Global Polyvinylidene Chloride Pvdc Food Packaging Market

Market Size in USD Billion

USD

1.00 Billion

USD

1.72 Billion

2025

2033

USD

1.00 Billion

USD

1.72 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.00 Billion | |

| USD 1.72 Billion | |

| % | |

|

What is the Global Polyvinylidene Chloride (PVDC) Food Packaging Market Size and Growth Rate?

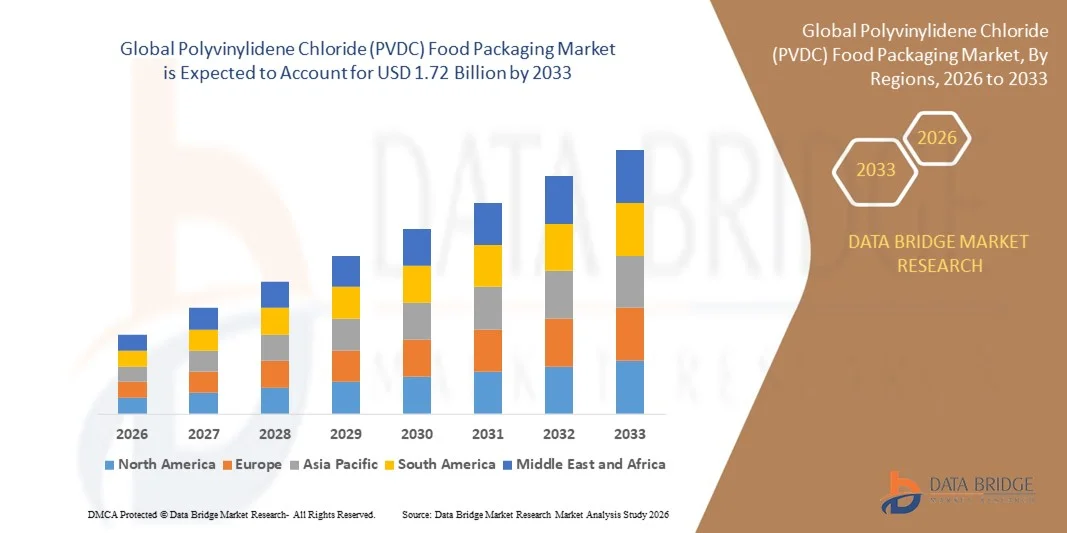

- The global polyvinylidene chloride (PVDC) food packaging market size was valued at USD 1.00 billion in 2025 and is expected to reach USD 1.72 billion by 2033, at a CAGR of 7.0% during the forecast period

- The growing levels of disposable income of the people, rapid urbanization across the globe, increasing demand for packaged food and beverages together with growing use of packaging material in various food service outlets, rising expansion of working population, increasing preferences towards the environment friendly product for food packaging such as packaging of processed meat, cheese, bread, snacks and the instant food are some of the major as well as important factors which will polyvinylidene chloride (PVDC) food packaging market

What are the Major Takeaways of Polyvinylidene Chloride (PVDC) Food Packaging Market?

- Increasing consumer preference for flexible packaging solutions that are easy to handle and transport along with changing consumer lifestyle which will further contribute by generating massive opportunities that will lead to the growth of the polyvinylidene chloride (PVDC) food packaging market

- Rising preferences towards the usages of BOPP along with high cost of product which will such asly to act as market restraints factor for the growth of the polyvinylidene chloride (PVDC) food packaging market

- North America dominated the polyvinylidene chloride (PVDC) food packaging market with the largest revenue share of 41.8% in 2025, driven by strong demand for high-barrier food packaging, convenience foods, and advanced sustainable film solutions

- Asia-Pacific is projected to witness the fastest CAGR of 11.62% during 2026–2033, fueled by urbanization, rising disposable incomes, and growth in processed and convenience foods across China, India, Japan, and South Korea

- The PVDC Resin segment dominated the market with the largest revenue share of 58.3% in 2025, driven by its superior barrier properties, chemical stability, and excellent resistance to oxygen and moisture

Report Scope and Polyvinylidene Chloride (PVDC) Food Packaging Market Segmentation

|

Attributes |

Polyvinylidene Chloride (PVDC) Food Packaging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Polyvinylidene Chloride (PVDC) Food Packaging Market?

Rising Focus on Sustainable, High-Barrier, and User-Friendly Packaging Solutions

- The polyvinylidene chloride (PVDC) food packaging market is witnessing a significant shift toward sustainability, enhanced barrier performance, and user convenience, driven by global initiatives to reduce food waste, extend shelf life, and meet eco-conscious consumer demands. Manufacturers are increasingly adopting recyclable, mono-material, and compostable PVDC-based films that align with circular economy principles

- For instance, Amcor plc and Berry Global have developed PVDC-coated films with excellent oxygen and moisture barrier properties, enabling longer product freshness while being compatible with recyclable PET or PE structures. These innovations allow manufacturers to maintain product quality and reduce environmental impact

- Growing consumer preference for convenient, easy-to-open, and resealable packaging is driving demand for PVDC films that combine functionality with high performance. Ready-to-eat meals, chilled meats, and dairy products are witnessing strong adoption

- Advanced multilayer extrusion, coating, and sealing technologies are being integrated into PVDC films to enhance peelability, contamination resistance, and overall packaging aesthetics. These technologies also improve operational efficiency during packing and filling

- Increasing focus on lightweight, minimalist designs, and adherence to sustainability regulations such as the EU Packaging and Packaging Waste Directive (PPWD) and Extended Producer Responsibility (EPR) initiatives is accelerating the adoption of eco-friendly PVDC packaging

- As demand for high-performance, sustainable, and consumer-friendly packaging continues to rise, PVDC films with recyclable and barrier-enhancing functionalities will remain the defining trend shaping the global market

What are the Key Drivers of Polyvinylidene Chloride (PVDC) Food Packaging Market?

- Rising consumption of packaged, ready-to-eat, and convenience foods is a major driver of the PVDC Food Packaging market. Consumers increasingly seek packaging that ensures freshness, hygiene, and ease of use, particularly in the dairy, meat, and frozen food sectors

- For instance, Sealed Air Corporation reported increased adoption of PVDC-coated Cryovac films in 2025 across North America and Europe due to heightened packaged food demand and extended shelf-life requirements

- Growing environmental awareness and sustainability initiatives are prompting manufacturers to adopt recyclable, mono-material PVDC films to reduce waste and improve circularity in packaging

- Technological innovations in polymer chemistry, co-extrusion, and multilayer lamination have improved PVDC film clarity, oxygen and moisture barrier properties, and peel performance, making them suitable for diverse applications, including food, pharmaceutical, and healthcare packaging

- Expansion of e-commerce, home delivery services, and retail-ready packaging is driving demand for durable, tamper-evident, and easy-to-open PVDC films, supporting the market’s shift toward consumer-centric solutions

- Continuous innovation in PVDC film formulations, barrier performance, and recyclability will sustain global market growth as industries prioritize eco-friendly and high-performing packaging

Which Factor is Challenging the Growth of the Polyvinylidene Chloride (PVDC) Food Packaging Market?

- High material and manufacturing costs associated with PVDC films pose a key challenge for market expansion. Specialized coatings, multilayer lamination, and advanced extrusion technologies increase production complexity and expenses

- Smaller converters in Asia-Pacific and Europe have reported difficulties in competing with large multinational producers due to cost disparities with conventional, non-recyclable films

- Regulatory fragmentation and recycling limitations across regions hinder standardized adoption. Variations in packaging waste management systems, particularly in the U.S., EU, and Asia, complicate the implementation of sustainable PVDC solutions

- Technical constraints in maintaining barrier integrity, heat resistance, and peel strength during recycling further restrict scalability. Manufacturers often struggle to balance environmental goals with product safety and shelf-life requirements

- Volatility in raw material pricing, especially for bio-based or specialty PVDC resins, adds financial uncertainty and limits widespread adoption by smaller firms

- Leading market players are addressing these challenges through strategic R&D, collaborative ventures, and automated extrusion technologies that improve cost-efficiency. Over time, standardized recycling frameworks and scalable PVDC innovations are expected to mitigate barriers and drive sustainable growth globally

How is the Polyvinylidene Chloride (PVDC) Food Packaging Market Segmented?

The market is segmented on the basis of product, application, and end use.

- By Product

On the basis of product, the polyvinylidene chloride (PVDC) food packaging market is segmented into PVDC Latex and PVDC Resin. The PVDC Resin segment dominated the market with the largest revenue share of 58.3% in 2025, driven by its superior barrier properties, chemical stability, and excellent resistance to oxygen and moisture, which make it ideal for high-performance food packaging applications. PVDC Resin is widely used in multilayer films for fresh and processed foods, ensuring extended shelf life and product quality. Its compatibility with recyclable and monomaterial structures has further strengthened adoption among manufacturers prioritizing sustainability without compromising functionality.

The PVDC Latex segment is expected to register the fastest CAGR from 2026 to 2033, fueled by rising demand for flexible coatings, enhanced adhesion, and cost-effective film solutions. PVDC Latex is increasingly utilized in specialty applications requiring lightweight, eco-conscious, and high-barrier film solutions globally.

- By Application

On the basis of application, the market is categorized into Multilayer Film, Monolayer Film, and PVDC Coated Film. The Multilayer Film segment dominated the market with a revenue share of 53.9% in 2025, due to its ability to combine PVDC with other polymers such as PE, PET, and PA to create high-barrier, heat-sealable, and durable films suitable for processed foods, chilled meats, and ready-to-eat products. Multilayer structures also facilitate compatibility with recycling initiatives while ensuring extended shelf life, making them highly preferred by global packaging manufacturers.

The PVDC Coated Film segment is expected to witness the fastest CAGR from 2026 to 2033, driven by its increasing application in lightweight, flexible, and sustainable packaging solutions. Coated films provide improved adhesion, enhanced moisture and oxygen resistance, and compatibility with printing and labeling technologies, making them suitable for dairy, bakery, and snack packaging applications.

- By End Use

On the basis of end use, the market is segmented into Dairy Products, Fruit and Vegetables, Pet Food, Baby Food, Confectionery, Meat, Poultry and Seafood, and Others. The Dairy Products segment dominated the market with the largest revenue share of 47.6% in 2025, owing to high adoption of PVDC packaging to preserve freshness, prevent contamination, and extend shelf life of milk, cheese, yogurt, and other processed dairy items. PVDC’s superior barrier and sealing properties, coupled with lightweight and flexible film formats, have reinforced its dominance in dairy packaging globally.

The Baby Food segment is projected to grow at the fastest CAGR from 2026 to 2033, supported by increasing demand for safe, tamper-evident, and eco-friendly packaging solutions for infant nutrition products. Manufacturers are increasingly employing PVDC multilayer and coated films to maintain product integrity, comply with stringent regulatory standards, and cater to evolving consumer expectations in emerging and developed markets.

Which Region Holds the Largest Share of the Polyvinylidene Chloride (PVDC) Food Packaging Market?

- North America dominated the polyvinylidene chloride (PVDC) food packaging market with the largest revenue share of 41.8% in 2025, driven by strong demand for high-barrier food packaging, convenience foods, and advanced sustainable film solutions

- The region’s focus on recyclable, tamper-evident, and user-friendly packaging formats is promoting widespread adoption across food, dairy, pharmaceutical, and industrial sectors. Stringent regulatory frameworks, including the U.S. Food and Drug Administration (FDA) and Canadian Food Inspection Agency (CFIA) standards, reinforce food safety, barrier protection, and sustainability compliance

- Continuous innovations in multilayer films, peelable coatings, and mono-material recyclable structures are bolstering North America’s leadership in the global PVDC Food Packaging market

U.S. Market Insight

The U.S. held the largest share within North America in 2025, supported by rising packaged food consumption, e-commerce growth, and demand for tamper-evident packaging. Companies such as Berry Global Inc. (U.S.) and Amcor plc (Australia) are investing in recyclable PE- and PET-based films to comply with sustainability targets. Easy peel, resealable, and high-barrier packaging is increasingly adopted across dairy, bakery, and ready-to-eat segments, driving innovation and market expansion.

Canada Market Insight

Canada contributes significantly, backed by a strong food processing sector, advanced recycling infrastructure, and initiatives to eliminate single-use plastics by 2030. Demand is particularly high for meat, dairy, and bakery packaging, with easy peel PVDC films ensuring freshness and safety. Manufacturers are aligning packaging innovations with Extended Producer Responsibility (EPR) programs, positioning Canada as a sustainability-driven hub.

Asia-Pacific Polyvinylidene Chloride (PVDC) Food Packaging Market Insight

Asia-Pacific is projected to witness the fastest CAGR of 11.62% during 2026–2033, fueled by urbanization, rising disposable incomes, and growth in processed and convenience foods across China, India, Japan, and South Korea. Regional manufacturers are increasingly adopting polyolefin-based, biodegradable, and recyclable films to meet international sustainability standards. Investments from global players such as Mondi Group (Austria) and Toray Plastics are enhancing production capacity and technological innovation. Cost-effective manufacturing and evolving consumer preferences make Asia-Pacific the most dynamic region for PVDC Food Packaging growth globally.

China Market Insight

China is emerging as a regional leader, driven by its robust manufacturing base, export-oriented food industry, and focus on sustainable PVDC and multilayer films. Increasing environmental awareness is accelerating development of biodegradable and mono-material structures, aligning with government green packaging policies.

India Market Insight

India is witnessing rapid growth supported by the expansion of FMCG, food processing, and pharmaceutical sectors. Government initiatives such as “Make in India” and bans on single-use plastics are stimulating demand for recyclable, lightweight, and resealable PVDC film solutions. Adoption by emerging brands and expanding retail infrastructure are expected to sustain market growth.

Europe Polyvinylidene Chloride (PVDC) Food Packaging Market Insight

Europe is growing steadily due to strict environmental regulations and adoption of recyclable mono-material films under the EU Packaging and Packaging Waste Directive (PPWD). Rising consumer demand for convenience and eco-friendly packaging, particularly in ready-to-eat foods, dairy, and pharmaceuticals, is driving growth. Countries such as Germany, France, and the U.K. are leading sustainable packaging innovations.

Germany Market Insight

Germany leads Europe with a strong manufacturing base and stringent sustainability regulations. Domestic production is rising due to packaged food and medical packaging demand. Investments in PET- and PE-based mono-material structures improve recyclability and reduce waste, supporting the country’s position as a green packaging hub.

U.K. Market Insight

The U.K. market is expanding steadily, fueled by consumer demand for convenient, sustainable, and premium packaging formats. Post-Brexit regulatory flexibility allows domestic innovation in compostable and recyclable easy peel films. Growth is further supported by food delivery, pharmaceutical, and personal care sectors, alongside the Plastic Packaging Tax driving sustainability-focused material adoption.

Which are the Top Companies in Polyvinylidene Chloride (PVDC) Food Packaging Market?

The Polyvinylidene Chloride (PVDC) Food Packaging industry is primarily led by well-established companies, including:

- Innovia Films Ltd (U.K.)

- Bilcare Limited (India)

- Sealed Air (U.S.)

- Perlen Packaging (Switzerland)

- Krehalon B.V. (Netherlands)

- Kureha Corporation (Japan)

- Caprihans India Limited (India)

- Marubeni Europe plc (U.K.)

- TSI (Italy)

- ACG (India)

- Cosmo Films Ltd (India)

- Interni Film (Italy)

- Jindal Poly Films (India)

- SD PACK CO., LTD (South Korea)

- Toray Plastics (America), Inc. (U.S.)

- Solvay (Belgium)

- Asahi Kasei Home Products Corporation (Japan)

What are the Recent Developments in Global Polyvinylidene Chloride (PVDC) Food Packaging Market?

- In January 2024, Kureha Corporation announced a JPY 10.00 billion (~ USD 70.0 million) investment in R&D targeting next-generation PVDC materials, aiming to enhance sustainability by developing thinner coatings with improved barrier performance and greater compatibility with recycling infrastructure. This initiative is expected to strengthen Kureha’s position in eco-friendly PVDC innovations globally

- In October 2023, Solvay introduced Diofan Ultra736, a next-generation PVDC coating for pharmaceutical blister films, offering ultra-high water‑vapor barrier protection while remaining thermally formable. As an aqueous, fluorine-free dispersion compliant with direct pharmaceutical contact, it provides strong oxygen barrier, transparency, and chemical resistance, enabling producers to design thinner, lighter packaging structures without sacrificing performance. This launch reinforces Solvay’s commitment to advanced, sustainable pharmaceutical packaging solutions

- In April 2022, Jindal Poly Films, a wholly owned subsidiary of Jindal PolyPack, acquired SMI Coated Products, expanding its offerings in labels and related products. Jindal PolyPack, which operates the world’s largest production sites for BOPP and BOPET films, leveraged this acquisition to strengthen its market presence and diversify its portfolio

- In April 2022, Cosmo Films Ltd. announced plans to establish a cast polypropylene production plant in Aurangabad with an annual capacity of 25,000 million tonnes, aimed at expanding the company’s manufacturing footprint. This project is expected to enhance Cosmo Films’ production capabilities and support growth in high-demand packaging markets

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Polyvinylidene Chloride Pvdc Food Packaging Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Polyvinylidene Chloride Pvdc Food Packaging Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Polyvinylidene Chloride Pvdc Food Packaging Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.