Global Polyisobutylene Market

Market Size in USD Billion

USD

2.37 Billion

USD

3.59 Billion

2025

2033

USD

2.37 Billion

USD

3.59 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.37 Billion | |

| USD 3.59 Billion | |

| % | |

|

Polyisobutylene Market Size

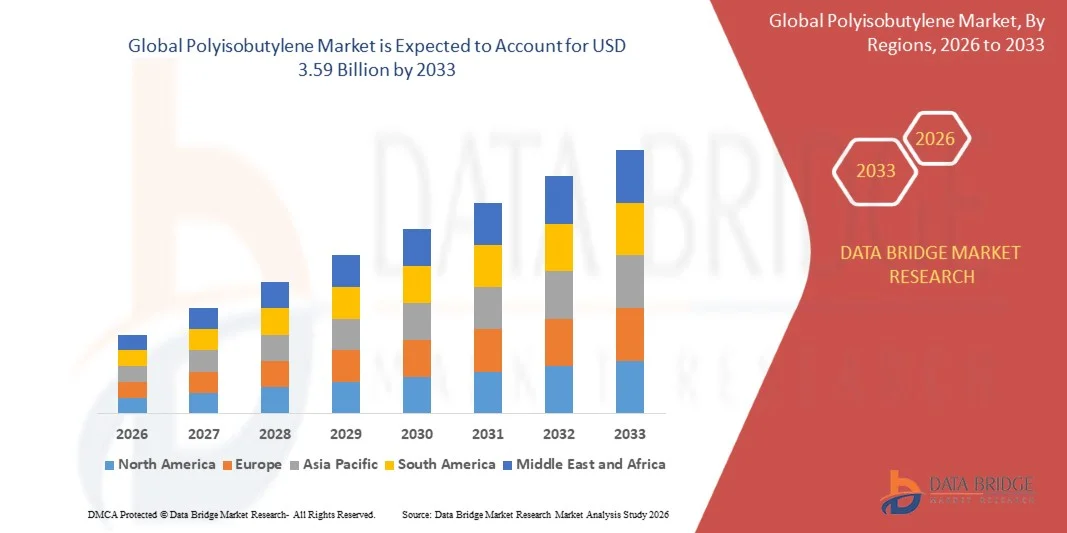

- The global polyisobutylene market size was valued at USD 2.37 billion in 2025 and is expected to reach USD 3.59 billion by 2033, at a CAGR of 5.35% during the forecast period

- The market growth is largely driven by increasing demand for high-performance lubricants, fuel additives, adhesives, and sealants across automotive, industrial, and construction sectors. Rising requirements for enhanced durability, efficiency, and chemical stability in these applications are accelerating the adoption of polyisobutylene globally

- Furthermore, growing automotive production, industrialization, and infrastructure development in emerging economies are boosting demand for PIB-based products. For instance, TPC Group and BASF have expanded their PIB production capacities to meet rising global requirements for medium and high molecular weight PIB used in lubricants, sealants, and adhesive applications

Polyisobutylene Market Analysis

- Polyisobutylene, a versatile synthetic polymer, is widely utilized in lubricants, adhesives, sealants, and personal care products due to its high viscosity index, chemical stability, and moisture barrier properties, making it essential in industrial and consumer applications

- The growing demand for polyisobutylene is primarily fueled by increasing automotive production, rising pharmaceutical and cosmetic formulations, and expanding packaging applications, driven by the need for high-performance and long-lasting material solutions

- Asia-Pacific dominated the polyisobutylene market with a share of 37.2% in 2025, due to strong growth in automotive production, increasing demand for lubricants and fuel additives, and the presence of large-scale chemical manufacturing hubs

- North America is expected to be the fastest growing region in the polyisobutylene market during the forecast period due to increasing demand for high-performance lubricants, fuel additives, and industrial sealants

- High MW PIB segment dominated the market with a market share of 68.7% in 2025, due to its extensive usage in adhesives, sealants, and rubber modification applications where superior viscosity and elasticity are critical. High MW PIB offers excellent impermeability and flexibility, making it highly suitable for applications such as tire inner liners and construction sealants. Its ability to enhance durability and resistance to environmental factors has further strengthened its adoption across industrial sectors

Report Scope and Polyisobutylene Market Segmentation

|

Attributes |

Polyisobutylene Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Polyisobutylene Market Trends

“Rising Demand for High-Performance Adhesives and Sealants”

- A significant trend in the polyisobutylene market is the increasing adoption of this polymer in high-performance adhesives, sealants, and coatings, driven by its superior chemical stability, moisture barrier properties, and flexibility across industries such as automotive, construction, and packaging. This rising application is positioning polyisobutylene as a critical material for products that require long-lasting adhesion and durability

- For instance, BASF supplies polyisobutylene-based adhesives for automotive assembly and packaging solutions, enhancing product strength and environmental resistance. Such applications are improving the reliability of bonded joints and extending the service life of end-use products

- The demand for polyisobutylene in personal care products is growing as formulations for hair styling gels, lip balms, and skin-care ointments benefit from its viscosity-modifying and film-forming properties. This is elevating its role as an essential ingredient in cosmetic and pharmaceutical industries where product performance is critical

- The packaging industry is increasingly incorporating polyisobutylene in flexible packaging films and moisture-resistant layers to improve barrier properties against gases and water vapor. This trend supports longer shelf life for food and pharmaceutical products while meeting stringent quality standards

- Industrial applications are expanding where polyisobutylene serves as a key component in lubricants, greases, and fuel additives, providing improved thermal stability and low volatility. The integration of polyisobutylene in these formulations is enhancing equipment efficiency and fuel performance across automotive and manufacturing sectors

- The market is witnessing robust growth in advanced sealant solutions where polyisobutylene contributes to chemical resistance and structural integrity in construction and marine applications. This rising utilization underlines its strategic importance in high-performance material solutions across global industries

Polyisobutylene Market Dynamics

Driver

“Growing Adoption in Automotive and Packaging Applications”

- The expanding automotive and packaging sectors are driving the demand for polyisobutylene due to its ability to improve fuel efficiency, reduce emissions, and enhance material durability. Its use in adhesives, sealants, and lubricants supports lightweight vehicle components and robust packaging solutions

- For instance, ExxonMobil produces polyisobutylene for fuel additive formulations that improve engine performance and reduce oil consumption in automotive applications. Such solutions reinforce the polymer’s value proposition and drive consistent adoption in performance-critical industries

- Increasing production of flexible packaging films for pharmaceuticals, food, and consumer goods is boosting the requirement for polyisobutylene-based materials that enhance moisture and oxygen barrier properties. These applications support regulatory compliance and extend product shelf life

- The rising focus on environmentally stable and chemically resistant adhesives in the automotive and industrial sectors is strengthening market growth. Polyisobutylene’s ability to maintain performance under temperature fluctuations and chemical exposure underpins its expanding use

- The adoption of polyisobutylene in specialty lubricants and greases for industrial machinery and transportation equipment is growing, ensuring smoother operation and reduced maintenance costs. This driver continues to support market expansion by providing value-added performance benefits

Restraint/Challenge

“Fluctuating Raw Material Prices and Supply Chain Constraints”

- The polyisobutylene market faces challenges due to volatility in raw material availability, particularly C4 fraction feedstocks derived from crude oil, which affects production costs and supply stability. Such fluctuations can impact pricing strategies and long-term contracts across industries

- For instance, LyondellBasell has reported production cost variations due to changes in n-butene feedstock prices, affecting the supply of polyisobutylene for adhesives and fuel additives. These constraints necessitate careful procurement and risk management strategies

- The dependence on petrochemical-derived feedstocks exposes the market to geopolitical tensions and fluctuating crude oil prices, influencing overall market dynamics and profitability

- Supply chain disruptions, including logistics challenges and production bottlenecks, can lead to delays in delivering high-demand polyisobutylene grades for automotive and packaging applications

- The market must continuously manage operational efficiency and inventory strategies to mitigate the effects of raw material price volatility and maintain consistent supply to key end-use industries

Polyisobutylene Market Scope

The market is segmented on the basis of molecular weight, product, application, and end-user.

• By Molecular Weight

On the basis of molecular weight, the polyisobutylene market is segmented into low MW PIB, medium MW PIB, and high MW PIB. The high molecular weight PIB segment dominated the market with the largest market revenue share of 68.7% in 2025, driven by its extensive usage in adhesives, sealants, and rubber modification applications where superior viscosity and elasticity are critical. High MW PIB offers excellent impermeability and flexibility, making it highly suitable for applications such as tire inner liners and construction sealants. Its ability to enhance durability and resistance to environmental factors has further strengthened its adoption across industrial sectors. In addition, increasing demand from automotive and infrastructure industries continues to reinforce its leading position.

The low molecular weight PIB segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by its rising demand in lubricant and fuel additive applications. Low MW PIB provides excellent dispersant and viscosity-modifying properties, making it highly suitable for modern engine formulations aimed at improving fuel efficiency and reducing emissions. Growing regulatory focus on cleaner fuels and high-performance lubricants is accelerating its adoption. Its ease of blending and compatibility with other additives further enhances its application scope. Increasing demand from automotive and industrial lubrication sectors is expected to drive strong growth in this segment.

• By Product

On the basis of product, the polyisobutylene market is segmented into conventional PIB and highly reactive PIB. The highly reactive PIB segment dominated the market with the largest market revenue share in 2025, driven by its superior reactivity and efficiency in producing dispersants and detergent additives for fuels and lubricants. Highly reactive PIB enables better functionalization, which enhances engine cleanliness and performance. Its growing importance in meeting stringent emission norms and fuel efficiency standards has significantly boosted its demand. In addition, its widespread use in high-performance lubricant formulations has strengthened its market position. Increasing advancements in additive chemistry further support the segment’s dominance.

The conventional PIB segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its cost-effectiveness and broad applicability across industrial uses such as adhesives, sealants, and rubber processing. Conventional PIB offers stable performance characteristics, making it suitable for large-scale applications where high reactivity is not essential. Its established presence in traditional manufacturing processes continues to support demand. Growing infrastructure development and construction activities are further accelerating its adoption. The balance between performance and cost efficiency is expected to drive steady growth in this segment.

• By Application

On the basis of application, the polyisobutylene market is segmented into tires, lube additives, fuel additives, stroke engines, adhesives and sealants, industrial lubes, and others. The lube additives segment dominated the market with the largest market revenue share in 2025, driven by the increasing demand for high-performance lubricants in automotive and industrial machinery. PIB plays a crucial role in enhancing viscosity, oxidation stability, and deposit control in lubricants. Rising vehicle production and the need for improved engine efficiency have significantly contributed to segment growth. In addition, the shift toward longer oil drain intervals has increased reliance on advanced additive formulations. This has further strengthened the dominance of the lube additives segment.

The fuel additives segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the rising focus on fuel efficiency and emission reduction. PIB-based additives help in maintaining engine cleanliness and improving combustion efficiency, which is critical in modern engines. Increasing regulatory pressure on emissions and growing adoption of cleaner fuels are accelerating demand. The expansion of the automotive sector in emerging economies is also contributing to growth. Continuous innovation in additive technologies is expected to further boost this segment.

• By End-user

On the basis of end-user, the polyisobutylene market is segmented into transportation, industrial, food, and others. The transportation segment dominated the market with the largest market revenue share in 2025, driven by extensive use of PIB in automotive lubricants, fuel additives, and tire manufacturing. The growth of the automotive industry and increasing demand for fuel-efficient vehicles have significantly contributed to the segment’s dominance. PIB’s role in enhancing engine performance and durability makes it essential in transportation applications. In addition, rising vehicle production and maintenance activities continue to drive demand. Strong integration of PIB in multiple automotive components further supports its leading position.

The industrial segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing demand for adhesives, sealants, and industrial lubricants across manufacturing and construction sectors. Rapid industrialization and infrastructure development are key factors driving growth in this segment. PIB’s properties such as chemical stability and flexibility make it suitable for diverse industrial applications. Expanding use in machinery maintenance and processing industries is further supporting demand. Continuous growth in global industrial activities is expected to accelerate this segment’s expansion.

Polyisobutylene Market Regional Analysis

- Asia-Pacific dominated the polyisobutylene market with the largest revenue share of 37.2% in 2025, driven by strong growth in automotive production, increasing demand for lubricants and fuel additives, and the presence of large-scale chemical manufacturing hubs

- The region’s cost-effective production environment, rising investments in petrochemical infrastructure, and expanding demand for high-performance materials are accelerating market expansion

- Rapid industrialization, supportive government policies, and growing consumption across transportation and industrial sectors are contributing to increased demand for polyisobutylene

China Polyisobutylene Market Insight

China held the largest share in the Asia-Pacific polyisobutylene market in 2025, owing to its dominance in petrochemical production and extensive manufacturing capabilities. The country’s strong automotive industry, high demand for lubricants and fuel additives, and large-scale tire production are key growth drivers. Government support for industrial expansion and increasing exports of chemical products further strengthen market growth. Rising investments in refining and chemical processing facilities continue to boost domestic demand.

India Polyisobutylene Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, fueled by rapid industrialization, expanding automotive production, and increasing demand for lubricants and adhesives. Government initiatives promoting domestic manufacturing and infrastructure development are driving higher consumption of polyisobutylene. Growth in the transportation sector and rising demand for fuel-efficient vehicles are further supporting market expansion. Increasing investments in petrochemical capacity and specialty chemicals are also contributing to strong growth.

Europe Polyisobutylene Market Insight

The Europe polyisobutylene market is expanding steadily, supported by strong demand for high-performance lubricants, stringent environmental regulations, and advanced manufacturing capabilities. The region emphasizes sustainability and efficiency, leading to increased adoption of PIB in fuel additives and industrial applications. Growing demand from automotive and construction sectors is further supporting market growth. Continuous innovation in specialty chemicals is enhancing product development across industries.

Germany Polyisobutylene Market Insight

Germany’s polyisobutylene market is driven by its well-established automotive industry, strong chemical manufacturing base, and focus on high-quality engineering solutions. The country’s demand for advanced lubricants, sealants, and performance materials supports PIB consumption. Strong R&D capabilities and collaboration between chemical companies and industrial sectors foster continuous innovation. Export-oriented production further strengthens Germany’s position in the regional market.

U.K. Polyisobutylene Market Insight

The U.K. market is supported by demand from automotive maintenance, industrial lubricants, and construction applications. Increasing focus on sustainability and efficiency in industrial operations is driving the use of high-performance chemical materials. Growth in infrastructure development and industrial activities is contributing to rising demand. Investments in specialty chemicals and advanced material applications are further supporting market expansion.

North America Polyisobutylene Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing demand for high-performance lubricants, fuel additives, and industrial sealants. Strong presence of automotive and manufacturing industries, along with advancements in chemical processing technologies, are boosting demand. Rising focus on fuel efficiency and emission reduction is further accelerating adoption. Increasing investments in petrochemical and refining capacities are supporting regional growth.

U.S. Polyisobutylene Market Insight

The U.S. accounted for the largest share in the North America market in 2025, underpinned by its advanced petrochemical industry and strong demand for automotive and industrial applications. The country’s focus on high-performance lubricants, fuel additives, and specialty materials is driving PIB consumption. Presence of major industry players and well-developed supply chains supports market expansion. Continuous innovation and investment in refining and chemical production further strengthen the U.S. market position.

Polyisobutylene Market Share

The polyisobutylene industry is primarily led by well-established companies, including:

- China Petroleum & Chemical Corporation (China)

- Royal Dutch Shell Plc (U.K.)

- Eni S.p.A. (Italy)

- Evonik Industries AG (Germany)

- Ineos Group AG (U.K.)

- LANXESS (Germany)

- LG Chem (South Korea)

- LyondellBasell Industries Holdings B.V. (Netherlands)

- Repsol (Spain)

- SABIC (Saudi Arabia)

- Dow (U.S.)

- TPC Group (U.S.)

- Formosa Plastics Corporation, U.S.A. (U.S.)

- Borealis AG (Austria)

- Versalis S.p.A. (Italy)

- Kothari Petrochemicals (India)

Latest Developments in Global Polyisobutylene Market

- In September 2023, TPC Group completed the initial phase of its di-isobutylene (DIB) capacity upgrade, marking a significant step in its expansion strategy. This development enables the company to address the rising global demand for DIB, particularly driven by the increasing adoption of low global warming potential refrigerants. The upgraded capacity strengthens its ability to supply critical intermediates required for environmentally compliant applications. It also positions the company to align with evolving regulatory standards and sustainability trends in the chemical industry

- In August 2023, BASF announced a 25% increase in production capacity for its medium molecular weight polyisobutenes under the OPPANOL B brand at its Ludwigshafen facility in Germany. This expansion is driven by growing global demand for high-quality PIB used in applications such as sealants, protective films, and battery materials. The move enhances BASF’s ability to ensure consistent supply and meet the needs of expanding industrial and automotive sectors. It also reinforces the company’s position in the specialty chemicals market through capacity scaling and innovation

- In July 2023, Kraton Corporation introduced a new range of polyisobutylene (PIB)-based adhesives and sealants tailored for automotive and construction applications. These products are designed to deliver improved durability, flexibility, and resistance to environmental conditions. The launch aligns with the increasing demand for high-performance materials across end-use industries. It also reflects the company’s focus on innovation and development of advanced polymer-based solutions

- In July 2023, Omsky Kauchuk, a subsidiary of the Titan Group, initiated the construction of a 10-kiloton polyisobutylene (PIB) production plant along with a technical butane processing facility in Omsk. This initiative aims to reduce Russia’s reliance on imports and strengthen domestic production capabilities. Integration of butane processing with PIB manufacturing is expected to improve feedstock efficiency and operational performance. The use of domestic technologies further supports long-term sustainability and supply chain resilience

- In March 2023, Pidilite Industries announced plans to manufacture Jowat’s hot melt adhesives at its advanced facility in Vapi, Gujarat. This initiative supports localized production, reducing import dependence and enhancing supply chain efficiency. The products will be marketed under the Pidilite brand, leveraging its strong distribution network. It also enables the company to meet rising demand across packaging, automotive, and industrial applications while expanding its product portfolio

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Polyisobutylene Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Polyisobutylene Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Polyisobutylene Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.