Global Polyethylene Terephthalate Pet Packaging Market

Market Size in USD Billion

USD

85.90 Billion

USD

126.91 Billion

2025

2033

USD

85.90 Billion

USD

126.91 Billion

2025

2033

| 2026 - 2033 | |

| USD 85.90 Billion | |

| USD 126.91 Billion | |

| % | |

|

Polyethylene Terephthalate (PET) Packaging Market Size

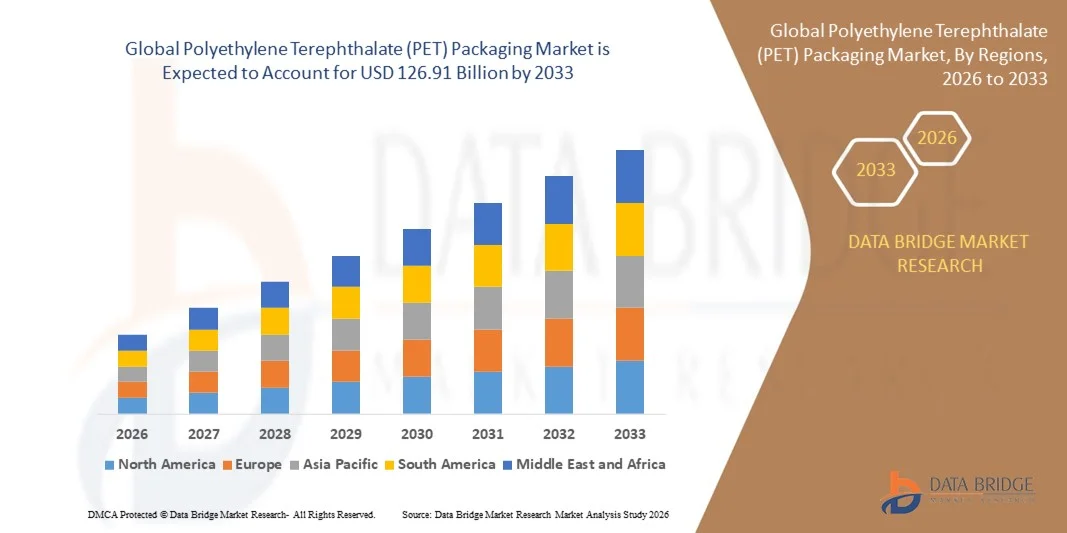

- The global polyethylene terephthalate (PET) packaging market size was valued at USD 85.90 billion in 2025 and is expected to reach USD 126.91 billion by 2033, at a CAGR of 5.00% during the forecast period

- The market growth is largely fuelled by the increasing demand for sustainable and lightweight packaging materials across the food and beverage, personal care, and pharmaceutical sectors

- The rising adoption of recyclable and reusable PET packaging solutions driven by environmental regulations and consumer preference for eco-friendly products is further propelling market expansion

Polyethylene Terephthalate (PET) Packaging Market Analysis

- The PET packaging market is witnessing robust growth due to its superior properties such as durability, chemical resistance, and versatility across multiple end-use industries

- Growing demand for packaged beverages, coupled with the expansion of e-commerce and urbanization, is further strengthening the adoption of PET packaging in global markets

- North America dominated the polyethylene terephthalate (PET) packaging market with the largest revenue share of 37.92% in 2025, driven by the extensive use of PET bottles in the beverage and food sectors and growing sustainability initiatives across the region

- Asia-Pacific region is expected to witness the highest growth rate in the global polyethylene terephthalate (PET) packaging market, driven by rising disposable incomes, increasing consumer shift toward convenient packaging formats, and government initiatives promoting sustainable packaging practices

- The bottles & jars segment held the largest market revenue share in 2025, driven by their extensive use in the beverage, food, and pharmaceutical industries due to their durability, transparency, and lightweight properties. The ability of PET bottles and jars to preserve product freshness and resist breakage makes them a preferred packaging solution across global markets

Report Scope and Polyethylene Terephthalate (PET) Packaging Market Segmentation

|

Attributes |

Polyethylene Terephthalate (PET) Packaging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Polyethylene Terephthalate (PET) Packaging Market Trends

Growing Adoption of Recycled PET (rPET) in Packaging Solutions

- The increasing emphasis on sustainability is driving widespread adoption of recycled polyethylene terephthalate (rPET) across industries such as food & beverage, cosmetics, and pharmaceuticals. Brands are prioritizing eco-friendly materials to meet corporate sustainability goals and align with global regulations on plastic waste reduction. This trend is fostering a circular economy approach, reducing environmental impact, and boosting rPET production capacity worldwide as companies focus on closing the material loop

- Government initiatives promoting plastic recycling and extended producer responsibility (EPR) programs are accelerating the transition toward rPET usage. Manufacturers are investing in advanced recycling technologies such as chemical depolymerization to enhance quality and clarity in recycled PET, making it suitable for high-end applications. These initiatives are supported by international collaborations and policy reforms designed to minimize landfill dependency and improve recycling efficiency across markets

- The cost-effectiveness and comparable performance of rPET compared to virgin PET are motivating packaging producers to incorporate higher recycled content in bottles, containers, and films. This not only reduces carbon footprints but also strengthens brand reputation among environmentally conscious consumers. The move toward circular packaging also helps companies meet carbon neutrality targets and align with global sustainability certifications and eco-labeling standards

- For instance, in 2024, several beverage companies in Europe announced the launch of 100% rPET bottles to meet EU packaging regulations and sustainability targets. These initiatives are setting new standards for responsible packaging practices and encouraging similar adoption across developing markets. The rapid expansion of rPET production facilities, especially in Asia-Pacific and North America, is expected to bridge supply gaps and meet growing industry demand

- While rPET adoption continues to gain momentum, ensuring a consistent supply of high-quality recycled material remains a challenge. Strengthening waste collection systems and improving recycling infrastructure will be key to scaling this sustainable trend globally. Collaboration between governments, producers, and recyclers is crucial to creating a closed-loop ecosystem that minimizes waste and supports long-term material sustainability

Polyethylene Terephthalate (PET) Packaging Market Dynamics

Driver

Increasing Demand for Lightweight and Durable Packaging Materials

- The rising need for lightweight, cost-efficient, and durable packaging solutions is propelling the demand for PET materials across multiple end-use sectors. PET packaging offers superior strength-to-weight ratio, excellent transparency, and chemical resistance, making it an ideal choice for beverages, personal care, and pharmaceutical products. The ability of PET to maintain product integrity while minimizing material use contributes significantly to sustainable and efficient packaging systems

- Manufacturers are increasingly adopting PET due to its recyclability and ability to reduce transportation costs. The material’s lightweight nature enables significant reductions in logistics expenses and carbon emissions, aligning with the global shift toward sustainable packaging. PET’s adaptability to different packaging formats further enhances its appeal, supporting cost efficiency and performance optimization for both rigid and flexible packaging applications

- Technological advancements in PET processing, such as improved stretch blow molding and barrier coating techniques, are further enhancing performance and extending product shelf life. These developments are broadening PET’s applicability in sectors demanding high-quality preservation such as dairy, beverages, and pharmaceuticals. Continuous R&D investments are also driving innovations in bio-based PET, which could further reduce environmental impacts and expand market potential

- For instance, in 2023, packaging producers introduced multi-layer PET containers designed for extended freshness and enhanced product protection, catering to growing demand in the food and beverage industry. These innovations are improving packaging efficiency, reducing waste, and providing brands with sustainable alternatives that do not compromise quality or consumer convenience. Manufacturers are increasingly integrating smart packaging features to improve functionality and user engagement

- Although PET remains a dominant packaging material, ongoing innovation is essential to address environmental concerns and increase recycling efficiency, ensuring long-term market competitiveness. Companies must focus on developing closed-loop systems, improving material traceability, and strengthening collection networks. The continuous evolution of PET packaging technologies will play a vital role in achieving circularity and reducing dependency on virgin plastic

Restraint/Challenge

Environmental Concerns and Fluctuating Raw Material Prices

- The environmental challenges associated with PET disposal and the limited efficiency of recycling systems continue to pose significant obstacles to market growth. Despite high recyclability potential, inadequate waste collection infrastructure often results in PET contributing to plastic pollution. Public and regulatory scrutiny over single-use plastics has increased pressure on packaging manufacturers to adopt greener, more sustainable alternatives

- Rising awareness of environmental sustainability and strict government regulations on single-use plastics are pressuring manufacturers to transition toward greener alternatives. However, achieving full-scale recycling remains difficult due to contamination issues and limited rPET processing capacities. The implementation of waste segregation systems and improved sorting technologies is necessary to address recycling inefficiencies and minimize plastic leakage into the environment

- Fluctuations in crude oil prices, which directly influence the cost of virgin PET resin, also create instability in production costs for packaging manufacturers. These price variations can impact profitability and disrupt supply chain planning for large-scale producers. Unpredictable raw material pricing also limits the ability of companies to maintain consistent pricing strategies, particularly in emerging markets with high consumption volumes

- For instance, in 2023, global PET resin prices surged due to supply constraints in feedstock materials such as PTA and MEG, leading to increased production costs for packaging companies. Manufacturers faced additional financial pressure as transportation costs and energy prices rose concurrently. These economic factors have reinforced the urgency for long-term supply contracts and diversification of raw material sources

- While the market continues to innovate in sustainable materials, overcoming recycling inefficiencies and stabilizing raw material supply chains will be critical to ensuring balanced and environmentally responsible PET packaging growth. Collaboration between governments, recyclers, and producers will play a key role in minimizing risks and promoting a more circular and cost-stable packaging economy

Polyethylene Terephthalate (PET) Packaging Market Scope

The global polyethylene terephthalate (PET) packaging market is segmented on the basis of pack type, form, filling technology, packaging type, and end-use industry.

- By Pack Type

On the basis of pack type, the PET packaging market is segmented into bottles & jars, bags & pouches, trays, and lids/caps & closures. The bottles & jars segment held the largest market revenue share in 2025, driven by their extensive use in the beverage, food, and pharmaceutical industries due to their durability, transparency, and lightweight properties. The ability of PET bottles and jars to preserve product freshness and resist breakage makes them a preferred packaging solution across global markets.

The bags & pouches segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the rising demand for flexible and portable packaging formats. These PET-based pouches are gaining popularity due to their convenience, lower material usage, and compatibility with modern filling technologies. The shift toward lightweight, space-efficient packaging is further fueling the adoption of PET bags and pouches, particularly in ready-to-eat and on-the-go food categories.

- By Form

On the basis of form, the PET packaging market is segmented into amorphous PET and crystalline PET. The amorphous PET segment accounted for the largest revenue share in 2025, attributed to its excellent clarity, flexibility, and ease of thermoforming, which make it ideal for various packaging applications. Its superior transparency allows for enhanced product visibility, a key factor driving demand in the food, beverage, and personal care industries.

The crystalline PET segment is projected to witness the fastest growth rate from 2026 to 2033, driven by its superior mechanical strength, temperature resistance, and chemical stability. Crystalline PET is increasingly used in applications requiring high durability and barrier properties, such as hot-fill beverage containers and pharmaceutical packaging. The segment’s expansion is further supported by innovations in crystallization technology and the development of recyclable high-performance PET materials.

- By Filling Technology

On the basis of filling technology, the PET packaging market is segmented into hot fill, cold fill, aseptic fill, and others. The cold fill segment dominated the market in 2025, primarily due to its extensive application in carbonated soft drinks, water bottles, and dairy packaging. Cold filling ensures product integrity without compromising material performance, making it a preferred choice among beverage manufacturers.

The aseptic fill segment is expected to grow at the fastest rate from 2026 to 2033, fuelled by rising demand for extended shelf-life packaging and contamination-free solutions. This technology is widely used for packaging juices, dairy products, and nutraceutical beverages that require sterile conditions. The growth of the aseptic fill segment is further supported by advancements in sterile barrier coatings and energy-efficient filling equipment.

- By Packaging Type

On the basis of packaging type, the PET packaging market is segmented into flexible packaging and rigid packaging. The rigid packaging segment held the largest revenue share in 2025 due to its structural strength, superior barrier properties, and extensive use in beverages and personal care products. PET rigid packaging offers high impact resistance and recyclability, which enhances its suitability for high-volume commercial applications.

The flexible packaging segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing demand for lightweight, cost-efficient, and sustainable packaging formats. Flexible PET packaging provides better material utilization and transport efficiency, catering to the growing e-commerce and convenience food sectors. This segment’s growth is also supported by the ongoing development of recyclable and bio-based PET films.

- By End-Use Industry

On the basis of end-use industry, the PET packaging market is segmented into food & beverages, pharmaceutical, personal care & cosmetic, and others. The food & beverages segment dominated the market in 2025, driven by high consumption of packaged water, carbonated drinks, and ready-to-eat products. PET’s clarity, safety, and versatility make it the material of choice for packaging a wide range of food and drink items globally.

The pharmaceutical segment is expected to witness the fastest growth rate from 2026 to 2033, owing to the increasing demand for safe, tamper-evident, and lightweight packaging solutions. PET is widely utilized for syrups, tablets, and healthcare products due to its excellent chemical resistance and non-reactive nature. Furthermore, the growing focus on hygienic and recyclable pharmaceutical packaging is accelerating PET adoption across global healthcare industries.

Polyethylene Terephthalate (PET) Packaging Market Regional Analysis

- North America dominated the polyethylene terephthalate (PET) packaging market with the largest revenue share of 37.92% in 2025, driven by the extensive use of PET bottles in the beverage and food sectors and growing sustainability initiatives across the region

- The strong presence of major beverage companies, coupled with advancements in recycling infrastructure and increased adoption of eco-friendly packaging solutions, is supporting market expansion

- Moreover, high consumer demand for lightweight, durable, and recyclable packaging materials is further boosting the region’s PET packaging adoption across multiple industries

U.S. Polyethylene Terephthalate (PET) Packaging Market Insight

The U.S. PET packaging market captured the largest revenue share in 2025 within North America, fuelled by strong demand from the food and beverage sector and the presence of leading packaging manufacturers. The rapid adoption of recycled PET (rPET) materials, combined with government regulations promoting sustainability, is driving significant market growth. Increasing consumption of bottled water, carbonated drinks, and ready-to-eat food products continues to reinforce the country’s dominance in the PET packaging segment.

Europe Polyethylene Terephthalate (PET) Packaging Market Insight

The Europe PET packaging market is expected to witness steady growth from 2026 to 2033, driven by stringent EU regulations promoting recycling and circular economy practices. European consumers and manufacturers are shifting toward sustainable packaging alternatives, with PET and rPET emerging as preferred materials due to their high recyclability. The beverage sector remains a major contributor, while the personal care and pharmaceutical industries are also increasingly adopting PET packaging solutions.

U.K. Polyethylene Terephthalate (PET) Packaging Market Insight

The U.K. PET packaging market is expected to witness robust growth from 2026 to 2033, driven by increased environmental awareness and the implementation of plastic recycling initiatives. The introduction of deposit return schemes (DRS) and the rising adoption of rPET bottles are strengthening market demand. The expanding ready-to-drink and on-the-go food sectors are further enhancing the utilization of PET packaging across the country.

Germany Polyethylene Terephthalate (PET) Packaging Market Insight

The Germany PET packaging market is expected to witness substantial growth from 2026 to 2033, supported by strong recycling infrastructure and advanced packaging technologies. German manufacturers are focusing on developing lightweight, recyclable, and high-barrier PET packaging for beverages and food applications. The increasing shift toward sustainability and the growing emphasis on reducing carbon emissions are further encouraging the adoption of rPET materials.

Asia-Pacific Polyethylene Terephthalate (PET) Packaging Market Insight

The Asia-Pacific PET packaging market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid industrialization, population growth, and increasing demand for packaged consumer goods in countries such as China, India, and Japan. The growing beverage industry, expansion of e-commerce, and rising investments in packaging innovation are significantly boosting market growth. Moreover, favorable government policies promoting recycling and sustainability are further propelling the market.

China Polyethylene Terephthalate (PET) Packaging Market Insight

The China PET packaging market accounted for the largest revenue share in Asia-Pacific in 2025, supported by high production capacities, growing consumption of packaged beverages, and expanding urbanization. The government’s emphasis on sustainable packaging and the strong presence of domestic PET resin producers are key drivers of market expansion. In addition, the growing use of rPET materials and the increasing demand for flexible packaging formats are accelerating market growth in China.

Japan Polyethylene Terephthalate (PET) Packaging Market Insight

The Japan PET packaging market is expected to witness steady growth from 2026 to 2033, driven by technological advancements in packaging design and the country’s strong focus on recycling efficiency. The beverage sector, particularly bottled water and functional drinks, represents a major demand source for PET packaging. The emphasis on lightweight materials and high-quality packaging aesthetics further supports Japan’s position as a key market within the region.

Polyethylene Terephthalate (PET) Packaging Market Share

The Polyethylene Terephthalate (PET) Packaging industry is primarily led by well-established companies, including:

• Amcor Plc (Switzerland)

• Graham Packaging Company (U.S.)

• RESILUX NV (Belgium)

• Gerresheimer AG (Germany)

• GTX HANEX Plastic Sp. z o.o. (Poland)

• Cospack America Corp (U.S.)

• BERICAP (Germany)

• Berry Global Inc. (U.S.)

• Ontario Plastic Container Producers Ltd (Canada)

• Alpha Packaging (U.S.)

• Alpack (Ireland)

• Plastipak Holdings, Inc. (U.S.)

• ExoPackaging (U.K.)

• WestRock Company (U.S.)

• Silgan Plastics (U.S.)

• Retal Industries LTD. (Lithuania)

• ALPLA (Austria)

• Esterform Ltd (U.K.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Polyethylene Terephthalate Pet Packaging Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Polyethylene Terephthalate Pet Packaging Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Polyethylene Terephthalate Pet Packaging Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.