Global Prescription Lens Market

Market Size in USD Billion

USD

44.79 Billion

USD

64.18 Billion

2025

2033

USD

44.79 Billion

USD

64.18 Billion

2025

2033

| 2026 - 2033 | |

| USD 44.79 Billion | |

| USD 64.18 Billion | |

| % | |

|

Prescription Lens Market Overview

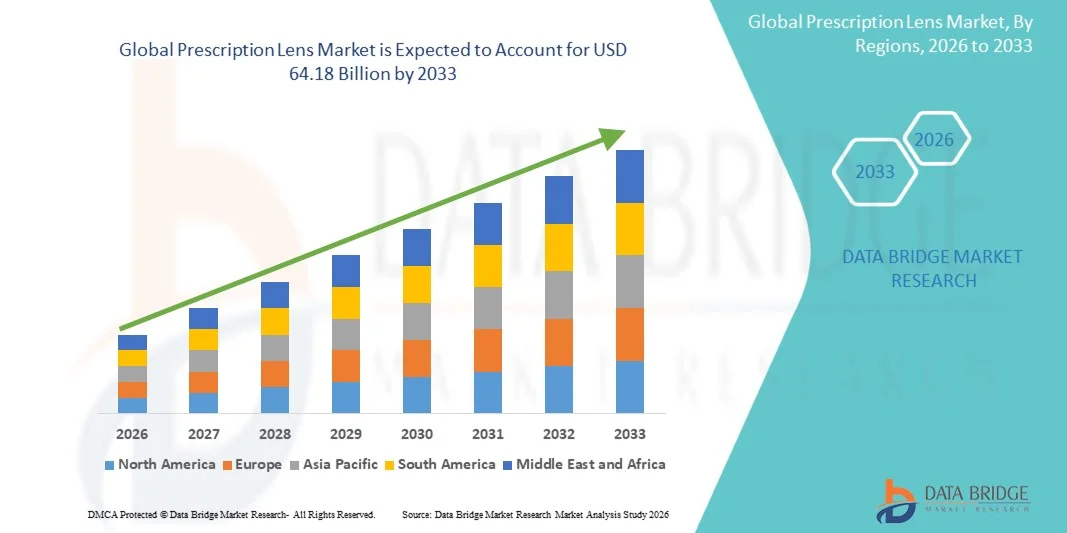

The Prescription Lens Market was valued at USD 44.79 billion in 2025 and is projected to reach USD 64.18 billion by 2033, growing at a CAGR of 4.60% from 2026 to 2033. The Prescription Lens market is experiencing steady growth driven by rising prevalence of refractive errors such as myopia, hyperopia, and astigmatism, increasing screen time across all age groups, and growing awareness of vision correction and eye health. Expanding adoption of advanced optical technologies, including digital free-form lenses, blue-light filtering coatings, and photochromic lenses, is further enhancing product demand across both developed and emerging markets.

The increasing incidence of vision impairment globally, combined with changing lifestyle patterns, prolonged digital device usage, and aging populations in several regions, is driving higher prescription lens adoption. Optometrists, ophthalmology clinics, and optical retail chains are witnessing growing patient inflows for vision correction solutions. In addition, advancements in lens materials and manufacturing technologies are enabling thinner, lighter, and more durable lenses, improving user comfort and visual clarity. The expansion of organized optical retail networks and e-commerce distribution channels is further accelerating market penetration, particularly in urban and semi-urban areas.

Key Market Trends & Insights

- North America dominated the Prescription Lens Market with the largest revenue share of 33.84% in 2025, supported by strong optical healthcare infrastructure, high awareness of vision correction solutions, widespread availability of optometry services, and presence of leading ophthalmic lens manufacturers across the region. The region also benefits from advanced lens manufacturing technologies, high adoption of premium progressive and digital free-form lenses, and strong reimbursement frameworks in several countries, which collectively strengthen Europe’s leading position in the global market.

- The Myopia segment dominated the global market with a share of 42.6% in 2025, primarily due to the rapidly increasing prevalence of nearsightedness worldwide, especially among children and young adults

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.2% from 2026 to 2033, fueled by rising prevalence of vision disorders such as myopia, increasing screen time exposure, rapid urbanization, expanding middle-class population, and improving access to eye care services across countries such as China, India, and Japan. Growing penetration of organized optical retail chains and e-commerce platforms is further accelerating regional market growth.

- The Progressive Lenses segment is expected to register the fastest CAGR of 7.0% from 2026 to 2033, driven by increasing cases of presbyopia among aging populations and rising demand for premium, multi-focus vision correction solutions. Advancements in digital free-form lens technology and personalized lens customization are further enhancing adoption among working professionals and elderly consumers.

- The Myopia segment dominated the application category with a substantial revenue share in 2025, supported by the rapidly increasing prevalence of near-sightedness globally, especially among children and young adults due to prolonged digital device usage and reduced outdoor activities. Rising awareness of early vision correction and regular eye screening programs is further strengthening this segment’s dominance.

- The Anti-reflective Coating segment held the largest share in 2025, driven by growing demand for improved visual clarity, reduced glare from digital screens, and enhanced comfort during prolonged device usage. Increasing adoption of premium lens coatings in urban populations and among professionals working in screen-intensive environments continues to support segment growth.

Market Size & Forecast

- Global Market Value (2025): USD 44.79 Billion

- Expected Market Value (2033): USD 64.18 Billion

- Forecast CAGR (2026–2033): 4.60%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Prescription Lens Market Segmentation

|

Attributes |

Prescription Lens Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Johnson & Johnson Vision Care Inc. (U.S.) |

|

Market Opportunities |

· Rising Demand for Premium and Customized Vision Solutions · Growth of E-commerce and Omnichannel Eyewear Retail · Technological Advancements in Lens Materials and Coatings |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Prescription Lens Market Trends

Trend: Rising Adoption of Advanced Digital Lens Technologies & Personalized Vision Correction

The Prescription Lens Market is witnessing strong growth driven by increasing demand for digitally enhanced, customized, and lifestyle-oriented eyewear solutions. Consumers are rapidly shifting toward blue-light filtering, anti-fatigue, photochromic, and digitally surfaced free-form lenses, especially due to increased screen exposure. For instance, studies indicate that over 60% of global digital device users experience digital eye strain, accelerating demand for blue-light protection lenses.

Leading manufacturers such as EssilorLuxottica and Carl Zeiss Vision are increasingly adopting digital surfacing technology and AI-based lens design optimization, enabling high-precision personalization of lenses based on lifestyle, occupation, and visual behavior. In addition, smart eyewear integration and AR-enabled vision correction are emerging as long-term innovation trends in the industry.

Prescription Lens Market Dynamics

Key Market Driver: Rising Prevalence of Vision Disorders & Expanding Eye Care Access

The global increase in refractive errors such as myopia, hyperopia, astigmatism, and presbyopia is significantly driving prescription lens demand. According to the World Health Organization (WHO), more than 2.2 billion people globally suffer from vision impairment or blindness, with at least 1 billion cases being preventable or unaddressed refractive errors. Rapid urbanization, increased screen time, and aging populations—especially in Asia-Pacific—are accelerating myopia prevalence. For example, East Asia reports myopia rates exceeding 80–90% among high school students, creating sustained demand for corrective lenses. Expanding eye-care infrastructure, optical retail chains, and online prescription platforms are further supporting global market expansion.

Key Restraint/Challenge: High Cost of Advanced Lens Technologies and Limited Access in Low-Income Regions

Despite strong demand, the market faces constraints due to the high cost of premium prescription lenses, including progressive, digital free-form, and customized coatings. Advanced lenses can cost 2–5 times more than standard single-vision lenses, limiting adoption in price-sensitive markets. In addition, access to professional eye examinations and optical retail infrastructure remains limited in rural and low-income regions. According to global eye care access reports, over 90% of untreated vision impairment cases occur in developing economies, highlighting affordability and accessibility gaps. This restricts penetration of high-end lens technologies despite strong clinical need.

Key Market Opportunity: Expansion of Digital Eye Care, E-commerce Eyewear & AI-Based Prescription Platforms

The integration of digital healthcare and e-commerce is creating significant growth opportunities in the prescription lens market. Online eyewear platforms such as Warby Parker, Lenskart, and Zenni Optical have demonstrated strong growth by offering virtual try-on, home eye testing kits, and AI-assisted prescription verification systems. For instance, Lenskart reportedly serves over 40 million customers globally and operates across 2,000+ offline stores combined with a strong online platform, highlighting the rapid hybrid retail expansion model in eyewear.

In addition, AI-driven eye screening tools and smartphone-based vision tests are improving early diagnosis and enabling remote prescription generation. Emerging technologies such as machine-learning-based lens recommendation systems and cloud-based optical prescription management platforms are expected to further democratize access to vision correction, especially across Asia-Pacific, Latin America, and Africa.

Prescription Lens Market Scope

The Prescription Lens Market is segmented on the basis of type, application, and lens coating

- By Type

On the basis of type, the Prescription Lens Market is segmented into Single Vision, Bifocal, Trifocal, Progressive, Workspace Progressive, and Others. The Single Vision segment dominated the market with the largest share of 38.9% in 2025, owing to its widespread usage for basic refractive error correction such as myopia and hyperopia. These lenses are highly affordable, easily accessible, and widely prescribed across all age groups, making them the most commonly used vision correction solution globally. Increasing screen exposure and rising prevalence of refractive errors are further sustaining demand for single vision lenses, particularly in emerging economies where cost-effective eyewear solutions are preferred. In addition, strong distribution through optical retail chains and e-commerce platforms is supporting segment dominance. However, demand is gradually shifting toward advanced lens types due to lifestyle changes and digital eye strain.

The Progressive Lens segment is expected to register the fastest CAGR of 7.4% from 2026 to 2033, driven by rising cases of presbyopia among the aging global population. Progressive lenses offer seamless vision correction across near, intermediate, and distance viewing without visible bifocal lines, making them highly preferred for premium eyewear users. Increasing adoption among working professionals exposed to digital devices is significantly boosting demand. Technological advancements in free-form digital surfacing and personalized lens design are improving visual comfort and precision. Moreover, growing preference for premium and aesthetic eyewear solutions is accelerating adoption in developed markets such as North America and Europe. Expanding awareness in Asia-Pacific is further supporting rapid segment growth.

- By Application

On the basis of application, the market is segmented into Myopia, Hyperopia/Hypermetropia, Astigmatism, and Presbyopia. The Myopia segment dominated the global market with a share of 42.6% in 2025, primarily due to the rapidly increasing prevalence of nearsightedness worldwide, especially among children and young adults. According to global ophthalmology studies, myopia prevalence is rising sharply in East Asia, with rates exceeding 80–90% among teenagers in countries like China, South Korea, and Japan, driven by increased screen time and reduced outdoor activity. The growing use of digital devices, smartphones, and online learning platforms has significantly accelerated myopia progression globally. Rising awareness of early vision correction and increasing availability of affordable prescription lenses are further strengthening this segment. In addition, expanding eye-care infrastructure and school-based vision screening programs are contributing to sustained demand.

The Presbyopia segment is expected to witness the fastest CAGR of 6.9% from 2026 to 2033, driven by the rapidly aging global population. Presbyopia typically affects individuals above 40 years, and its prevalence is increasing significantly in developed as well as emerging economies. Growing demand for progressive lenses and workspace progressive lenses is supporting this segment’s expansion. Increasing digital device usage among middle-aged populations is further intensifying near-vision correction needs. Technological advancements in premium progressive lens design are improving visual clarity and comfort. Rising disposable incomes and preference for high-quality vision correction solutions are also accelerating adoption across urban populations.

- By Lens Coating

On the basis of lens coating, the market is segmented into Anti-reflective, Scratch Resistant Coating, Anti-Fog Coating, and Ultraviolet (UV) Treatment. The Anti-reflective Coating segment dominated the market with a share of 36.8% in 2025, due to its ability to reduce glare, improve visual clarity, and enhance aesthetic appearance of lenses. This coating is widely used in premium prescription lenses, especially among working professionals and digital device users. Increasing screen exposure and demand for reduced eye strain have significantly boosted adoption of anti-reflective coatings. Optical retailers and manufacturers are increasingly offering AR-coated lenses as a standard upgrade, further supporting segment dominance. In addition, integration with blue-light filtering technologies is enhancing product value.

The Scratch Resistant Coating segment is expected to register the fastest CAGR of 6.7% from 2026 to 2033, driven by rising demand for durable and long-lasting eyewear solutions. Increasing usage of prescription lenses in daily activities, sports, and outdoor environments is boosting demand for protective coatings. Consumers are increasingly prioritizing lens longevity and reduced maintenance costs, especially in cost-sensitive markets. Advancements in nano-coating technologies are significantly improving scratch resistance performance. Growing adoption of premium eyewear products in urban populations and expanding e-commerce eyewear sales are further accelerating segment growth globally.

Prescription Lens Market Regional Analysis

North America dominated the Prescription Lens Market and accounted for the largest revenue share of 33.84% in 2025, supported by strong optical healthcare infrastructure, high awareness of vision correction solutions, and widespread availability of advanced optometry services. The region benefits from a high prevalence of refractive errors, particularly myopia and presbyopia, driven by increased digital device usage and aging populations. In addition, strong presence of leading ophthalmic lens manufacturers, advanced lens manufacturing technologies, and high adoption of premium progressive and digitally surfaced free-form lenses are further strengthening market growth. Expanding optical retail chains and increasing consumer preference for customized vision correction solutions continue to reinforce North America’s dominant position in the global market.

U.S. Prescription Lens Market Insight

The U.S. Prescription Lens market is witnessing steady growth due to rising prevalence of vision disorders, increasing screen time exposure, and strong consumer awareness regarding eye health. The country has a well-established eye care ecosystem, including optometrists, ophthalmologists, and large optical retail chains such as EssilorLuxottica and national eyewear providers. Growing demand for premium lenses such as blue-light filtering, anti-fatigue, and progressive lenses is significantly contributing to market expansion. In addition, increasing adoption of e-commerce eyewear platforms and tele-optometry services is improving accessibility and convenience for consumers, further supporting market growth across the United States.

Europe Prescription Lens Market Insight

The Europe Prescription Lens market remains a major contributor to global revenue, driven by strong healthcare systems, high penetration of vision correction solutions, and advanced optical manufacturing capabilities. Countries such as Germany, France, and Italy have a strong presence of leading lens manufacturers and optician networks. The region also benefits from increasing adoption of digital free-form lenses, progressive lenses, and advanced lens coatings such as anti-reflective and UV protection. Rising aging population and increasing awareness of preventive eye care are further supporting demand. In addition, well-established reimbursement frameworks in several European countries enhance accessibility to prescription eyewear products.

U.K. Prescription Lens Market Insight

The U.K. Prescription Lens market is experiencing steady growth, supported by increasing prevalence of myopia and presbyopia, rising screen exposure, and strong presence of optical retail chains. The National Health Service (NHS) and private optometry providers play a key role in expanding access to vision correction services. Growing demand for affordable yet advanced lens solutions, including progressive and blue-light filtering lenses, is driving market expansion. In addition, increasing adoption of online eyewear platforms and virtual eye testing solutions is improving consumer accessibility and accelerating market growth across the U.K.

Germany Prescription Lens Market Insight

The Germany Prescription Lens market is expanding steadily due to strong optical manufacturing capabilities, advanced R&D in lens technologies, and high consumer preference for premium eyewear products. Germany is home to leading global lens manufacturers such as Carl Zeiss Vision and Rodenstock, which are driving innovation in digital surfacing and precision optics. Increasing adoption of progressive lenses and anti-reflective coatings is supporting market growth. In addition, rising aging population and strong healthcare infrastructure are contributing to sustained demand for prescription eyewear solutions across the country.

Asia-Pacific Prescription Lens Market Insight

The Asia-Pacific Prescription Lens market is expected to witness rapid growth, driven by increasing prevalence of myopia, rising digital device usage, and expanding middle-class population. Countries such as China, India, and Japan are experiencing high demand for affordable and premium eyewear solutions. Rapid urbanization, growing awareness of eye health, and improving access to optometry services are further supporting regional expansion. In addition, strong growth of organized optical retail chains and e-commerce eyewear platforms is accelerating product penetration. Asia-Pacific is also witnessing increasing adoption of progressive lenses and anti-blue light coatings due to high screen exposure among younger populations.

Japan Prescription Lens Market Insight

The Japan Prescription Lens market is witnessing consistent growth due to a rapidly aging population and increasing prevalence of presbyopia. Japan has one of the highest rates of advanced eyewear adoption, particularly progressive and workspace progressive lenses. Strong technological innovation in optical manufacturing and lens precision is supporting market expansion. In addition, high screen time usage and increasing demand for premium vision correction solutions are driving adoption of advanced coatings such as anti-reflective and UV protection lenses. The country’s well-developed optical retail infrastructure further supports steady market growth.

China Prescription Lens Market Insight

The China Prescription Lens market is growing rapidly, driven by a large population base, rising myopia prevalence, and increasing digital device usage. According to ophthalmology studies, myopia rates among young people in urban China are among the highest globally, exceeding 80% in school-aged populations, significantly boosting demand for corrective lenses. Expanding middle-class income levels, growing awareness of eye care, and rapid expansion of optical retail chains are further accelerating market growth. In addition, strong adoption of e-commerce eyewear platforms and increasing availability of affordable prescription lenses are positioning China as one of the fastest-growing markets globally.

Prescription Lens Market Share

The Prescription Lens industry is primarily led by well-established companies, including:

- Johnson & Johnson Vision Care Inc. (U.S.)

- Carl Zeiss Vision GmbH (Germany)

- HOYA Corporation (Japan)

- Bausch + Lomb Corporation (U.S.)

- CooperVision (U.S.)

- Rodenstock GmbH (Germany)

- Nikon Lenswear (Japan)

- Shamir Optical Industry Ltd. (Israel)

- Vision Rx Lab (India)

- Younger Optics (U.S.)

- Tokai Optical Co., Ltd. (Japan)

- SEIKO Optical Products Co., Ltd. (Japan)

- Hoya Vision Care Europe (Europe)

- Shanghai Conant Optical Co., Ltd. (China)

- Mingyue Optical Lens Co., Ltd. (China)

- Wanxin Optical (China)

- Xiamen Yarui Optical Co., Ltd. (China)

- Essilor India Pvt. Ltd. (India)

- GKB Ophthalmics Ltd. (India)

- Eastman Vision Care (India)

- Lenskart Solutions Pvt. Ltd. (India)

- Vision Ease Lens (U.S.)

- Alpha Corporation (Japan)

- SEED Co., Ltd. (Japan)

- Menicon Co., Ltd. (Japan)

- Rodenstock India (India)

- Carl Zeiss India (India)

- Novacel Optical (France)

Latest Developments in Prescription Lens Market

- In January 2021, EssilorLuxottica announced the launch of “Ray-Ban Authentic” lenses in the United States, combining Ray-Ban frames with Essilor’s advanced prescription lens technologies such as Varilux progressive lenses, Crizal coatings, and Transitions photochromic options. The initiative strengthened the integration of premium eyewear and advanced optical correction, expanding access to customized single vision and progressive lens solutions. This launch marked a key step in the company’s strategy to diversify prescription lens offerings through branded eyewear ecosystems and advanced lens customization

- In February 2022, ZEISS Vision Care launched ZEISS PhotoFusion X photochromic lenses globally, introducing a next-generation self-tinting lens technology with significantly improved performance. The lenses darken up to 60% faster and clear up to 80% faster compared to previous generations, while also integrating enhanced blue light and UV protection. This development addressed rising consumer demand for adaptive eyewear suited for both indoor digital environments and outdoor light exposure. The launch strengthened ZEISS’s position in premium photochromic and digital lens innovation

- In May 2024, LensCrafters (EssilorLuxottica) launched Transitions GEN S photochromic lenses across North America, featuring ultra-responsive clear-to-dark performance and improved optical clarity. The lenses are designed to adapt rapidly to changing light conditions, offering enhanced visual comfort for consumers with active lifestyles and high digital exposure. This launch highlights the continued evolution of adaptive lens technologies and the strong expansion of premium photochromic solutions in retail optical channels

- In February 2025, EssilorLuxottica received FDA clearance for Nuance Audio Glasses, integrating prescription lenses with hearing assistance technology, marking a major step in multifunctional smart eyewear. The product combines optical correction with audio enhancement capabilities, targeting individuals with mild to moderate hearing loss while maintaining prescription lens functionality. This innovation represents the convergence of prescription eyewear with assistive medical technology and smart wearable ecosystems

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.