Global Primary Haemophagocytic Lymphohistiocytosis Market

Market Size in USD Billion

USD

2.95 Billion

USD

4.84 Billion

2025

2033

USD

2.95 Billion

USD

4.84 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.95 Billion | |

| USD 4.84 Billion | |

| % | |

|

Primary Haemophagocytic Lymphohistiocytosis Market Size

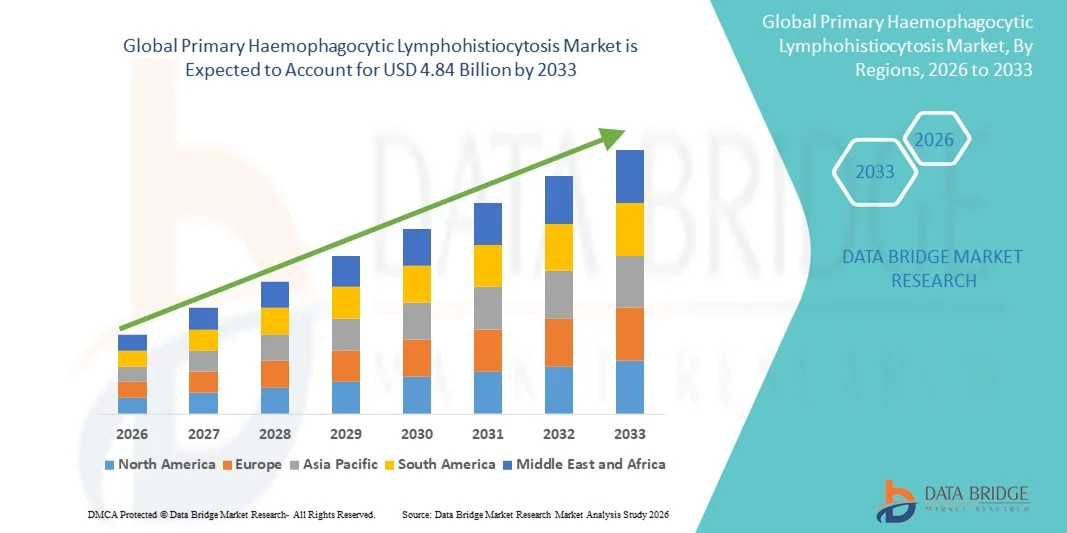

- The global primary haemophagocytic lymphohistiocytosis market size was valued at USD 2.95 billion in 2025 and is expected to reach USD 4.84 billion by 2033, at a CAGR of 6.40% during the forecast period

- The market growth is largely fueled by increasing awareness of primary haemophagocytic lymphohistiocytosis (HLH), advancements in diagnostic technologies, and the adoption of targeted therapies, immunomodulatory treatments, and hematopoietic stem cell transplantation

- Furthermore, rising investments in rare disease research, improved access to specialized treatment centers, and government-led initiatives for early diagnosis and patient education are significantly accelerating the uptake of Primary haemophagocytic lymphohistiocytosis solutions, thereby boosting overall industry growth

Primary Haemophagocytic Lymphohistiocytosis Market Analysis

- Primary Haemophagocytic Lymphohistiocytosis (HLH) is a rare, life-threatening disorder, and the market growth is largely fueled by increasing awareness of HLH, advancements in diagnostic technologies, and the adoption of targeted therapies and hematopoietic stem cell transplantation

- Furthermore, rising investments in rare disease research, improved access to specialized treatment centers, and government-led initiatives for early diagnosis and patient education are significantly accelerating the uptake of primary haemophagocytic lymphohistiocytosis solutions, thereby boosting overall industry growth

- North America dominated the primary haemophagocytic lymphohistiocytosis market with the largest revenue share of 42.5% in 2025, characterized by well-established healthcare infrastructure, high healthcare spending, and the presence of leading biopharmaceutical companies. The U.S. is experiencing substantial growth in clinical adoption of enzyme replacement therapies, immunotherapy programs, and expanded newborn screening initiatives

- Asia-Pacific is expected to be the fastest-growing region in the primary haemophagocytic lymphohistiocytosis market during the forecast period, projected to expand at a CAGR of 16.0% from 2026 to 2033. Growth is driven by increasing healthcare modernization, rising awareness of rare genetic disorders, expanding pediatric and adult HLH treatment centers, and improving access to specialized therapies in countries such as Japan, China, and India

- The Parenteral segment dominated the largest market revenue share of 71.3% in 2025, owing to its precise dosing, rapid therapeutic effect, and suitability for hospital-based management of complex PHLH cases

Report Scope and Primary Haemophagocytic Lymphohistiocytosis Market Segmentation

|

Attributes |

Primary Haemophagocytic Lymphohistiocytosis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Primary Haemophagocytic Lymphohistiocytosis Market Trends

Growing Focus on Targeted and Personalized Treatments

- A significant and accelerating trend in the global primary haemophagocytic lymphohistiocytosis (PHLH) market is the increasing adoption of targeted therapies and personalized treatment approaches that aim to improve patient outcomes

- Advances in understanding the genetic and molecular mechanisms of PHLH are enabling physicians to offer patient-specific therapies tailored to disease severity, mutation type, and immune response patterns

- For instance, in June 2024, a study published in Allergy highlighted the effectiveness of newly optimized cytokine inhibitors in reducing immune hyperactivation and improving survival rates in pediatric PHLH patients

- This trend reflects the broader move toward precision medicine in rare immunologic disorders, where treatment is adapted to the individual’s disease profile

- Biopharmaceutical companies are increasingly investing in research and development to produce therapies with improved safety profiles, longer dosing intervals, and formulations suitable for both inpatient and outpatient use

- Moreover, emerging gene therapy approaches for familial PHLH are gaining attention, offering potential long-term solutions for patients with refractory disease

- Clinical trials are focusing not only on efficacy but also on minimizing treatment-related adverse events, reflecting an emphasis on quality-of-life improvements

- Combination therapies targeting multiple immune pathways are being explored to provide more comprehensive disease management for severe or recurrent PHLH cases

- The trend also includes the development of more accessible therapies in oral or subcutaneous forms, reducing hospitalization needs and enabling home-based care

- Global collaboration among research institutions, patient advocacy groups, and pharmaceutical companies is facilitating faster translation of discoveries into clinical applications

- Increasing awareness of PHLH and its heterogeneous presentation is prompting earlier diagnosis and treatment initiation, which is critical to improving outcomes

- This evolution toward precision, targeted, and patient-centric therapies is reshaping clinician and patient expectations for PHLH management

Primary Haemophagocytic Lymphohistiocytosis Market Dynamics

Driver

Rising Awareness and Growing Need for Effective Treatments

- The increasing prevalence of both primary and secondary PHLH cases, combined with rising awareness among clinicians and caregivers, is a significant driver of market growth

- For instance, in April 2025, key hospitals and specialty clinics expanded clinical programs for early diagnosis and treatment of PHLH, reflecting the growing need for specialized care

- Improved understanding of immune dysregulation and its biomarkers is enabling faster identification of patients at risk, driving demand for advanced therapeutics

- As patients and families seek more effective, life-saving treatments, biopharmaceutical investment in innovative therapy development is increasing

- Enhanced availability of treatment guidelines and standardized protocols for PHLH management is encouraging wider adoption of evidence-based therapies. The rising adoption of therapies suitable for both inpatient and homecare settings enables broader reach and convenience for patients

- Growing collaborations between hospitals, specialty clinics, and research organizations are accelerating the introduction of new treatment options. Healthcare providers are increasingly focusing on reducing disease-related complications and mortality, which drives the adoption of advanced therapies

- Government support for rare disease research and orphan drug development is also contributing to market growth

- The increasing availability of patient education and awareness programs is prompting earlier intervention, which boosts demand for therapies. Expansion of healthcare infrastructure and improved access to specialty clinics in emerging markets further supports market uptake

- Overall, the urgent clinical need for effective, safe, and personalized therapies is a key growth driver for the PHLH market

Restraint/Challenge

Limited Awareness, High Treatment Costs, and Complex Disease Management

- The rare and complex nature of PHLH poses significant challenges for broader market penetration, including limited awareness among general practitioners and caregivers

- For instance, misdiagnosis or delayed diagnosis remains common, affecting timely treatment initiation and patient outcomes. The high cost of targeted therapies and advanced biologics can limit access, particularly in low- and middle-income countries

- Complex treatment regimens, which may involve combination immunotherapies, gene therapy, or hematopoietic stem cell transplantation, present logistical and clinical challenges. Limited availability of trained specialists and treatment centers capable of managing PHLH can hinder patient access

- Safety concerns related to immunosuppressive therapies, risk of infections, and long-term adverse effects require careful monitoring, which may restrict adoption

- Insurance coverage and reimbursement issues for rare disease treatments remain a barrier for many patients. While clinical trials continue to expand, the limited patient population can slow the pace of research and commercialization of new therapies

- Addressing the challenges of treatment adherence and managing severe disease flares requires robust patient support and monitoring programs. Regional disparities in healthcare infrastructure can further restrict access to advanced PHLH therapies

- High costs associated with gene therapy and emerging biologics may delay adoption despite their potential long-term benefits. Overcoming these barriers through awareness programs, patient support initiatives, and efforts to reduce therapy costs will be critical to sustaining market growth

Primary Haemophagocytic Lymphohistiocytosis Market Scope

The market is segmented on the basis of type, therapy type, treatment, drugs, route of administration, and end-users.

- By Type

On the basis of type, the Primary Haemophagocytic Lymphohistiocytosis market is segmented into Familial and Acquired. The Familial segment dominated the largest market revenue share of 55.6% in 2025, driven by its early onset, genetic predisposition, and the critical need for early diagnosis and treatment. Familial PHLH cases are frequently identified in pediatric populations through newborn screening programs, allowing timely intervention with medications and supportive therapies. Hospitals and specialty clinics are increasingly focusing on genetic counseling and family-based screening programs, ensuring early detection and better outcomes. The segment benefits from extensive research in gene therapy, immunotherapy, and hematopoietic stem cell transplantation. Family-focused awareness initiatives by healthcare providers enhance adherence to treatment protocols. The predictable progression of familial cases allows clinicians to implement structured care pathways. Continuous monitoring, early therapeutic intervention, and long-term follow-up are key drivers of market dominance. Insurance and government programs supporting rare genetic disorders also bolster market adoption. Investment in advanced treatment options like targeted therapies ensures sustained growth. Clinical trials demonstrating improved survival and remission rates further support the segment’s leadership. Pediatric hospital wards and specialty immunology centers are central to managing familial PHLH. The combination of genetic prevalence, structured care, and treatment innovations underpins this segment’s market dominance.

The Acquired segment is expected to witness the fastest CAGR of 9.8% from 2026 to 2033, fueled by rising incidence of secondary PHLH due to infections, autoimmune disorders, and malignancies. Improved awareness of acquired triggers and enhanced diagnostic techniques are facilitating rapid identification in adult populations. Hospitals and specialty clinics increasingly adopt immunomodulatory and targeted therapy strategies tailored to acquired cases. Advancements in supportive care, combined with early intervention protocols, are driving higher adoption rates. Ongoing research into cytokine-targeted therapies and immune checkpoint modulation further accelerates growth. The segment’s expansion is supported by increasing adult patient populations, rising healthcare expenditure, and improved access to specialty care. Multi-disciplinary approaches are increasingly used for acquired PHLH, enhancing treatment effectiveness. Rising clinician awareness and education on the disease contribute to timely therapeutic adoption. Government and private initiatives focusing on rare autoimmune disorders provide additional support. Early diagnosis and patient stratification improve clinical outcomes, reinforcing market demand. Acquired PHLH cases require flexible treatment options across hospital and homecare settings. The need for individualized therapy and increased R&D in adult-targeted drugs ensures sustained CAGR growth.

- By Therapy Type

On the basis of therapy type, the market is segmented into Immunotherapy, Chemotherapy, Targeted Therapy, and Others. The Immunotherapy segment held the largest market revenue share of 48.7% in 2025, owing to its efficacy in controlling hyperactive immune responses and improving survival rates. Immunotherapy, including monoclonal antibodies, cytokine inhibitors, and stem cell transplantation, is widely adopted across hospitals and specialty clinics. Clinical protocols aim to maximize efficacy while minimizing adverse events, with outpatient monitoring increasingly feasible. Biopharmaceutical investments in new immune-modulating agents have expanded available treatment options. Immunotherapy enables long-term disease management with reduced relapse rates. Hospitals provide specialized monitoring and supportive care for immunotherapy patients. Patient adherence is facilitated through structured therapy schedules and follow-up programs. Awareness campaigns and clinical trials validating safety and effectiveness reinforce segment dominance. Research into combination immunotherapy regimens further supports adoption. Access to immunotherapy is growing due to improved insurance coverage and reimbursement policies. Pediatric and adult populations benefit from personalized immunotherapy approaches. Overall, efficacy, clinical focus, and ongoing innovation drive market leadership in immunotherapy.

The Targeted Therapy segment is expected to witness the fastest CAGR of 10.3% from 2026 to 2033, fueled by advances in molecular understanding of PHLH and development of therapies inhibiting specific disease pathways. Personalized treatment targeting cytokine signaling and immune checkpoint regulation is gaining traction. Clinical adoption is increasing in specialty clinics and hospitals due to the precision and reduced toxicity of targeted therapies. Pharmaceutical investments in novel inhibitors further accelerate growth. Improved diagnostic methods allow better patient stratification for targeted interventions. Patient preference for therapies with fewer side effects drives adoption. Regulatory approvals and guideline inclusion support widespread clinical use. Multi-center trials demonstrate efficacy and safety, enhancing confidence among clinicians. Adoption is growing in both pediatric and adult populations. Enhanced treatment monitoring and biomarker-guided therapy improve outcomes. Targeted therapies are increasingly integrated into combination treatment regimens. Awareness among physicians and caregivers reinforces patient uptake.

- By Treatment

On the basis of treatment, the market is segmented into Medication and Surgery. The Medication segment dominated the largest market revenue share of 62.4% in 2025, driven by the use of immunosuppressants, cytokine inhibitors, and biologics for long-term disease control. Hospitals and specialty clinics rely on medications for both familial and acquired cases due to their effectiveness and ease of administration. Medication enables outpatient and homecare management, improving patient compliance. Continuous development of biologics and novel agents ensures sustained market dominance. Combination therapy approaches enhance efficacy while minimizing toxicity. Healthcare providers emphasize adherence and monitoring through structured programs. Medication allows early intervention, reducing complications and hospital stays. Pediatric cases particularly rely on pharmacologic management for survival and quality of life. Insurance coverage and government support for rare diseases further boost uptake. Educational initiatives for caregivers enhance treatment compliance. Overall, medication remains the backbone of PHLH management.

The Surgery segment is expected to witness the fastest CAGR of 8.7% from 2026 to 2033, driven by the increasing adoption of hematopoietic stem cell transplantation and other interventional procedures for patients with refractory Primary Haemophagocytic Lymphohistiocytosis. This growth is supported by continuous improvements in surgical protocols, better patient selection criteria, and advanced post-operative care practices, which collectively enhance patient outcomes. In addition, rising awareness among clinicians about the benefits of surgical interventions and growing access to specialized healthcare facilities are further contributing to the segment’s rapid expansion, making surgery an increasingly preferred treatment option for complex PHLH cases.

- By Drug Class

On the basis of drug class, the Primary Haemophagocytic Lymphohistiocytosis market is segmented into C1-INH Concentrates, Bradykinin B2-Receptor Antagonist, Icatibant, Kallikrein Inhibitor, Ecallantide, and Others. The C1-INH Concentrates segment dominated the largest market revenue share of 48.7% in 2025, owing to its proven efficacy in controlling acute PHLH episodes and reducing morbidity. These concentrates are preferred due to their rapid onset of action, reliability, and established clinical guidelines supporting their use. Hospitals and specialty clinics predominantly administer C1-INH therapy for both familial and acquired PHLH cases. Clinical trials and ongoing research validate its safety and long-term benefits, reinforcing adoption among healthcare providers. Availability in parenteral formulations supports precision dosing and emergency interventions. Widespread inclusion in treatment protocols and reimbursement programs further strengthens its dominance. The drug’s compatibility with multi-disciplinary care models enhances integration in complex treatment plans. Pharmaceutical advancements continue to optimize formulation and storage conditions. Patient outcomes improve with structured therapy schedules and monitoring. Training programs for nurses and clinicians ensure correct administration. Comprehensive clinical evidence maintains physician confidence. Overall, C1-INH concentrates remain the cornerstone for PHLH drug therapy management.

The Bradykinin B2-Receptor Antagonist segment is expected to witness the fastest CAGR of 11.8% from 2026 to 2033, driven by the development of new oral and subcutaneous formulations that enhance patient convenience. These antagonists provide targeted action on the bradykinin pathway, effectively reducing attack frequency and severity. Rising adoption is supported by increased awareness of hereditary and acquired forms of PHLH. Physicians are incorporating antagonists in combination regimens to reduce overall therapy burden. Research initiatives are focused on improving safety profiles and minimizing adverse reactions. Growing patient preference for home-based and outpatient administration fuels market expansion. The segment benefits from inclusion in updated clinical guidelines and insurance coverage for rare diseases. Continuous clinical studies support real-world efficacy and safety data. Educational programs for clinicians increase confidence in prescribing. Broader accessibility through specialty and online pharmacies further accelerates adoption. The antagonists’ ability to complement standard therapies enhances treatment flexibility. Overall, the segment’s targeted mechanism and patient-centric approach drive robust CAGR growth.

- By Route of Administration

On the basis of route of administration, the market is segmented into Oral and Parenteral. The Parenteral segment dominated the largest market revenue share of 71.3% in 2025, owing to its precise dosing, rapid therapeutic effect, and suitability for hospital-based management of complex PHLH cases. Parenteral administration is preferred for biologics, monoclonal antibodies, and immunotherapies that require controlled infusion and professional monitoring. Hospitals and specialty clinics are the primary settings for administration due to the need for continuous patient observation and management of adverse events. Parenteral therapies ensure faster onset of action, critical in acute PHLH episodes. They allow clinicians to tailor dosages according to patient weight, severity, and response. Pediatric and adult patients both benefit from the safety and predictability of this route. In addition, parenteral administration supports combination therapy strategies, enhancing efficacy while minimizing systemic toxicity. Availability of trained healthcare personnel, infusion centers, and monitoring equipment further reinforces market dominance. Pharmaceutical investments continue to improve formulations and delivery systems, boosting adoption. Standardized treatment protocols and hospital-based insurance coverage facilitate wider access. The route remains the backbone for treating severe PHLH manifestations effectively.

The Oral segment is expected to witness the fastest CAGR of 12.5% from 2026 to 2033, driven by increasing patient preference for convenient home-based treatment options and advancements in oral immune-modulating therapies. Oral formulations allow easier long-term management and improve adherence in both pediatric and adult populations. Clinicians are gradually incorporating oral therapy as part of combination regimens to reduce hospital visits and healthcare costs. Pharmaceutical innovations focus on enhancing bioavailability, reducing dosing frequency, and minimizing gastrointestinal side effects. The convenience of self-administration and reduced need for trained personnel are key growth drivers. Growing awareness among patients and caregivers about at-home treatment feasibility is accelerating adoption. Improved regulatory approvals and guideline inclusion support broader clinical use. Integration of oral therapies in homecare programs contributes to the trend. Availability through specialty pharmacies and online distribution channels increases access. Oral therapy adoption is further encouraged by patient education initiatives and telemedicine support. Rising demand for chronic disease management solutions reinforces market expansion. The route’s potential to reduce healthcare burden while maintaining efficacy ensures sustained CAGR growth.

- By End-Users

On the basis of end-users, the market is segmented into Hospitals, Homecare, Specialty Clinics, Oncologists, Immunologists, and Others. The Hospitals segment accounted for the largest market revenue share of 53.8% in 2025, driven by their ability to manage complex PHLH cases requiring multi-disciplinary care. Hospitals provide integrated diagnostics, therapy initiation, continuous monitoring, and emergency management, which are critical for patient survival. Hospital-based management allows access to trained clinicians, advanced laboratory facilities, and infusion centers necessary for parenteral therapies. Multi-specialty teams coordinate immunotherapy, targeted therapy, and supportive care for optimal outcomes. Pediatric and adult patients benefit from structured treatment protocols and evidence-based care pathways. Insurance coverage and government programs typically favor hospital-based treatment, supporting market dominance. Continuous research collaborations and clinical trials conducted in hospitals reinforce adoption. Availability of comprehensive patient support services, including counseling, follow-up, and education, improves compliance. Hospitals also facilitate participation in novel therapy programs, expanding access to innovative treatments. Centralized record-keeping ensures accurate patient monitoring and data collection. Overall, hospitals remain the primary point of care for PHLH due to the combination of expertise, infrastructure, and integrated services.

The Homecare segment is expected to witness the fastest CAGR of 13.1% from 2026 to 2033, fueled by the rise of outpatient management trends, increased availability of oral therapies, and simplified parenteral regimens suitable for home administration. Homecare adoption is supported by telemedicine, caregiver training programs, and remote monitoring technologies. Patients and caregivers increasingly prefer home-based care due to convenience, reduced hospital visits, and improved quality of life. Oral and self-administered parenteral therapies are expanding the feasibility of homecare. Healthcare providers are developing structured protocols to safely manage patients in non-hospital settings. Government and private programs supporting rare disease management are further boosting adoption. Homecare allows flexibility in dosing schedules and monitoring, enhancing adherence. Integration with home infusion services ensures patient safety. The growing demand for patient-centric care models accelerates growth. Continuous education for caregivers and virtual follow-ups reinforce home-based management. Improved access to medications through specialty and online pharmacies supports market expansion. Overall, homecare’s growth reflects the trend toward decentralized, patient-friendly treatment approaches.

Primary Haemophagocytic Lymphohistiocytosis Market Regional Analysis

- North America dominated the primary haemophagocytic lymphohistiocytosis market with the largest revenue share of 42.5% in 2025

- Driven by well-established healthcare infrastructure, high healthcare spending, and the presence of leading biopharmaceutical companies. The region benefits from advanced diagnostic programs, expanded newborn screening initiatives, and widespread clinical adoption of enzyme replacement and immunotherapy programs, which together contribute to robust market growth

- Consumers and healthcare providers in North America are increasingly prioritizing early diagnosis and comprehensive management of HLH. The rising awareness of rare genetic disorders, strong reimbursement policies, and high adoption of advanced therapeutics further support the region’s market dominance

U.S. Primary Haemophagocytic Lymphohistiocytosis Market Insight

The U.S. primary haemophagocytic lymphohistiocytosis market captured the largest revenue share in 2025 within North America, fueled by extensive clinical adoption of enzyme replacement therapies, immunotherapy programs, and newborn screening initiatives. The country is witnessing significant growth due to specialized HLH treatment centers, increasing investment in rare disease research, and improved access to advanced therapies for pediatric and adult patients. Supportive government policies and strong R&D pipelines of leading biopharmaceutical companies further propel market expansion.

Europe Primary Haemophagocytic Lymphohistiocytosis Market Insight

The Europe primary haemophagocytic lymphohistiocytosis market is projected to expand at a substantial CAGR of 12.8% from 2026 to 2033, driven by improved awareness of rare genetic disorders, growing investments in healthcare infrastructure, and increasing adoption of enzyme replacement and immunotherapy programs. Countries such as Germany, France, and the U.K. are witnessing higher demand for specialized HLH treatments in hospitals and specialty clinics.

U.K. Primary Haemophagocytic Lymphohistiocytosis Market Insight

The U.K. primary haemophagocytic lymphohistiocytosis market is expected to grow at a notable CAGR of 13.2% during the forecast period, propelled by enhanced pediatric and adult HLH care programs, rising awareness among healthcare professionals, and the expansion of outpatient treatment initiatives. Government support for rare disease management and increased patient access to advanced therapies are key growth drivers.

Germany Primary Haemophagocytic Lymphohistiocytosis Market Insight

Germany primary haemophagocytic lymphohistiocytosis market is projected to expand at a CAGR of 12.5% during 2026–2033, supported by robust healthcare infrastructure, widespread clinical adoption of HLH treatment protocols, and investments in research and development. Hospitals and specialty clinics are increasingly offering enzyme replacement therapy, immunotherapies, and targeted therapeutic programs, boosting market demand.

Asia-Pacific Primary Haemophagocytic Lymphohistiocytosis Market Insight

The Asia-Pacific primary haemophagocytic lymphohistiocytosis market is expected to be the fastest-growing region with a CAGR of 16.0% from 2026 to 2033, driven by healthcare modernization, rising awareness of rare genetic disorders, expanding HLH treatment centers, and improving access to specialized therapies in countries such as Japan, China, and India. Increasing government support, rising healthcare spending, and growing pediatric and adult patient populations are further fueling growth.

Japan Primary Haemophagocytic Lymphohistiocytosis Market Insight

Japan’s primary haemophagocytic lymphohistiocytosis market is gaining momentum due to high healthcare standards, a growing focus on rare disease management, and increasing adoption of enzyme replacement and immunotherapy programs. The availability of advanced diagnostic programs and specialized HLH centers supports the market’s CAGR of 15.2% during 2026–2033.

China Primary Haemophagocytic Lymphohistiocytosis Market Insight

China primary haemophagocytic lymphohistiocytosis market accounted for the largest market revenue share in the Asia-Pacific region in 2025, driven by expanding healthcare infrastructure, rising awareness of rare genetic disorders, and increasing access to enzyme replacement and targeted therapies. Growing pediatric and adult HLH treatment centers, government initiatives for rare disease management, and investment by domestic and multinational pharmaceutical companies are key growth factors. The market is expected to grow at a CAGR of 16.8% from 2026 to 2033.

Primary Haemophagocytic Lymphohistiocytosis Market Share

The Primary Haemophagocytic Lymphohistiocytosis industry is primarily led by well-established companies, including:

- Roche (Switzerland)

- Sobi (Sweden)

- Hemogenyx Pharmaceuticals (U.S.)

- Novartis (Switzerland)

- BioCryst Pharmaceuticals (U.S.)

- Genentech (U.S.)

- Argenx (Belgium)

- Pfizer (U.S.)

- Catalent (U.S.)

- Horizon Therapeutics (U.S.)

- Lundbeck (Denmark)

- Alexion Pharmaceuticals (U.S.)

- Amgen (U.S.)

- Moderna (U.S.)

- CureVac (Germany)

- Novavax (U.S.)

Latest Developments in Global Primary Haemophagocytic Lymphohistiocytosis Market

- In February 2022, Sobi announced that China’s regulatory authorities recommended the approval of Gamifant (emapalumab‑lzsg) for the treatment of primary HLH. This marked a significant milestone for the company, enabling access to the Chinese market and offering a vital therapeutic option for patients with this rare and life-threatening disorder. The recommendation highlighted the increasing global recognition of targeted therapies for HLH and underscored efforts to expand access to innovative treatments in emerging markets

- In June 2025, the U.S. FDA approved Gamifant (emapalumab‑lzsg) for the treatment of macrophage activation syndrome (MAS) in Still’s disease, a condition closely related to HLH. This approval expanded the therapeutic indications of Gamifant beyond primary HLH, reflecting its efficacy in managing severe immune dysregulation. The development strengthened treatment options for patients, particularly those with rare inflammatory disorders, and demonstrated the ongoing progress in the development and clinical adoption of targeted therapies for HLH and related syndromes

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.