Global Primary Biliary Cirrhosis Market

Market Size in USD Billion

USD

1.15 Billion

USD

2.11 Billion

2025

2033

USD

1.15 Billion

USD

2.11 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.15 Billion | |

| USD 2.11 Billion | |

| % | |

|

Primary Biliary Cirrhosis Market Size

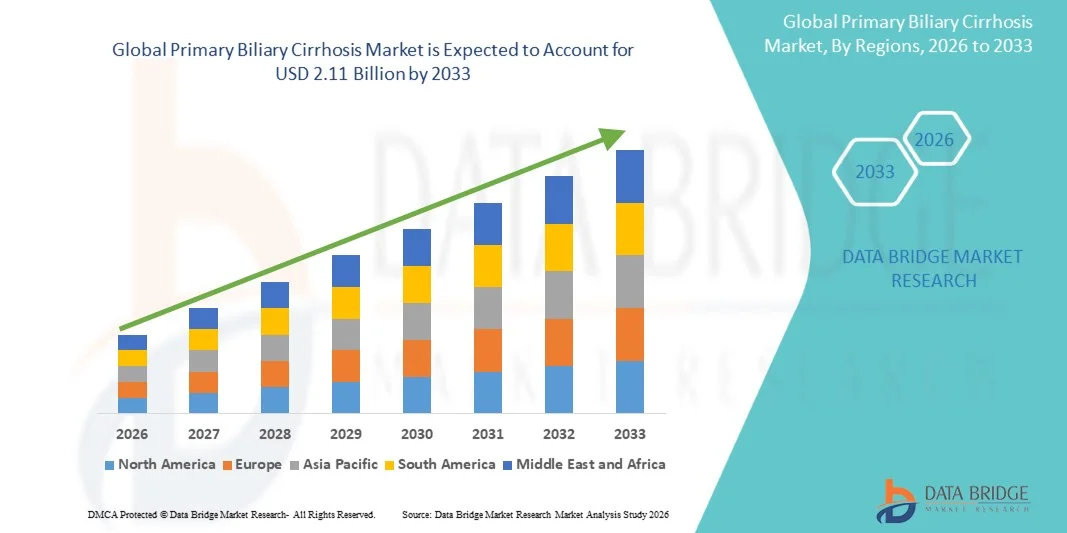

- The global primary biliary cirrhosis market size was valued at USD 1.15 billion in 2025and is expected to reach USD 2.11 billion by 2033, at a CAGR of 7.90% during the forecast period

- The market growth is largely fueled by the increasing prevalence of chronic autoimmune liver diseases, rising awareness regarding early diagnosis of cholestatic liver disorders, and continuous advancements in targeted therapies such as bile acid modulators and immunosuppressive treatments, leading to improved disease management outcomes

- Furthermore, growing demand for effective long-term symptom control, increasing focus on slowing disease progression and preventing liver failure, and expanding access to hepatology specialty care are establishing Primary Biliary Cirrhosis solutions as an essential part of modern liver disease management. These converging factors are accelerating the uptake of Primary Biliary Cirrhosis solutions, thereby significantly boosting the industry's growth

Primary Biliary Cirrhosis Market Analysis

- Primary Biliary Cirrhosis (Primary Biliary Cholangitis) treatments, including ursodeoxycholic acid (UDCA), obeticholic acid, immunosuppressants, and emerging targeted therapies, are increasingly vital components of modern hepatology care due to their role in slowing bile duct damage, improving liver function, and delaying progression to cirrhosis and liver failure

- The escalating demand for Primary Biliary Cirrhosis treatments is primarily fueled by rising prevalence of autoimmune liver diseases, increasing awareness and early diagnosis of cholestatic disorders, and continuous advancements in liver-specific pharmacological therapies and disease-modifying drugs

- North America dominated the Primary Biliary Cirrhosis market with the largest revenue share of approximately 39.4% in 2025, characterized by advanced hepatology care infrastructure, high disease awareness, strong adoption of novel therapies, and significant presence of leading pharmaceutical companies, particularly in the U.S.

- Asia-Pacific is expected to be the fastest growing region in the Primary Biliary Cirrhosis market during the forecast period due to improving healthcare access, rising awareness of chronic liver diseases, increasing diagnostic rates, expanding specialty liver clinics, and growing healthcare expenditure across emerging economies

- The Oral segment accounted for the largest market revenue share of 74.6% in 2025, driven by the dominance of oral drugs such as UDCA and Obeticholic Acid

Report Scope and Primary Biliary Cirrhosis Market Segmentation

|

Attributes |

Primary Biliary Cirrhosis Key Market Insights |

|

Segments Covered |

· By Drug Type: Ursodeoxycholic acid (UDCA), Obeticholic acid · By Stages: Portal, Periportal, Septal, Cirrhotic, and Others · By Treatment Indication: Cirrhosis, Itching, Dry Eye, Dry Mouth, and Others · By Treatment Type: Medication, Surgery, and Others · By Route of Administration: Oral, Parenteral, and Others · By End-Users: Hospitals, Homecare, Specialty Clinics, and Others · By Distribution Channel: Hospital Pharmacy, Retail Pharmacy, Online Pharmacies, and Others |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Pfizer Inc. (U.S.) · AbbVie Inc. (U.S.) · Johnson & Johnson (U.S.) · Novartis AG (Switzerland) · Merck & Co., Inc. (U.S.) · Bristol-Myers Squibb Company (U.S.) · Eli Lilly and Company (U.S.) · Roche Holding AG (Switzerland) · Sanofi S.A. (France) · AstraZeneca plc (U.K.) · GlaxoSmithKline plc (U.K.) · UCB S.A. (Belgium) · Biogen Inc. (U.S.) · Amgen Inc. (U.S.) · Teva Pharmaceutical Industries Ltd. (Israel) · Sun Pharmaceutical Industries Ltd. (India) · Dr. Reddy’s Laboratories Ltd. (India) · Cipla Limited (India) · Alnylam Pharmaceuticals, Inc. (U.S.) · Intercept Pharmaceuticals, Inc. (U.S.) |

|

Market Opportunities |

· Growing demand for targeted and disease-modifying liver therapies · Expanding diagnosis rates and improved access in emerging markets |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Primary Biliary Cirrhosis Market Trends

“Advancements in Targeted Therapies and Disease-Modifying Treatment Approaches”

- A significant and accelerating trend in the global Primary Biliary Cirrhosis (PBC) market is the growing shift toward advanced disease-modifying therapies that target the underlying autoimmune and cholestatic mechanisms of the disease rather than only managing symptoms. Increasing understanding of PBC pathophysiology is driving innovation in precision hepatology and immune-targeted treatment strategies

- For instance, ursodeoxycholic acid (UDCA) remains the first-line standard therapy for PBC, but a notable clinical advancement has been the adoption of obeticholic acid (OCA) as a second-line treatment for patients with inadequate response to UDCA. In several hepatology centers across North America and Europe, OCA has demonstrated improved biochemical response in reducing alkaline phosphatase levels and slowing disease progression

- Another emerging development includes the use of fibrates such as bezafibrate and fenofibrate as off-label adjunct therapies. Clinical studies, particularly in Japan and parts of Europe, have shown that fibrates can improve cholestatic markers and may enhance long-term disease control when combined with UDCA therapy

- In addition, research into novel FXR agonists, PPAR agonists, and immunomodulatory agents is expanding the treatment pipeline. Pharmaceutical companies are actively conducting clinical trials focused on slowing fibrosis progression and improving bile acid metabolism regulation in PBC patients

- There is also increasing emphasis on early-stage diagnosis and intervention, as treating patients in the early asymptomatic phase significantly improves long-term liver outcomes. Advanced diagnostic tools such as anti-mitochondrial antibody (AMA) testing and liver elastography are helping clinicians identify PBC earlier and initiate timely therapy

- Globally, increasing awareness of autoimmune liver diseases and improvements in hepatology care infrastructure are supporting earlier diagnosis and better disease management across both developed and emerging healthcare systems

Primary Biliary Cirrhosis Market Dynamics

Driver

“Rising Prevalence of Autoimmune Liver Disorders and Improved Diagnostic Awareness”

- The increasing global prevalence of autoimmune liver diseases is a key driver for the growth of the Primary Biliary Cirrhosis market. Improved awareness among clinicians and patients is leading to higher diagnosis rates, particularly among middle-aged women who are most commonly affected by the disease

- For instance, in recent years, several national liver disease registries in countries such as the United States, United Kingdom, and Canada have reported rising detection of early-stage PBC cases, largely due to increased use of routine liver function testing and improved screening protocols in primary care settings

- Advancements in diagnostic tools such as anti-mitochondrial antibody (AMA) testing, liver biopsy techniques, and non-invasive fibrosis assessment methods (e.g., elastography) are enabling earlier and more accurate identification of disease progression

- Expanding access to specialized hepatology care and multidisciplinary liver clinics is further improving patient outcomes by enabling earlier intervention and long-term disease monitoring

- In addition, increasing healthcare investments in chronic liver disease management and growing physician awareness of autoimmune etiologies are contributing to improved treatment initiation rates globally

Restraint/Challenge

“Limited Curative Options and Progressive Nature of the Disease”

- A major challenge in the Primary Biliary Cirrhosis market is the absence of a definitive curative treatment, as current therapies primarily aim to slow disease progression rather than reverse liver damage. This creates long-term management challenges for both patients and healthcare providers

- For instance, while UDCA and second-line agents such as obeticholic acid can improve biochemical markers, a subset of patients continues to experience disease progression, eventually leading to cirrhosis, liver failure, or the need for transplantation

- Another key limitation is the variable patient response to existing therapies, with some individuals showing excellent biochemical improvement while others demonstrate poor or partial response despite long-term treatment adherence

- Late diagnosis in many regions further complicates disease outcomes, as patients may already present with advanced fibrosis or cirrhosis at the time of detection, reducing the effectiveness of pharmacological interventions

- In addition, long-term therapy can be associated with side effects such as pruritus, gastrointestinal discomfort, and metabolic changes, which may impact patient adherence and quality of life

- Addressing these challenges will require continued investment in novel drug development, improved early screening programs, and expanded access to specialized hepatology care to ensure better long-term disease control

Primary Biliary Cirrhosis Market Scope

The market is segmented on the basis of drug type, stages, treatment indication, treatment type, route of administration, end-users, and distribution channel.

- By Drug Type

On the basis of drug type, the Primary Biliary Cirrhosis market is segmented into Ursodeoxycholic Acid (UDCA), Obeticholic Acid, and Others. The Ursodeoxycholic Acid (UDCA) segment dominated the largest market revenue share of 61.4% in 2025, driven by its status as the first-line standard therapy for slowing disease progression. UDCA is widely prescribed due to its proven efficacy in improving liver function and delaying cirrhosis onset. Strong clinical guideline recommendations support its dominance. High global availability and affordability further enhance adoption. Increasing early-stage diagnosis contributes to long-term usage. Its well-established safety profile strengthens physician preference. Expanding awareness programs for liver disorders also support market leadership.

The Obeticholic Acid segment is expected to witness the fastest CAGR of 24.8% from 2026 to 2033, driven by rising use in patients with inadequate response to UDCA. It offers a novel mechanism targeting bile acid pathways and improving liver biochemistry. Increasing regulatory approvals across regions support market penetration. Growing adoption in second-line therapy enhances demand. Strong clinical trial outcomes boost physician confidence. Expanding use in combination therapy strengthens effectiveness. Rising prevalence of progressive PBC cases accelerates uptake.

- By Stages

On the basis of stages, the Primary Biliary Cirrhosis market is segmented into Portal, Periportal, Septal, Cirrhotic, and Others. The Portal stage segment accounted for the largest market revenue share of 34.9% in 2025, driven by early disease detection during routine liver function screening. At this stage, patients respond well to pharmacological interventions. Increasing awareness of liver health supports early diagnosis. Growing use of routine biochemical testing boosts identification rates. Strong focus on early intervention delays disease progression. Expanding healthcare access improves screening coverage. Rising physician vigilance contributes to higher detection rates.

The Cirrhotic stage segment is expected to witness the fastest CAGR of 23.6% from 2026 to 2033, driven by increasing progression of untreated or late-diagnosed cases. Patients at this stage require intensive management and advanced therapies. Rising liver transplant evaluations contribute to demand. Growing complications such as liver failure increase hospitalization rates. Expanding use of biologics and supportive care enhances treatment needs. Increasing mortality awareness supports aggressive management strategies. Advancements in cirrhosis care improve survival outcomes.

- By Treatment Indication

On the basis of treatment indication, the Primary Biliary Cirrhosis market is segmented into Cirrhosis, Itching, Dry Eye, Dry Mouth, and Others. The Cirrhosis segment dominated the largest market revenue share of 42.7% in 2025, driven by its critical role as the advanced stage of disease requiring long-term management. High hospitalization rates and liver complications contribute to dominance. Increasing need for disease-modifying therapies supports demand. Strong focus on liver function preservation reinforces treatment adoption. Rising global burden of chronic liver disease strengthens segment growth. Expanding clinical management protocols improve patient outcomes.

The Itching (Pruritus) segment is expected to witness the fastest CAGR of 25.1% from 2026 to 2033, driven by high symptom prevalence and significant impact on patient quality of life. Growing use of bile acid modulators and antipruritic therapies supports treatment adoption. Increasing patient awareness encourages early symptom management. Advancements in targeted therapies enhance relief outcomes. Rising dermatological-liver care collaboration boosts diagnosis. Expanding prescription of novel agents strengthens demand. Continuous research into pruritus mechanisms drives innovation.

- By Treatment Type

On the basis of treatment type, the Primary Biliary Cirrhosis market is segmented into Medication, Surgery, and Others. The Medication segment held the largest market revenue share of 68.3% in 2025, driven by widespread use of UDCA and second-line therapies. Pharmacological management remains the primary treatment approach for all disease stages. Increasing availability of disease-modifying drugs supports dominance. Strong clinical guidelines favor long-term medication use. Rising early diagnosis enhances drug adoption rates. Expanding pharmaceutical pipelines strengthen treatment options. High patient adherence to oral therapies further supports growth.

The Surgery segment is expected to witness the fastest CAGR of 22.9% from 2026 to 2033, driven by increasing liver transplant procedures in end-stage disease. Rising cases of liver failure accelerate surgical interventions. Advancements in transplant techniques improve survival outcomes. Growing donor availability supports procedure volume. Increasing healthcare infrastructure development enhances access. Strong post-operative care systems boost success rates. Rising awareness of transplant options drives segment expansion.

- By Route of Administration

On the basis of route of administration, the Primary Biliary Cirrhosis market is segmented into Oral, Parenteral, and Others. The Oral segment accounted for the largest market revenue share of 74.6% in 2025, driven by the dominance of oral drugs such as UDCA and Obeticholic Acid. Oral administration offers ease of use and long-term compliance benefits. High outpatient treatment preference supports growth. Increasing chronic disease management reinforces oral therapy adoption. Strong availability of oral formulations enhances accessibility. Physician preference for non-invasive treatment supports dominance. Expanding generic drug availability boosts affordability.

The Parenteral segment is expected to witness the fastest CAGR of 23.7% from 2026 to 2033, driven by increasing use of injectable supportive therapies in advanced disease stages. Hospital-based administration supports acute care management. Rising adoption of biologic agents contributes to growth. Advancements in injectable drug delivery improve efficacy. Increasing severity of late-stage PBC cases boosts demand. Expanding clinical research enhances therapeutic innovation. Growing inpatient care requirements further support adoption.

- By End-Users

On the basis of end-users, the Primary Biliary Cirrhosis market is segmented into Hospitals, Homecare, Specialty Clinics, and Others. The Hospitals segment dominated the largest market revenue share of 55.8% in 2025, driven by availability of advanced diagnostic facilities and specialist hepatology care. Hospitals manage most moderate to severe cases requiring continuous monitoring. Strong infrastructure for liver disease management supports dominance. Increasing inpatient admissions for cirrhosis complications boosts demand. Availability of multidisciplinary care enhances outcomes. Expanding transplant evaluation centers further strengthen market leadership.

The Specialty Clinics segment is expected to witness the fastest CAGR of 24.3% from 2026 to 2033, driven by increasing preference for focused liver disease management. Rising outpatient consultations support adoption. Growing availability of specialized hepatology expertise enhances care quality. Increasing patient preference for targeted treatment improves demand. Expanding diagnostic services in clinics strengthens accessibility. Strong referral networks from hospitals boost growth. Rising awareness of chronic liver diseases further accelerates expansion.

- By Distribution Channel

On the basis of distribution channel, the Primary Biliary Cirrhosis market is segmented into Hospital Pharmacy, Retail Pharmacy, Online Pharmacy, and Others. The Hospital Pharmacy segment held the largest market revenue share of 52.6% in 2025, driven by direct dispensing of prescription therapies in clinical settings. Strong control over specialty drug distribution supports dominance. High reliance on hospital-based treatment pathways reinforces usage. Increasing hospitalization rates for liver disease contribute to demand. Availability of high-cost therapies within hospitals strengthens market position. Integrated care models improve drug access efficiency.

The Online Pharmacy segment is expected to witness the fastest CAGR of 26.2% from 2026 to 2033, driven by rising digital healthcare adoption and convenience of home delivery. Increasing telemedicine consultations support e-prescriptions. Growing patient preference for privacy and accessibility boosts demand. Expansion of e-pharmacy platforms enhances drug availability. Improved logistics systems ensure timely delivery of medications. Rising awareness of chronic disease management strengthens adoption. Continuous digital transformation in healthcare accelerates growth.

Primary Biliary Cirrhosis Market Regional Analysis

- North America dominated the primary biliary cirrhosis market with the largest revenue share of approximately 39.4% in 2025, characterized by advanced hepatology care infrastructure, high disease awareness, strong adoption of novel therapies, and significant presence of leading pharmaceutical companies, particularly in the U.S.

- Patients and healthcare providers in the region highly value early diagnosis, access to advanced disease-modifying therapies, and specialized liver care services that help slow disease progression, manage symptoms, and improve long-term quality of life

- This dominance is further supported by robust healthcare expenditure, well-established specialty hepatology centers, active clinical research in autoimmune liver diseases, and increasing availability of targeted treatment options, positioning North America as a leading market for Primary Biliary Cirrhosis management

U.S. Primary Biliary Cirrhosis Market Insight

The U.S. primary biliary cirrhosis market captured the largest revenue share in 2025 within North America, driven by strong diagnostic capabilities, increasing awareness of autoimmune liver disorders, and widespread adoption of advanced therapies including bile acid-based treatments and emerging targeted drugs. Patients benefit from well-structured hepatology care pathways and early intervention strategies. The presence of major pharmaceutical companies and ongoing clinical research programs further supports market expansion.

Europe Primary Biliary Cirrhosis Market Insight

The Europe primary biliary cirrhosis market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by strong public healthcare systems, increasing awareness of chronic liver diseases, and growing availability of novel therapeutic options. Expansion of hepatology specialty centers and improved diagnostic screening are further supporting treatment uptake across the region.

U.K. Primary Biliary Cirrhosis Market Insight

The U.K. primary biliary cirrhosis market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by improved disease recognition, access to specialist liver clinics, and increasing use of guideline-based treatment approaches. Public healthcare support and growing awareness campaigns are also contributing to earlier diagnosis and management.

Germany Primary Biliary Cirrhosis Market Insight

The Germany primary biliary cirrhosis market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced healthcare infrastructure, strong focus on early diagnosis, and increasing adoption of innovative liver disease therapies. Germany’s emphasis on research-driven treatment and specialty care networks is further strengthening market growth.

Asia-Pacific Primary Biliary Cirrhosis Market Insight

The Asia-Pacific primary biliary cirrhosis market is poised to grow at the fastest CAGR during the forecast period, due to improving healthcare access, rising awareness of chronic liver diseases, increasing diagnostic rates, expanding specialty liver clinics, and growing healthcare expenditure across emerging economies. Strengthening healthcare systems and better disease recognition are key growth drivers in the region.

Japan Primary Biliary Cirrhosis Market Insight

The Japan primary biliary cirrhosis market is gaining momentum due to advanced healthcare infrastructure, strong screening programs, and increasing awareness of autoimmune liver disorders. The adoption of modern treatment approaches and specialized hepatology care is steadily improving patient outcomes.

China Primary Biliary Cirrhosis Market Insight

The China primary biliary cirrhosis market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rising disease awareness, improving diagnostic infrastructure, increasing healthcare expenditure, and expanding availability of specialist liver care services. Growing hospital capacity and improved access to advanced therapies are key factors driving market growth in China.

Primary Biliary Cirrhosis Market Share

The Primary Biliary Cirrhosis industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Johnson & Johnson (U.S.)

- Novartis AG (Switzerland)

- Merck & Co., Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- Eli Lilly and Company (U.S.)

- Roche Holding AG (Switzerland)

- Sanofi S.A. (France)

- AstraZeneca plc (U.K.)

- GlaxoSmithKline plc (U.K.)

- UCB S.A. (Belgium)

- Biogen Inc. (U.S.)

- Amgen Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Reddy’s Laboratories Ltd. (India)

- Cipla Limited (India)

- Alnylam Pharmaceuticals, Inc. (U.S.)

- Intercept Pharmaceuticals, Inc. (U.S.)

Latest Developments in Global Primary Biliary Cirrhosis Market

- In April 2021, Gilead Sciences’ seladelpar (PPAR-δ agonist) demonstrated significant Phase 3 efficacy results in reducing alkaline phosphatase and improving pruritus in patients with primary biliary cholangitis, strengthening its position as a next-generation second-line therapy after ursodeoxycholic acid (UDCA)

- In April 2023, long-term Phase 3 data from the ENHANCE trial of seladelpar showed sustained biochemical response and clinically meaningful improvement in itching symptoms in PBC patients, supporting its advancement toward regulatory approval as a disease-modifying therapy

- In June 2024, the U.S. FDA granted accelerated approval to elafibranor (Iqirvo, Ipsen) for the treatment of primary biliary cholangitis in adults with inadequate response to UDCA, marking one of the first dual PPARα/δ agonists approved for PBC management

- In August 2024, the U.S. FDA granted accelerated approval to seladelpar (Livdelzi, Gilead Sciences) for treatment of primary biliary cholangitis, recognizing its efficacy in improving biochemical markers and reducing pruritus, and establishing it as a key second-line therapy option

- In September 2025, the U.S. FDA confirmed withdrawal of obeticholic acid (Ocaliva, Intercept Pharmaceuticals) for PBC due to post-marketing safety concerns, including risks of serious liver injury, significantly reshaping the treatment landscape and accelerating adoption of newer PPAR-based therapies

- In October 2025, real-world evidence presented at major hepatology conferences showed increasing use of seladelpar and elafibranor following obeticholic acid withdrawal, with data demonstrating improved liver stiffness outcomes and sustained biochemical control in long-term PBC management

- In November 2025, comparative health-economic analyses highlighted that elafibranor and seladelpar are now the dominant second-line therapies in PBC, with ongoing studies evaluating their long-term cost-effectiveness, safety, and symptom control superiority over older agents

- In December 2025, updated clinical reviews confirmed that UDCA, elafibranor, and seladelpar represent the current FDA-approved therapeutic backbone for PBC, reflecting a major transition from bile acid modulators (like obeticholic acid) toward PPAR-targeted disease-modifying therapies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.