Global Potato Starch For Food Industry Market

Market Size in USD Billion

USD

3.98 Billion

USD

6.69 Billion

2025

2033

USD

3.98 Billion

USD

6.69 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.98 Billion | |

| USD 6.69 Billion | |

| % | |

|

What is the Global Potato Starch for Food Industry Market Size and Growth Rate?

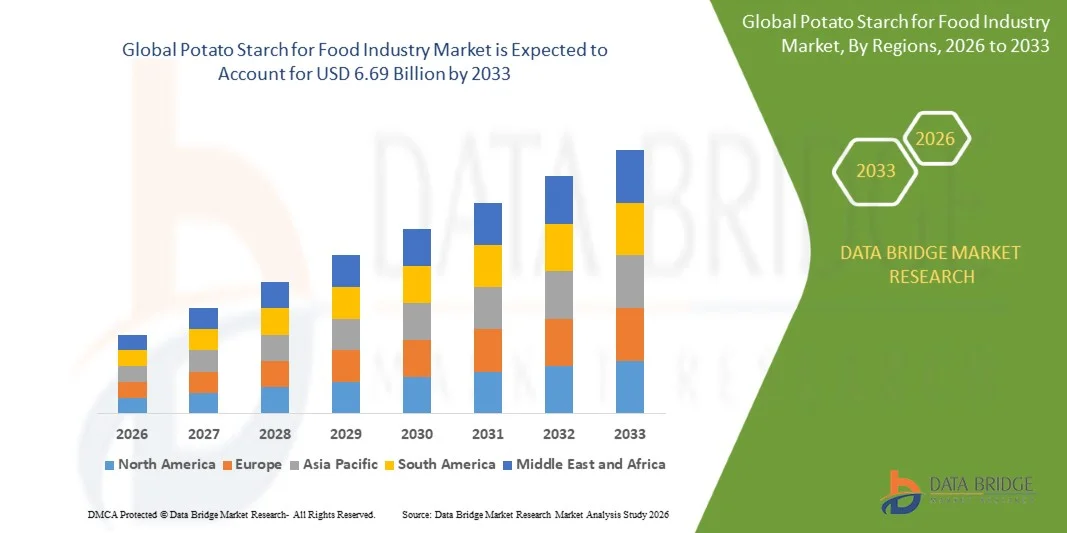

- The global potato starch for food industry market size was valued at USD 3.98 billion in 2025 and is expected to reach USD 6.69 billion by 2033, at a CAGR of 6.70% during the forecast period

- Increasing consumption of potato starch as it offer numerous health benefits which include absorption of carcinogenic and toxic compounds, regulating blood sugar levels, rising the absorption of several minerals such as magnesium and calcium, increasing popularity of the product among the vegan and health-conscious consumers, easy availability of the raw material as it is largest grown vegetable across the globe are some of the major as well as vital factors which will likely to augment the growth of the potato starch for food industry market

What are the Major Takeaways of Potato Starch for Food Industry Market?

- Rising trend of organic processed food along with new product development in food and beverages industry which will further contribute by generating massive opportunities that will lead to the growth of the potato starch for food industry market

- Growing awareness among the consumers regarding the health risks caused by the excessive carbohydrates consumption along with volatility in the prices of potato which will likely to act as market restraints factor for the growth of the potato starch for food industry

- In 2025, Asia-Pacific dominated the potato starch for food industry market with a 39.2% revenue share, supported by strong demand across China, Japan, India, and South Korea

- North America is projected to register the fastest CAGR of 11.36% from 2026 to 2033, driven by rising demand for clean-label, organic, and specialty potato starch products in the U.S. and Canada

- The Native Starch segment dominated the market with a revenue share of 58.7% in 2025, driven by its natural composition, high functional versatility, and widespread use in bakery, dairy, sauces, and snack applications

Report Scope and Potato Starch for Food Industry Market Segmentation

|

Attributes |

Potato Starch for Food Industry Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Potato Starch for Food Industry Market?

“Rising Demand for Nutrient-Enriched and Multi-Potato Starch Applications”

- The potato starch for food industry market is experiencing strong growth toward nutrient-enriched, multifunctional, and clean-label formulations, including blends with fibers, prebiotics, and plant-based ingredients to improve texture, stability, and nutritional value

- Manufacturers are introducing multi-purpose potato starch systems that support viscosity control, fat replacement, calorie reduction, and broader functional applications in bakery, dairy, confectionery, sauces, and ready-to-eat products

- Consumers are increasingly choosing natural, safe, and functional ingredients, boosting demand for potato starch over synthetic stabilizers and thickeners across food and beverage categories

- For instance, companies such as Cargill, Ingredion, Roquette, Avebe, and Tereos have expanded their potato starch portfolios with functional blends for gluten-free bakery, dairy alternatives, and clean-label processed foods

- Growing awareness of health management, clean-label diets, and dietary fiber intake is accelerating global adoption

- As demand for plant-based, multifunctional, and natural food ingredients rises, potato starch is expected to remain central to innovation in food formulation worldwide.

What are the Key Drivers of Potato Starch for Food Industry Market?

- Rising consumer preference for plant-based, clean-label, and functionally enhanced ingredients is driving strong adoption of potato starch globally

- For instance, in 2025, companies like Roquette, Cargill, and Avebe expanded their potato starch product lines for bakery, dairy alternatives, and convenience foods

- Growing global awareness of obesity management, sugar reduction, and healthy food consumption is boosting demand across North America, Europe, and Asia-Pacific

- Advancements in starch modification, granulation, and functional blending have improved water-binding, texturizing, and shelf-life performance in processed foods

- Rising demand for organic, non-GMO, vegan, and clean-label formulations is supporting market expansion, aligned with consumer preferences for sustainable and ethical ingredients

- With continuous R&D, product launches, strategic partnerships, and global distribution, the potato starch market is expected to maintain steady growth in the coming years

Which Factor is Challenging the Growth of the Potato Starch for Food Industry Market?

- High production, processing, and modification costs associated with premium potato starch and functional blends limit affordability in price-sensitive regions

- For instance, during 2024–2025, fluctuations in potato crop yields, extraction costs, and transport impacted production volumes for several manufacturers

- Strict regulatory standards for ingredient safety, clean-label claims, and food additive approvals increase operational complexity

- Limited consumer awareness in emerging markets about natural starch benefits and functional properties restricts widespread adoption

- Strong competition from corn starch, tapioca, modified food starches, and low-cost thickeners creates pricing and differentiation pressure

- To overcome these challenges, companies are focusing on efficient sourcing, cost-effective processing, regulatory compliance, and consumer education to expand global adoption of high-quality potato starch for the food industry

How is the Potato Starch for Food Industry Market Segmented?

The market is segmented on the basis of product type, nature, and end use.

• By Product Type

On the basis of product type, the potato starch for food industry market is segmented into Native Starch, Modified Starch, and Sweeteners. The Native Starch segment dominated the market with a revenue share of 58.7% in 2025, driven by its natural composition, high functional versatility, and widespread use in bakery, dairy, sauces, and snack applications. Native starches are preferred for their thickening, gelling, and stabilizing properties, as well as compatibility with gluten-free, vegan, and clean-label formulations. Manufacturers rely on native starch for cost-effective production, consistent quality, and large-scale industrial processing.

The Modified Starch segment is projected to grow at the fastest CAGR from 2026 to 2033, supported by rising demand for enhanced functional properties such as freeze-thaw stability, improved viscosity, and customized texturizing for soups, sauces, ready-to-eat meals, and frozen foods. Continuous innovation in modified starch formulations is expected to expand its adoption across diverse food categories.

• By Nature

On the basis of nature, the potato starch for food industry market is segmented into Organic and Conventional. The Conventional segment dominated the market with a revenue share of 63.5% in 2025, driven by broad availability, cost-efficient production, and strong adoption in mainstream bakery, confectionery, sauces, and snack products. Conventional potato starch provides consistent functional performance and large-scale supply, making it ideal for industrial applications.

The Organic segment is projected to grow at the fastest CAGR from 2026 to 2033, fueled by increasing consumer preference for chemical-free, non-GMO, and sustainably sourced ingredients. Organic potato starch is widely used in clean-label bakery items, premium dairy desserts, plant-based meat analogues, and health-focused snacks. Rising awareness of sustainable farming practices and environmental impact further accelerates the growth of organic formulations globally.

• By End Use

On the basis of end use, the potato starch for food industry market is segmented into Bakery, Dairy & Desserts, Soups, Sauces & Dressings, Meat & Fish, Savory & Snacks, Confectionery, Pet Food, and Others. The Bakery segment dominated the market with a revenue share of 35.8% in 2025, supported by high demand for gluten-free bread, pastries, and baked goods that require potato starch for improved texture, shelf-life, and moisture retention.

The Dairy & Desserts segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by rising consumption of yogurt, puddings, frozen desserts, and plant-based dairy alternatives, which rely on potato starch for thickening, stabilization, and creaminess. Innovations in functional, low-calorie, and clean-label dessert products continue to accelerate adoption across retail and foodservice channels globally.

Which Region Holds the Largest Share of the Potato Starch for Food Industry Market?

- In 2025, Asia-Pacific dominated the potato starch for food industry market with a 39.2% revenue share, supported by strong demand across China, Japan, India, and South Korea. Rising consumption of natural, clean-label, and plant-based ingredients in bakery, dairy, snacks, and ready-to-eat foods drives regional leadership

- Manufacturers are expanding functional and low-calorie starch-based products through innovations in texture enhancement, stabilization, and fortification

- Regulatory support for food safety, non-GMO certifications, and natural ingredient standards further strengthens market dominance. High population density, increasing disposable incomes, urbanization, and growing health-conscious consumer behavior fuel strong adoption across retail and e-commerce channels

China Potato Starch for Food Industry Market Insight

China is the largest contributor to Asia-Pacific, benefiting from robust potato cultivation, processing infrastructure, and rising demand in bakery, dairy, and functional foods. Investments in R&D, vertical integration, and eco-friendly processing enhance domestic consumption and export potential, strengthening regional leadership.

Japan Potato Starch for Food Industry Market Insight

Japan shows steady growth, driven by high consumer preference for functional, low-calorie, and clean-label starch products. Innovations in taste, purity, and blending techniques attract health-conscious consumers. Strong retail networks and regulatory support boost market expansion.

India Potato Starch for Food Industry Market Insight

India is a growing market, fueled by awareness of diabetes management, obesity reduction, and natural ingredients. Expansion of e-commerce, clean-label adoption, and rising consumption in beverages, packaged foods, and home cooking accelerate market penetration.

South Korea Potato Starch for Food Industry Market Insight

South Korea contributes significantly with rising interest in natural, plant-based starches in functional foods, bakery, and diet products. Wellness trends, K-food exports, and premium packaging innovations enhance market growth.

North America Potato Starch for Food Industry Market Insight

North America is projected to register the fastest CAGR of 11.36% from 2026 to 2033, driven by rising demand for clean-label, organic, and specialty potato starch products in the U.S. and Canada. Consumers increasingly prefer low-calorie, natural, and functional ingredients across bakery, snacks, dairy alternatives, and ready-to-eat products. Manufacturers are investing in advanced extraction, formulation technologies, and blended starch solutions. Strong retail and e-commerce penetration, combined with regulatory support and health-focused consumer trends, accelerates adoption in this high-potential growth region.

U.S. Potato Starch for Food Industry Market Insight

The U.S. is the largest contributor in North America, with high demand for specialty starches in functional foods, bakery, and snacks. Investments in advanced processing and clean-label solutions enhance market expansion.

Which are the Top Companies in Potato Starch for Food Industry Market?

The potato starch for food industry is primarily led by well-established companies, including:

- Emsland Group (Germany)

- Cargill, Incorporated (U.S.)

- Südstärke GmbH (Germany)

- PEPEES Group (Poland)

- Ingredion Incorporated (U.S.)

- Novidon (Netherlands)

- Avebe (Netherlands)

- AGRANA Beteiligungs AG (Austria)

- Tereos (France) Wikipedia

- AKV Langholt AmbA (Denmark)

- Finnamyl (Finland)

- Roquette Frères (France)

- Škrobárny Pelhrimov, a.s. (Czechia)

- MSP Starch Products Inc. (Canada)

- VIMAL PPCE (India)

- ALOJA STARKELSEN (Latvia)

- Lyckeby (Sweden)

- PPZ Trzemeszno Sp. z o.o. (Poland)

- Siddharth Starch Pvt. Ltd. (India)

- Meelunie B.V. (Netherlands)

What are the Recent Developments in Global Potato Starch for Food Industry Market?

- In January 2025, Red Bull unveiled its “Red Bull Zero” energy drink in the U.S., incorporating monk fruit extract along with other sweeteners to create a completely zero-sugar formulation, strengthening the brand’s presence in the health-focused beverage category

- In January 2024, Elo Life Systems secured USD 20.5 Mn in Series A2 funding, led by Novo Holdings and DCVC Bio, to accelerate the planned 2026 launch of a natural, plant-based monk fruit-derived sweetener, marking a major step in expanding clean-label ingredient innovation

- In October 2023, Lakanto introduced a new addition to its Potato Starch for Food Industry range, the Monkfruit Sweetener with Allulose, blending monk fruit’s natural sweetness with the unique characteristics of allulose to broaden consumer choices for natural sugar alternatives, reinforcing the company’s product diversification strategy.

- In April 2023, SweetLeaf partnered with the American Diabetes Association to promote its natural, sugar-free Potato Starch for Food Industry as a diabetes-friendly option, participating in ADA programs such as the Tour de Cure event in Arizona, enhancing the brand’s credibility within the diabetic and wellness community

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Potato Starch For Food Industry Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Potato Starch For Food Industry Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Potato Starch For Food Industry Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.