Global Pompe Disease Market

Market Size in USD Billion

USD

1.70 Billion

USD

2.51 Billion

2025

2033

USD

1.70 Billion

USD

2.51 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.70 Billion | |

| USD 2.51 Billion | |

| % | |

|

Pompe Disease Market Overview

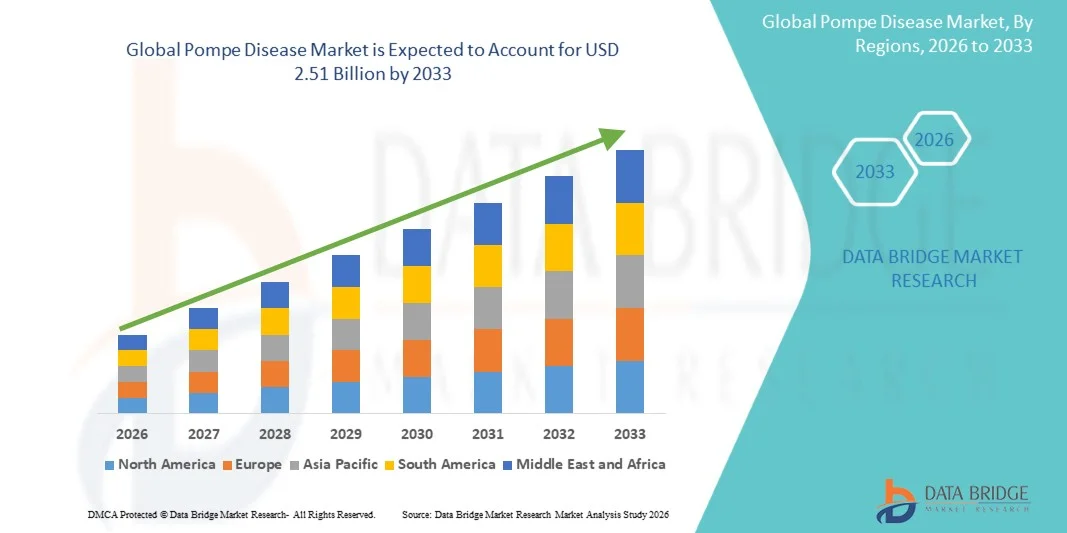

The Pompe Disease Market was valued at USD 1.70 billion in 2025 and is projected to reach USD 2.51 billion by 2033, growing at a CAGR of 5.00% from 2026 to 2033. The Pompe Disease Market is experiencing consistent growth driven by rising awareness regarding rare genetic disorders, increasing diagnosis rates, advancements in enzyme replacement therapies, and growing investments in rare disease research and treatment development. The expanding availability of newborn screening programs, improved genetic testing capabilities, and increasing focus on early disease identification are encouraging healthcare providers and patients to adopt advanced Pompe disease management solutions.

The growing prevalence of late-onset and infantile Pompe disease cases, combined with advancements in targeted therapies and supportive care approaches, is increasing demand for innovative treatment options globally. Enzyme replacement therapies (ERT), next-generation therapies, and emerging gene therapy approaches are transforming disease management by improving patient outcomes and slowing disease progression. In addition, increasing government initiatives for rare disease treatment, expansion of specialized healthcare centers, and rising collaborations between pharmaceutical companies and research organizations are further supporting the growth of the Pompe Disease Market.

Key Market Trends & Insights

- North America dominated the Pompe Disease Market with the largest revenue share of 3% in 2025, supported by advanced healthcare infrastructure, early adoption of innovative rare disease therapies, strong diagnostic capabilities, and the presence of leading pharmaceutical companies developing enzyme replacement therapies. The region benefits from improved access to genetic testing, newborn screening programs, specialized metabolic disorder centers, and favorable reimbursement frameworks that support long-term Pompe disease management.

- The Parenteral segment dominated the market with a 91.5% share in 2025, due to the extensive use of intravenous enzyme replacement therapies in Pompe disease treatment

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.7% from 2026 to 2033, fueled by improving rare disease awareness, expanding healthcare infrastructure, increasing availability of genetic diagnostics, and rising investments in specialized treatment centers across countries such as China, India, and Japan. Government initiatives supporting rare disease management and increasing access to advanced therapies are further accelerating regional growth.

- The Genetic Test segment dominated the diagnosis category with revenue share in 2025, due to its high accuracy in confirming GAA gene mutations associated with Pompe disease, increasing adoption in rare disease diagnosis, and growing use of molecular testing for early detection and family screening.

- The Enzyme Replacement Therapy (ERT) segment accounted for the largest share of the treatment category with revenue share in 2025, driven by its established role as the standard treatment approach for Pompe disease. Increasing availability of therapies such as alglucosidase alfa and next-generation enzyme replacement treatments continues to support segment dominance by improving patient survival and disease management outcomes.

- Specialty Centres dominated the end-user segment with revenue share in 2025, supported by the need for multidisciplinary care involving genetic specialists, metabolic disorder physicians, neurologists, and infusion care teams. Increasing establishment of rare disease centers is improving diagnosis, treatment access, and long-term monitoring of Pompe disease patients.

- Hospital Pharmacy remained the leading distribution channel with revenue share in 2025, driven by the specialized nature of Pompe disease therapies, high-cost biologic treatments, and the requirement for hospital-based administration and monitoring of enzyme replacement therapies.

Market Size & Forecast

- Global Market Value (2025): USD 1.70 Billion

- Expected Market Value (2033): USD 2.51 Billion

- Forecast CAGR (2026–2033): 5.00%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Pompe Disease Market Segmentation

|

Attributes |

Pompe Disease Key Market Insights |

|

Segments Covered |

· By Type: Classic Infantile Form, Non-Classic Infantile Form, Late-Onset Form, and Others · By Diagnosis: Blood Test, Genetic Test, Prenatal Test, and Others · By Treatment: Enzyme Replacement Therapy, Supportive Therapies, and Others · By Route of Administration: Oral, Parenteral, and Others · By End Users: Hospitals, Homecare, Specialty Centres, and Others · By Distribution Channel: Hospital Pharmacy, Online Pharmacy, and Retail Pharmacy |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Sanofi Genzyme (France) |

|

Market Opportunities |

· Increasing adoption of advanced enzyme replacement therapies (ERT) and development of next-generation treatments · Expansion of newborn screening programs · Growing investments in rare disease research |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Pompe Disease Market Trends

Trend: Increasing Focus on Early Diagnosis and Advanced Management of Rare Genetic Disorders

The Pompe Disease Market is witnessing a growing shift toward early diagnosis, newborn screening, and long-term disease management due to increasing awareness of rare lysosomal storage disorders. Healthcare systems are increasingly prioritizing genetic testing and biomarker-based diagnosis to identify patients earlier and enable timely treatment initiation. Pompe disease, caused by mutations in the GAA gene leading to acid alpha-glucosidase deficiency, requires early intervention to prevent progressive muscle weakness, respiratory complications, and disease-related mortality. The trend is supported by the expansion of newborn screening programs in several countries, enabling earlier identification of infantile-onset Pompe disease. For instance, the inclusion of Pompe disease in newborn screening panels in regions such as the U.S. has improved early detection and access to enzyme replacement therapy (ERT). According to rare disease organizations, Pompe disease affects approximately 1 in 40,000 people globally, highlighting the importance of improved diagnostic approaches for identifying undiagnosed patients. Increasing adoption of advanced diagnostic methods, including molecular genetic testing, enzyme activity assays, and next-generation sequencing technologies, is further strengthening market growth. Pharmaceutical companies are also focusing on developing next-generation therapies with improved efficacy, longer duration of action, and reduced treatment burden for patients requiring lifelong management.

Pompe Disease Market Dynamics

Key Market Driver: Rising Adoption of Enzyme Replacement Therapy and Growing Investment in Rare Disease Treatments

The increasing availability and adoption of enzyme replacement therapy (ERT) is a major factor driving growth in the Pompe Disease Market. ERT remains the established standard treatment for Pompe disease, helping improve survival rates, motor function, and quality of life, particularly among patients diagnosed at an early stage.

The approval and commercialization of therapies such as Myozyme®/Lumizyme® (alglucosidase alfa) by Sanofi have significantly transformed Pompe disease management by providing a disease-modifying treatment option. In addition, the development of next-generation therapies such as avalglucosidase alfa has expanded treatment options by improving enzyme delivery and clinical outcomes. Growing healthcare investments in rare disease research are also supporting market expansion. Pharmaceutical companies are increasing research activities focused on improved enzyme replacement therapies, gene therapy approaches, and personalized treatment strategies. For instance, advances in gene therapy research are creating potential future alternatives to lifelong intravenous enzyme replacement. North America remains a major market due to strong rare disease infrastructure, early adoption of advanced therapies, and availability of specialized metabolic disorder centers. Meanwhile, Asia-Pacific markets, including China and India, are experiencing increasing demand due to improving genetic testing availability, rising awareness, and expanding access to rare disease treatments.

Key Restraint/Challenge: High Treatment Cost and Limited Access to Rare Disease Care

A major challenge in the Pompe Disease Market is the high cost associated with diagnosis, lifelong treatment, and disease management. Enzyme replacement therapies require regular intravenous infusions, often throughout a patient’s lifetime, resulting in substantial healthcare expenditure for patients, families, and healthcare systems. The requirement for specialized infusion centers, trained healthcare professionals, genetic counseling, and continuous monitoring increases the overall treatment burden. These challenges are particularly significant in low- and middle-income countries where rare disease reimbursement systems and specialized healthcare infrastructure remain limited. For instance, access disparities continue to exist between developed and emerging markets due to differences in healthcare funding, availability of genetic testing facilities, and reimbursement coverage for high-cost orphan drugs. Limited awareness among physicians and delayed diagnosis also remains barriers, as symptoms of Pompe disease can overlap with other neuromuscular disorders, leading to underdiagnosis. Improving affordability, expanding newborn screening programs, and strengthening rare disease healthcare networks remain critical factors for increasing global treatment access.

Key Market Opportunity: Advancements in Gene Therapy, Digital Monitoring, and Personalized Treatment Approaches

The integration of advanced biotechnology, gene therapy, and digital healthcare solutions presents significant growth opportunities for the Pompe Disease market. Researchers are increasingly exploring gene replacement approaches designed to address the underlying genetic cause of Pompe disease rather than only managing symptoms. Gene therapy platforms aim to deliver functional copies of the GAA gene to restore enzyme production, potentially reducing dependence on lifelong enzyme replacement therapy. Clinical research activities in this area are creating new opportunities for long-term disease modification. In addition, digital health technologies and remote monitoring solutions are improving patient management by enabling continuous tracking of muscle function, respiratory health, treatment response, and disease progression. These tools support personalized care strategies and improve coordination between patients and multidisciplinary healthcare teams. The expansion of specialized metabolic disorder centers, increased government support for rare disease programs, and growing investments in emerging healthcare markets are expected to further accelerate Pompe Disease market growth through 2033.

Pompe Disease Market Scope

The Pompe Disease market is segmented on the basis of type, diagnosis, treatment, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the Pompe Disease Market is segmented into classic infantile form, non-classic infantile form, late-onset form, and others. The Late-Onset Form segment dominated the market with a 54.6% share in 2025, owing to the higher diagnosed patient population compared with infantile variants and increasing recognition of adult-onset symptoms such as progressive muscle weakness, respiratory impairment, and mobility challenges. The segment benefits from improved disease awareness among neurologists, genetic specialists, and metabolic disorder physicians, leading to higher diagnosis rates. Increasing availability of enzyme replacement therapies and long-term disease management programs is further supporting treatment adoption among late-onset patients. Growing use of genetic testing and biomarker-based diagnosis is enabling earlier identification of affected individuals. In addition, expanding rare disease registries and patient support programs are improving disease monitoring and management. The increasing focus on improving quality of life and delaying disease progression is further strengthening demand for Pompe disease therapies. Rising healthcare expenditure and improved access to specialty care centers are also contributing to segment dominance globally.

The Classic Infantile Form segment is expected to witness the fastest growth at a CAGR of 7.8% from 2026 to 2033, driven by increasing newborn screening initiatives, rising awareness regarding early diagnosis, and growing availability of advanced treatment options for infants. Early identification of Pompe disease allows timely initiation of enzyme replacement therapy, which can significantly improve survival rates and clinical outcomes. Expansion of neonatal screening programs across developed and emerging markets is expected to increase detection rates. Increasing government initiatives supporting rare disease diagnosis and pediatric genetic testing are further accelerating segment growth. Advancements in molecular diagnostics and improved access to specialized pediatric metabolic centers are enhancing treatment opportunities. Pharmaceutical companies are also investing in innovative therapies targeting early-stage disease progression. The rising focus on reducing infant mortality associated with Pompe disease is expected to create significant growth opportunities during the forecast period.

- By Diagnosis

On the basis of diagnosis, the Pompe Disease Market is segmented into blood test, genetic test, prenatal test, and others. The Blood Test segment dominated the market with a 46.8% share in 2025, due to its widespread application as an initial diagnostic method for suspected Pompe disease cases. Blood-based enzyme activity testing, particularly measurement of acid alpha-glucosidase (GAA) activity, is commonly used because of its accessibility and relatively faster diagnostic process. Increasing awareness among healthcare providers regarding early detection of rare metabolic disorders is supporting segment growth. The availability of diagnostic laboratories and improved healthcare infrastructure is further increasing adoption of blood-based testing. Blood tests are also widely used for patient monitoring during enzyme replacement therapy. Growing screening programs and increasing referrals to metabolic specialists are strengthening demand for diagnostic testing. In addition, the lower cost compared with advanced molecular testing supports wider adoption across healthcare settings.

The Genetic Test segment is projected to register the fastest growth at a CAGR of 8.3% from 2026 to 2033, driven by increasing adoption of precision medicine and improved accuracy in confirming Pompe disease diagnosis. Genetic testing helps identify mutations in the GAA gene and supports differentiation from other neuromuscular disorders with similar symptoms. Rising availability of next-generation sequencing technologies is improving accessibility and reducing testing costs. Increasing demand for family screening and carrier identification is further supporting genetic testing adoption. Healthcare providers are increasingly using genetic information for personalized treatment planning and disease prognosis. Government initiatives supporting rare disease diagnostics are also contributing to market expansion. Growing collaborations between diagnostic companies and research institutions are expected to accelerate innovation in genetic testing solutions.

- By Treatment

On the basis of treatment, the Pompe Disease Market is segmented into enzyme replacement therapy, supportive therapies, and others. The Enzyme Replacement Therapy (ERT) segment dominated the market with a 78.2% share in 2025, owing to its position as the primary approved treatment approach for Pompe disease management. ERT replaces the deficient GAA enzyme responsible for disease progression and helps improve muscle function and reduce complications. The availability of established therapies such as alglucosidase alfa and next-generation enzyme replacement treatments is driving widespread adoption. Increasing diagnosis rates and long-term treatment requirements are supporting consistent demand for ERT solutions. Growing investments by pharmaceutical companies in improving enzyme therapies are further strengthening the segment. Hospitals and specialty centers continue to rely on ERT as the standard treatment option for both infantile and late-onset patients. Expansion of reimbursement programs in several countries is also improving patient access to these therapies.

The Supportive Therapies segment is expected to witness the fastest growth at a CAGR of 8.7% from 2026 to 2033, driven by increasing demand for comprehensive disease management beyond enzyme replacement therapy. Supportive treatments such as respiratory care, physiotherapy, nutritional support, and mobility assistance play an important role in improving patient quality of life. Growing adoption of multidisciplinary care models is encouraging integration of supportive therapies into Pompe disease management programs. Increasing awareness among caregivers and healthcare professionals regarding supportive interventions is further contributing to segment expansion. Rising patient survival rates due to improved treatments are increasing the need for long-term supportive care. Healthcare systems are increasingly focusing on holistic management approaches for rare diseases. Expansion of rehabilitation services and specialized care programs is expected to create additional growth opportunities.

- By Route of Administration

On the basis of route of administration, the Pompe Disease Market is segmented into oral, parenteral, and others. The Parenteral segment dominated the market with a 91.5% share in 2025, due to the extensive use of intravenous enzyme replacement therapies in Pompe disease treatment. Current approved ERT solutions require infusion-based administration to effectively deliver therapeutic enzymes into the body. The established clinical effectiveness of intravenous treatment has resulted in widespread adoption across hospitals and specialty centers. Increasing availability of infusion facilities and trained healthcare professionals is supporting segment dominance. The requirement for regular administration and disease monitoring further strengthens demand for parenteral therapies. Growing diagnosis rates and increasing patient enrollment in treatment programs are contributing to sustained market growth. Pharmaceutical companies continue to focus on improving infusion efficiency and treatment outcomes.

The Oral segment is expected to witness the fastest growth at a CAGR of 9.2% from 2026 to 2033, driven by increasing research into patient-friendly and non-invasive treatment approaches. Oral therapies have the potential to reduce the treatment burden associated with frequent intravenous infusions. Rising investments in innovative drug delivery technologies are supporting development of alternative administration methods. Increasing patient preference for convenient treatment options is encouraging research into oral formulations. Advancements in molecular therapies and targeted treatment approaches are expected to create future opportunities. Pharmaceutical companies are exploring improved delivery mechanisms to enhance patient compliance. The shift toward personalized and less invasive therapies is expected to support long-term segment growth.

- By End Users

On the basis of end users, the Pompe Disease Market is segmented into hospitals, homecare, specialty centres, and others. The Hospitals segment dominated the market with a 45.7% share in 2025, due to the availability of advanced diagnostic facilities, specialist physicians, and infusion services required for Pompe disease treatment. Hospitals remain the primary location for diagnosis, treatment initiation, and management of disease complications. Increasing investments in healthcare infrastructure and expansion of rare disease programs are supporting hospital adoption. The availability of multidisciplinary teams including neurologists, genetic specialists, and rehabilitation experts strengthens hospital-based care. Growing patient preference for specialized treatment environments is further supporting segment growth. Hospitals also play a key role in administering enzyme replacement therapies and monitoring patient responses. Expansion of tertiary healthcare facilities is expected to maintain segment dominance.

The Specialty Centres segment is expected to witness the fastest growth at a CAGR of 8.9% from 2026 to 2033, driven by increasing demand for specialized rare disease management facilities. Specialty centres provide advanced diagnostic services, genetic counseling, and personalized treatment strategies. Growing establishment of metabolic disorder centers is improving access to expert care. Increasing collaborations between pharmaceutical companies and specialized healthcare providers are supporting segment development. Rising complexity of Pompe disease management is increasing the need for dedicated treatment centers. Growing awareness among patients regarding specialized care options is further accelerating adoption. Expansion of rare disease networks globally is expected to create additional opportunities.

- By Distribution Channel

On the basis of distribution channel, the Pompe Disease Market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The Hospital Pharmacy segment dominated the market with a 69.4% share in 2025, owing to the specialized handling, storage, and administration requirements of Pompe disease therapies. Hospital pharmacies play a critical role in managing enzyme replacement therapies and ensuring proper treatment delivery. The requirement for controlled storage conditions and professional supervision supports hospital pharmacy dominance. Increasing availability of rare disease treatments through hospital networks is strengthening this segment. Hospitals also provide integrated patient support services, improving treatment adherence. Growing adoption of specialty care models further supports the importance of hospital pharmacies. Strong relationships between healthcare providers and pharmaceutical suppliers are reinforcing segment growth.

The Online Pharmacy segment is expected to witness the fastest growth at a CAGR of 10.1% from 2026 to 2033, driven by increasing digital healthcare adoption and growing demand for convenient medication access. Online pharmacy platforms are expanding availability of supportive medicines and healthcare products for rare disease patients. Rising internet penetration and improvements in healthcare logistics are supporting online distribution growth. Increasing acceptance of digital healthcare services is encouraging patients and caregivers to use online platforms. Growth of e-commerce healthcare ecosystems is improving accessibility, especially in emerging markets. Online channels provide convenience for long-term disease management needs. The increasing integration of digital health solutions is expected to further accelerate segment expansion.

Pompe Disease Market Regional Analysis

North America dominated the Pompe Disease Market with the largest revenue share of approximately 41.3% in 2025, supported by advanced healthcare infrastructure, early adoption of innovative rare disease therapies, strong diagnostic capabilities, and the presence of leading pharmaceutical companies developing enzyme replacement therapies. The region benefits from well-established newborn screening programs, improved access to genetic testing, specialized metabolic disorder centers, and favorable reimbursement frameworks that support long-term Pompe disease management. The strong presence of rare disease research organizations, advanced clinical trial infrastructure, and increasing availability of enzyme replacement therapies are further strengthening market growth. Healthcare providers across the region are increasingly focusing on early diagnosis and multidisciplinary management approaches to improve patient outcomes. In addition, rising investments in rare disease research and development are supporting advancements in next-generation treatments, including improved enzyme replacement therapies and emerging gene therapy approaches

U.S. Pompe Disease Market Insight

The U.S. Pompe Disease market is witnessing strong growth due to increasing diagnosis rates, expanding newborn screening initiatives, and high adoption of advanced rare disease treatments. The country’s well-developed healthcare ecosystem, availability of specialized metabolic centers, and strong reimbursement support are enabling broader access to enzyme replacement therapy and genetic testing. The U.S. remains a major hub for Pompe disease research and innovation, supported by the presence of leading biotechnology and pharmaceutical companies focused on rare disease therapies. Increasing awareness among healthcare professionals regarding early identification of Pompe disease, along with advancements in molecular diagnostics, is improving patient detection and treatment initiation. Furthermore, growing clinical research activities focused on gene therapy and next-generation enzyme replacement solutions are expected to create additional market opportunities.

Europe Pompe Disease Market Insight

The Europe Pompe Disease market represents a significant share of the global market, driven by strong healthcare systems, increasing rare disease awareness, and expanding access to advanced treatment options. European countries have established rare disease networks, genetic testing capabilities, and specialized treatment centers that support diagnosis and long-term patient management. The region’s focus on improving rare disease care pathways, increasing adoption of enzyme replacement therapies, and strengthening newborn screening programs is supporting market expansion. Government initiatives aimed at improving access to orphan drugs and personalized medicine approaches are further contributing to market growth. In addition, increasing collaborations between research institutions, healthcare providers, and pharmaceutical companies are accelerating innovation in Pompe disease treatment.

U.K. Pompe Disease Market Insight

The U.K. Pompe Disease market is experiencing steady growth due to increasing awareness of rare genetic disorders, improved diagnostic capabilities, and expanding access to specialized healthcare services. The country’s focus on rare disease management programs and genetic medicine initiatives is supporting earlier diagnosis and improved treatment outcomes. The availability of specialized metabolic disorder centers and growing adoption of advanced diagnostic technologies are contributing to market development. In addition, increasing healthcare investments in genomic medicine and personalized treatment approaches are strengthening the country’s position in rare disease care. The U.K.’s growing focus on improving patient access to orphan therapies is expected to further support Pompe disease market growth.

Germany Pompe Disease Market Insight

The Germany Pompe Disease market is expanding steadily due to its advanced healthcare infrastructure, strong biotechnology sector, and well-established rare disease management ecosystem. Germany has a strong network of specialized hospitals and metabolic disorder centers capable of providing diagnosis, enzyme replacement therapy, and long-term monitoring for Pompe disease patients. The country’s emphasis on precision medicine, genetic diagnostics, and innovative therapies is supporting market growth. Increasing investments in clinical research, biotechnology development, and rare disease treatment programs are further enhancing access to advanced Pompe disease management solutions. Germany’s strong pharmaceutical and research capabilities continue to make it a key contributor to the European Pompe Disease market.

Asia-Pacific Pompe Disease Market Insight

The Asia-Pacific Pompe Disease market is expected to witness the fastest growth globally, registering a CAGR of approximately 8.7% from 2026 to 2033, driven by improving rare disease awareness, expanding healthcare infrastructure, increasing availability of genetic diagnostics, and rising investments in specialized treatment centers across countries such as China, India, and Japan. The region is experiencing increasing demand for advanced Pompe disease management solutions due to rising healthcare expenditure, improving access to molecular testing, and growing recognition of rare genetic disorders. Government initiatives supporting rare disease diagnosis and treatment, along with increasing adoption of enzyme replacement therapies, are accelerating market expansion. The growth of specialty hospitals, metabolic disorder clinics, and rare disease programs is further improving patient access to advanced therapies.

Japan Pompe Disease Market Insight

The Japan Pompe Disease market is witnessing consistent growth due to the country’s advanced healthcare system, aging population, strong focus on genetic medicine, and increasing awareness of rare metabolic disorders. Japan has established specialized medical facilities and diagnostic capabilities that support early identification and management of Pompe disease. The increasing adoption of genetic testing, newborn screening programs, and enzyme replacement therapies is contributing to market growth. In addition, Japan’s strong research ecosystem and focus on innovative healthcare technologies are supporting advancements in rare disease treatment approaches. Growing investments in personalized medicine and improved patient support programs are expected to further strengthen the Pompe Disease market.

China Pompe Disease Market Insight

The China Pompe Disease market is growing rapidly, supported by improving rare disease awareness, expanding healthcare infrastructure, increasing availability of genetic testing, and rising government focus on rare disease management. The country’s large population base and increasing healthcare investments are creating significant opportunities for Pompe disease diagnosis and treatment adoption. Growing establishment of specialized treatment centers, improved access to advanced diagnostics, and increasing availability of enzyme replacement therapies are supporting market growth. Government initiatives aimed at strengthening rare disease care and improving access to orphan drugs are further accelerating adoption. In addition, increasing collaboration between international pharmaceutical companies and Chinese healthcare institutions is enhancing treatment availability and positioning China as one of the fastest-growing markets for Pompe Disease globally.

Pompe Disease Market Share

The Pompe Disease industry is primarily led by well-established companies, including:

• Sanofi Genzyme (France)

• Amicus Therapeutics, Inc. (U.S.)

• BioMarin Pharmaceutical Inc. (U.S.)

• Takeda Pharmaceutical Company Limited (Japan)

• Chiesi Farmaceutici S.p.A. (Italy)

• Genzyme Corporation (U.S.)

• Spark Therapeutics, Inc. (U.S.)

• Rocket Pharmaceuticals, Inc. (U.S.)

• Sarepta Therapeutics, Inc. (U.S.)

• Ultragenyx Pharmaceutical Inc. (U.S.)

• Audentes Therapeutics, Inc. (U.S.)

• Asklepion Pharmaceuticals LLC (U.S.)

• Moderna, Inc. (U.S.)

• Pfizer Inc. (U.S.)

• Novartis AG (Switzerland)

• F. Hoffmann-La Roche Ltd. (Switzerland)

• Johnson & Johnson Innovative Medicine (U.S.)

• Bayer AG (Germany)

• Merck KGaA (Germany)

• Thermo Fisher Scientific Inc. (U.S.)

• Illumina, Inc. (U.S.)

• Qiagen N.V. (Netherlands)

• PerkinElmer Inc. (U.S.)

• Revvity, Inc. (U.S.)

• Quest Diagnostics Incorporated (U.S.)

• Laboratory Corporation of America Holdings (Labcorp) (U.S.)

• Eurofins Scientific SE (Luxembourg)

• Bio-Techne Corporation (U.S.)

• Charles River Laboratories International, Inc. (U.S.)

• Catalent, Inc. (U.S.)

• Lonza Group AG (Switzerland)

• GenScript Biotech Corporation (China)

• WuXi AppTec Co., Ltd. (China)

• Sarepta Therapeutics Gene Therapy Division (U.S.)

• Orphan Biovitrum AB (Sweden)

Latest Developments in Pompe Disease Market

- In December 2021, clinical trial results for next-generation enzyme replacement therapies in Pompe disease were published, highlighting advancements in treatment effectiveness and disease management. Studies evaluating avalglucosidase alfa and cipaglucosidase alfa-based therapies demonstrated improved or maintained respiratory function and mobility outcomes among patients with late-onset Pompe disease. These developments supported continued innovation in enzyme replacement approaches and increased focus on improving therapeutic benefits beyond existing treatment options

- In June 2022, the European Commission approved Nexviadyme® (avalglucosidase alfa) developed by Sanofi for the treatment of both late-onset and infantile-onset Pompe disease. The approval expanded access to a new enzyme replacement therapy option for European patients and represented the first newly approved Pompe disease treatment in Europe in more than 15 years. The authorization strengthened the adoption of advanced ERT solutions and supported broader global availability of next-generation Pompe disease therapies

- In March 2023, Amicus Therapeutics received European approval for Pombiliti (cipaglucosidase alfa) in combination with miglustat for adults with late-onset Pompe disease. The therapy introduced a new enzyme replacement treatment approach designed to provide an alternative option for adult patients previously managed with existing ERTs. This development expanded the competitive landscape of Pompe disease treatments and highlighted increasing pharmaceutical investment in rare metabolic disorders.

- In April 2023, Amicus Therapeutics continued global commercialization efforts for Pombiliti™ and Opfolda combination therapy following regulatory progress in Pompe disease treatment. The therapy combination was developed to improve enzyme stability and enhance treatment outcomes for adults living with late-onset Pompe disease. The advancement reflected growing industry focus on developing differentiated therapies that address limitations associated with traditional enzyme replacement approaches.

- In September 2023, pharmaceutical and biotechnology companies continued expanding research programs focused on gene therapy approaches for Pompe disease. Emerging gene therapy platforms aimed to provide long-term correction of GAA enzyme deficiency by introducing functional genetic material into patient cells. These developments highlighted the shift toward potentially disease-modifying treatments beyond lifelong enzyme replacement therapy and created future growth opportunities in the rare disease market

- In February 2024, Sanofi continued expanding global access and commercialization of Nexviazyme (avalglucosidase alfa) as adoption increased across additional healthcare markets. The therapy gained attention as an advanced treatment option for Pompe disease due to its targeted enzyme delivery mechanism and potential benefits in muscle and respiratory function management. Increasing physician awareness and improvements in rare disease diagnosis supported broader treatment adoption

- In May 2024, biotechnology companies increased investment in next-generation Pompe disease therapies, including improved enzyme replacement technologies and gene therapy candidates. Research activities focused on enhancing treatment durability, reducing infusion burden, and improving outcomes for patients with both infantile-onset and late-onset Pompe disease. These innovations supported market expansion by addressing unmet clinical needs among Pompe disease patients

- In January 2025, healthcare organizations and rare disease networks continued strengthening newborn screening and early diagnosis initiatives for Pompe disease. Increased implementation of genetic testing and enzyme activity screening programs supported earlier identification of affected infants, enabling faster initiation of treatment. These efforts contributed to rising demand for specialized therapies and diagnostic solutions in the Pompe Disease Market

- In June 2025, the global Pompe disease treatment landscape continued moving toward personalized and advanced therapeutic approaches, with companies focusing on improved enzyme therapies, genetic technologies, and supportive care solutions. Increasing investments in rare disease research, expansion of specialty treatment centers, and improved access to innovative therapies supported long-term market growth. The growing emphasis on early diagnosis and comprehensive disease management further accelerated development opportunities across the Pompe disease ecosystem

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.