Global Presbyopia Market

Market Size in USD Billion

USD

11.43 Billion

USD

16.75 Billion

2025

2033

USD

11.43 Billion

USD

16.75 Billion

2025

2033

| 2026 - 2033 | |

| USD 11.43 Billion | |

| USD 16.75 Billion | |

| % | |

|

Presbyopia Market Size

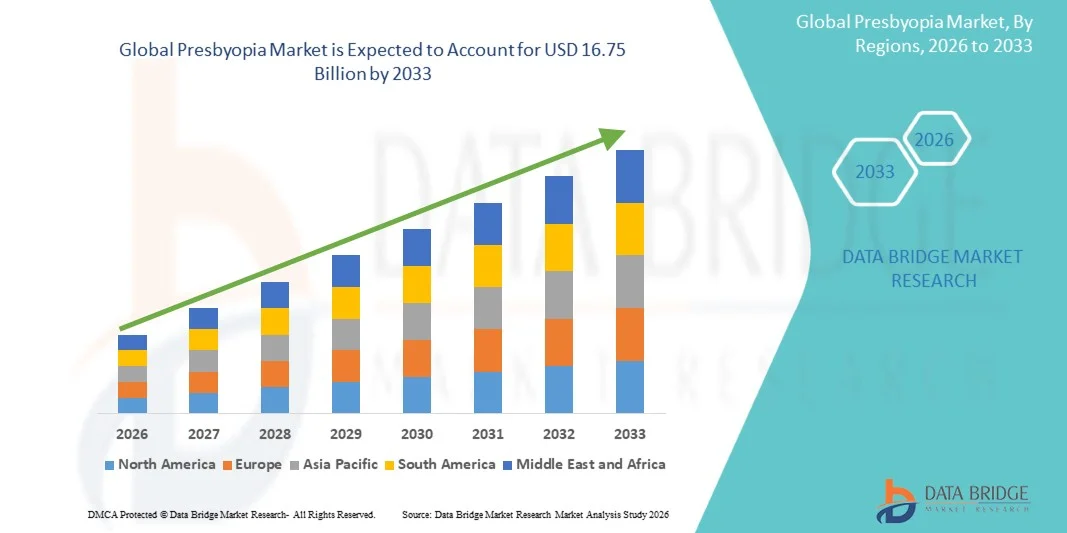

- As per Data Bridge Market Research Analysis the global presbyopia market size was valued at USD 11.43 billion in 2025 and is expected to reach USD 16.75 billion by 2033, at a CAGR of 4.90% during the forecast period

- The market growth is primarily driven by the rising prevalence of age-related vision disorders and the increasing global geriatric population, leading to higher demand for effective vision correction and treatment solutions across both developed and emerging economies

- Furthermore, continuous advancements in ophthalmic therapies, contact lenses, intraocular lenses, and minimally invasive corrective procedures are encouraging wider adoption of presbyopia management solutions. Growing consumer awareness regarding eye health and preference for convenient, long-term vision correction options are further accelerating the expansion of the global presbyopia market

Market Size & Forecast

- Global Market Value (2025): USD 11.43 billion

- Expected Market Value (2033): USD 16.75 billion

- Forecast CAGR (2026–2033): 4.90%

Presbyopia Market Analysis

- Presbyopia, an age-related vision condition that gradually reduces the eye’s ability to focus on nearby objects, is becoming an increasingly significant concern within global eye care and ophthalmology sectors due to the growing aging population and rising demand for effective vision correction solutions

- The increasing demand for presbyopia treatment solutions is primarily driven by the expanding geriatric population, greater awareness regarding eye health, and rising adoption of advanced corrective options such as eyeglasses, contact lenses, and refractive surgical procedures

- North America dominated the presbyopia market with the largest revenue share of 39.8% in 2025, supported by advanced healthcare infrastructure, high adoption of innovative ophthalmic treatments, and strong presence of leading eye care companies, with the U.S. witnessing substantial growth in presbyopia diagnosis and corrective treatment adoption driven by increasing screen exposure and aging demographics

- Asia-Pacific is expected to be the fastest growing region in the presbyopia market during the forecast period due to improving healthcare access, rapidly aging populations, and increasing awareness regarding vision correction treatments

- Eyeglasses segment dominated the presbyopia market with a market share of 46.3% in 2025, driven by their affordability, widespread accessibility, and strong consumer preference for non-invasive and convenient vision correction solutions

Report Scope and Presbyopia Market Segmentation

|

Attributes |

Presbyopia Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· The growing development and commercialization of presbyopia-correcting eye drops · Rising adoption of premium multifocal intraocular lenses and laser-based corrective surgeries |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Presbyopia Market Trends

“Advancements in Non-Invasive Vision Correction Therapies”

- A significant and accelerating trend in the global presbyopia market is the growing development and adoption of non-invasive treatment solutions such as presbyopia-correcting eye drops, advanced multifocal lenses, and digitally enhanced diagnostic technologies. This convergence of innovations is significantly improving patient convenience and treatment accessibility

- For instance, AbbVie’s VUITY eye drops gained substantial market attention as the first FDA-approved prescription eye drop for presbyopia, offering temporary near-vision improvement without the need for glasses. Similarly, Alcon continues expanding its portfolio of multifocal contact lenses designed for enhanced visual performance across varying distances

- Technological advancements in presbyopia management are enabling more personalized treatment approaches through improved lens materials, precision diagnostics, and optimized refractive correction procedures. For instance, several ophthalmology companies are investing in AI-assisted eye examination tools to improve diagnostic accuracy and support customized treatment planning. Furthermore, minimally invasive correction options are providing patients with greater flexibility and reduced dependency on traditional reading glasses

- The seamless integration of advanced ophthalmic technologies with digital healthcare platforms is facilitating improved patient monitoring and streamlined treatment management. Through connected diagnostic systems and teleophthalmology platforms, healthcare providers can efficiently evaluate vision conditions and recommend personalized corrective solutions, creating a more integrated patient care experience

- This trend toward more advanced, patient-friendly, and technology-driven presbyopia treatments is fundamentally reshaping expectations for age-related vision correction. Consequently, companies such as Johnson & Johnson Vision are developing innovative multifocal and extended-depth-of-focus lens technologies aimed at improving visual outcomes and patient comfort

- The demand for presbyopia solutions that offer improved convenience, reduced dependence on eyewear, and enhanced visual quality is growing rapidly across both developed and emerging markets, as consumers increasingly prioritize long-term eye health and lifestyle flexibility

Presbyopia Market Dynamics

Driver

“Growing Need Due to Rising Aging Population and Increasing Vision Care Awareness”

- The increasing prevalence of age-related vision disorders among the global aging population, coupled with growing awareness regarding preventive eye care, is a significant driver for the heightened demand for presbyopia treatment solutions

- For instance, in October 2023, Alcon announced continued expansion of its presbyopia-correcting intraocular lens portfolio to address rising global demand for advanced vision correction procedures. Such strategies by key companies are expected to drive the presbyopia market growth in the forecast period

- As consumers become more conscious of maintaining visual health and quality of life, presbyopia treatment solutions offer advanced corrective options such as multifocal lenses, refractive surgery, and prescription eye drops, providing significant improvements over conventional reading glasses alone

- Furthermore, the growing accessibility of ophthalmic care services and the increasing popularity of minimally invasive corrective procedures are making presbyopia treatments an integral component of modern vision care systems, offering enhanced convenience and personalized treatment outcomes

- In addition, the rising adoption of digital eye strain management solutions and growing demand for customized vision correction products among working-age adults are creating new growth opportunities for manufacturers and eye care providers operating in the global presbyopia market

- The convenience of advanced corrective options, improved accessibility to eye examinations, and the ability to manage age-related vision impairment through customized therapies are key factors propelling the adoption of presbyopia treatments in both developed and emerging healthcare markets. The trend toward early diagnosis and growing consumer willingness to invest in premium vision correction solutions further contribute to market growth

Restraint/Challenge

“High Treatment Costs and Limited Accessibility in Developing Regions”

- Concerns surrounding the high costs associated with advanced presbyopia treatments, including premium intraocular lenses and refractive surgeries, pose a significant challenge to broader market penetration. As many innovative corrective procedures require specialized equipment and skilled professionals, affordability concerns remain substantial among large patient populations

- For instance, limited insurance coverage for elective vision correction procedures in several countries has made some consumers hesitant to adopt advanced presbyopia treatment options despite their long-term benefits

- Addressing these affordability concerns through improved healthcare reimbursement policies, wider availability of cost-effective treatment alternatives, and expanded ophthalmic infrastructure is crucial for improving patient access. Companies such as Bausch + Lomb and Carl Zeiss Meditec continue emphasizing innovation in accessible corrective technologies to support broader adoption. In addition, the limited availability of specialized ophthalmic care in rural and underdeveloped regions can restrict access to timely diagnosis and treatment, particularly among aging populations with lower healthcare awareness

- While technological advancements are improving treatment outcomes, the relatively high cost of premium corrective procedures and insufficient access to specialized eye care services can still hinder widespread adoption, especially in low- and middle-income economies where affordability remains a major concern

- Overcoming these challenges through expanded healthcare access, increased awareness regarding presbyopia management, and the development of more affordable corrective solutions will be vital for sustained market growth

Presbyopia Market Scope

The market is segmented on the basis of diagnosis, treatment, symptoms, end-users, and distribution channel.

- By Diagnosis

On the basis of diagnosis, the presbyopia market is segmented into eye exam and others. The eye exam segment dominated the market with the largest market revenue share in 2025, driven by the increasing prevalence of age-related vision disorders and the growing emphasis on routine ophthalmic screening. Eye examinations remain the primary and most reliable method for diagnosing presbyopia, enabling early detection and personalized corrective recommendations for patients. The widespread availability of optometry clinics, ophthalmology centers, and advanced diagnostic technologies further supports the dominance of this segment. In addition, rising awareness regarding preventive eye care and increasing healthcare spending are encouraging individuals to undergo regular vision assessments. Healthcare providers also rely heavily on comprehensive eye exams to evaluate associated refractive conditions and determine appropriate treatment pathways. The growing aging population across both developed and emerging economies continues to strengthen demand for diagnostic eye examination services globally.

The others segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing adoption of digital and AI-assisted diagnostic technologies in ophthalmology practices. Emerging diagnostic methods such as teleophthalmology consultations, smartphone-based vision assessment tools, and automated refractive testing systems are gaining traction due to their convenience and accessibility. These technologies support faster diagnosis, improved patient engagement, and expanded reach in underserved regions with limited access to eye care specialists. Increasing investments in digital healthcare infrastructure and remote patient monitoring solutions are further accelerating segment growth. In addition, growing consumer preference for accessible and time-efficient diagnostic options is contributing to higher adoption of alternative presbyopia screening methods. Continuous advancements in smart diagnostic platforms are expected to create significant opportunities for innovation within this segment.

- By Treatment

On the basis of treatment, the presbyopia market is segmented into eyeglasses, contact lenses, refractive surgery, lens implants, and others. The eyeglasses segment dominated the market with the largest market revenue share of 46.3% in 2025, driven by their affordability, convenience, and widespread availability across global markets. Eyeglasses remain the most commonly prescribed and non-invasive solution for managing presbyopia, particularly among aging populations seeking cost-effective vision correction. The availability of customized lenses, including bifocal and progressive lenses, further enhances consumer preference for this treatment option. In addition, growing awareness regarding vision care and increasing accessibility through retail optical stores and online platforms continue to support segment growth. Patients often prefer eyeglasses due to their ease of use, minimal risk profile, and suitability for long-term daily wear. The rising global geriatric population and increasing incidence of age-related visual impairment continue to drive sustained demand for prescription eyewear solutions.

The refractive surgery segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing demand for permanent and minimally invasive vision correction procedures. Technological advancements in laser-assisted surgeries and corneal reshaping techniques are significantly improving treatment precision, safety, and patient outcomes. Consumers seeking reduced dependence on glasses and contact lenses are increasingly opting for advanced refractive surgical solutions. In addition, growing healthcare expenditure and rising awareness regarding modern ophthalmic procedures are accelerating adoption across developed and emerging markets. The expansion of specialized eye care centers and availability of experienced ophthalmic surgeons further contribute to segment growth. Continuous innovation in laser technologies and personalized surgical planning is expected to enhance the long-term growth potential of the refractive surgery segment.

- By Symptoms

On the basis of symptoms, the presbyopia market is segmented into eye strain, headaches, fatigue, blurred vision, and others. The blurred vision segment dominated the market with the largest market revenue share in 2025, driven by its status as the most common and recognizable symptom associated with presbyopia. Patients experiencing difficulty focusing on nearby objects frequently seek medical attention and corrective treatment due to the impact of blurred vision on daily activities such as reading and digital device usage. Increasing screen exposure among adults and aging populations has further contributed to the prevalence of this symptom globally. Healthcare professionals prioritize blurred vision during diagnostic evaluations as it strongly indicates progressive age-related focusing difficulties. In addition, growing awareness regarding vision health and accessibility to ophthalmic care services are supporting increased diagnosis rates linked to blurred vision complaints. The widespread occurrence and direct impact on quality of life continue to strengthen the dominance of this segment within the market.

The eye strain segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing digital device usage and prolonged screen exposure across working-age populations. Rising cases of digital eye fatigue and visual discomfort are encouraging individuals to seek early ophthalmic consultations and preventive vision care solutions. Consumers are becoming more aware of the relationship between eye strain and underlying presbyopia progression, particularly among middle-aged adults. In addition, the expansion of remote working environments and growing dependence on smartphones, tablets, and computers are contributing to higher incidence of eye strain symptoms globally. Healthcare providers are increasingly recommending vision correction solutions and ergonomic practices to manage eye strain-related complications. The growing emphasis on workplace eye health and preventive ophthalmology is expected to further accelerate growth within this segment.

- By End-Users

On the basis of end-users, the presbyopia market is segmented into hospitals, specialty clinics, homecare, and others. The hospitals segment dominated the market with the largest market revenue share in 2025, driven by the availability of advanced ophthalmic infrastructure, specialized healthcare professionals, and comprehensive diagnostic capabilities. Hospitals remain primary centers for presbyopia diagnosis, corrective procedures, and surgical interventions due to their ability to provide integrated patient care services. Increasing patient preference for hospital-based eye care treatments and rising healthcare expenditure further support the segment’s dominance. In addition, hospitals frequently adopt advanced ophthalmic technologies and minimally invasive surgical equipment, enhancing treatment efficiency and patient outcomes. The growing burden of age-related eye disorders and expanding hospital ophthalmology departments continue to strengthen demand for hospital-based presbyopia management services. Government investments in healthcare infrastructure and ophthalmic service expansion also contribute significantly to segment growth.

The homecare segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing consumer preference for convenient and self-managed vision care solutions. The growing availability of online eye consultation services, home-based vision monitoring tools, and direct-to-consumer eyewear products is accelerating adoption of homecare-based presbyopia management. Patients are increasingly seeking accessible and cost-effective alternatives that minimize frequent hospital visits while supporting long-term vision correction needs. In addition, technological advancements in telemedicine and remote ophthalmic assessment platforms are improving the feasibility of home-based eye care services. The aging global population and rising awareness regarding preventive vision management are further contributing to segment growth. Expanding digital healthcare ecosystems and increasing consumer comfort with virtual healthcare solutions are expected to support continued expansion of the homecare segment.

- By Distribution Channel

On the basis of distribution channel, the presbyopia market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others. The retail pharmacy segment dominated the market with the largest market revenue share in 2025, driven by strong consumer accessibility and widespread availability of vision care products through established pharmacy networks. Retail pharmacies serve as convenient distribution points for prescription eyeglasses, contact lenses, eye drops, and other presbyopia management products. Increasing consumer preference for immediate product availability and personalized in-store assistance further supports the dominance of this segment. In addition, collaborations between ophthalmic companies and retail pharmacy chains are improving product reach and strengthening market penetration globally. Retail pharmacies also benefit from strong consumer trust and accessibility across both urban and semi-urban regions. The rising aging population and growing demand for over-the-counter vision care products continue to drive consistent growth within the segment.

The online pharmacy segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rapid digitalization and increasing consumer preference for e-commerce-based healthcare purchasing. Online pharmacies offer enhanced convenience, broader product selection, competitive pricing, and doorstep delivery services, making them increasingly attractive for presbyopia patients seeking long-term vision care products. The expansion of telemedicine services and online prescription management platforms is further supporting the adoption of digital distribution channels. In addition, growing internet penetration and smartphone usage across emerging economies are accelerating online pharmacy accessibility. Consumers are increasingly utilizing digital platforms for purchasing contact lenses, prescription eyewear, and ophthalmic medications due to improved convenience and affordability. Continuous advancements in digital healthcare infrastructure and secure online payment systems are expected to further strengthen the long-term growth of the online pharmacy segment.

Presbyopia Market Regional Analysis

- North America dominated the presbyopia market with the largest revenue share of 39.8% in 2025, supported by advanced healthcare infrastructure, high adoption of innovative ophthalmic treatments, and strong presence of leading eye care companies

- Patients in the region highly value the accessibility, treatment effectiveness, and technological advancements offered by modern presbyopia correction options such as multifocal lenses, prescription eye drops, and refractive surgical procedures

- This widespread adoption is further supported by advanced healthcare infrastructure, high healthcare spending, a rapidly aging population, and the growing preference for minimally invasive vision correction solutions, establishing presbyopia treatments as an essential component of modern eye care management across both clinical and outpatient settings

U.S. Presbyopia Market Insight

The U.S. presbyopia market captured the largest revenue share within North America in 2025, fueled by the rising aging population and increasing demand for advanced vision correction solutions. Patients are increasingly prioritizing effective and convenient treatment options for age-related near vision impairment through prescription eyewear, contact lenses, and minimally invasive corrective procedures. The growing preference for technologically advanced ophthalmic treatments, combined with strong demand for premium multifocal lenses and prescription eye drops, further propels the presbyopia industry. Moreover, the increasing availability of advanced diagnostic technologies and expanding awareness regarding preventive eye care are significantly contributing to the market's expansion.

Europe Presbyopia Market Insight

The Europe presbyopia market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the growing geriatric population and increasing awareness regarding age-related vision disorders. The increase in healthcare expenditure, coupled with rising demand for advanced ophthalmic treatments, is fostering the adoption of presbyopia management solutions. European consumers are also drawn to the convenience and effectiveness offered by multifocal lenses, refractive surgeries, and innovative corrective therapies. The region is experiencing significant growth across hospitals, specialty clinics, and optical care centers, with advanced presbyopia treatments being increasingly incorporated into routine ophthalmic care services.

U.K. Presbyopia Market Insight

The U.K. presbyopia market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the escalating prevalence of vision impairment among aging populations and a growing desire for convenient corrective solutions. In addition, increasing awareness regarding eye health and preventive ophthalmic care is encouraging patients to seek early diagnosis and treatment for presbyopia. The U.K.’s strong healthcare infrastructure, alongside rising adoption of advanced vision correction technologies, is expected to continue to stimulate market growth.

Germany Presbyopia Market Insight

The Germany presbyopia market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness regarding advanced eye care treatments and the demand for technologically sophisticated ophthalmic solutions. Germany’s well-developed healthcare infrastructure, combined with its emphasis on medical innovation and precision healthcare, promotes the adoption of presbyopia treatments, particularly in hospitals and specialty eye clinics. The integration of advanced diagnostic systems and minimally invasive corrective procedures is also becoming increasingly prevalent, with a strong preference for high-quality and personalized vision correction solutions aligning with local patient expectations.

Asia-Pacific Presbyopia Market Insight

The Asia-Pacific presbyopia market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by increasing aging populations, improving healthcare access, and rising awareness regarding vision correction treatments in countries such as China, Japan, and India. The region's growing inclination toward preventive healthcare, supported by expanding ophthalmic infrastructure and digital healthcare initiatives, is driving the adoption of presbyopia treatment solutions. Furthermore, as APAC emerges as a significant market for affordable ophthalmic products and corrective technologies, the accessibility and availability of presbyopia treatments are expanding to a wider patient population.

Japan Presbyopia Market Insight

The Japan presbyopia market is gaining momentum due to the country’s rapidly aging population, advanced healthcare infrastructure, and strong demand for innovative vision correction solutions. The Japanese market places a significant emphasis on preventive healthcare and quality of life, and the adoption of presbyopia treatments is driven by the increasing number of elderly individuals requiring long-term vision management. The integration of advanced ophthalmic technologies with digital diagnostic systems and minimally invasive treatment options is fueling growth. Moreover, Japan's strong focus on healthcare innovation is likely to spur demand for efficient, patient-friendly presbyopia management solutions across both residential and clinical care settings.

India Presbyopia Market Insight

The India presbyopia market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country's expanding aging population, increasing healthcare awareness, and rising accessibility to ophthalmic care services. India stands as one of the fastest-growing markets for vision correction products and treatments, and presbyopia management solutions are becoming increasingly popular across hospitals, specialty clinics, and optical retail networks. The push toward improved healthcare infrastructure and expanding availability of affordable eyeglasses, contact lenses, and diagnostic services, alongside growing domestic ophthalmic manufacturers, are key factors propelling the market in India.

Presbyopia Market Share

The Presbyopia industry is primarily led by well-established companies, including:

- AbbVie Inc. (U.S.)

- Alcon Vision LLC (Switzerland)

- Bausch + Lomb Incorporated (U.S.)

- Novartis AG (Switzerland)

- Essilor International SAS (France)

- Carl Zeiss Meditec AG (Germany)

- CooperVision, Inc. (U.S.)

- Santen Pharmaceutical Co., Ltd. (Japan)

- Glaukos Corporation (U.S.)

- STAAR Surgical Company (U.S.)

- LENZ Therapeutics, Inc. (U.S.)

- Orasis Pharmaceuticals Inc. (U.S.)

- Visus Therapeutics, Inc. (U.S.)

- Eyenovia, Inc. (U.S.)

- Oculis Holding AG (Switzerland)

- Atia Vision Inc. (U.S.)

- Ziemer Ophthalmic Systems AG (Switzerland)

- Hoya Corporation (Japan)

- Menicon Co., Ltd. (Japan)

What are the Recent Developments in Global Presbyopia Market?

- In July 2025, LENZ Therapeutics received FDA approval for VIZZ (aceclidine ophthalmic solution 1.44%), a once-daily presbyopia eye drop designed to improve near vision for up to 10 hours. Clinical trials showed rapid onset of action and strong improvement in reading ability without affecting distance vision. This approval marked a second major breakthrough in pharmacological presbyopia treatment after VUITY. It significantly expanded non-surgical treatment options and strengthened the growing eye-drop-based presbyopia market segment

- In April 2024, LENZ Therapeutics announced positive Phase 3 clinical trial results for its presbyopia treatment candidate LNZ100, showing statistically significant improvement in near vision for patients aged 45–75 years. The study demonstrated that a high proportion of patients achieved functional near vision improvement without impacting distance clarity. These results supported regulatory submission plans for commercialization in the U.S. market. This development strengthened competition in the prescription eye-drop segment for presbyopia

- In April 2023, Orasis Pharmaceuticals advanced its investigational presbyopia eye drop CSF-1 into late-stage clinical development, demonstrating improved near vision without compromising distance vision in Phase 3 trials. The therapy uses a low-dose pilocarpine formulation designed to minimize side effects while improving visual acuity. The results supported its potential as a next-generation alternative to existing presbyopia treatments. This development highlighted strong pipeline innovation in non-surgical vision correction solutions

- In November 2021, Allergan (now part of AbbVie) initiated commercial rollout activities for VUITY across the U.S. market following its regulatory approval. The launch focused on making the first presbyopia-correcting eye drop widely available through ophthalmologists and retail pharmacies. Physicians began adopting the therapy as an alternative to reading glasses for eligible patients aged 40 and above. This commercialization marked the beginning of a new prescription-based approach to presbyopia treatment

- In October 2021, AbbVie announced FDA approval of VUITY (pilocarpine hydrochloride ophthalmic solution 1.25%), marking the first prescription eye drop approved for the treatment of presbyopia. The once-daily eye drop helps improve near vision by reducing pupil size, creating a pinhole effect that enhances focus. This approval represented a major shift in presbyopia management from traditional corrective lenses toward pharmacological treatment options. It opened a new non-invasive treatment category in ophthalmology, significantly expanding patient choices for age-related near vision loss

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.