Global Postmenopausal Osteoporosis Market

Market Size in USD Billion

USD

12.24 Billion

USD

16.75 Billion

2025

2033

USD

12.24 Billion

USD

16.75 Billion

2025

2033

| 2026 - 2033 | |

| USD 12.24 Billion | |

| USD 16.75 Billion | |

| % | |

|

Postmenopausal Osteoporosis Market Overview

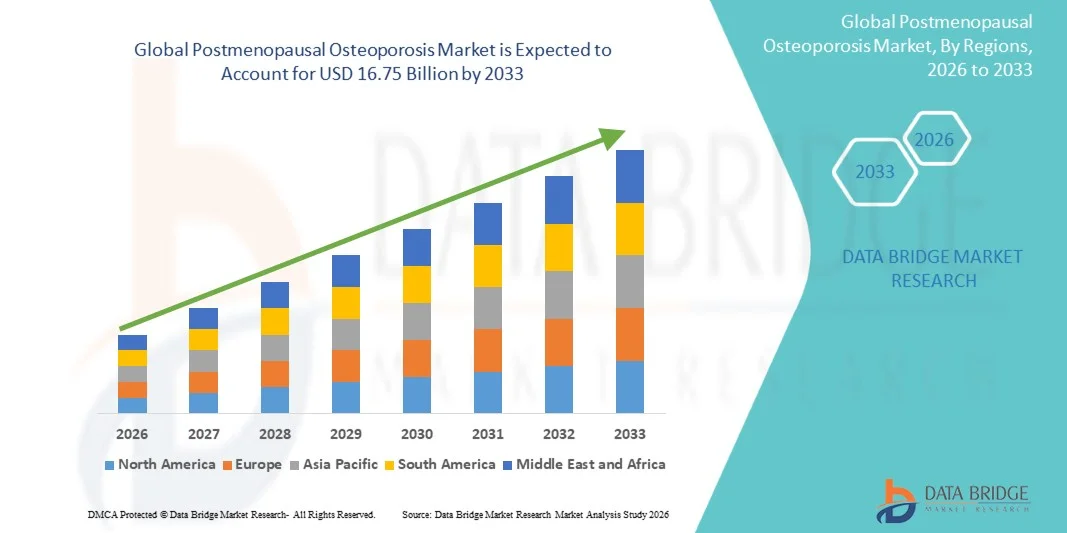

The Postmenopausal Osteoporosis Market was valued at USD 12.24 billion in 2025 and is projected to reach USD 16.75 billion by 2033, growing at a CAGR of 4.00% from 2026 to 2033. The market is experiencing steady growth driven by the increasing prevalence of osteoporosis among aging women, rising awareness regarding bone health, and continuous advancements in therapeutic options aimed at fracture prevention and long-term disease management.

The growing global geriatric female population, coupled with hormonal changes associated with menopause that accelerate bone density loss, is significantly increasing the demand for effective osteoporosis treatments. In addition, government-led screening initiatives, improved diagnostic technologies, and greater access to anti-resorptive and anabolic therapies are encouraging early diagnosis and intervention. Biologic drugs, targeted therapies, and patient-friendly treatment regimens are increasingly being adopted across healthcare systems, supporting better treatment adherence and improved clinical outcomes while reducing the burden of osteoporosis-related fractures.

Key Market Trends & Insights

- North America dominated the Postmenopausal Osteoporosis Market with the largest revenue share of 39.12% in 2025, supported by a high prevalence of osteoporosis, strong healthcare expenditure, widespread screening programs, and favorable reimbursement policies.

- The Bisphosphonates segment led the market with a 38.64% share in 2025, driven by its long-established role as the first-line treatment for postmenopausal osteoporosis and proven effectiveness in reducing fracture risk.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 5.3% from 2026 to 2033, fueled by a rapidly aging female population, improving healthcare access, increasing awareness of bone health, and expanding osteoporosis diagnosis rates across China, India, and Japan.

- Parathyroid Hormone are the fastest-growing treatment type, projected to register a CAGR of 5.9%, reflecting the surge in demand for anabolic therapies that actively stimulate new bone formation rather than merely slowing bone loss

- The Oral segment dominated the route of administration category with a 57.46% revenue share in 2025, led by widespread use of oral bisphosphonates and other osteoporosis medications as primary treatment options.

- Hospitals accounted for 46.82% of the market, preferred by high volume of osteoporosis diagnosis, treatment initiation, and fracture management procedures performed within hospital settings.

- The Parenteral segment is the fastest-growing software category, with a CAGR of 5.4%, driven by increasing adoption of biologics, monoclonal antibodies, and anabolic osteoporosis therapies administered through injections.

Market Size & Forecast

- Global Market Value (2025): USD 12.24 Billion

- Expected Market Value (2033): USD 16.75 Billion

- Forecast CAGR (2026–2033): 4.00%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Postmenopausal Osteoporosis Market Segmentation

|

Attributes |

Postmenopausal Osteoporosis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Amgen Inc. (U.S.) · Eli Lilly and Company (U.S.) · Merck & Co., Inc. (U.S.) · Pfizer Inc. (U.S.) · AbbVie Inc. (U.S.) · Radius Health, Inc. (U.S.) · Viatris Inc. (U.S.) · Organon & Co. (U.S.) · Theramex (U.K.) · UCB (Belgium) · Novartis AG (Switzerland) · F. Hoffmann-La Roche Ltd (Switzerland) · Sandoz AG (Switzerland) · Bayer AG (Germany) · STADA Arzneimittel AG (Germany) · Daiichi Sankyo Company, Limited (Japan) · Takeda Pharmaceutical Company Limited (Japan) · Teva Pharmaceutical Industries Ltd. (Israel) · Zydus Lifesciences Limited (India) · Dr. Reddy’s Laboratories Ltd. (India) |

|

Market Opportunities |

· Expansion of anabolic and bone-building therapies · Growing adoption of AI-assisted fracture risk assessment and osteoporosis screening programs · Rising osteoporosis awareness and healthcare infrastructure development in emerging economies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Postmenopausal Osteoporosis Market Trends

Trend: Rising Adoption of Biologic and Bone-Building Therapies

Healthcare providers are increasingly adopting biologic and anabolic osteoporosis therapies to improve bone density, reduce fracture risk, and address unmet treatment needs among high-risk postmenopausal women. The integration of personalized treatment strategies enables more effective disease management and supports long-term patient outcomes. Hospitals and specialty clinics are similarly utilizing advanced therapeutic options to manage severe osteoporosis cases through evidence-based protocols, while innovations in targeted therapies create treatment approaches that closely align with individual patient risk profiles.

For instance, in May 2024, Amgen highlighted continued adoption of Prolia (denosumab) and Evenity (romosozumab) across global markets, supporting fracture prevention and bone health management in postmenopausal osteoporosis patients.

Postmenopausal Osteoporosis Market Dynamics

Key Market Driver: Growing Prevalence of Osteoporosis Among Aging Female Populations

The rapid growth of the aging female population and increasing life expectancy have created substantial demand for effective osteoporosis therapies that can reduce fracture risk, preserve mobility, and improve quality of life. Pharmaceutical manufacturers, healthcare providers, and public health organizations are expanding osteoporosis management programs as a core component of preventive healthcare strategies, supporting early intervention, improving treatment adherence, and reducing the long-term burden of osteoporotic fractures.

For instance, in October 2023, the International Osteoporosis Foundation reported that osteoporosis and fragility fractures continue to rise globally due to population aging, reinforcing demand for long-term osteoporosis treatment solutions.

Key Restraint/Challenge: Long-Term Treatment Adherence and Medication Persistence Issues

A significant restraint in the Postmenopausal Osteoporosis Market is the challenge of maintaining long-term patient adherence to prescribed therapies. Many treatment regimens require extended administration periods, regular monitoring, and ongoing lifestyle modifications, creating barriers to sustained compliance. The burden of treatment extends to concerns regarding side effects, dosing schedules, and discontinuation rates, making disease management difficult for healthcare providers and patients seeking consistent therapeutic outcomes across diverse care settings. For instance, in January 2024, findings published by the National Osteoporosis Foundation highlighted persistent medication discontinuation trends among osteoporosis patients, reflecting broader adherence challenges affecting long-term treatment effectiveness.

Key Market Opportunity: Expansion of Early Screening and Fracture Risk Assessment Programs

The expansion of osteoporosis screening initiatives presents a significant market opportunity. Advanced diagnostic technologies can support earlier disease detection, improve fracture risk stratification, and enable timely therapeutic intervention across broader patient populations. The development of digital health platforms and integrated care pathways is further improving access to osteoporosis management services, opening growth opportunities across underserved markets in Asia-Pacific, Latin America, and the Middle East. For instance, in April 2024, Hologic continued expanding access to bone densitometry and osteoporosis assessment technologies, supporting earlier diagnosis and preventive treatment strategies for postmenopausal women worldwide.

Postmenopausal Osteoporosis Market Scope

The postmenopausal osteoporosis market is segmented on the basis of treatment type, route of administration, end-users, and distribution channel.

- By Treatment Type

On the basis of treatment type, the Postmenopausal Osteoporosis Market is segmented into vitamin D, bisphosphonates, calcitonin, hormone replacement therapy tablets, estrogen antagonist, parathyroid hormone, combination therapy, and others. The Bisphosphonates segment dominated the market with a 38.64% share in 2025, owing to its long-established role as the first-line treatment for postmenopausal osteoporosis and proven effectiveness in reducing fracture risk. These drugs are widely prescribed due to their affordability, extensive clinical evidence, and broad availability across developed and emerging markets. Strong physician familiarity and inclusion in major osteoporosis treatment guidelines further support their widespread adoption. The segment also benefits from the availability of both branded and generic formulations, enhancing patient accessibility. Oral administration convenience and favorable reimbursement policies contribute to high utilization rates. Continued use in long-term osteoporosis management reinforces its dominant position in the global market.

The Parathyroid Hormone segment is projected to register the fastest growth at a CAGR of 5.9% from 2026 to 2033, driven by increasing demand for anabolic therapies that actively stimulate new bone formation rather than merely slowing bone loss. These therapies are gaining traction among patients with severe osteoporosis and those at high risk of fractures. Growing awareness of the benefits of bone-building treatments is encouraging physician adoption worldwide. Advances in biologic drug development and expanding clinical evidence are strengthening confidence in these therapies. Rising healthcare expenditure and improved access to specialty osteoporosis treatments are also supporting growth. Furthermore, increasing focus on personalized medicine and improved patient outcomes is expected to accelerate segment expansion throughout the forecast period.

- By Route of Administration

On the basis of route of administration, the Postmenopausal Osteoporosis Market is segmented into oral, parenteral, and others. The Oral segment led the market with a 57.46% share in 2025, driven by the widespread use of oral bisphosphonates and other osteoporosis medications as primary treatment options. Oral therapies offer convenience, ease of self-administration, and lower treatment costs compared to injectable alternatives. High patient acceptance and extensive availability through retail and hospital pharmacies further support segment growth. Physicians frequently prescribe oral medications for early-stage osteoporosis management due to established safety and efficacy profiles. The segment also benefits from strong reimbursement coverage and generic drug availability. Its suitability for long-term therapy continues to make oral administration the preferred route globally.

The Parenteral segment is expected to witness the fastest growth at a CAGR of 5.4% from 2026 to 2033, fueled by increasing adoption of biologics, monoclonal antibodies, and anabolic osteoporosis therapies administered through injections. These treatments offer enhanced efficacy for patients at high fracture risk and those who do not respond adequately to oral medications. Growing physician preference for targeted therapies is supporting demand across specialty care settings. Improvements in injectable drug formulations and patient adherence programs are further accelerating uptake. Expanding access to advanced osteoporosis treatments in emerging economies is contributing to market growth. In addition, rising awareness regarding fracture prevention is expected to strengthen demand for parenteral therapies over the coming years.

- By End-Users

On the basis of end-users, the Postmenopausal Osteoporosis Market is segmented into hospitals, homecare, specialty clinics, and others. The Hospitals segment dominated the market with a 46.28% share in 2025 due to the high volume of osteoporosis diagnosis, treatment initiation, and fracture management procedures performed within hospital settings. Hospitals provide comprehensive care supported by advanced diagnostic technologies, multidisciplinary treatment teams, and access to specialized therapies. The availability of bone density assessment services and fracture prevention programs further enhances their role in disease management. Patients with severe osteoporosis and complex medical conditions often receive treatment through hospital-based care pathways. Strong reimbursement mechanisms and integration with specialty departments support continued utilization. As a result, hospitals remain the leading end-user segment globally.

The Homecare segment is projected to grow at the fastest rate with a CAGR of 5.6% from 2026 to 2033, driven by increasing preference for patient-centered care and long-term disease management outside traditional healthcare facilities. Advances in self-administered therapies and remote patient monitoring technologies are making home-based osteoporosis care more feasible and effective. Elderly patients increasingly favor homecare services due to convenience and reduced hospital visits. Healthcare systems are also promoting home-based treatment models to lower overall care costs. Growing awareness regarding medication adherence and preventive care supports segment expansion. Rising adoption of telehealth and digital health solutions is expected to further accelerate growth in this segment.

- By Distribution Channel

On the basis of distribution channel, the Postmenopausal Osteoporosis Market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The Retail Pharmacy segment accounted for the largest market share of 48.83% in 2025, supported by widespread availability of osteoporosis medications and strong consumer accessibility. Retail pharmacies serve as the primary dispensing channel for oral osteoporosis treatments and long-term prescription refills. Their extensive geographic presence enables patients to access medications conveniently and consistently. Pharmacist-led counseling and medication management services further enhance treatment adherence. The availability of generic formulations and reimbursement-supported prescriptions also contributes to segment dominance. Strong integration within healthcare distribution networks continues to support market leadership.

The Online Pharmacy segment is anticipated to register the fastest growth at a CAGR of 6.2% from 2026 to 2033, driven by increasing digitalization of healthcare services and growing consumer preference for convenient medication purchasing options. Online platforms provide easy access to osteoporosis treatments, home delivery services, and competitive pricing structures. Rising internet penetration and smartphone adoption are supporting expansion across both developed and emerging markets. Patients managing chronic conditions increasingly utilize online pharmacies for recurring prescription needs. Regulatory improvements and secure digital payment systems are further strengthening consumer confidence. The growing adoption of e-pharmacy platforms is expected to significantly boost segment growth throughout the forecast period.

Postmenopausal Osteoporosis Market Regional Analysis

North America dominated the Postmenopausal Osteoporosis Market with the largest revenue share of 39.12% in 2025, supported by a high prevalence of osteoporosis, strong healthcare expenditure, widespread screening programs, and favorable reimbursement policies. The region also benefits from widespread osteoporosis screening programs, favorable reimbursement policies, and high adoption of advanced biologic and anabolic therapies. Growing prevalence of osteoporosis among aging women, increasing fracture prevention initiatives, and expanding access to bone density diagnostic services continue to drive treatment demand. Increasing focus on early diagnosis, personalized treatment approaches, and long-term disease management continues to strengthen North America's leadership position in the global market.

U.S. Postmenopausal Osteoporosis Market Insight

The U.S. postmenopausal osteoporosis market is witnessing strong growth due to rising prevalence of osteoporosis among aging women, increasing awareness regarding bone health, and expanding access to advanced treatment options. The country’s well-established healthcare infrastructure, along with growing adoption of biologics, anabolic therapies, and fracture prevention programs, is driving demand across hospitals, specialty clinics, and homecare settings. In addition, growing emphasis on early diagnosis, routine bone density screening, and long-term disease management is accelerating treatment adoption across healthcare providers and patient populations.

Europe Postmenopausal Osteoporosis Market Insight

The Europe postmenopausal osteoporosis market remains a major contributor to global revenue, driven by strong healthcare systems, increasing awareness of osteoporosis prevention, and high demand for advanced therapeutic solutions. The widespread use of bone density screening programs, biologic therapies, and fracture risk assessment tools is supporting market expansion across the region. Increasing investments in osteoporosis research, coupled with favorable reimbursement policies and a rapidly aging female population, continue to enhance the adoption of osteoporosis treatments throughout Europe.

U.K. Postmenopausal Osteoporosis Market Insight

The U.K. postmenopausal osteoporosis market is experiencing steady growth, supported by rising awareness of bone health, increasing osteoporosis screening initiatives, and expanding access to innovative treatment options. Increasing investments in preventive healthcare programs and growing demand for effective fracture prevention strategies are contributing to market growth. Furthermore, integration of digital health technologies, patient monitoring solutions, and evidence-based treatment pathways is improving disease management efficiency, positioning the U.K. as a key market for osteoporosis care and innovation.

Germany Postmenopausal Osteoporosis Market Insight

The Germany postmenopausal osteoporosis market is expanding steadily due to the country’s advanced healthcare infrastructure, strong pharmaceutical industry presence, and increasing adoption of next-generation osteoporosis therapies. Healthcare providers, specialty clinics, and research institutions are increasingly utilizing advanced diagnostic tools and targeted treatments for osteoporosis management. Continuous advancements in biologics, bone density assessment technologies, and personalized treatment approaches, along with strong government focus on healthy aging and fracture prevention, are further driving market growth in Germany.

Asia-Pacific Postmenopausal Osteoporosis Market Insight

The Asia-Pacific postmenopausal osteoporosis market is expected to witness rapid growth, driven by increasing life expectancy, expanding healthcare access, and rising awareness of osteoporosis management across countries such as China, India, and Japan. Growing awareness regarding bone health, rising adoption of advanced treatment options, and increasing demand for affordable and effective therapies are supporting regional market expansion. In addition, the growing burden of age-related bone disorders and expanding healthcare infrastructure are accelerating osteoporosis treatment adoption across both urban and rural populations.

Japan Postmenopausal Osteoporosis Market Insight

The Japan postmenopausal osteoporosis market is witnessing consistent growth due to rising prevalence of osteoporosis among elderly women, increasing healthcare investments, and expanding osteoporosis prevention initiatives. Pharmaceutical companies, healthcare providers, and research institutions are increasingly adopting advanced therapies and diagnostic technologies for fracture prevention and disease management. Moreover, increasing integration of digital healthcare solutions and the country’s focus on healthy aging and quality of life improvements are further contributing to market growth.

China Postmenopausal Osteoporosis Market Insight

The China postmenopausal osteoporosis market is growing rapidly, driven by increasing population aging, expanding healthcare infrastructure, and rising government focus on osteoporosis awareness and early diagnosis. Growing adoption of biologic therapies and advanced bone health management solutions across hospitals and specialty care centers is significantly boosting market demand. In addition, rising investments in healthcare modernization, increasing awareness regarding fracture prevention, and rapid improvements in diagnostic capabilities are positioning China as one of the fastest-growing markets for postmenopausal osteoporosis treatments globally.

Postmenopausal Osteoporosis Market Share

The postmenopausal osteoporosis industry is primarily led by well-established companies, including:

- Amgen Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Merck & Co., Inc. (U.S.)

- Pfizer Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Radius Health, Inc. (U.S.)

- Viatris Inc. (U.S.)

- Organon & Co. (U.S.)

- Theramex (U.K.)

- UCB (Belgium)

- Novartis AG (Switzerland)

- Hoffmann-La Roche Ltd (Switzerland)

- Sandoz AG (Switzerland)

- Bayer AG (Germany)

- STADA Arzneimittel AG (Germany)

- Daiichi Sankyo Company, Limited (Japan)

- Takeda Pharmaceutical Company Limited (Japan)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Zydus Lifesciences Limited (India)

- Reddy’s Laboratories Ltd. (India)

Latest Developments in Postmenopausal Osteoporosis Market

- In November 2025, Teva Pharmaceuticals received European Medicines Agency (EMA) marketing authorization for Ponlimsi (denosumab biosimilar), a biosimilar to Prolia, indicated for postmenopausal women with osteoporosis at high risk of fracture. The approval is expected to expand patient access to cost-effective osteoporosis treatments across Europe while increasing competition in the bone health therapeutics market

- In May 2024, Sandoz announced that the European Commission approved Jubbonti (denosumab biosimilar) for osteoporosis and bone disease indications. The approval strengthens the availability of lower-cost biologic alternatives for osteoporosis management and supports broader access to fracture-prevention therapies for postmenopausal women across European markets

- In April 2024, 16 Bit Inc. announced that the U.S. FDA granted De Novo marketing authorization for Rho™, an AI-enabled software platform designed to identify patients with low bone mineral density from standard X-rays. The technology aims to improve osteoporosis screening and early detection, helping healthcare providers identify high-risk postmenopausal women before fractures occur

- In April 2023, Zydus Lifesciences received final U.S. FDA approval for Estradiol Transdermal System USP (0.014 mg/day), indicated for the prevention of postmenopausal osteoporosis. The approval expanded the company’s women’s health portfolio and provided an additional hormone-based therapeutic option for osteoporosis prevention among postmenopausal women

- In December 2022, Radius Health announced that the European Commission approved ELADYNOS (abaloparatide) for the treatment of osteoporosis in postmenopausal women at increased risk of fracture. As a bone-forming anabolic therapy, ELADYNOS offers a novel treatment option aimed at reducing fracture risk and improving bone density in women with severe osteoporosis

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.