manufacturing capacity globally as manufacturers continue transitioning toward higher-efficiency cell technologies. Unless supported by further manufacturing innovations and cost reductions, the growing dominance of high-efficiency monocrystalline technologies is expected to remain a significant competitive challenge for the polycrystalline solar cell market.

Key Market Opportunity: Expansion of Affordable Solar Electrification Across Developing Regions

Expanding access to affordable electricity across developing economies presents a significant opportunity for the global polycrystalline solar cell (multi Si) market. Many countries in Asia, Africa, and Latin America continue to prioritize cost-effective photovoltaic solutions for rural electrification, distributed generation, commercial rooftop installations, and public infrastructure projects. Polycrystalline modules remain attractive because of their relatively lower manufacturing costs and reliable long-term performance. Increasing financial support from multilateral development institutions and national renewable energy programs is expected to further strengthen market opportunities. For instance, in 2024, the World Bank continued expanding its renewable energy financing initiatives through the Mission 300 program and other clean energy investments aimed at accelerating electricity access across Africa, supporting large-scale deployment of affordable photovoltaic systems. Rising investment in rural electrification, distributed solar projects, and cost-sensitive utility installations across emerging economies is expected to create long-term growth opportunities for polycrystalline solar cell manufacturers despite increasing competition from premium photovoltaic technologies.

Polycrystalline Solar Cell (Multi Si) Market Scope

The polycrystalline solar cell (Multi Si) market is segmented on the basis of grid type, installation, technology, and application.

- By Grid Type

On the basis of grid type, the global polycrystalline solar cell (Multi Si) market is segmented into gridconnected and off-grid. The Grid Connected segment dominated the market with an estimated 82.64% share in 2025, owing to the widespread deployment of utility-scale solar power plants and commercial rooftop photovoltaic systems connected to national electricity grids. Supportive government policies, including feed-in tariffs, net-metering programs, renewable energy targets, and investments in grid modernization, have significantly accelerated the adoption of grid-connected solar installations. In addition, higher system reliability, improved energy efficiency, and better return on investment continue to reinforce the leading position of this segment across global markets.

The off-grid segment is expected to witness the fastest CAGR of 7.21% from 2026 to 2033, driven by increasing rural electrification initiatives, growing demand for decentralized renewable energy systems, and expanding deployment of solar-powered solutions in remote and underserved regions. Declining battery storage costs, government support for off-grid electrification, and increasing adoption across residential, agricultural, telecom, and healthcare applications are expected to further accelerate segment growth during the forecast period.

- By Installation

On the basis of installation, the global polycrystalline solar cell (Multi Si) market is segmented into Ground-Mount and Rooftop Solar PV. The ground-mount segment dominated the market with an estimated 69.48% share in 2025 due to its extensive use in utility-scale solar farms requiring higher generation capacity and superior operational efficiency. Ground-mounted systems provide better panel orientation, easier maintenance, improved cooling efficiency, and greater scalability, making them the preferred installation type for large renewable energy projects worldwide. Increasing investments in solar parks and renewable infrastructure continue to strengthen the dominance of this segment.

The rooftop solarPV segment is projected to register the fastest CAGR of 6.95% from 2026 to 2033, driven by rising adoption across residential and commercial buildings, supportive net-metering policies, declining installation costs, and increasing electricity prices. Growing consumer awareness regarding clean energy and favorable financing schemes are further supporting rooftop solar deployment across developed and emerging economies.

- By Technology

On the basis of technology, the global polycrystalline solar cell (Multi Si) market is segmented into crystalline silicon cells, thin film cells, and ultra-thin film cells. The Crystalline Silicon Cells segment dominated the market with an estimated 78.91% share in 2025, owing to its mature manufacturing ecosystem, cost competitiveness, proven reliability, and strong conversion efficiency. Continuous technological advancements, large-scale manufacturing capabilities, and widespread adoption across residential, commercial, and utility-scale applications continue to reinforce the dominance of crystalline silicon technology globally.

The ultra-thin film cells segment is anticipated to witness the fastest CAGR of 8.03% from 2026 to 2033, driven by ongoing innovations in lightweight photovoltaic materials, flexible solar modules, and building-integrated photovoltaic applications. Increasing research investments, improved manufacturing processes, and growing demand for portable and lightweight solar solutions are expected to create significant growth opportunities during the forecast period.

- By Application

On the basis of application, the global polycrystalline solar cell (Multi Si) market is segmented into residential, commercial, industrial, and power utilities. The power utilities segment dominated the market with an estimated 46.82% share in 2025, owing to increasing investments in utility-scale solar power generation projects, supportive renewable energy policies, and growing global electricity demand. Large-scale deployment of photovoltaic power plants by utilities and independent power producers continues to drive significant demand for cost-effective polycrystalline solar cells across major renewable energy markets.

The commercial segment is expected to register the fastest CAGR of 7.12% from 2026 to 2033, driven by increasing rooftop solar adoption across office buildings, educational institutions, hospitals, shopping complexes, and industrial facilities. Rising corporate sustainability initiatives, favorable government incentives, and growing emphasis on reducing electricity costs and carbon emissions are expected to support robust market expansion throughout the forecast period.

Polycrystalline Solar Cell (Multi Si) Market Regional Analysis

The Asia-Pacific polycrystalline solar cell (Multi Si) market dominated the global market and accounted for the largest revenue share of 55.00% in 2025, supported by unparalleled manufacturing infrastructure, abundant polysilicon production capacity, and extensive deployment of utility-scale and distributed solar photovoltaic projects. China, India, Japan, South Korea, and Southeast Asian countries continue to invest heavily in renewable energy infrastructure to meet rising electricity demand and achieve carbon neutrality targets. Favorable government policies, declining manufacturing costs, increasing domestic installations, and continuous expansion of manufacturing capacities by leading solar companies continue to strengthen Asia-Pacific's leadership in the global market.

China Polycrystalline Solar Cell (Multi Si) Market Insight

The China polycrystalline solar cell (Multi Si) market dominates the Asia-Pacific region owing to its world-leading polysilicon production, integrated photovoltaic manufacturing ecosystem, and extensive utility-scale solar installations. The country continues to expand manufacturing capacity through significant investments in wafers, cells, and module production while supporting large-scale renewable energy deployment under its carbon neutrality objectives. Strong government support, technological innovation, and export competitiveness continue to reinforce China's position as the world's largest producer and consumer of polycrystalline solar cells.

India Polycrystalline Solar Cell (Multi Si) Market Insight

The India polycrystalline solar cell (Multi Si) market is witnessing robust growth due to increasing investments in utility-scale solar parks, expanding rooftop solar installations, and government initiatives such as the National Solar Mission and Production Linked Incentive (PLI) Scheme for domestic solar manufacturing. Rising electricity demand, ambitious renewable energy targets, and growing investments in domestic photovoltaic manufacturing are accelerating market expansion. Continued policy support and increasing adoption of grid-connected solar systems are expected to drive significant growth during the forecast period.

Middle East and Africa Polycrystalline Solar Cell (Multi Si) Market Insight

The Middle East & Africa polycrystalline solar cell (multi si) market is projected to register the fastest CAGR of 20.0% from 2026 to 2033, driven by rapidly expanding utility-scale solar projects, abundant solar irradiation, increasing investments in renewable energy infrastructure, and government initiatives aimed at diversifying national energy portfolios. Countries including Saudi Arabia, the United Arab Emirates, Egypt, Morocco, and South Africa are investing heavily in large-scale photovoltaic developments to meet rising electricity demand while reducing dependence on fossil fuels. Declining solar installation costs, increasing foreign direct investment, supportive policy frameworks, and growing public-private partnerships are expected to significantly accelerate market expansion across the region throughout the forecast period.

Saudi Arabia Polycrystalline Solar Cell (Multi Si) Market Insight

The Saudi Arabia polycrystalline solar cell (Multi Si) market is witnessing significant growth owing to the country's ambitious renewable energy targets under Vision 2030 and increasing investments in large-scale solar power projects. The government is actively expanding photovoltaic generation capacity to diversify its energy mix and reduce dependence on fossil fuels. Rising investments in domestic solar manufacturing, utility-scale solar parks, and grid infrastructure modernization are driving demand for cost-effective polycrystalline solar cells. Furthermore, favorable regulatory support and public-private partnerships continue to strengthen the country's position as a leading solar market in the Middle East.

U.A.E. Polycrystalline Solar Cell (Multi Si) Market Insight

The U.A.E. polycrystalline solar cell (Multi Si) market is experiencing robust growth, driven by increasing investments in utility-scale photovoltaic projects, ambitious clean energy strategies, and growing adoption of renewable energy technologies. Government initiatives such as the UAE Energy Strategy 2050 and large-scale solar developments are accelerating the deployment of solar power across the country. Continuous investments in smart grid infrastructure, energy storage systems, and sustainable urban development are further supporting market expansion. In addition, the country's commitment to achieving net-zero emissions is expected to create substantial opportunities for polycrystalline solar cell manufacturers during the forecast period.

Polycrystalline Solar Cell (Multi Si) Market Share

The polycrystalline solar cell (Multi Si) industry is primarily led by well-established companies, including:

- LONGi Green Energy Technology Co., Ltd. (China)

- Trina Solar Co., Ltd. (China)

- JA Solar Technology Co., Ltd. (China)

- JinkoSolar Holding Co., Ltd. (China)

- Canadian Solar Inc. (Canada)

- Risen Energy Co., Ltd. (China)

- Astronergy (CHINT New Energy Technology Co., Ltd.) (China)

- Talesun Solar Technologies Co., Ltd. (China)

- GCL System Integration Technology Co., Ltd. (China)

- Yingli Green Energy Holding Company Limited (China)

- First Solar, Inc. (U.S.)

- Hanwha Solutions Corporation (Qcells) (South Korea)

- Adani Solar (India)

- Waaree Energies Limited (India)

- Vikram Solar Limited (India)

- Tata Power Solar Systems Limited (India)

- RenewSys India Pvt. Ltd. (India)

- Premier Energies Limited (India)

- REC Group (Singapore)

- Meyer Burger Technology AG (Switzerland)

- Sharp Corporation (Japan)

- Panasonic Holdings Corporation (Japan)

- SunPower Corporation (U.S.)

- Neo Solar Power Corporation (Taiwan)

- Motech Industries Inc. (Taiwan)

Latest Developments in Polycrystalline Solar Cell (Multi Si) Market

- In May 2023, LONGi Green Energy, one of the world's leading solar technology companies, announced the global launch of its Hi-MO 7 photovoltaic module based on HPDC (High Performance and Hybrid Passivated Dual-Junction Cell) technology at the SNEC exhibition in Shanghai. The module delivers up to 580 W output with 22.5% conversion efficiency and is specifically designed for utility-scale solar power plants to reduce the levelized cost of electricity (LCOE) while improving long-term energy yield and reliability

- In September 2023, REC Group announced the launch of the REC Alpha Pure-RX Series, its highest-power residential solar panel based on advanced heterojunction (HJT) cell technology. Offering up to 470 W of output, the new module provides higher power density, lead-free construction, and improved sustainability, enabling homeowners to maximize rooftop solar generation while supporting the industry's transition toward higher-efficiency photovoltaic technologies

- In October 2023, LONGi Green Energy expanded the commercialization of its Hi-MO 7 module globally, highlighting its HPDC cell technology, improved conversion efficiency, enhanced reliability, and optimized module dimensions for utility-scale photovoltaic projects. The company stated that the product was developed to increase energy generation and lower lifetime system costs for large solar installations worldwide.

- In January 2025, Trina Solar announced that it had achieved a world record conversion efficiency of 25.44% for a large-area n-type heterojunction (HJT) solar module, as certified by Germany's Fraunhofer CalLab. The achievement demonstrates significant advancements in high-efficiency crystalline silicon photovoltaic technology and reinforces the industry's focus on improving module performance for next-generation solar energy systems Reuters:

- In September 2023, REC Group unveiled the REC Alpha Pure 2 alongside the Alpha Pure-RX Series at RE+ 2023. The new panel features lead-free construction, improved power output of up to 430 W, and heterojunction (HJT) technology designed to enhance residential solar system efficiency while supporting more sustainable photovoltaic manufacturing practices

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Polycrystalline Solar Cell Multi Si Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Polycrystalline Solar Cell Multi Si Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Polycrystalline Solar Cell Multi Si Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.