Global Primary Clostridioides Difficile Infection Market

Market Size in USD Billion

USD

1.27 Billion

USD

2.07 Billion

2025

2033

USD

1.27 Billion

USD

2.07 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.27 Billion | |

| USD 2.07 Billion | |

| % | |

|

Primary Clostridioides Difficile Infection Market Size

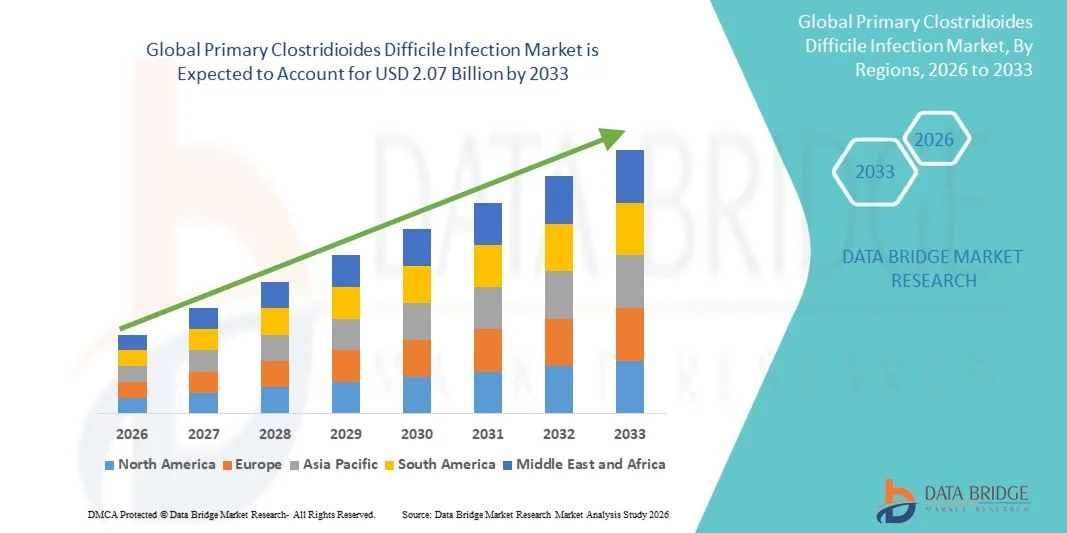

- The global primary clostridioides difficile infection market size was valued at USD 1.27 billion in 2025 and is expected to reach USD 2.07 billion by 2033, at a CAGR of 6.30% during the forecast period

- The market growth is largely fueled by the rising prevalence of hospital-acquired infections, increasing antibiotic usage, and growing awareness regarding gastrointestinal healthcare, leading to greater demand for effective diagnostic, preventive, and treatment solutions across hospitals, clinics, and long-term care facilities

- Furthermore, rising demand for rapid diagnosis, targeted antimicrobial therapies, and infection control measures is establishing Primary Clostridioides Difficile Infection solutions as an essential component of modern healthcare management. These converging factors are accelerating the uptake of Primary Clostridioides Difficile Infection solutions, thereby significantly boosting the industry's growth

Primary Clostridioides Difficile Infection Market Analysis

- Primary Clostridioides Difficile Infection solutions, including antibiotics, microbiome-based therapeutics, diagnostic tests, and infection prevention products, are increasingly vital components of modern healthcare systems across hospitals, specialty clinics, and long-term care facilities due to their role in managing severe gastrointestinal infections and reducing recurrence risk

- The escalating demand for Primary Clostridioides Difficile Infection solutions is primarily fueled by rising incidence of hospital-acquired infections, increasing use of broad-spectrum antibiotics, growing elderly population, and heightened focus on antimicrobial stewardship and infection control practices

- North America dominated the primary clostridioides difficile infection market with the largest revenue share of approximately 44.2% in 2025, characterized by advanced healthcare infrastructure, high diagnosis rates, favorable reimbursement systems, and the presence of major pharmaceutical companies, with the U.S. experiencing substantial growth in targeted therapies, rapid diagnostics, and hospital infection management programs

- Asia-Pacific is expected to be the fastest growing region in the primary clostridioides difficile infection market during the forecast period due to improving healthcare infrastructure, increasing hospitalization rates, growing awareness of healthcare-associated infections, rising antibiotic consumption, and expanding access to advanced diagnostic and treatment options across China, India, Japan, and Southeast Asia

- The medication segment dominated the largest market revenue share of 74.8% in 2025, driven by the widespread use of first-line antibiotic therapies such as vancomycin, fidaxomicin, and metronidazole for managing primary infections

Report Scope and Primary Clostridioides Difficile Infection Market Segmentation

|

Attributes |

Primary Clostridioides Difficile Infection Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Primary Clostridioides Difficile Infection Market Trends

“Enhanced Infection Management Through Advanced Diagnostics and Microbiome-Based Therapies”

- A significant and accelerating trend in the global Primary Clostridioides Difficile Infection market is the growing adoption of rapid molecular diagnostics, microbiome restoration therapies, and precision infection management strategies. These innovations are improving early detection, treatment outcomes, and recurrence prevention in patients with primary C. difficile infection

- Advanced diagnostic technologies are increasingly being used to identify toxigenic C. difficile strains quickly and accurately, enabling faster treatment decisions and infection control measures

- For instance, hospitals worldwide are adopting PCR-based stool diagnostic assays from companies such as bioMérieux and Cepheid to rapidly confirm C. difficile infections

- The increasing use of microbiome-based therapeutics is also reshaping treatment pathways by restoring healthy gut flora after antibiotic disruption, reducing recurrence risk and improving patient recovery

- Another notable trend is the growing emphasis on antimicrobial stewardship programs in hospitals to reduce unnecessary antibiotic exposure, a major risk factor for CDI development. For instance, healthcare systems in the U.S. and Europe are implementing stewardship protocols to lower broad-spectrum antibiotic overuse and associated C. difficile incidence

- In addition, healthcare providers are increasingly adopting digital surveillance systems and hospital infection monitoring tools to track outbreaks, improve hygiene compliance, and strengthen prevention programs

- This shift toward faster diagnostics, preventive care, and microbiome-focused treatment is fundamentally reshaping CDI management and driving demand for innovative therapeutic solutions

Primary Clostridioides Difficile Infection Market Dynamics

Driver

“Rising Hospital-Acquired Infections and Increasing Antibiotic Usage”

- The increasing incidence of hospital-acquired infections and widespread antibiotic use remain major drivers for the Primary Clostridioides Difficile Infection market, as antibiotic exposure is one of the leading causes of gut microbiome disruption linked to CDI

- Growing hospitalization rates among elderly and immunocompromised populations are further supporting market demand

- For instance, aging populations in the U.S., Japan, Germany, and Italy have contributed to higher hospitalization volumes, increasing the patient pool at risk of primary CDI

- Rising awareness regarding infection control and earlier diagnosis is also encouraging greater use of targeted antibiotics, probiotics, and novel microbiome therapies

- Furthermore, expanding healthcare infrastructure, improved laboratory testing capabilities, and stronger infection prevention policies are contributing to market growth globally

- The continued need to reduce morbidity, hospital stays, and treatment costs associated with CDI is expected to sustain demand over the forecast period

Restraint/Challenge

“High Treatment Costs, Recurrence Risks, and Diagnostic Complexity”

- One of the major challenges restraining the Primary Clostridioides Difficile Infection market is the high treatment cost associated with advanced antibiotics, microbiome therapeutics, and prolonged hospitalization in severe cases

- Recurrence risk after initial treatment continues to create clinical and economic burdens for healthcare systems

- For instance, a notable proportion of patients treated with vancomycin or fidaxomicin may still experience repeat infections, requiring additional intervention or fecal microbiota-based therapies

- Diagnostic complexity is another challenge, as distinguishing colonization from active toxin-producing infection can delay appropriate treatment decisions

- In addition, limited awareness and inadequate infection control practices in some developing healthcare settings may restrict timely diagnosis and effective disease management

- Overcoming these barriers through affordable treatment access, better recurrence prevention strategies, improved diagnostics, and expanded antimicrobial stewardship programs will be essential for sustained market growth

Primary Clostridioides Difficile Infection Market Scope

The market is segmented on the basis of treatment, route of administration, end-users, and distribution channel.

• By Treatment

On the basis of treatment, the Primary Clostridioides Difficile Infection market is segmented into medication, surgery, and others. The medication segment dominated the largest market revenue share of 74.8% in 2025, driven by the widespread use of first-line antibiotic therapies such as vancomycin, fidaxomicin, and metronidazole for managing primary infections. Medication remains the standard of care for most diagnosed patients due to its effectiveness in symptom control and bacterial eradication. Growing awareness among healthcare professionals regarding early diagnosis and prompt treatment further supported segment growth. Hospitals and outpatient centers increasingly follow evidence-based treatment guidelines favoring pharmacological management. Rising incidence of hospital-acquired infections and antibiotic-associated diarrhea also expanded patient demand. The availability of branded and generic treatment options improved affordability across multiple regions. Recurring prescriptions for follow-up management and supportive therapies strengthened revenues. Improved stool testing and rapid diagnostics enabled faster therapy initiation. Expanding elderly populations with higher infection susceptibility also contributed to demand. Strong reimbursement support in developed markets sustained treatment accessibility. Continuous product innovation in anti-infective therapies reinforced market leadership. These factors collectively ensured dominance in 2025.

The surgery segment is anticipated to witness the fastest growth rate of 8.9% from 2026 to 2033, fueled by increasing use in severe, fulminant, and treatment-resistant cases requiring urgent intervention. Surgical procedures such as colectomy are considered for patients with toxic megacolon, perforation, or life-threatening complications. Growing awareness regarding timely escalation of care is improving referral rates for surgery. Advancements in minimally invasive surgical techniques are reducing recovery times and complication risks. Hospitals are expanding specialized gastrointestinal and colorectal surgical capabilities. Rising recurrence burden in complex patients is also contributing to future procedural demand. Improved ICU support and perioperative management have enhanced outcomes in critical cases. Increasing multidisciplinary treatment pathways support faster surgical decisions. Emerging markets are investing in advanced hospital infrastructure, expanding access. Greater clinician education on severe infection protocols also aids growth. Though smaller in share, surgery remains clinically important for advanced disease. These factors position surgery as the fastest-growing treatment segment.

• By Route of Administration

On the basis of route of administration, the Primary Clostridioides Difficile Infection market is segmented into oral, injectable, and others. The oral segment held the largest market revenue share of 68.5% in 2025, driven by the strong preference for oral antibiotics such as vancomycin and fidaxomicin in first-line therapy. Oral administration is convenient, non-invasive, and highly effective for localized treatment within the gastrointestinal tract. Physicians commonly prescribe oral therapies for mild-to-moderate and many severe cases depending on patient condition. Home-based continuation therapy after discharge also supported segment growth. Higher patient compliance and ease of dosing contributed to sustained adoption. Retail and hospital pharmacy availability of oral formulations improved accessibility. Lower administration costs compared with injectable therapies favored healthcare systems. Growing outpatient management trends further increased oral prescriptions. Clinical guidelines in several countries prioritize oral treatment regimens. Expanding elderly patient populations requiring practical dosing options also added demand. Continuous innovation in tablet and suspension formulations supported usability. These factors maintained oral segment dominance.

The injectable segment is expected to witness the fastest CAGR of 9.4% from 2026 to 2033, driven by increasing use in hospitalized patients unable to tolerate oral treatment and in severe systemic complications. Injectable therapies are often utilized when immediate medical intervention is required or gastrointestinal absorption is compromised. Rising ICU admissions among elderly and immunocompromised patients support demand growth. Hospitals are increasingly maintaining ready inventories of intravenous anti-infective agents. Advances in hospital infection management protocols are accelerating appropriate injectable use. Combination treatment strategies in critical care settings also contribute to expansion. Improved inpatient monitoring enables safer administration of potent therapies. Emerging healthcare markets are upgrading infusion and inpatient capabilities. Physicians prefer injectable routes in selected emergency scenarios for rapid control. Strong hospital procurement activity further supports revenues. Growth in tertiary care centers remains a key factor. These drivers make injectable therapies the fastest-growing route segment.

• By End-Users

On the basis of end-users, the Primary Clostridioides Difficile Infection market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment accounted for the largest market revenue share of 63.7% in 2025, driven by the high incidence of healthcare-associated infections and the need for immediate diagnosis and treatment. Hospitals remain the primary centers for stool testing, isolation protocols, antibiotic administration, and management of severe dehydration or complications. Large inpatient populations and frequent antibiotic use increase infection risk, sustaining demand for treatment services. Presence of infectious disease specialists and gastroenterologists improves treatment outcomes. Hospitals also manage recurrent and severe cases requiring close observation. Strong procurement of anti-infective medications supported segment revenues. Infection prevention programs and screening protocols further increased diagnostic volumes. Public and private hospitals remain central to disease surveillance systems. ICU and emergency care capabilities add strategic importance. Reimbursement systems often favor inpatient management for serious cases. These factors collectively ensured segment dominance.

The homecare segment is anticipated to witness the fastest CAGR of 10.1% from 2026 to 2033, fueled by rising preference for recovery at home after initial stabilization in hospitals. Many mild-to-moderate patients continue oral treatment and hydration management in home settings. Telehealth follow-ups are improving treatment adherence and symptom monitoring. Aging populations increasingly prefer home-based care to avoid prolonged hospital stays. Home nursing services for medication management are expanding in developed regions. Lower treatment costs compared with inpatient care encourage adoption. Availability of doorstep pharmacy delivery improves medicine access. Digital health tools help monitor recurrence symptoms early. Family support systems also enhance patient comfort and compliance. Governments are promoting decentralized care to reduce hospital burden. Improved awareness of hygiene protocols supports safe home recovery. These factors drive strong growth in the homecare segment.

• By Distribution Channel

On the basis of distribution channel, the Primary Clostridioides Difficile Infection market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The hospital pharmacy segment dominated the largest market revenue share of 56.9% in 2025, driven by high inpatient treatment volumes and immediate access needs for anti-infective medications. Hospital pharmacies are critical for dispensing vancomycin, fidaxomicin, IV therapies, probiotics, and supportive care products. Centralized inventory systems ensure rapid treatment initiation for newly diagnosed patients. Hospitals also rely on controlled antibiotic stewardship programs managed through internal pharmacies. Strong institutional purchasing contracts supported steady revenue generation. Severe and recurrent patients commonly receive medications directly within hospital settings. Integration with electronic health records improves dispensing accuracy and compliance. Isolation wards and emergency units further increase pharmacy demand. Public hospitals in major markets remain large-volume buyers. Reimbursement structures often route acute-care prescriptions through hospital channels. Continuous patient inflow sustained segment leadership. These factors maintained dominance in 2025.

The online pharmacy segment is expected to witness the fastest CAGR of 11.3% from 2026 to 2033, fueled by increasing digital healthcare adoption and demand for convenient prescription refills. Patients recovering at home increasingly use online channels to purchase oral antibiotics and supportive therapies. Doorstep delivery improves access for elderly and mobility-limited patients. Telemedicine integration is accelerating prescription-to-purchase conversion rates. Price comparison tools and discounts attract cost-conscious consumers. Growing smartphone penetration is expanding customer reach globally. Subscription refill services improve continuity of care and adherence. Rural patients benefit from wider medicine availability through e-pharmacy platforms. Regulatory frameworks for online medicine sales are gradually strengthening. Improved logistics networks support faster and temperature-safe deliveries. Rising preference for contactless healthcare purchasing adds momentum. These factors make online pharmacy the fastest-growing distribution channel.

Primary Clostridioides Difficile Infection Market Regional Analysis

- North America dominated the primary clostridioides difficile infection market with the largest revenue share of approximately 44.2% in 2025, driven by advanced healthcare infrastructure, high diagnosis rates, and favorable reimbursement systems across the region

- The presence of major pharmaceutical companies and leading diagnostic manufacturers has significantly supported market expansion. Rising incidence of healthcare-associated infections and recurrent gastrointestinal disorders has increased demand for effective CDI management solutions. Hospitals and long-term care facilities are increasingly adopting infection prevention protocols and rapid diagnostic testing. Strong physician awareness regarding targeted antibiotic therapies and microbiome-based treatments further supports growth

- Government healthcare spending and hospital quality initiatives are also strengthening the market. Continuous innovation in rapid molecular diagnostics and recurrence prevention therapies is improving patient outcomes. High focus on antimicrobial stewardship programs contributes to early intervention and treatment optimization. North America is expected to maintain its leading market position during the forecast period

U.S. Primary Clostridioides Difficile Infection Market Insight

The U.S. primary clostridioides difficile infection market captured the largest revenue share in 2025 within North America, fueled by substantial growth in targeted therapies, rapid diagnostics, and hospital infection management programs. The country has a large hospitalized and elderly patient population at higher risk of CDI, creating strong treatment demand. Advanced laboratory networks and widespread use of PCR-based testing are improving early diagnosis rates. Strong reimbursement coverage supports access to branded therapies and supportive care solutions. Increasing physician adoption of narrow-spectrum antibiotics, monoclonal antibodies, and microbiome therapeutics is boosting market growth. Hospitals are investing heavily in infection control measures and environmental decontamination systems. Rising awareness regarding recurrence prevention and antibiotic stewardship further supports expansion. Ongoing clinical research and product launches continue to strengthen the competitive landscape. The U.S. remains the primary contributor to regional revenue growth.

Europe Primary Clostridioides Difficile Infection Market Insight

The Europe primary clostridioides difficile infection market is projected to expand at a substantial CAGR throughout the forecast period, driven by strong public healthcare systems and rising awareness of healthcare-associated infections. Increasing elderly populations and growing hospitalization rates are supporting market demand across the region. Government-backed surveillance programs and infection control guidelines are improving diagnosis and treatment pathways. Availability of advanced laboratory diagnostics and targeted therapeutic options further boosts adoption. Countries such as Germany, the U.K., France, and Italy are strengthening antimicrobial stewardship initiatives to reduce CDI burden. Rising investments in hospital hygiene and patient safety programs are also contributing to growth. Expanding clinical research in microbiome therapies and recurrence prevention supports innovation. The region benefits from established reimbursement frameworks and healthcare accessibility. Continuous modernization of healthcare facilities is expected to sustain long-term market expansion.

U.K. Primary Clostridioides Difficile Infection Market Insight

The U.K. primary clostridioides difficile infection market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by NHS-supported infection control programs and increasing focus on hospital-acquired infection reduction. The country maintains strong surveillance systems for monitoring CDI incidence and recurrence trends. Rising demand for rapid diagnostics and evidence-based treatment protocols is supporting growth. Government emphasis on antimicrobial stewardship and responsible antibiotic prescribing is reducing infection severity while increasing targeted treatment adoption. Growing elderly population and chronic disease burden continue to create treatment demand. Expansion of hospital sanitation programs and patient safety initiatives further supports the market. Research collaborations between universities and healthcare institutions are encouraging therapeutic innovation. Digital healthcare monitoring systems are improving patient management outcomes. These factors are expected to sustain market growth in the U.K.

Germany Primary Clostridioides Difficile Infection Market Insight

The Germany primary clostridioides difficile infection market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced hospital infrastructure and strong awareness regarding infection prevention. Germany has broad access to diagnostics and specialist care, supporting timely detection and treatment of CDI cases. Rising hospitalization rates and increasing elderly population are contributing to market demand. Physicians are increasingly adopting guideline-based therapies and recurrence prevention strategies for high-risk patients. Strong pharmaceutical manufacturing and healthcare research capabilities enhance product availability. Preventive healthcare policies and hygiene standards support long-term market development. Digital hospital management systems are improving infection monitoring and patient care. Germany’s focus on quality healthcare delivery is expected to drive continued expansion. The country remains one of Europe’s most significant CDI treatment markets.

Asia-Pacific Primary Clostridioides Difficile Infection Market Insight

The Asia-Pacific primary clostridioides difficile infection market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by improving healthcare infrastructure and increasing hospitalization rates. Growing awareness of healthcare-associated infections and infection control practices is accelerating regional market growth. Rising antibiotic consumption and broader use of broad-spectrum antimicrobials are increasing CDI risk, thereby driving demand for diagnosis and treatment. Governments across China, India, Japan, and Southeast Asia are expanding access to advanced healthcare services and laboratory capabilities. Increasing investments in hospital modernization and patient safety programs further support market expansion. Growing pharmaceutical manufacturing capacity is improving affordability of treatment options. Rising incidence of chronic diseases requiring hospitalization also contributes to demand. Expansion of private healthcare and diagnostic chains is enhancing accessibility. Asia-Pacific is expected to remain the fastest growing regional market during the forecast period.

Japan Primary Clostridioides Difficile Infection Market Insight

The Japan primary clostridioides difficile infection market is gaining momentum due to the country’s aging population, advanced healthcare system, and strong infection prevention standards. Japan has high awareness regarding hospital-acquired infections and routine use of diagnostic screening in healthcare facilities. Rising demand for targeted CDI therapies and recurrence prevention solutions is supporting growth. Government healthcare programs encourage early diagnosis and evidence-based treatment pathways. Increasing hospitalization among elderly populations is creating additional market demand. Physicians are adopting advanced therapies with improved safety and efficacy profiles. Strong pharmaceutical innovation and microbiome research further strengthen the market. Digital monitoring tools and integrated hospital systems support better infection management. Japan is expected to witness steady growth over the forecast period.

China Primary Clostridioides Difficile Infection Market Insight

The China primary clostridioides difficile infection market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s large patient base, expanding hospital infrastructure, and rising healthcare expenditure. Increasing awareness regarding healthcare-associated infections is improving diagnosis rates and treatment uptake. Rapid growth in hospitalization and antibiotic use has increased focus on CDI prevention and management. Government initiatives promoting hospital quality improvement and infection surveillance support market growth. Strong domestic pharmaceutical manufacturing enhances treatment availability and affordability. Expansion of laboratory testing capabilities and tertiary hospitals is improving patient access. Rising adoption of modern therapeutics and evidence-based treatment protocols is driving demand. Growth of private healthcare services further strengthens accessibility. China is expected to maintain leadership within the regional market.

Primary Clostridioides Difficile Infection Market Share

The Primary Clostridioides Difficile Infection industry is primarily led by well-established companies, including:

- Merck & Co., Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Ferring Pharmaceuticals (Switzerland)

- Astellas Pharma Inc. (Japan)

- Summit Therapeutics Inc. (U.S.)

- Seres Therapeutics, Inc. (U.S.)

- Sanofi S.A. (France)

- AstraZeneca plc (U.K.)

- GlaxoSmithKline plc (U.K.)

- Johnson & Johnson (U.S.)

- Bayer AG (Germany)

- AbbVie Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Viatris Inc. (U.S.)

- Sun Pharmaceutical Industries Ltd. (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Cipla Ltd. (India)

- Lupin Limited (India)

- Takeda Pharmaceutical Company Limited (Japan)

- Daewoong Pharmaceutical Co., Ltd. (South Korea)

Latest Developments in Global Primary Clostridioides Difficile Infection Market

- In June 2021, the Infectious Diseases Society of America (IDSA) and Society for Healthcare Epidemiology of America (SHEA) updated their clinical practice guidelines for Clostridioides difficile infection, recommending fidaxomicin over vancomycin for initial CDI episodes when feasible. The update significantly influenced treatment standards for primary Clostridioides difficile infection by emphasizing lower recurrence rates and improved clinical outcomes

- In December 2021, Astellas Pharma highlighted broader global adoption of DIFICID/Dificlir (fidaxomicin) following expanded guideline support for Clostridioides difficile infection treatment. The development strengthened market demand for narrow-spectrum antibiotics specifically designed to reduce recurrence risk in CDI patients

- In November 2022, the U.S. Food and Drug Administration approved Rebyota (fecal microbiota, live-jslm), the first FDA-approved microbiota-based therapy for prevention of recurrent Clostridioides difficile infection in adults following antibacterial treatment. Although approved for recurrent infection, the milestone marked a major commercial breakthrough in the broader CDI treatment market and accelerated microbiome-based therapeutic development

- In April 2023, the U.S. Food and Drug Administration approved Vowst™, developed by Seres Therapeutics, as the first orally administered fecal microbiota product for prevention of recurrent Clostridioides difficile infection in adults after antibacterial treatment. The capsule-based therapy improved convenience and accessibility compared with procedure-based microbiota therapies, representing a major innovation in the CDI market

- In May 2023, Nature Reviews Drug Discovery reported that Vowst’s approval created direct competition with Rebyota, establishing a new microbiome therapeutics segment within the Clostridioides difficile infection market. The launch of multiple approved microbiota products signaled increasing investment in non-antibiotic CDI prevention strategies

- In January 2025, Merck withdrew Zinplava (bezlotoxumab) from the market, according to industry treatment landscape reports. The withdrawal reshaped prevention strategies for recurrent CDI and increased commercial focus on microbiota therapies and antibiotic-based management options across the broader Clostridioides difficile infection market

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.