Global Precision Diagnostics Service Platforms Market

Market Size in USD Billion

USD

2.12 Billion

USD

8.46 Billion

2025

2033

USD

2.12 Billion

USD

8.46 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.12 Billion | |

| USD 8.46 Billion | |

| % | |

|

Precision Diagnostics Service Platforms Market Overview

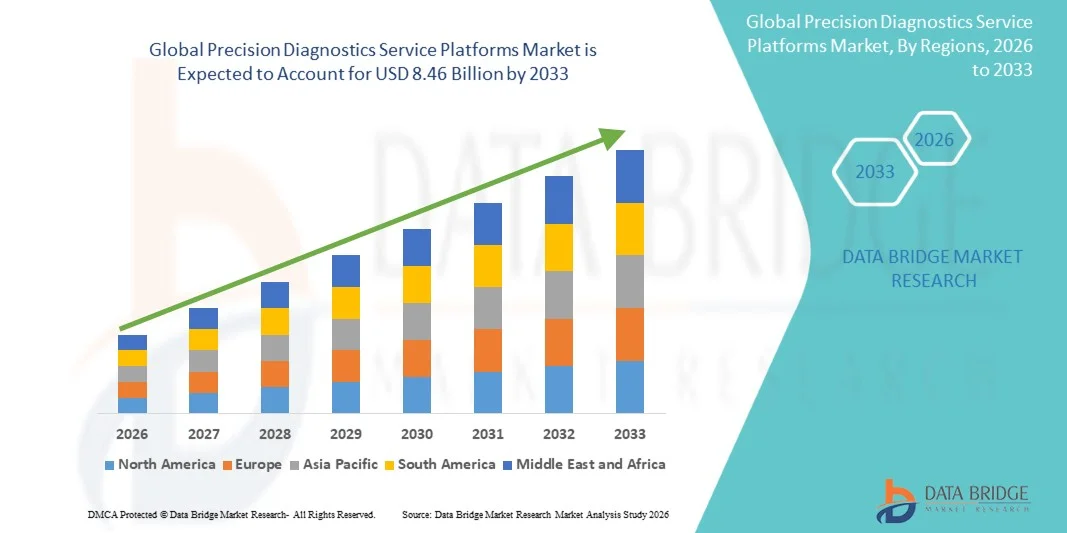

The Precision Diagnostics Service Platforms Market was valued at USD 2.12 billion in 2025 and is projected to reach USD 8.46 billion by 2033, growing at a CAGR of 18.90% from 2026 to 2033. The Precision Diagnostics Service Platforms Market is experiencing consistent growth driven by rising demand for early, accurate, and personalized disease detection solutions, along with rapid advancements in molecular diagnostics, biomarker analysis, and AI-enabled diagnostic platforms. Increasing prevalence of chronic diseases such as cancer, cardiovascular disorders, and genetic conditions is significantly boosting the adoption of precision diagnostics across healthcare systems worldwide.

The growing shift toward personalized medicine, combined with advancements in genomic sequencing, liquid biopsy technologies, and bioinformatics-driven diagnostic interpretation, is further accelerating market expansion. Hospitals, diagnostic laboratories, and pharmaceutical companies are increasingly integrating precision diagnostic platforms to improve treatment selection, patient outcomes, and clinical decision-making efficiency. In addition, rising healthcare expenditure, supportive government initiatives for precision medicine programs, and expanding use of companion diagnostics in drug development are strengthening market growth. The integration of cloud-based diagnostic platforms, AI-powered analytics, and real-time data interpretation tools is also transforming traditional diagnostic workflows into more efficient, scalable, and data-driven systems across global healthcare networks.

Key Market Trends & Insights

- North America dominated the Precision Diagnostics Service Platforms Market with the largest revenue share of 34.62% in 2025, supported by advanced healthcare infrastructure, strong adoption of genomic and molecular diagnostic technologies, and significant investments in precision medicine programs. The presence of leading diagnostic companies, well-established laboratory networks, and favorable reimbursement frameworks further strengthens regional dominance.

- The Molecular Diagnostics Services segment led the market with a 42.18% share in 2025, driven by increasing demand for early and accurate disease detection, widespread use in oncology and infectious disease testing, and growing integration of AI-based diagnostic interpretation tools in clinical workflows.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.1% from 2026 to 2033, fueled by rising healthcare expenditure, expanding diagnostic laboratory networks, increasing adoption of precision medicine, and growing prevalence of chronic and genetic diseases in China, India, and Japan.

- The Companion Diagnostics Services segment is expected to be the fastest-growing service type, projected to register a CAGR of 8.3%, driven by the rapid expansion of targeted therapies in oncology and increasing collaboration between pharmaceutical companies and diagnostic platform providers.

- The Hospitals & Diagnostic Laboratories segment dominated the end-user category with a 48.76% revenue share in 2025, owing to high patient inflow, strong adoption of advanced diagnostic technologies, and increasing demand for centralized, high-throughput testing services.

- The Pharmaceutical & Biotechnology Companies segment is expected to be the fastest-growing end-user category, registering a CAGR of 8.5%, driven by rising use of precision diagnostics in drug development, clinical trials, and companion diagnostic integration for targeted therapies.

Market Size & Forecast

- Global Market Value (2025): USD 2.12 Billion

- Expected Market Value (2033): USD 8.46 Billion

- Forecast CAGR (2026–2033): 18.90%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Precision Diagnostics Service Platforms Market Segmentation

|

Attributes |

Precision Diagnostics Service Platforms Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Illumina Inc. (U.S.) |

|

Market Opportunities |

· Expansion of AI-Driven Diagnostic Platforms · Growth in Companion Diagnostics for Targeted Therapies · Expansion in Emerging Healthcare Markets and Genomic Testing Infrastructure |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Precision Diagnostics Service Platforms Market Trends

Trend: Growth in AI-Driven Personalized and Data-Centric Healthcare Diagnostics

The Precision Diagnostics Service Platforms Market is witnessing strong growth driven by increasing adoption of AI-enabled genomic analysis, next-generation sequencing (NGS), and biomarker-based testing across clinical and research settings. Healthcare providers are increasingly shifting toward data-driven diagnostic ecosystems that enable early disease detection and personalized treatment planning. For instance, Illumina’s sequencing platforms have enabled large-scale genomic initiatives such as population-level cancer and rare disease studies, significantly improving diagnostic accuracy. In addition, cloud-based diagnostic platforms and interoperable health data systems are enhancing real-time access to patient genomic and clinical data, supporting precision medicine adoption across hospitals and laboratories worldwide.

Precision Diagnostics Service Platforms Market Dynamics

Key Market Driver: Rising Adoption of Precision Medicine and Genomic Testing in Disease Management

The rapid expansion of precision medicine programs and increasing prevalence of cancer, cardiovascular disorders, and rare genetic diseases are major drivers of the global market. According to global oncology data trends, cancer cases are expected to surpass 29 million annually by 2040, significantly increasing demand for molecular and companion diagnostics. Pharmaceutical companies and diagnostic providers are increasingly collaborating to integrate biomarker-based testing into clinical trials and targeted therapy development. For example, Roche’s Foundation Medicine platform is widely used for comprehensive genomic profiling in oncology, enabling treatment selection based on tumor-specific mutations. The growing use of liquid biopsy technologies and next-generation sequencing is further improving non-invasive early detection and disease monitoring capabilities.

Key Restraint/Challenge: High Cost of Advanced Diagnostic Technologies and Limited Accessibility in Emerging Markets

A major challenge in the precision diagnostics market is the high cost of advanced genomic sequencing systems, molecular testing platforms, and associated bioinformatics infrastructure. Full genomic sequencing and advanced biomarker analysis can still cost hundreds to thousands of dollars per patient depending on test complexity, limiting adoption in cost-sensitive healthcare systems. In addition, limited reimbursement policies in several developing regions restrict patient access to advanced diagnostic services. Smaller diagnostic laboratories also face challenges related to infrastructure requirements, skilled workforce shortages, and data management complexities. The lack of standardized regulatory frameworks for genomic data interpretation across countries further slows widespread adoption.

Key Market Opportunity: Expansion of AI-Integrated Diagnostic Platforms and Global Precision Medicine Initiatives

The integration of artificial intelligence with precision diagnostics is creating significant market opportunities by enabling faster and more accurate interpretation of complex genomic and clinical datasets. AI-driven platforms can analyze multi-omics data, identify disease biomarkers, and support real-time clinical decision-making. Large-scale initiatives such as the U.S. “All of Us” Research Program and the UK Biobank project are accelerating demand for advanced diagnostic analytics platforms. In addition, expansion of national genomic programs in China, India, and the Middle East is driving investment in sequencing infrastructure and diagnostic data platforms. The growing shift toward decentralized diagnostics, cloud-based laboratory systems, and telemedicine-enabled testing is further opening new avenues for scalable and accessible precision healthcare solutions globally.

Precision Diagnostics Service Platforms Market Scope

The Precision Diagnostics Service Platforms market is segmented on the basis of service type and end user.

- By Service Type

On the basis of service type, the Precision Diagnostics Service Platforms Market is segmented into genetic testing services, molecular diagnostics services, biomarker-based testing services, and companion diagnostics services. The Molecular Diagnostics Services segment dominated the market with a 42.18% revenue share in 2025, driven by increasing demand for early disease detection, widespread adoption in oncology and infectious disease testing, and strong integration of AI-enabled diagnostic interpretation tools in clinical workflows. High adoption by hospitals and diagnostic laboratories for accurate, rapid, and scalable testing solutions further strengthens this segment’s dominance globally.

The Companion Diagnostics Services segment is expected to be the fastest-growing, registering a CAGR of 8.3% from 2026 to 2033, driven by rising demand for targeted therapies in oncology and precision medicine. Increasing collaboration between pharmaceutical companies and diagnostic platform providers to identify patient-specific biomarkers for drug response is accelerating adoption. Expanding clinical trials for personalized therapies and regulatory approvals for biomarker-linked drugs are further boosting growth across developed and emerging healthcare markets.

- By End User

On the basis of end user, the Precision Diagnostics Service Platforms Market is segmented into hospitals & diagnostic laboratories, research & academic institutes, pharmaceutical & biotechnology companies, and specialty clinics. The Hospitals & Diagnostic Laboratories segment dominated the market with a 48.76% revenue share in 2025, owing to high patient inflow, strong adoption of molecular and genomic testing technologies, and increasing demand for centralized high-throughput diagnostic services. The presence of advanced laboratory infrastructure and expanding use of precision medicine workflows further reinforces this segment’s leading position.

The Pharmaceutical & Biotechnology Companies segment is expected to be the fastest-growing, registering a CAGR of 8.5% from 2026 to 2033, driven by rising integration of precision diagnostics in drug discovery, clinical trials, and companion diagnostic development. Increasing use of genomic profiling for patient stratification and biomarker identification is accelerating adoption. Growing investments in targeted therapy development and personalized medicine pipelines are further strengthening demand for advanced diagnostic service platforms globally.

Precision Diagnostics Service Platforms Market Regional Analysis

North America dominated the Precision Diagnostics Service Platforms Market with the largest revenue share of 34.62% in 2025, supported by advanced healthcare infrastructure, strong adoption of genomic and molecular diagnostic technologies, and significant investments in precision medicine programs. The presence of leading diagnostic companies, well-established laboratory networks, and favorable reimbursement frameworks further strengthens regional dominance. The region also benefits from high integration of AI-driven diagnostic platforms, widespread adoption of next-generation sequencing (NGS), and increasing use of biomarker-based testing across oncology, infectious diseases, and rare genetic disorders. Expanding collaborations between pharmaceutical companies and diagnostic service providers further enhance clinical application of precision diagnostics across the U.S. and Canada.

U.S. Precision Diagnostics Service Platforms Market Insight

The U.S. Precision Diagnostics Service Platforms market is witnessing strong growth due to rising investments in precision medicine initiatives, genomic sequencing programs, and advanced molecular diagnostic infrastructure. The country’s strong biotechnology ecosystem, along with rapid adoption of AI-enabled diagnostic interpretation tools and cloud-based laboratory platforms, is driving demand across hospitals, diagnostic laboratories, and pharmaceutical companies. In addition, increasing focus on early disease detection, cancer screening programs, and personalized treatment pathways is accelerating the adoption of precision diagnostic solutions nationwide.

Europe Precision Diagnostics Service Platforms Market Insight

The Europe Precision Diagnostics Service Platforms market remains a key contributor to global revenue, accounting for a significant share in 2025, supported by strong healthcare systems, advanced diagnostic infrastructure, and rapid adoption of precision medicine technologies. The region benefits from well-established genomic and molecular diagnostic capabilities, strong regulatory frameworks under the European Medicines Agency (EMA), and increasing integration of AI-enabled diagnostic platforms across hospitals, laboratories, and research institutions. Growing investments in personalized medicine programs and expanding clinical research networks across countries such as France, Italy, and the Nordics are further strengthening market expansion throughout Europe. The widespread adoption of advanced diagnostic service platforms in oncology, rare disease screening, and infectious disease management is also driving demand across public and private healthcare systems. In addition, Europe’s strong emphasis on early disease detection, preventive healthcare strategies, and cross-border healthcare initiatives continues to support sustained market growth. Increasing collaboration between biotech firms, diagnostic laboratories, and academic institutions is further accelerating innovation in precision diagnostics across the region.

U.K. Precision Diagnostics Service Platforms Market Insight

The U.K. Precision Diagnostics Service Platforms market is witnessing steady growth, driven by strong adoption of genomic testing programs, expansion of the National Health Service (NHS) precision medicine initiatives, and increasing use of advanced molecular diagnostics in clinical workflows. Rising investments in early cancer detection programs, rare disease diagnosis, and pharmacogenomics are significantly strengthening demand for high-accuracy diagnostic platforms.

In addition, the U.K.’s strong research ecosystem, supported by institutions such as Genomics England and leading academic hospitals, is accelerating innovation in AI-driven diagnostics and biomarker-based testing. Growing partnerships between healthcare providers and diagnostic technology companies are further enhancing access to advanced testing solutions, positioning the U.K. as a major innovation hub in the European precision diagnostics landscape.

Germany Precision Diagnostics Service Platforms Market Insight

The Germany Precision Diagnostics Service Platforms market is expanding steadily, supported by the country’s strong healthcare infrastructure, advanced laboratory networks, and leadership in biomedical research. Germany’s robust pharmaceutical and biotechnology sector is a key driver of demand for molecular diagnostics, genetic testing, and companion diagnostics services, particularly in oncology and chronic disease management.

Government-backed healthcare modernization programs and strong funding for precision medicine research are further accelerating adoption of advanced diagnostic platforms. In addition, Germany’s focus on digital health transformation, including AI-assisted diagnostics and integrated laboratory information systems, is improving efficiency and accuracy across clinical workflows. The presence of leading diagnostic companies and research institutes continues to reinforce Germany’s position as a major European hub for precision diagnostics innovation.

Asia-Pacific Precision Diagnostics Service Platforms Market Insight

Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.1% from 2026 to 2033, fueled by rising healthcare expenditure, expanding diagnostic laboratory networks, increasing adoption of precision medicine, and growing prevalence of chronic and genetic diseases in China, India, and Japan. Rapid healthcare infrastructure development, government-backed genomic research initiatives, and increasing awareness of early disease detection are further supporting regional market expansion.

Japan Precision Diagnostics Service Platforms Market Insight

The Japan Precision Diagnostics Service Platforms market is witnessing steady growth driven by increasing adoption of advanced genomic sequencing technologies, rising cancer screening programs, and strong focus on personalized medicine. Healthcare providers and research institutions are increasingly integrating molecular diagnostics and AI-based diagnostic analytics to improve early detection and treatment accuracy. The country’s aging population and high burden of chronic diseases are further driving demand for advanced precision diagnostic services.

China Precision Diagnostics Service Platforms Market Insight

The China Precision Diagnostics Service Platforms market is expanding rapidly due to strong government support for precision medicine, rising investment in healthcare digitization, and increasing deployment of large-scale genomic sequencing programs. Growing adoption of AI-enabled diagnostic platforms, expansion of hospital laboratory infrastructure, and rising prevalence of cancer and genetic disorders are significantly boosting market demand. In addition, collaborations between domestic biotech firms and global diagnostic companies are accelerating technology transfer and innovation in the country’s precision diagnostics ecosystem.

Precision Diagnostics Service Platforms Market Share

The Precision Diagnostics Service Platforms industry is primarily led by well-established companies, including:

- Illumina Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Qiagen N.V. (Netherlands)

- Bio-Rad Laboratories Inc. (U.S.)

- Agilent Technologies Inc. (U.S.)

- Danaher Corporation (U.S.)

- Abbott Laboratories (U.S.)

- Siemens Healthineers AG (Germany)

- PerkinElmer Inc. (U.S.)

- Guardant Health Inc. (U.S.)

- Foundation Medicine Inc. (U.S.)

- Exact Sciences Corporation (U.S.)

- Myriad Genetics Inc. (U.S.)

- BGI Genomics Co. Ltd. (China)

- SOPHiA GENETICS SA (Switzerland)

- Invitae Corporation (U.S.)

- Natera Inc. (U.S.)

- GE HealthCare Technologies Inc. (U.S.)

Latest Developments in Precision Diagnostics Service Platforms Market

- In June 2021, Illumina completed its acquisition of GRAIL, a cancer detection company developing multi-cancer early detection blood testing platforms. The acquisition strengthened Illumina’s position in liquid biopsy and precision oncology diagnostics by integrating GRAIL’s Galleri test development capabilities with Illumina’s next-generation sequencing (NGS) platforms. The deal marked one of the most significant consolidations in the precision diagnostics space, highlighting the growing importance of early cancer detection technologies

- In September 2022, Illumina announced the NovaSeq X and NovaSeq X Plus sequencing systems, its next-generation high-throughput genomic platforms. These systems were designed to significantly reduce sequencing costs while increasing speed and accuracy for large-scale genomic analysis. The launch reinforced Illumina’s leadership in precision diagnostics infrastructure, enabling broader adoption of population-scale sequencing and clinical genomics applications

- In January 2023, Illumina officially launched the NovaSeq X Series globally for clinical and research applications. The platform introduced enhanced flow cell chemistry and improved automation, enabling faster turnaround times for genomic sequencing in oncology, rare disease diagnosis, and reproductive health. This launch supported the expansion of precision medicine programs worldwide

- In March 2023, the U.S. Food and Drug Administration (FDA) granted Breakthrough Device Designation to Guardant Health’s Shield blood test for colorectal cancer screening. The designation accelerated the development and regulatory pathway of this liquid biopsy-based diagnostic platform, reflecting increasing adoption of non-invasive precision diagnostics for early cancer detection and population screening programs

- In May 2023, Thermo Fisher Scientific expanded its precision diagnostics portfolio through enhancements to its Ion Torrent Genexus Dx Integrated Sequencer platform. The system upgrade focused on improving automation, reducing hands-on time, and enabling rapid molecular diagnostic workflows for infectious diseases, oncology, and inherited genetic conditions, strengthening its use in clinical laboratories

- In October 2024, Roche announced advancements in its digital pathology and molecular diagnostics ecosystem through expansion of its navify and Cobas diagnostic platforms. These enhancements aimed to improve integration of laboratory data, AI-driven decision support, and workflow automation across clinical laboratories, reinforcing Roche’s position in digital and precision diagnostics transformation

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.