Global Portable Ultrasound Market

Market Size in USD Billion

USD

5.05 Billion

USD

8.76 Billion

2024

2032

USD

5.05 Billion

USD

8.76 Billion

2024

2032

| 2025 - 2032 | |

| USD 5.05 Billion | |

| USD 8.76 Billion | |

| % | |

|

Portable Ultrasound Market Size

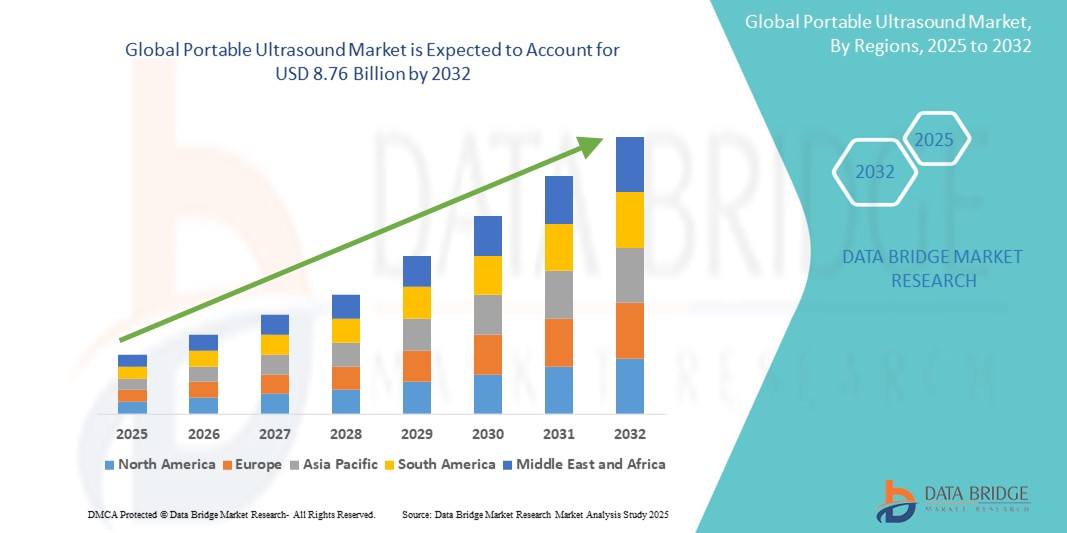

- The global portable ultrasound market size was valued at USD 5.05 billion in 2024 and is expected to reach USD 8.76 billion by 2032, at a CAGR of 7.12% during the forecast period

- The market growth is largely fueled by the growing adoption and technological progress within point-of-care diagnostics and portable medical imaging, leading to increased digitalization and miniaturization of ultrasound devices in both hospital and non-hospital settings

- Furthermore, rising healthcare demand for compact, user-friendly, and versatile diagnostic solutions is establishing portable ultrasound systems as the preferred imaging modality for emergency care, remote clinics, and home healthcare services. These converging factors are accelerating the uptake of portable ultrasound solutions, thereby significantly boosting the industry's growth

Portable Ultrasound Market Analysis

- Portable ultrasound devices, offering compact and real-time diagnostic imaging solutions, are increasingly vital components of modern healthcare and diagnostic systems in both hospital and non-hospital settings due to their enhanced mobility, rapid imaging capabilities, and integration with telemedicine platforms

- The escalating demand for portable ultrasound systems is primarily fueled by the rising prevalence of chronic diseases, increased focus on point-of-care diagnostics, and a growing preference for non-invasive, bedside imaging tools, especially in emergency care, rural healthcare, and home care settings

- North America dominated the portable ultrasound market with the largest revenue share of 39.7% in 2024, characterized by a strong healthcare infrastructure, rapid adoption of advanced imaging technologies, and the presence of key industry players. The U.S., in particular, saw substantial growth in portable ultrasound deployment across ambulatory surgical centers, rural health outreach programs, and mobile diagnostic clinics, driven by innovations in AI-enhanced imaging and wireless probe technologies

- Asia-Pacific is expected to be the fastest-growing region in the portable ultrasound market during the forecast period (2025–2032), with a projected CAGR of 8.9%, due to increasing investments in healthcare infrastructure, rising healthcare awareness, growing geriatric population, and expanding access to diagnostic services in underserved areas

- The handheld ultrasound device segment dominated the largest market revenue share of 58.4% in 2024, driven by its lightweight design, wireless functionality, and increasing adoption across point-of-care settings, especially in emergency care and remote healthcare environments. The convenience of connecting with smartphones and tablets further accelerates usage among frontline health workers

Report Scope and Portable Ultrasound Market Segmentation

|

Attributes |

Portable Ultrasound Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Portable Ultrasound Market Trends

“Improved Diagnostic Accessibility and Workflow Efficiency”

- A significant and accelerating trend in the global portable ultrasound market is the integration of advanced software, wireless connectivity, and compatibility with digital platforms. This evolution is significantly improving diagnostic convenience, enabling healthcare providers to capture, share, and interpret ultrasound images more efficiently than ever before

- For instance, GE Healthcare’s Vscan Air provides handheld wireless ultrasound capabilities and connects to mobile devices, allowing clinicians to perform real-time scanning and share images directly through secure digital platforms. Similarly, Philips Lumify offers smartphone and tablet compatibility, delivering hospital-grade imaging in a pocket-sized format that improves point-of-care diagnosis

- Software enhancements in portable ultrasound systems now include automated image interpretation, real-time cloud syncing, and workflow optimization tools, enabling faster clinical decisions and reducing patient wait times. Some models can analyze image quality and suggest scan corrections, helping non-specialists capture more accurate diagnostic data

- Furthermore, wireless portability offers the flexibility to perform ultrasound imaging in diverse clinical settings—from emergency rooms and ICUs to rural clinics and home visits. Healthcare professionals can initiate scans, transmit results, and consult specialists remotely, improving access to quality care

- The seamless integration of portable ultrasound devices with electronic health record (EHR) systems also streamlines documentation and enhances data accuracy, supporting clinical audits and reimbursement processes. This convergence of mobility, smart software, and interoperability is shaping the future of diagnostic imaging

- The demand for portable ultrasound systems that support real-time diagnostics, remote usage, and cross-platform integration is growing rapidly across primary care, critical care, and remote healthcare settings. Manufacturers such as Butterfly Network, Clarius Mobile Health, and Mindray are leading innovations that align with evolving clinical needs and digital health trends

Portable Ultrasound Market Dynamics

Driver

“Growing Need Due to Rising Chronic Diseases and Point-of-Care Diagnostics”

- The increasing global burden of chronic diseases, such as cardiovascular conditions, kidney disorders, and pregnancy-related complications, coupled with the growing demand for decentralized and rapid diagnostic imaging, is a significant driver for the heightened demand for portable ultrasound systems

- For instance, in April 2024, Philips Healthcare announced enhancements to its Lumify handheld ultrasound system, incorporating improved transducer technology and advanced image processing software. Such innovations by key companies are expected to drive the Portable Ultrasound industry growth in the forecast period

- As healthcare systems shift toward point-of-care diagnostics and mobile imaging solutions, portable ultrasound devices offer advanced features such as bedside imaging, real-time results, wireless data transmission, and compatibility with mobile platforms, providing a compelling alternative to traditional, bulky ultrasound systems

- Furthermore, the rising popularity of telemedicine and the need for scalable diagnostic tools in underserved or remote areas are making portable ultrasound devices an essential component of modern healthcare delivery. These systems offer seamless integration with cloud-based health platforms, enabling remote consultation and follow-up

- The convenience of lightweight design, battery-powered operation, and smartphone/tablet compatibility is propelling the adoption of portable ultrasound in emergency medicine, home care, military settings, and rural clinics. The trend towards affordable, user-friendly, and AI-assisted ultrasound tools further contributes to market expansion across both developed and emerging regions

Restraint/Challenge

“Concerns Regarding Diagnostic Accuracy and High Initial Costs”

- Concerns surrounding the diagnostic limitations of portable ultrasound devices compared to high-end stationary machines pose a challenge to broader adoption. Issues such as limited imaging depth, lower resolution for complex scans, and operator dependency raise hesitations among some healthcare providers, particularly for advanced diagnostic applications

- For instance, several comparative studies have highlighted the need for specialized training and experience to ensure accurate results using portable systems, especially in cardiology or abdominal imaging

- Addressing these concerns through ongoing operator training, certification programs, and technological enhancements in image quality is essential to build clinician trust. Companies such as Butterfly Network and Clarius are emphasizing AI-driven support tools and educational partnerships to overcome this challenge

- In addition, the relatively high initial cost of some advanced portable ultrasound devices—especially those integrated with wireless probes, AI analysis, or specialty applications—can be a barrier to adoption for price-sensitive settings such as small clinics or community health centers

- While entry-level models have become more accessible, the perceived investment required for high-performance devices can limit penetration in developing markets or lower-tier hospitals

- Overcoming these challenges through affordable pricing strategies, government subsidies, and expanded reimbursement policies, along with showcasing the long-term cost-effectiveness of portable imaging, will be vital for sustained growth of the Portable Ultrasound Market

Portable Ultrasound Market Scope

The market is segmented on the basis of device type, application, and end users.

• By Device Type

On the basis of device type, the portable ultrasound market is segmented into handheld ultrasound devices and mobile ultrasound devices. The handheld ultrasound device segment dominated the largest market revenue share of 58.4% in 2024, driven by its lightweight design, wireless functionality, and increasing adoption across point-of-care settings, especially in emergency care and remote healthcare environments. The convenience of connecting with smartphones and tablets further accelerates usage among frontline health workers.

The mobile ultrasound device segment is projected to witness the fastest CAGR of 9.8% from 2025 to 2032, owing to its higher imaging capability, better screen resolution, and growing demand from hospitals and specialty clinics for mobile diagnostic imaging solutions.

• By Application

On the basis of application, the market is segmented into cardiovascular, obstetrics and gynecology, gastric, musculoskeletal, and others. The cardiovascular segment accounted for the largest market revenue share of 28.7% in 2024, due to the rising global burden of cardiac disorders and the frequent need for non-invasive cardiac evaluations in acute care settings.

The musculoskeletal segment is expected to witness the fastest CAGR of 10.5% from 2025 to 2032, driven by the increasing use of portable ultrasound for joint assessments, sports injuries, and rehabilitation monitoring in outpatient and homecare settings.

• By End Users

On the basis of end users, the market is segmented into hospitals, diagnostic centers, ambulatory care centers, and others. The hospitals segment dominated the market with a revenue share of 41.2% in 2024, owing to high patient footfall, availability of trained personnel, and integration of portable ultrasound systems in intensive care units (ICUs), operating rooms (ORs), and emergency departments.

The ambulatory care centers segment is projected to grow at the fastest CAGR of 11.3% during the forecast period, fueled by the rise in minimally invasive procedures and the demand for quick, onsite diagnostic services in outpatient facilities.

Portable Ultrasound Market Regional Analysis

- North America dominated the portable ultrasound market with the largest revenue share of 39.7% in 2024, driven by the rising prevalence of chronic diseases, increasing demand for point-of-care diagnostics, and the strong adoption of advanced imaging technologies in both hospital and outpatient settings

- The region benefits from high healthcare expenditure, well-established infrastructure, and supportive reimbursement policies that encourage the use of portable diagnostic devices

- The growing focus on decentralized care and home-based monitoring is also driving the adoption of portable ultrasound devices across primary care and emergency services

U.S. Portable Ultrasound Market Insight

The U.S. portable ultrasound market captured the largest revenue share of 81% in 2024 within North America, fueled by the strong presence of key players, early adoption of innovative diagnostic tools, and widespread use in cardiology, OB/GYN, and emergency care. The market is further driven by the growing prevalence of cardiovascular disorders and a shift toward value-based care. Rising demand for handheld ultrasound devices among physicians for bedside and remote diagnostics is also accelerating market growth. The U.S. market is expected to expand at a CAGR of 7.2% from 2025 to 2032.

Europe Portable Ultrasound Market Insight

The Europe portable ultrasound market is projected to grow at a CAGR of 6.4% during the forecast period, driven by increasing use of non-invasive diagnostic imaging in outpatient settings, aging populations, and supportive healthcare regulations. The demand for compact and mobile medical imaging solutions is rising in both public and private healthcare facilities. The market also benefits from national screening programs and technological advancements in imaging resolution and battery-operated systems.

U.K. Portable Ultrasound Market Insight

The U.K. portable ultrasound market is anticipated to grow at a CAGR of 6.9% during the forecast period. This growth is attributed to increasing focus on women’s health, early prenatal screening, and growing investments in telehealth infrastructure. Portable ultrasound devices are being increasingly used in rural and home healthcare settings, as the NHS promotes decentralized diagnostic care.

Germany Portable Ultrasound Market Insight

The Germany portable ultrasound market is expected to grow at a CAGR of 6.2% during the forecast period. Germany’s emphasis on healthcare innovation, digitization, and point-of-care services drives demand for portable imaging tools in outpatient clinics and ambulatory surgery centers. The nation’s large base of geriatric patients also contributes to sustained usage across cardiology and internal medicine.

Asia-Pacific Portable Ultrasound Market Insight

The Asia-Pacific portable ultrasound market is poised to grow at the fastest CAGR of 8.9% from 2025 to 2032. This growth is fueled by increasing healthcare access, rising awareness of early diagnosis, and strong government initiatives supporting the use of portable diagnostic tools in primary and secondary care. Countries such as China, India, and Japan are witnessing rapid deployment of portable ultrasound devices in maternal health, cardiac screening, and rural health centers.

Japan Portable Ultrasound Market Insight

The Japan portable ultrasound market contributed 18.9% to the Asia-Pacific market in 2024 and is growing steadily due to strong demand for advanced, compact diagnostic tools. Japan’s aging population and widespread integration of AI in imaging diagnostics are key factors boosting the market. Portable ultrasound is widely used in home visits, emergency medical services, and telehealth applications. The market is expected to expand at a CAGR of 7.5% over the forecast period.

China Portable Ultrasound Market Insight

The China portable ultrasound market accounted for the largest revenue share of 35.2% in Asia Pacific in 2024, driven by expanding healthcare infrastructure, growing middle-class awareness, and a booming domestic manufacturing base. China is witnessing increased adoption of affordable handheld and mobile ultrasound devices in public hospitals, private clinics, and rural healthcare programs. Government investment in maternal and rural care continues to be a significant driver. The market is projected to grow at a CAGR of 9.1% from 2025 to 2032.

Portable Ultrasound Market Share

The portable ultrasound industry is primarily led by well-established companies, including:

- FUJIFILM SonoSite, Inc. (U.S.)

- General Electric Company (U.S.)

- Hitachi Ltd. (Japan)

- FUKUDA DENSHI (Japan)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Koninklijke Philips N.V. (Netherlands)

- SAMSUNG (South Korea)

- Clarius (Canada)

- Analogic Corporation (U.S.)

- Esaote SPA (Italy)

- EDAN Instruments, Inc. (China)

- Shimadzu Corporation (Japan)

- Trivitron Healthcare (India)

- Hologic Inc. (U.S.)

- ALPINION MEDICAL SYSTEMS Co., Ltd. (South Korea)

- Carestream Health (U.S.)

- Daxsonics Ultrasound Inc. (U.S.)

Latest Developments in Global Portable Ultrasound Market

- In September 2024, GE HealthCare unveiled the upgraded Venue ultrasound systems, introducing the Venue Sprint, a groundbreaking solution in point-of-care ultrasound (POCUS). This device emphasizes portability while incorporating the user-friendly Venue software alongside AI-driven features for superior imaging quality. In addition, it boasts wireless probe capabilities that work seamlessly with Vscan Air handheld ultrasound systems

- In August 2022, Echonous formed a partnership with Samsung to advance ultrasound imaging by leveraging AI-guided technology. This collaboration focuses on improving both the usability and accuracy of ultrasound procedures, thereby making them more accessible to healthcare providers. By incorporating artificial intelligence into their systems, the partnership aims to empower clinicians to deliver more accurate diagnostics and enhance overall patient care, aligning with the growing trend of integrating AI in medical imaging

- In April 2022, GE HealthCare and Elekta entered into a global commercial collaboration agreement focused on radiation oncology. This partnership aims to provide hospitals with a comprehensive solution that integrates imaging and treatment for cancer patients in need of radiation therapy. By combining their expertise, the two companies seek to enhance the quality of care and streamline processes for oncology services

- In March 2021, GE Healthcare, a leader in medical technology and digital solutions, introduced the Vscan Air, a wireless compact ultrasound device. This innovative tool offers exceptional image quality along with the ability to perform whole-body scans. The Vscan Air aims to enhance diagnostic capabilities and improve patient care through its portability and advanced imaging technology

- In October 2020, Clarius Mobile Health reported a growing acceptance of its Clarius L7 H.D. handheld ultrasound scanner among pain management specialists globally. This device provides high-quality ultrasound imaging of subcutaneous anatomy, facilitating more accurate and reliable placement of pain medication. The increasing adoption highlights the scanner's effectiveness in enhancing procedural precision and patient outcomes

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.