Global Preparative And Process Chromatography Market

Market Size in USD Billion

USD

11.27 Billion

USD

22.12 Billion

2025

2033

USD

11.27 Billion

USD

22.12 Billion

2025

2033

| 2026 - 2033 | |

| USD 11.27 Billion | |

| USD 22.12 Billion | |

| % | |

|

Preparative and Process Chromatography Market Overview

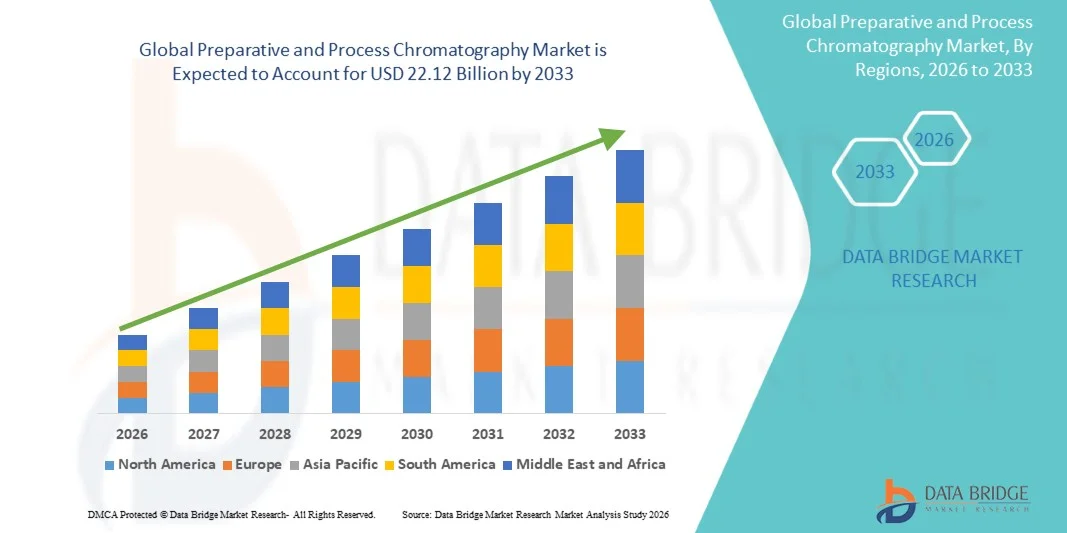

The Preparative and Process Chromatography Market was valued at USD 11.27 billion in 2025 and is projected to reach USD 22.12 billion by 2033, growing at a CAGR of 8.80% from 2026 to 2033. The market is witnessing steady growth driven by increasing demand for high-purity biopharmaceutical products, expanding applications in large-scale biologics manufacturing, and continuous advancements in chromatography resins, columns, and separation technologies.

The rising prevalence of chronic diseases, growing production of monoclonal antibodies, vaccines, and recombinant proteins, and stringent regulatory requirements for product purity are encouraging pharmaceutical and biotechnology companies to invest in advanced chromatography systems. Process-scale and preparative chromatography solutions are increasingly being adopted for downstream purification, active pharmaceutical ingredient (API) production, and industrial biotechnology applications, offering high separation efficiency, scalability, and cost-effective purification processes.

Key Market Trends & Insights

- North America dominated the Preparative and Process Chromatography Market with the largest revenue share of 38.12% in 2025, supported by a strong biopharmaceutical manufacturing base, extensive R&D activities, and the presence of leading chromatography technology providers.

- The Process Chromatography segment led the market with a 64.85% share in 2025, driven by its critical role in large-scale purification of biologics such as monoclonal antibodies, vaccines, and recombinant proteins.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.1% from 2026 to 2033, fueled by expanding biopharmaceutical production capacities, increasing contract manufacturing activities, and growing investments in biotechnology across China, India, South Korea, and Japan.

- Consumables are the fastest-growing product type, projected to register a CAGR of 8.4%, reflecting the surge in repeated usage of resins, buffers, and columns in ongoing bioprocessing operations.

- The Liquid Chromatography segment dominated the type category with a 52.36% revenue share in 2025, led by its extensive use in pharmaceutical and biopharmaceutical purification processes.

- Life Sciences accounted for 46.37% of the market, preferred by the extensive use in drug development, biologics purification, and biotechnology research.

- The Clinical Diagnostics segment is the fastest-growing application category, with a CAGR of 7.9%, driven by the increasing use of chromatography in disease detection and biomarker analysis.

Market Size & Forecast

- Global Market Value (2025): USD 11.27 Billion

- Expected Market Value (2033): USD 22.12 Billion

- Forecast CAGR (2026–2033): 8.80%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Preparative and Process Chromatography Market Segmentation

|

Attributes |

Preparative and Process Chromatography Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Merck KGaA (Germany) · Thermo Fisher Scientific Inc. (U.S.) · Cytiva (U.S.) · Sartorius AG (Germany) · Agilent Technologies, Inc. (U.S.) · Waters Corporation (U.S.) · Bio-Rad Laboratories, Inc. (U.S.) · Shimadzu Corporation (Japan) · Tosoh Corporation (Japan) · Repligen Corporation (U.S.) · Avantor, Inc. (U.S.) · Pall Corporation (U.S.) · Phenomenex Inc. (U.S.) · YMC Co., Ltd. (Japan) · Bio-Works Technologies AB (Sweden) · KNAUER Wissenschaftliche Geräte GmbH (Germany) · Sepax Technologies, Inc. (U.S.) · Novasep Holding S.A.S (France) · Daicel Corporation (Japan) · GE HealthCare (U.S.) |

|

Market Opportunities |

· Growing commercialization of cell and gene therapies · Increasing adoption of continuous bioprocessing · Expansion of biopharmaceutical manufacturing capacity in emerging markets |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Preparative and Process Chromatography Market Trends

Trend: Rising Adoption of Continuous Chromatography in Bioprocessing

Biopharmaceutical manufacturers are increasingly adopting continuous chromatography systems to improve productivity, reduce resin consumption, and enhance process efficiency in large-scale biologics manufacturing. The integration of automated process controls enables real-time monitoring and optimization of purification workflows. Contract development and manufacturing organizations are similarly leveraging continuous chromatography to support high-volume production through standardized, scalable purification platforms, while advanced resin technologies improve separation performance and closely support commercial bioprocessing requirements. For instance, in June 2024, Cytiva expanded its continuous bioprocessing capabilities through advanced chromatography solutions designed to enhance efficiency and scalability in biologics manufacturing.

Preparative and Process Chromatography Market Dynamics

Key Market Driver: Growing Demand for Biopharmaceutical Purification and Manufacturing

The rapid expansion of biopharmaceutical production and monoclonal antibody development has created substantial demand for preparative and process chromatography systems that can purify complex biomolecules, remove impurities, and ensure product quality at commercial scale. Pharmaceutical manufacturers, biotechnology companies, and contract manufacturing organizations are deploying chromatography platforms as a core component of downstream processing, reducing production risks, accelerating manufacturing timelines, and improving regulatory compliance. For instance, in February 2024, Merck KGaA introduced expanded downstream processing technologies to support increasing global demand for biologics purification and manufacturing.

Key Restraint/Challenge: High Cost of Chromatography Resins and Processing Systems

A significant restraint in the Preparative and Process Chromatography Market is the high upfront investment required for advanced purification systems. Modern platforms integrate high-performance columns, specialized chromatography resins, automated control software, and large-scale processing capabilities, demanding substantial expenditure in procurement, validation, and ongoing operation. The total cost of ownership extends to resin replacement, process optimization, and regulatory qualification, making adoption difficult for smaller biotechnology companies, academic laboratories, and emerging-market manufacturers.

For instance, in September 2024, industry discussions surrounding next-generation chromatography infrastructure highlighted the substantial capital requirements associated with large-scale purification facilities, reflecting the broader challenge of adoption beyond well-funded organizations.

Key Market Opportunity: Expansion of Cell and Gene Therapy Manufacturing Platforms

The expansion of cell and gene therapy manufacturing presents a significant market opportunity. Advanced chromatography platforms can support purification of viral vectors, plasmid DNA, and complex therapeutic biomolecules while maintaining stringent quality standards. The development of high-capacity resins and single-use chromatography systems is further improving manufacturing flexibility, opening growth opportunities across emerging biopharmaceutical markets in Asia-Pacific, Latin America, and the Middle East. For instance, in March 2024, Sartorius AG expanded its bioprocess solutions portfolio to support growing demand for advanced purification technologies in cell and gene therapy manufacturing.

Preparative and Process Chromatography Market Scope

The preparative and process chromatography market is segmented on the basis of product type, type, application, and end user.

- By Product Type

On the basis of product type, the Preparative and Process Chromatography Market is segmented into process chromatography, chromatography instruments, consumables, system, column, service, and others. The Process Chromatography segment dominated the market with a 64.85% share in 2025, owing to its critical role in large-scale purification of biologics such as monoclonal antibodies, vaccines, and recombinant proteins. It is extensively used in downstream bioprocessing due to its scalability and ability to ensure high-purity output in commercial manufacturing. Increasing biopharmaceutical production and rising demand for biosimilars are further strengthening its dominance. The segment benefits from strong integration with continuous manufacturing systems and automated purification workflows. Regulatory requirements for product purity and safety are also boosting adoption. Its established role in industrial-scale production makes it the backbone of chromatography applications globally.

The Consumables segment is expected to witness the fastest growth at a CAGR of 8.4% from 2026 to 2033, driven by repeated usage of resins, buffers, and columns in ongoing bioprocessing operations. Consumables are essential for every purification cycle, making them a recurring revenue stream for manufacturers. Rising biologics production volumes are significantly increasing demand for high-capacity and high-performance resins. Continuous innovation in resin chemistry and binding efficiency is improving separation outcomes. Expansion of contract manufacturing organizations is further accelerating consumption rates. Growing adoption of single-use and disposable chromatography components is also contributing to rapid growth.

- By Type

On the basis of type, the Preparative and Process Chromatography Market is segmented into liquid chromatography, gas chromatography, thin layer chromatography, paper chromatography, gel-permeation (molecular sieve) chromatography, and hydrophobic interaction chromatography. The Liquid Chromatography segment dominated the market with a 52.36% share in 2025, owing to its extensive use in pharmaceutical and biopharmaceutical purification processes. It is widely preferred for separating complex biomolecules due to its high resolution and scalability. Increasing production of monoclonal antibodies and protein-based therapeutics is strengthening its dominance. Advanced high-performance liquid chromatography systems are widely integrated into industrial downstream processes. Strong regulatory emphasis on purity and consistency is further supporting adoption. Its versatility across research and large-scale manufacturing makes it the most widely used technique globally.

The Hydrophobic Interaction Chromatography (HIC) segment is expected to witness the fastest growth at a CAGR of 8.1% from 2026 to 2033, driven by increasing use in protein purification and biopharmaceutical development. HIC is highly effective in separating biomolecules based on hydrophobic properties under mild conditions. It is particularly valuable in preserving protein structure and biological activity. Growing demand for monoclonal antibodies and biosimilars is significantly supporting adoption. Continuous improvements in resin selectivity and binding efficiency are enhancing performance. Expanding research in protein engineering and biologics development is further accelerating growth.

- By Application

On the basis of application, the Preparative and Process Chromatography Market is segmented into clinical diagnostics, environmental testing, forensic tests, life sciences, and others. The Life Sciences segment dominated the market with a 46.37% share in 2025, owing to extensive use in drug development, biologics purification, and biotechnology research. It plays a central role in downstream processing of vaccines, antibodies, and recombinant proteins. Increasing R&D investments in pharmaceutical and biotechnology sectors are strengthening dominance. Academic and industrial research institutions are widely adopting chromatography for molecular analysis and separation. Rising prevalence of chronic diseases is driving biologics demand, further supporting this segment. Its broad applicability across drug discovery and manufacturing ensures sustained leadership.

The Clinical Diagnostics segment is expected to witness the fastest growth at a CAGR of 7.9% from 2026 to 2033, driven by increasing use of chromatography in disease detection and biomarker analysis. It is widely applied in identifying metabolic disorders, drug residues, and protein abnormalities. Growing demand for precision medicine is further boosting adoption in diagnostic workflows. Advancements in analytical chromatography systems are improving sensitivity and accuracy. Expansion of healthcare infrastructure in emerging markets is supporting wider implementation. Increasing focus on early disease detection is accelerating clinical adoption globally.

- By End User

On the basis of end user, the Preparative and Process Chromatography Market is segmented into hospital and research laboratories, biotechnology and pharmaceutical industries, and others. The Biotechnology and Pharmaceutical Industries segment dominated the market with a 61.24% share in 2025, owing to large-scale adoption of chromatography systems in biologics manufacturing and drug development. These industries rely heavily on chromatography for purification, quality control, and regulatory compliance. Increasing production of monoclonal antibodies, vaccines, and biosimilars is driving demand. Strong investment in biomanufacturing infrastructure is further strengthening dominance. Integration of automated and continuous processing technologies is improving efficiency. Its critical role in ensuring product safety and efficacy makes it the primary end-user segment globally.

The Hospital and Research Laboratories segment is expected to witness the fastest growth at a CAGR of 7.6% from 2026 to 2033, driven by increasing clinical research activities and diagnostic applications. Hospitals are increasingly using chromatography for disease biomarker identification and therapeutic monitoring. Research laboratories are adopting advanced systems for drug discovery and molecular analysis. Growing funding for biomedical research is supporting expansion. Rising academic-industry collaborations are further accelerating adoption. Increasing focus on precision medicine and personalized treatment is also contributing to strong growth in this segment.

Preparative and Process Chromatography Market Regional Analysis

North America dominated the Preparative and Process Chromatography Market with the largest revenue share of 38.12% in 2025, supported by a strong biopharmaceutical manufacturing base, extensive R&D activities, and the presence of leading chromatography technology providers. The region also benefits from high R&D investments, rapid adoption of biologics and biosimilars, and strong regulatory frameworks ensuring product quality and safety. Increasing demand for monoclonal antibodies, vaccines, and cell and gene therapies continues to drive extensive use of chromatography systems across production and research environments. Growing integration of automated and continuous chromatography platforms further strengthens efficiency in large-scale purification processes. The presence of major industry players and contract manufacturing organizations reinforces North America’s leadership position in the global market.

U.S. Preparative and Process Chromatography Market Insight

The U.S. preparative and process chromatography market is witnessing strong growth due to rising biopharmaceutical production, advanced downstream processing infrastructure, and increasing investments in biologics and biosimilars manufacturing. The country’s well-established pharmaceutical ecosystem, along with strong presence of leading biotechnology firms and CDMOs, is driving demand for high-performance chromatography systems. In addition, growing focus on monoclonal antibodies, cell and gene therapies, and vaccine development is accelerating adoption across industrial and research applications. Increasing integration of automated, continuous, and high-throughput purification technologies is further enhancing process efficiency and scalability across manufacturing facilities.

Europe Preparative and Process Chromatography Market Insight

The Europe preparative and process chromatography market remains a major contributor to global revenue, driven by strong regulatory frameworks, advanced pharmaceutical manufacturing capabilities, and high demand for biologics purification solutions. The widespread use of chromatography systems in drug development, clinical research, and large-scale bioprocessing is supporting market expansion across the region. Increasing investments in sustainable biomanufacturing technologies and continuous processing platforms are further strengthening adoption. Moreover, strong presence of leading pharmaceutical companies and research institutions continues to enhance Europe’s position in the global chromatography landscape.

U.K. Preparative and Process Chromatography Market Insight

The U.K. preparative and process chromatography market is experiencing steady growth, supported by strong pharmaceutical research activity, expanding biologics development programs, and increasing adoption of advanced purification technologies. Rising investments in life sciences infrastructure and growing demand for high-quality therapeutic proteins are contributing to market expansion. Furthermore, integration of automated chromatography systems, digital process monitoring, and continuous manufacturing approaches is improving efficiency and scalability. The presence of leading academic research institutions and biotech startups is positioning the U.K. as an important innovation hub in chromatography applications.

Germany Preparative and Process Chromatography Market Insight

The Germany preparative and process chromatography market is expanding steadily due to the country’s strong chemical and pharmaceutical manufacturing base, advanced R&D capabilities, and increasing focus on biologics production. Pharmaceutical companies and biotechnology firms are widely adopting chromatography systems for purification, quality control, and regulatory compliance. Continuous advancements in high-capacity resins, process optimization technologies, and automated purification systems are further supporting market growth. Strong emphasis on industrial innovation and biomanufacturing efficiency continues to reinforce Germany’s position in the European chromatography market.

Asia-Pacific Preparative and Process Chromatography Market Insight

The Asia-Pacific preparative and process chromatography market is expected to witness rapid growth, driven by expanding biopharmaceutical manufacturing, increasing contract development and manufacturing activities, and rising investments in life sciences infrastructure across countries such as China, India, and Japan. Growing demand for biosimilars, vaccines, and recombinant proteins is significantly boosting adoption of advanced purification technologies. In addition, increasing government support for biotechnology development and rising focus on affordable biologics production are supporting regional market expansion. The growing presence of CDMOs and research institutions is further accelerating chromatography adoption across commercial and academic sectors.

Japan Preparative and Process Chromatography Market Insight

The Japan preparative and process chromatography market is witnessing consistent growth due to strong pharmaceutical innovation, increasing biologics production, and advanced research in protein purification technologies. Leading pharmaceutical companies and research institutes are increasingly adopting high-precision chromatography systems for drug development and downstream processing. Moreover, continuous advancements in resin technology, automation, and process optimization are improving purification efficiency and scalability. Japan’s strong focus on regenerative medicine, biopharmaceutical innovation, and quality-driven manufacturing is further contributing to market expansion.

China Preparative and Process Chromatography Market Insight

The China preparative and process chromatography market is growing rapidly, driven by expanding biopharmaceutical production, rising government support for biotechnology development, and increasing investments in pharmaceutical manufacturing infrastructure. Growing adoption of monoclonal antibodies, biosimilars, and vaccine production is significantly boosting demand for advanced chromatography systems. In addition, increasing presence of domestic CDMOs and rapid expansion of life sciences R&D capabilities are strengthening market growth. Continuous technological advancements and cost-effective manufacturing initiatives are positioning China as one of the fastest-growing chromatography markets globally.

Preparative and Process Chromatography Market Share

The preparative and process chromatography industry is primarily led by well-established companies, including:

- Merck KGaA (Germany)

- Thermo Fisher Scientific Inc. (U.S.)

- Cytiva (U.S.)

- Sartorius AG (Germany)

- Agilent Technologies, Inc. (U.S.)

- Waters Corporation (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Shimadzu Corporation (Japan)

- Tosoh Corporation (Japan)

- Repligen Corporation (U.S.)

- Avantor, Inc. (U.S.)

- Pall Corporation (U.S.)

- Phenomenex Inc. (U.S.)

- YMC Co., Ltd. (Japan)

- Bio-Works Technologies AB (Sweden)

- KNAUER Wissenschaftliche Geräte GmbH (Germany)

- Sepax Technologies, Inc. (U.S.)

- Novasep Holding S.A.S (France)

- Daicel Corporation (Japan)

- GE HealthCare (U.S.)

Latest Developments in Preparative and Process Chromatography Market

- In April 2024, Thermo Fisher Scientific expanded its bioprocessing and chromatography consumables manufacturing capabilities to support growing global demand for biologics production and purification solutions. This expansion aimed to improve supply reliability for chromatography resins, columns, and single-use technologies used in downstream processing. The development reflects rising demand for large-scale biologics manufacturing infrastructure worldwide. It also highlights the industry’s increasing focus on strengthening production capacity for critical purification components

- In March 2023, Cytiva introduced enhancements to its ÄKTA process chromatography platform, aimed at improving automation, scalability, and digital integration in biopharmaceutical purification workflows. The development focused on strengthening continuous and connected bioprocessing capabilities for large-scale biologics production. It supports increasing industry demand for high-throughput and digitally enabled purification systems. This advancement reflects the broader shift toward automated and data-driven chromatography platforms in modern biomanufacturing

- In June 2022, Sartorius expanded its chromatography resin and bioprocessing production capabilities in Europe to support rising global demand for biologics manufacturing solutions. The development focused on strengthening supply chain resilience and increasing availability of high-performance purification consumables used in downstream processing. This expansion highlights growing investment in chromatography infrastructure to support monoclonal antibody and vaccine production. It also reflects increasing demand for scalable and efficient purification technologies in the biopharmaceutical industry

- In May 2021, Repligen Corporation announced the acquisition of Avitide, a biotechnology company specializing in affinity chromatography ligand development for biologics purification. This acquisition strengthened Repligen’s position in high-value chromatography consumables by enhancing its capabilities in next-generation affinity separation technologies. The development supports increasing demand for high-selectivity purification solutions in monoclonal antibody and recombinant protein manufacturing. It also reflects the broader industry shift toward advanced, highly specific purification platforms for complex biologics

- In February 2021, Ecolab completed the acquisition of Purolite, a leading provider of ion exchange resins used in chromatography and bioprocessing applications. The acquisition strengthened Ecolab’s presence in life sciences purification technologies by expanding its portfolio of high-performance separation and purification materials used in biopharmaceutical manufacturing. This development reflects the increasing importance of resin-based technologies in large-scale biologics production and downstream processing. The integration of Purolite’s capabilities is expected to enhance innovation in chromatography consumables and support growing global demand for biologics purification

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.