Global Powertrain Sensor Market

Market Size in USD Billion

USD

23.37 Billion

USD

29.14 Billion

2025

2033

USD

23.37 Billion

USD

29.14 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 23.37 Billion |

Market Size (Forecast Year) |

USD 29.14 Billion |

CAGR |

% |

Major Markets Players |

|

Powertrain Sensor Market Overview

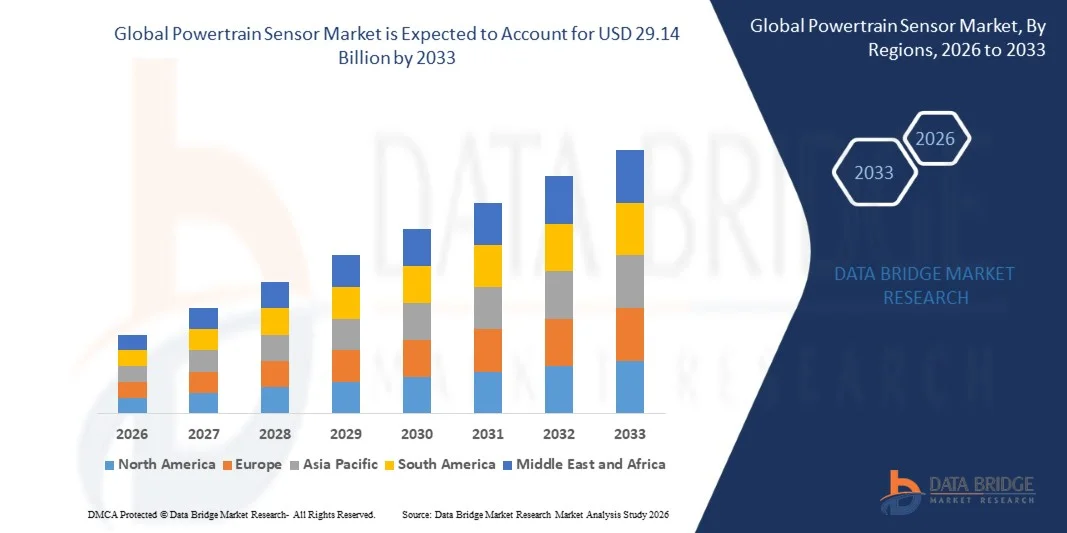

The Powertrain Sensor Market was valued at USD 23.37 billion in 2025 and is projected to reach USD 29.14 billion by 2033, growing at a CAGR of 2.80% from 2026 to 2033. The market is witnessing steady growth driven by increasing vehicle electrification, rising adoption of advanced driver-assistance systems (ADAS), and growing demand for fuel efficiency and emission control across automotive applications.

The expansion of electric and hybrid vehicles, coupled with stringent global emission regulations, is significantly boosting the integration of advanced powertrain sensors for real-time monitoring of engine performance, transmission efficiency, and battery management systems. In addition, continuous advancements in sensor technologies such as pressure sensors, temperature sensors, and speed sensors are enhancing vehicle performance, reliability, and predictive maintenance capabilities across passenger and commercial vehicle segments.

Key Market Trends & Insights

- North America dominated the powertrain sensor market with the largest revenue share of approximately 34.8% in 2025, supported by strong automotive production, early adoption of advanced vehicle technologies, and strict emission regulations. The region benefits from high penetration of connected and hybrid vehicles, driving demand for intelligent sensor systems across engine, transmission, and exhaust applications.

- Asia-Pacific powertrain sensor market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid vehicle production, rising urbanization, and increasing disposable incomes in countries such as China, India, and Japan. The region is experiencing strong demand for both ICE and electric vehicles, driving large-scale adoption of powertrain sensors.

- The Pressure Sensor segment held the largest market revenue share of approximately 29.6% in 2025, driven by its extensive deployment in fuel injection control, lubrication monitoring, and combustion chamber pressure optimization. These sensors are critical for improving engine efficiency, reducing emissions, and ensuring compliance with global regulatory standards. Rising integration of electronic control units in ICE vehicles further strengthens demand for pressure sensing solutions.

- The Temperature Sensor segment is projected to register the fastest growth with a CAGR of 9.8% from 2026 to 2033, supported by increasing focus on engine thermal efficiency and emission reduction systems. Temperature sensors are widely used in exhaust gas monitoring, coolant systems, and turbocharger protection applications. Growing demand for high-performance vehicles and stricter emission norms are further accelerating adoption across automotive OEMs.

- The Gasoline segment held the largest market revenue share of approximately 54.3% in 2025, attributed to higher global passenger vehicle production and widespread use of gasoline engines in compact and mid-sized cars. Gasoline engines increasingly rely on advanced sensor systems for real-time combustion optimization and fuel efficiency improvements. In addition, rising urban mobility demand supports segment dominance.

- The Diesel segment is projected to grow steadily at a CAGR of 7.9% from 2026 to 2033, driven by strong adoption in commercial vehicles, logistics fleets, and long-haul transportation. Diesel engines benefit significantly from sensor integration for emission control and fuel efficiency enhancement. Increasing regulatory pressure for cleaner diesel technologies is also encouraging advanced sensor deployment.

- The Engine segment accounted for the largest market revenue share of approximately 46.7% in 2025, driven by high sensor concentration for air-fuel ratio control, ignition timing, and engine performance optimization. Modern engines increasingly depend on multiple sensors for real-time diagnostics and predictive maintenance. Expanding adoption of turbocharged and hybrid engines further boosts segment growth.

- The Exhaust segment is projected to register the fastest growth at a CAGR of 10.2% from 2026 to 2033, supported by tightening emission standards such as Euro and EPA regulations. Exhaust sensors such as oxygen and NOx sensors play a key role in emission after-treatment systems. Rising adoption of catalytic converters and selective catalytic reduction systems is further driving demand.

- The ICE Propulsion segment held the largest market revenue share of approximately 71.4% in 2025, driven by the massive global installed base of internal combustion engine vehicles. These vehicles require extensive sensor integration for fuel efficiency, engine control, and emission monitoring. Despite electrification trends, ICE vehicles continue to dominate global fleets, sustaining sensor demand.

- The EV Propulsion segment is projected to register the fastest growth at a CAGR of 18.6% from 2026 to 2033, driven by rapid electrification and government incentives supporting electric mobility. EVs require advanced sensors for battery management, motor control, and thermal regulation. Increasing investments in EV infrastructure and battery technology are accelerating sensor innovation.

- The Light-Duty Vehicle segment held the largest market revenue share of approximately 62.9% in 2025, supported by high production volumes of passenger cars and light commercial vehicles. These vehicles extensively use sensors for engine control, safety systems, and efficiency optimization. Growing consumer preference for connected and fuel-efficient vehicles further supports dominance.

- The Heavy-Duty Vehicle segment is projected to grow at a CAGR of 8.7% from 2026 to 2033, driven by expansion in logistics, construction, and freight transportation sectors. Heavy-duty applications require robust sensors for durability under extreme operating conditions. Increasing fleet electrification and emission compliance requirements are also boosting adoption.

- The BEV segment held the largest market revenue share of approximately 58.2% in 2025, driven by strong global adoption of fully electric vehicles and government-backed electrification policies. BEVs rely heavily on sensor systems for battery monitoring, power distribution, and thermal control. Expanding charging infrastructure further supports market dominance.

- The FCEV segment is projected to register the fastest growth at a CAGR of 21.3% from 2026 to 2033, driven by increasing investment in hydrogen fuel technologies. Fuel cell vehicles require specialized sensors for hydrogen flow, pressure control, and safety monitoring. Growing adoption in heavy-duty and long-range transport applications is accelerating segment expansion.

- The Temperature Sensor segment held the largest market revenue share of approximately 26.8% in 2025, driven by critical use in battery thermal management systems and electric drivetrain efficiency. These sensors ensure safe operating conditions and prevent overheating in high-energy battery packs. Rising EV adoption significantly increases demand for thermal monitoring solutions.

- The Current Sensor segment is projected to register the fastest growth at a CAGR of 19.4% from 2026 to 2033, driven by increasing need for precise battery state monitoring and energy optimization. Current sensors play a key role in managing charging cycles and protecting electrical components. Growing complexity of EV power electronics is further boosting adoption across automotive platforms.

Market Size & Forecast

- Global Market Value (2025): USD 23.37 Billion

- Expected Market Value (2033): USD 29.14 Billion

- Forecast CAGR (2026–2033): 2.80%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Powertrain Sensor Market Segmentation

|

Attributes |

Powertrain Sensor Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Continental AG (Germany) |

|

Market Opportunities |

• Rising Adoption Of Electric Vehicles |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Powertrain Sensor Market Trends

Trend: Growth In Electrification, Advanced Emission Control, And Intelligent Vehicle Monitoring Systems

Increasing demand for fuel-efficient, low-emission, and software-driven vehicles is accelerating the adoption of advanced powertrain sensors across automotive systems. Traditional mechanical monitoring approaches are being replaced by high-precision electronic sensors that provide real-time data on engine performance, transmission behavior, and exhaust emissions, enabling improved efficiency and compliance with global emission standards such as Euro 6 and China VI.

In modern electric and hybrid vehicles, manufacturers are integrating powertrain sensors for battery monitoring, torque measurement, and thermal management, For instance in EV platforms from leading OEMs such as Tesla and BYD, multi-point temperature and pressure sensors are embedded within battery packs and drivetrains to enhance safety and extend component lifespan. In internal combustion engine vehicles, oxygen sensors and NOx sensors are widely used to optimize combustion efficiency and reduce harmful emissions in real time.

The rapid expansion of autonomous and connected vehicle systems is also increasing demand for intelligent sensor networks capable of supporting predictive diagnostics and real-time performance optimization. In addition, industrial automotive testing environments and motorsport applications continue to adopt high-accuracy powertrain sensors for performance tuning and durability assessment. Growing validation through automotive testing programs in 2025 across Europe integrating next-generation MEMS-based pressure and speed sensors has shown fuel efficiency improvements of approximately 5–8% under optimized engine load conditions.

Powertrain Sensor Market Dynamics

Key Market Driver: Rising Demand For Vehicle Electrification And Emission Compliance

Automotive manufacturers are under increasing regulatory and environmental pressure to reduce carbon emissions and improve fuel efficiency, driving strong adoption of advanced powertrain sensing technologies. Governments across regions are tightening emission norms, such as Euro 7 standards expected to be implemented in the late 2020s, compelling OEMs to integrate high-precision sensors for real-time monitoring of combustion and exhaust systems.

Automakers such as Volkswagen, Toyota, and General Motors are increasingly deploying multi-sensor architectures in hybrid and electric powertrains to optimize energy usage and enhance vehicle performance. For instance in hybrid vehicle platforms, integrated torque and temperature sensors are used to balance engine and electric motor output for improved efficiency and reduced fuel consumption.

Similarly, the growing adoption of electric vehicles is accelerating demand for battery management system sensors that monitor voltage, current, and thermal conditions to ensure operational safety and performance stability. Industry deployment data from 2024 indicates that EV platforms using advanced sensor-based powertrain control systems can achieve energy efficiency improvements of around 6–10% compared to conventional control architectures.

Key Restraint/Challenge: High System Complexity And Cost Of Advanced Sensor Integration

The integration of advanced powertrain sensors increases overall vehicle system complexity due to the need for high-speed data processing, calibration accuracy, and compatibility with electronic control units. These sensors require precise engineering and frequent calibration, particularly in high-temperature and high-vibration automotive environments, which increases maintenance requirements and operational challenges.

In addition, high manufacturing costs associated with MEMS-based sensors, semiconductor materials, and advanced signal processing units create affordability challenges for entry-level vehicle segments and cost-sensitive markets. Supply chain constraints in semiconductor manufacturing further impact production scalability and pricing stability.

Industry benchmarks indicate that advanced multi-functional powertrain sensor systems can increase overall vehicle electronics costs by approximately 8–12% compared to traditional mechanical sensing systems, limiting adoption in low-cost automotive segments in emerging economies.

Key Market Opportunity: Integration With Electric Vehicles And Autonomous Driving Platforms

The rapid expansion of electric vehicles, autonomous driving systems, and connected mobility solutions is creating significant opportunities for advanced powertrain sensor deployment. Modern EV architectures require precise monitoring of battery health, motor torque, and thermal conditions to ensure optimal performance and safety under varying driving conditions.

Automotive OEMs are increasingly integrating multi-functional powertrain sensors, For instance in next-generation EV platforms for real-time energy management, regenerative braking optimization, and predictive maintenance capabilities. In autonomous vehicles, sensor fusion systems combining powertrain data with ADAS inputs are enabling improved decision-making and vehicle control accuracy.

In addition, advancements in semiconductor-based sensor miniaturization and wireless sensing technologies are opening new opportunities across shared mobility fleets, logistics vehicles, and smart transportation systems. Pilot deployments in 2025 across South Korea and Germany integrating AI-enabled powertrain sensor systems have demonstrated predictive maintenance accuracy improvements of nearly 12–15%, reducing unexpected drivetrain failures and maintenance downtime.

Powertrain Sensor Market Scope

The market is segmented on the basis of sensor type for ICE vehicle, fuel type, powertrain subsystem, propulsion type, vehicle type, electric vehicle type, and sensor type for electric vehicle

• By Sensor Type for ICE Vehicle

On the basis of sensor type for ICE vehicle, the powertrain sensor market is segmented into Pressure Sensor, Temperature Sensor, Speed Sensor, Position Sensor, and Other. The Pressure Sensor segment held the largest market revenue share of approximately 29.6% in 2025, driven by its extensive deployment in fuel injection control, lubrication monitoring, and combustion chamber pressure optimization. These sensors are critical for improving engine efficiency, reducing emissions, and ensuring compliance with global regulatory standards. Rising integration of electronic control units in ICE vehicles further strengthens demand for pressure sensing solutions.

The Temperature Sensor segment is projected to register the fastest growth with a CAGR of 9.8% from 2026 to 2033, supported by increasing focus on engine thermal efficiency and emission reduction systems. Temperature sensors are widely used in exhaust gas monitoring, coolant systems, and turbocharger protection applications. Growing demand for high-performance vehicles and stricter emission norms are further accelerating adoption across automotive OEMs.

• By Fuel Type

On the basis of fuel type, the market is segmented into Diesel and Gasoline. The Gasoline segment held the largest market revenue share of approximately 54.3% in 2025, attributed to higher global passenger vehicle production and widespread use of gasoline engines in compact and mid-sized cars. Gasoline engines increasingly rely on advanced sensor systems for real-time combustion optimization and fuel efficiency improvements. In addition, rising urban mobility demand supports segment dominance.

The Diesel segment is projected to grow steadily at a CAGR of 7.9% from 2026 to 2033, driven by strong adoption in commercial vehicles, logistics fleets, and long-haul transportation. Diesel engines benefit significantly from sensor integration for emission control and fuel efficiency enhancement. Increasing regulatory pressure for cleaner diesel technologies is also encouraging advanced sensor deployment.

• By Powertrain Subsystem

On the basis of powertrain subsystem, the market is segmented into Engine, Transmission, and Exhaust. The Engine segment accounted for the largest market revenue share of approximately 46.7% in 2025, driven by high sensor concentration for air-fuel ratio control, ignition timing, and engine performance optimization. Modern engines increasingly depend on multiple sensors for real-time diagnostics and predictive maintenance. Expanding adoption of turbocharged and hybrid engines further boosts segment growth.

The Exhaust segment is projected to register the fastest growth at a CAGR of 10.2% from 2026 to 2033, supported by tightening emission standards such as Euro and EPA regulations. Exhaust sensors such as oxygen and NOx sensors play a key role in emission after-treatment systems. Rising adoption of catalytic converters and selective catalytic reduction systems is further driving demand.

• By Propulsion Type

On the basis of propulsion type, the market is segmented into ICE Propulsion and EV Propulsion. The ICE Propulsion segment held the largest market revenue share of approximately 71.4% in 2025, driven by the massive global installed base of internal combustion engine vehicles. These vehicles require extensive sensor integration for fuel efficiency, engine control, and emission monitoring. Despite electrification trends, ICE vehicles continue to dominate global fleets, sustaining sensor demand.

The EV Propulsion segment is projected to register the fastest growth at a CAGR of 18.6% from 2026 to 2033, driven by rapid electrification and government incentives supporting electric mobility. EVs require advanced sensors for battery management, motor control, and thermal regulation. Increasing investments in EV infrastructure and battery technology are accelerating sensor innovation.

• By Vehicle Type

On the basis of vehicle type, the market is segmented into Light-Duty Vehicle and Heavy-Duty Vehicle. The Light-Duty Vehicle segment held the largest market revenue share of approximately 62.9% in 2025, supported by high production volumes of passenger cars and light commercial vehicles. These vehicles extensively use sensors for engine control, safety systems, and efficiency optimization. Growing consumer preference for connected and fuel-efficient vehicles further supports dominance.

The Heavy-Duty Vehicle segment is projected to grow at a CAGR of 8.7% from 2026 to 2033, driven by expansion in logistics, construction, and freight transportation sectors. Heavy-duty applications require robust sensors for durability under extreme operating conditions. Increasing fleet electrification and emission compliance requirements are also boosting adoption.

• By Electric Vehicle Type

On the basis of electric vehicle type, the market is segmented into BEV, PHEV, and FCEV. The BEV segment held the largest market revenue share of approximately 58.2% in 2025, driven by strong global adoption of fully electric vehicles and government-backed electrification policies. BEVs rely heavily on sensor systems for battery monitoring, power distribution, and thermal control. Expanding charging infrastructure further supports market dominance.

The FCEV segment is projected to register the fastest growth at a CAGR of 21.3% from 2026 to 2033, driven by increasing investment in hydrogen fuel technologies. Fuel cell vehicles require specialized sensors for hydrogen flow, pressure control, and safety monitoring. Growing adoption in heavy-duty and long-range transport applications is accelerating segment expansion.

• By Sensor Type for Electric Vehicle

On the basis of sensor type for electric vehicle, the market is segmented into Speed Sensor, Temperature Sensor, Pressure Sensor, Position Sensor, Current Sensor, Voltage Sensor, and Other. The Temperature Sensor segment held the largest market revenue share of approximately 26.8% in 2025, driven by critical use in battery thermal management systems and electric drivetrain efficiency. These sensors ensure safe operating conditions and prevent overheating in high-energy battery packs. Rising EV adoption significantly increases demand for thermal monitoring solutions.

The Current Sensor segment is projected to register the fastest growth at a CAGR of 19.4% from 2026 to 2033, driven by increasing need for precise battery state monitoring and energy optimization. Current sensors play a key role in managing charging cycles and protecting electrical components. Growing complexity of EV power electronics is further boosting adoption across automotive platforms.

Powertrain Sensor Market Regional Analysis

North America Powertrain Sensor Market Insight

North America dominated the powertrain sensor market with the largest revenue share of approximately 34.8% in 2025, supported by strong automotive production, early adoption of advanced vehicle technologies, and strict emission regulations. The region benefits from high penetration of connected and hybrid vehicles, driving demand for intelligent sensor systems across engine, transmission, and exhaust applications. Increasing investments in vehicle electrification and autonomous driving technologies further strengthen market expansion. In addition, the presence of major automotive OEMs and technology providers supports continuous innovation in sensor integration for enhanced vehicle performance and efficiency.

U.S. Powertrain Sensor Market Insight

The U.S. powertrain sensor market captured the largest revenue share in North America in 2025, driven by rapid adoption of fuel-efficient and emission-compliant vehicles. Consumers and fleet operators are increasingly prioritizing advanced engine management systems, boosting demand for pressure, temperature, and position sensors. The growing shift toward hybrid and electric vehicles is further accelerating sensor deployment across battery and drivetrain systems. Moreover, strong R&D investments in automotive electronics and the integration of AI-based diagnostics are significantly contributing to market growth.

Europe Powertrain Sensor Market Insight

The Europe powertrain sensor market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent emission regulations such as Euro standards and the rapid transition toward electric mobility. The region’s strong focus on sustainability and fuel efficiency is increasing the adoption of advanced sensor technologies in both ICE and EV platforms. Rising demand for connected vehicles and smart mobility solutions is also supporting market expansion. In addition, automotive manufacturers are increasingly integrating multi-sensor architectures to improve vehicle safety, performance, and regulatory compliance.

U.K. Powertrain Sensor Market Insight

The U.K. powertrain sensor market is expected to grow at a strong pace from 2026 to 2033, driven by increasing adoption of hybrid vehicles and rising demand for low-emission transport solutions. Growing consumer preference for advanced vehicle diagnostics and predictive maintenance is supporting sensor integration across automotive systems. In addition, government initiatives promoting electrification and smart mobility are encouraging OEMs to adopt next-generation powertrain sensor technologies. Expansion of connected vehicle infrastructure is also contributing to market growth.

Germany Powertrain Sensor Market Insight

The Germany powertrain sensor market is expected to witness significant growth from 2026 to 2033, supported by the country’s strong automotive manufacturing base and leadership in engineering innovation. Demand for high-precision sensors is increasing due to the rapid shift toward electric and hybrid powertrains. German OEMs are heavily investing in advanced sensor systems to improve efficiency, emission control, and drivetrain optimization. Furthermore, the country’s emphasis on Industry 4.0 and smart manufacturing is accelerating the integration of intelligent automotive sensor solutions.

Asia-Pacific Powertrain Sensor Market Insight

The Asia-Pacific powertrain sensor market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid vehicle production, rising urbanization, and increasing disposable incomes in countries such as China, India, and Japan. The region is experiencing strong demand for both ICE and electric vehicles, driving large-scale adoption of powertrain sensors. Government initiatives promoting electric mobility and smart transportation are further accelerating market expansion. In addition, Asia-Pacific serves as a major manufacturing hub for automotive components, improving affordability and accessibility of advanced sensor technologies.

Japan Powertrain Sensor Market Insight

The Japan powertrain sensor market is expected to grow steadily from 2026 to 2033, driven by the country’s strong focus on automotive innovation and high demand for fuel-efficient vehicles. Japan’s advanced automotive industry emphasizes precision engineering, leading to widespread use of high-performance sensors in engine and hybrid systems. The increasing adoption of electric vehicles and hybrid electric vehicles is further boosting sensor demand. Moreover, integration of smart diagnostics and IoT-enabled automotive systems is enhancing overall market development.

China Powertrain Sensor Market Insight

The China powertrain sensor market accounted for the largest revenue share in Asia-Pacific in 2025, supported by high vehicle production, rapid electrification, and strong domestic automotive manufacturing capabilities. The country’s expanding electric vehicle ecosystem is significantly increasing demand for advanced sensor systems used in battery, motor, and power management applications. Government policies promoting new energy vehicles and smart mobility are further driving adoption. In addition, the presence of large-scale OEMs and cost-effective manufacturing infrastructure is strengthening China’s leadership in the regional market.

Powertrain Sensor Market Share

The Powertrain Sensor industry is primarily led by well-established companies, including:

• Continental AG (Germany)

• Robert Bosch GmbH (Germany)

• DENSO CORPORATION (Japan)

• HELLA GmbH & Co. KGaA (Germany)

• VALEO SERVICE (France)

• Mitsubishi Electric Automotive America Inc. (U.S.)

• Infineon Technologies AG (Germany)

• Texas Instruments Incorporated (U.S.)

• NXP Semiconductors (Netherlands)

• TE Connectivity (U.S.)

• Littelfuse, Inc. (U.S.)

• Allegro MicroSystems, Inc. (U.S.)

• TDK-Micronas GmbH (Germany)

• Melexis (Belgium)

• HYUNDAI KEFICO Corporation (South Korea)

• PCB Piezotronics, Inc. (U.S.)

• Kyocera (Japan)

• Murata Manufacturing Co., Ltd (Japan)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.