Global Primary Lymphedema Treatment Market

Market Size in USD Million

USD

220.88 Million

USD

455.86 Million

2025

2033

USD

220.88 Million

USD

455.86 Million

2025

2033

| 2026 - 2033 | |

| USD 220.88 Million | |

| USD 455.86 Million | |

| % | |

|

Primary Lymphedema Treatment Market Size

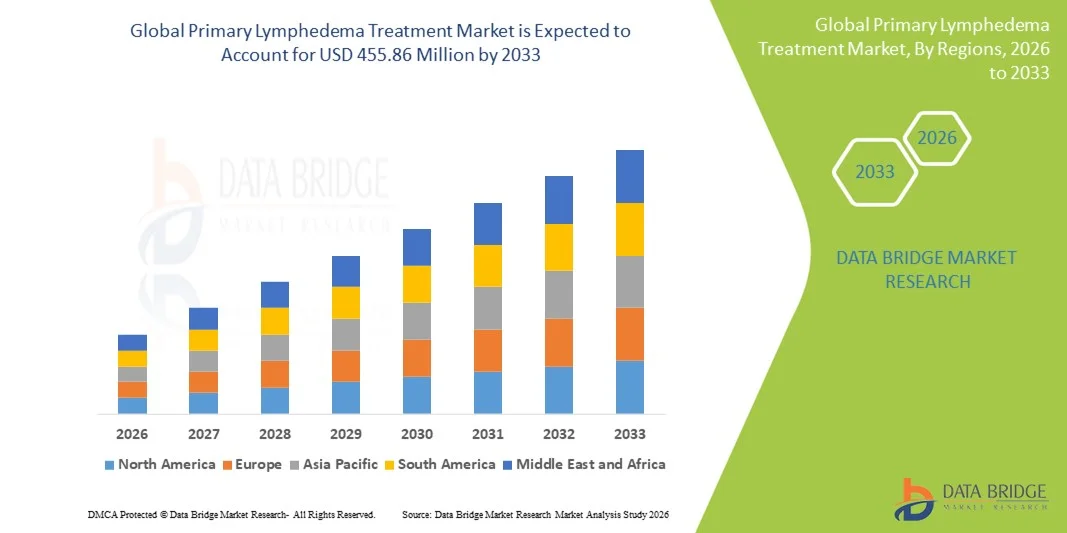

- The global primary lymphedema treatment market size was valued at USD 220.88 Million in 2025 and is expected to reach USD 455.86 Million by 2033, at a CAGR of 9.48% during the forecast period

- The market growth is largely fueled by the increasing prevalence of lymphatic disorders, rising awareness about early diagnosis and management, and technological advancements in treatment options, leading to improved patient outcomes in both clinical and homecare settings

- Furthermore, growing patient demand for effective, minimally invasive, and integrated therapeutic solutions is driving the adoption of Primary Lymphedema Treatment solutions, thereby significantly boosting the industry's growth

Primary Lymphedema Treatment Market Analysis

- Primary lymphedema treatments, offering therapeutic interventions for lymphatic system disorders, are increasingly vital in both clinical and homecare settings due to their ability to improve patient mobility, reduce swelling, and prevent complications

- The escalating demand for primary lymphedema treatment is primarily fueled by rising prevalence of lymphatic disorders, growing awareness among patients and healthcare providers, and increasing adoption of advanced therapeutic techniques and devices

- North America dominated the primary lymphedema treatment market with the largest revenue share of 44.45% in 2025, characterized by strong healthcare infrastructure, high awareness of lymphatic disorders, and the presence of key pharmaceutical and medical device companies, with the U.S. contributing the majority of this share due to proactive healthcare policies and growing patient adoption of advanced therapies

- Asia-Pacific is expected to be the fastest growing region in the Primary Lymphedema Treatment market during the forecast period, registering a CAGR from 2026 to 2033, driven by rising healthcare expenditure, increasing prevalence of lymphatic disorders, expanding healthcare facilities, and growing awareness of treatment options in countries such as China, India, and Japan

- The Adult segment held the largest revenue share of 54.6% in 2025, due to a higher prevalence of primary lymphedema among adults, including lifestyle- and hereditary-related factors

Report Scope and Primary Lymphedema Treatment Market Segmentation

|

Attributes |

Primary Lymphedema Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Cardinal Health (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Primary Lymphedema Treatment Market Trends

Growing Adoption of Minimally Invasive and Targeted Therapies

- A significant trend in the global primary lymphedema treatment market is the increasing adoption of minimally invasive therapies and targeted treatment approaches that improve patient outcomes while reducing recovery time

- For instance, in June 2023, the National Lymphedema Network highlighted successful outcomes of pneumatic compression therapy in early-stage patients, encouraging wider clinical adoption

- Patients and healthcare providers are increasingly favoring techniques such as manual lymphatic drainage, pneumatic compression devices, and targeted pharmacological interventions for early-stage lymphedema management

- These modern approaches are supported by advancements in diagnostic imaging and lymphatic mapping, enabling more precise and personalized treatment plans

- The trend also reflects rising awareness among patients about non-surgical management options and home-based treatment devices, contributing to enhanced patient compliance and quality of life

- Moreover, integration of physiotherapy programs and advanced compression therapy is enabling more holistic care for primary lymphedema patients

- Healthcare providers are actively investing in patient education programs to encourage early intervention and consistent management, driving adoption of comprehensive treatment protocol

- The shift toward patient-centric treatment solutions is reshaping clinical practices, emphasizing outcomes, comfort, and long-term disease management

Primary Lymphedema Treatment Market Dynamics

Driver

Rising Prevalence of Lymphedema and Growing Healthcare Awareness

- The increasing prevalence of primary lymphedema globally is a key driver for market growth. Factors such as genetic predisposition, aging populations, and rising obesity rates contribute to higher incidence rates

- In addition, growing awareness of the disease among healthcare professionals and patients is resulting in earlier diagnosis and more proactive management

- For instance, in March 2024, a global clinical consortium published new guidelines for early detection and management of primary lymphedema, emphasizing standardized care pathways and preventive strategies

- The availability of reimbursement support and insurance coverage for lymphedema therapies in key markets is further enabling access to treatment

- Research and clinical trials focused on novel pharmacological agents and lymphatic-targeted therapies are expanding the treatment landscape, boosting adoption rates

- Increased hospital infrastructure, lymphatic clinics, and specialized care centers in emerging regions also support market expansion

- Patient support programs and awareness campaigns by healthcare organizations are encouraging timely intervention and consistent follow-up care, which is expected to propel market growth in the forecast period

Restraint/Challenge

High Treatment Costs and Limited Accessibility in Emerging Regions

- The relatively high cost of advanced primary lymphedema therapies, including compression garments, pneumatic devices, and pharmacological interventions, poses a challenge to widespread adoption, particularly in price-sensitive markets

- For instance, patients in low-income regions often face limited access to specialized clinics and trained healthcare professionals, constraining treatment availability

- Addressing these challenges requires the development of cost-effective treatment solutions, local manufacturing of compression and medical devices, and expansion of healthcare infrastructure

- Awareness campaigns and patient education initiatives are necessary to overcome barriers related to delayed diagnosis and inadequate self-management practices

- While gradual reduction in device costs and therapy packages is observed, perceived treatment affordability remains a concern for a significant portion of the target population

- Overcoming these barriers through government initiatives, public-private partnerships, and innovative delivery models will be vital for sustaining market growth

Primary Lymphedema Treatment Market Scope

The market is segmented on the basis of treatment type, age group, and end-user.

- By Treatment Type

On the basis of treatment type, the Primary Lymphedema Treatment market is segmented into Compression Therapy, Manual Lymphatic Drainage, Pneumatic Compression Devices, Surgical Interventions, and Pharmacological Treatments. The Compression Therapy segment dominated the market with the largest revenue share of 42.8% in 2025, driven by its non-invasive nature, well-established clinical efficacy, and recommendation by physicians worldwide. Patients prefer compression therapy due to its ability to reduce swelling, improve lymphatic flow, and enhance quality of life without requiring surgical interventions. The availability of advanced compression garments in various sizes and pressure classes further supports adoption. Hospitals and clinics widely recommend compression therapy as a first-line intervention. Rising awareness programs and insurance coverage for compression devices in developed countries also contribute to market dominance. Patient compliance is high due to ease of use and minimal side effects. The segment benefits from increasing global lymphedema prevalence, especially among adults and geriatrics. Growing demand for home-based therapy kits and telehealth support drives continuous revenue growth. Technological innovations such as adjustable and wearable compression systems further strengthen adoption.

The Pneumatic Compression Devices segment is expected to witness the fastest CAGR of 20.3% from 2026 to 2033, fueled by technological advancements in automated, portable, and home-use devices. Pneumatic devices offer controlled lymphatic drainage and improved patient adherence, making them ideal for adult and geriatric populations. The integration of app-controlled and Bluetooth-enabled devices supports real-time monitoring and therapy customization. Rising awareness of early intervention benefits and the growing adoption of home-based therapy contribute to rapid growth. Hospitals, clinics, and home-care providers increasingly recommend these devices for both primary and secondary lymphedema management. The segment is further driven by government initiatives promoting chronic disease management and reimbursement support. Increased research on device efficacy and patient safety boosts confidence among medical professionals. The market sees growing investments from manufacturers to enhance portability and ease of use.

- By Age Group

On the basis of age group, the market is segmented into Pediatric, Adult, and Geriatric populations. The Adult segment held the largest revenue share of 54.6% in 2025, due to a higher prevalence of primary lymphedema among adults, including lifestyle- and hereditary-related factors. Adults have access to a broader range of treatment options such as compression therapy, pneumatic devices, and manual lymphatic drainage. Awareness programs and physician-led interventions targeting adults contribute to sustained market dominance. Adoption is further supported by employer wellness programs and insurance coverage. Adults also seek long-term management options to prevent disease progression. The segment benefits from increasing disposable income in developed regions. Healthcare providers focus on preventive care and patient education for adults. The rise of home-based therapy kits for adults supports convenience and compliance. Clinical studies highlighting treatment efficacy further reinforce segment preference.

The Geriatric segment is projected to witness the fastest CAGR of 18.7% from 2026 to 2033, driven by the growing elderly population globally and age-related lymphatic deterioration. Geriatric patients benefit from non-invasive and home-use treatments that allow independent care. Increased awareness of early diagnosis and preventive therapy drives rapid adoption. Portable pneumatic compression devices and user-friendly garments enhance compliance in older populations. The expansion of home-care services in emerging markets supports growth. Government health programs targeting elderly populations promote lymphedema management. Adoption of telehealth and virtual consultation services enhances access. Clinical guidelines recommend proactive intervention for elderly patients. Insurance coverage for geriatric therapies is expanding. The rising focus on improving quality of life for older adults fuels demand.

- By End-User

On the basis of end-user, the market is segmented into Hospitals, Clinics, Home Care, and Rehabilitation Centers. The Hospitals segment dominated with the largest revenue share of 48.3% in 2025, due to the availability of comprehensive treatment services, advanced diagnostic facilities, and specialized clinical staff. Hospitals are preferred for severe cases requiring a combination of therapies, surgical interventions, and continuous monitoring. Expansion of hospital networks in emerging economies supports market dominance. Patients trust hospitals for effective treatment outcomes and multidisciplinary care. Hospitals also benefit from insurance reimbursements for advanced therapies. Integration of rehabilitation units in hospitals strengthens patient adherence. Awareness campaigns and early detection programs drive hospital adoption. Hospitals often serve as referral centers for home-care therapy. Clinical trials and research activities conducted in hospitals further promote treatment adoption. The segment maintains robust revenue due to growing global lymphedema prevalence.

The Home Care segment is expected to witness the fastest CAGR of 21% from 2026 to 2033, driven by the rising preference for home-based therapy, portability of pneumatic devices, and convenience of self-administered treatment. Home care allows flexible scheduling, reduces hospital visits, and enhances patient comfort. Telehealth integration supports monitoring and virtual guidance for patients. Home-care adoption is fueled by increasing patient awareness, supportive government initiatives, and reimbursement policies. The segment sees rapid growth among adult and geriatric populations. Technological advancements in wearable devices and user-friendly kits improve compliance. Manufacturers are introducing easy-to-use home therapy solutions with adjustable compression. The growing focus on preventive care and early intervention further boosts demand. Home care provides cost-effective and convenient treatment options for long-term lymphedema management.

Primary Lymphedema Treatment Market Regional Analysis

- North America dominated the primary lymphedema treatment market with the largest revenue share of 44.45% in 2025

- Characterized by strong healthcare infrastructure, high awareness of lymphatic disorders, and the presence of key pharmaceutical and medical device companies

- The market contributing the majority of this share due to proactive healthcare policies and growing patient adoption of advanced therapies

U.S. Primary Lymphedema Treatment Market Insight

The U.S. primary lymphedema treatment market captured the largest revenue share in North America in 2025, supported by the adoption of advanced therapeutic options, availability of specialized clinics, and increasing awareness programs targeting both patients and healthcare providers. Rising reimbursement coverage for lymphedema therapies and innovative medical devices further propel market growth.

Europe Primary Lymphedema Treatment Market Insight

The Europe primary lymphedema treatment market is projected to expand at a substantial CAGR throughout the forecast period, driven by strong regulatory frameworks for patient care, government-led awareness campaigns, and technological advancements in treatment options. Increasing investments in healthcare infrastructure across countries such as Germany, the U.K., and France support the adoption of advanced lymphedema therapies.

U.K. Primary Lymphedema Treatment Market Insight

The U.K. primary lymphedema treatment market is anticipated to grow steadily, driven by increasing incidence of lymphatic disorders, growing awareness about early treatment, and the presence of specialized healthcare facilities offering advanced therapies. Strong public and private healthcare initiatives also encourage patient adoption.

Germany Primary Lymphedema Treatment Market Insight

Germany’s primary lymphedema treatment market is expected to expand at a significant CAGR, fueled by well-established healthcare systems, high patient awareness, and continuous development of innovative therapies and medical devices. The emphasis on preventive care and rehabilitation programs further supports market growth.

Asia-Pacific Primary Lymphedema Treatment Market Insight

The Asia-Pacific primary lymphedema treatment market is poised to grow at the fastest CAGR during 2026–2033, driven by rising healthcare expenditure, increasing prevalence of lymphedema, expansion of specialized clinics, and growing awareness about early intervention in countries such as China, India, and Japan. Government initiatives promoting healthcare accessibility also contribute to market expansion.

Japan Primary Lymphedema Treatment Market Insight

The Japan primary lymphedema treatment market is gaining momentum due to the aging population, high healthcare spending, and growing emphasis on rehabilitation services. Advanced therapies and increased patient awareness are driving adoption in both residential and hospital-based treatment centers.

China Primary Lymphedema Treatment Market Insight

China primary lymphedema treatment market accounted for the largest revenue share in Asia-Pacific in 2025, driven by rising incidence of lymphatic disorders, government initiatives for healthcare improvement, rapid urbanization, and expanding access to advanced therapies and specialized healthcare facilities.

Primary Lymphedema Treatment Market Share

The Primary Lymphedema Treatment industry is primarily led by well-established companies, including:

• Cardinal Health (U.S.)

• Mölnlycke Health Care (Sweden)

• Huntleigh Healthcare (U.K.)

• ConvaTec (U.S.)

• Kinetic Concepts (U.S.)

• BSN Medical (Germany)

• Hy-Tape (U.S.)

• Medline Industries (U.S.)

• Smith & Nephew (U.K.)

• 3M Healthcare (U.S.)

• CooperSurgical (U.S.)

• Blount International (U.S.)

• Velcro Companies (U.S.)

• Alloga Healthcare (U.S.)

• Braun Melsungen (Germany)

• BD (Becton, Dickinson and Company) (U.S.)

• Hartmann Group (Germany)

• Swing Medical (U.K.)

• Coloplast (Denmark)

Latest Developments in Global Primary Lymphedema Treatment Market

- In October 2022, Koya Medical announced the U.S. commercial availability of its “Dayspring” active dynamic compression system for lymphedema and venous diseases of the lower extremities — the first non‑pneumatic active compression therapy cleared by the FDA. This represents a shift toward more active, patient‑friendly therapies, potentially increasing compliance and expanding treatment options beyond traditional static compression garments

- In April 2023, AIROS Medical, Inc. received U.S. FDA clearance to market a new peristaltic pneumatic compression device (with truncal garments) for lymphedema treatment. This approval marks a significant innovation: by combining pneumatic compression with trunk‑level support garments, AIROS’s device could improve fluid drainage more effectively than standard limb‑only compression, potentially enhancing patient outcomes

- In May 2025, Institute for Advanced Reconstruction (IFAR), in conjunction with a research partner, launched a first‑of‑its‑kind prospective study investigating whether GLP‑1 receptor agonists (commonly used for diabetes and weight‑loss) can be repurposed to treat lymphedema. Given the lack of approved pharmacological treatments for primary lymphedema, this trial — if successful — could represent a breakthrough toward drug‑based therapy beyond compression

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.