Global Prostate Cancer Nuclear Medicine Diagnostics Market

Market Size in USD Million

USD

605.78 Million

USD

1,468.04 Million

2025

2033

USD

605.78 Million

USD

1,468.04 Million

2025

2033

| 2026 - 2033 | |

| USD 605.78 Million | |

| USD 1,468.04 Million | |

| % | |

|

Prostate Cancer Nuclear Medicine Diagnostics Market Overview

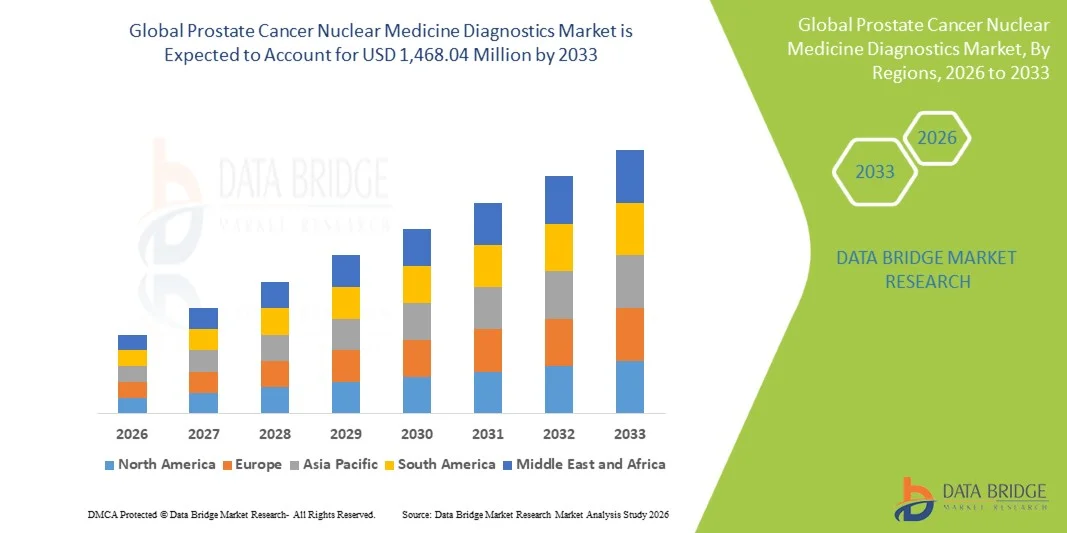

The Prostate Cancer Nuclear Medicine Diagnostics Market was valued at USD 605.78 million in 2025 and is projected to reach USD 1,468.04 million by 2033, growing at a CAGR of 11.70% from 2026 to 2033. The market is witnessing steady expansion driven by the rising global prevalence of prostate cancer, increasing adoption of PET/CT and PET/MRI imaging modalities, and growing clinical preference for early and precise molecular-level diagnosis. Advancements in radiotracers such as PSMA-targeted imaging agents are further enhancing diagnostic accuracy and transforming disease staging and treatment planning.

The increasing burden of prostate cancer in aging male populations, along with improved healthcare infrastructure and expanding access to nuclear imaging facilities, is significantly boosting market adoption. In addition, strong clinical validation of PSMA PET imaging in detecting recurrent and metastatic prostate cancer is encouraging wider regulatory approvals and integration into oncology guidelines. Growing investments in nuclear medicine infrastructure and the shift toward personalized oncology diagnostics are also accelerating the use of advanced imaging techniques across hospitals and specialized cancer centers globally.

Key Market Trends & Insights

- North America dominated the Prostate Cancer Nuclear Medicine Diagnostics Market with the largest revenue share of 38.92% in 2025, supported by high prostate cancer prevalence, advanced PET imaging infrastructure, and strong reimbursement frameworks for nuclear medicine procedures.

- The Positron Emission Computed Tomography (PET) segment led the market with a 72.6% share in 2025, driven by its superior diagnostic accuracy, higher sensitivity, and ability to detect prostate cancer at an early molecular stage

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.1% from 2026 to 2033, fueled by rising cancer incidence, improving healthcare access, and expanding investments in nuclear imaging facilities across China, India, and Japan.

- Single Photon Emission Computed Tomography (SPECT) are the fastest-growing simulation type, projected to register a CAGR of 7.1%, reflecting the surge in its relatively lower cost and wider accessibility in resource-constrained healthcare systems

- The Ga-68 PSMA segment dominated the product category with a 48.3% revenue share in 2025, led by its high diagnostic accuracy, strong tumor specificity, and excellent ability to detect prostate cancer lesions even at low PSA levels.

- Hospital accounted for 64.1% of the market, preferred by high patient inflow, availability of advanced PET/CT and PET/MRI systems, and strong integration of nuclear medicine into oncology care pathways.

- The F-18 segment is the fastest-growing product category, with a CAGR of 8.9%, driven by its longer half-life, superior image quality, and ability to support centralized production and wider distribution networks.

Market Size & Forecast

- Global Market Value (2025): USD 605.78 Million

- Expected Market Value (2033): USD 1,468.04 Million

- Forecast CAGR (2026–2033): 11.70%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Prostate Cancer Nuclear Medicine Diagnostics Market Segmentation

|

Attributes |

Prostate Cancer Nuclear Medicine Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Siemens Healthineers AG (Germany) · GE HealthCare (U.S.) · Koninklijke Philips N.V. (Netherlands) · CANON MEDICAL SYSTEMS CORPORATION (Japan) · Bracco Imaging S.p.A. (Italy) · Bayer AG (Germany) · Novartis AG (Switzerland) · Lantheus Holdings, Inc. (U.S.) · Telix Pharmaceuticals Limited (Australia) · Curium Pharma (France) · Eckert & Ziegler SE (Germany) · Nordic Nanovector ASA (Norway) · ITM Isotope Technologies Munich SE (Germany) · Blue Earth Diagnostics Ltd (U.K.) · Advanced Accelerator Applications (France) · Cardinal Health, Inc. (U.S.) · Nihon Medi-Physics Co., Ltd. (Japan) · SOFIE Biosciences (U.S.) |

|

Market Opportunities |

· Rapid expansion of PSMA-targeted PET tracers · Growing adoption of hybrid PET/MRI systems in oncology centers · Rising investment in cyclotron infrastructure and local radiotracer production |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Prostate Cancer Nuclear Medicine Diagnostics Market Trends

Trend: Expansion of PSMA PET Imaging in Clinical Oncology

PSMA-targeted PET imaging is rapidly becoming a core standard in prostate cancer diagnosis due to its superior ability to detect both primary tumors and metastatic lesions at an early stage. Compared to conventional CT and bone scans, PSMA PET provides significantly higher accuracy, leading to better staging precision and improved treatment planning in oncology practice. Hospitals and cancer centers are increasingly embedding PSMA-based imaging into routine diagnostic workflows, especially for high-risk and recurrent prostate cancer cases.

For instance, the growing clinical adoption of radiotracers such as Gallium-68 PSMA-11 and Fluorine-18 DCFPyL across North America and Europe demonstrates how nuclear medicine is shifting toward highly targeted molecular imaging, improving detection rates even at low PSA levels and enabling earlier therapeutic intervention decisions.

Prostate Cancer Nuclear Medicine Diagnostics Market Dynamics

Key Market Driver: Rising Demand for Early and Precise Cancer Detection

The increasing global incidence of prostate cancer, particularly among aging male populations, is driving strong demand for highly accurate and non-invasive diagnostic solutions. Nuclear medicine techniques such as PET/CT and PET/MRI are gaining preference because they allow clinicians to visualize tumor biology at the molecular level rather than relying only on anatomical changes. This improves early detection, staging accuracy, and treatment monitoring.

For instance, PSMA PET imaging is increasingly being used in patients with biochemical recurrence after prostatectomy or radiation therapy, enabling clinicians to detect microscopic metastatic disease that traditional imaging often fails to identify, thereby significantly improving patient management outcomes and personalized treatment planning.

Key Restraint/Challenge: High Cost and Limited Accessibility of Advanced Imaging

Despite strong clinical benefits, the adoption of prostate cancer nuclear medicine diagnostics is constrained by high capital and operational costs. PET/CT and PET/MRI systems require substantial investment, along with expensive radiotracers, cyclotron facilities, and specialized infrastructure for radiopharmaceutical handling. These cost barriers limit adoption in smaller hospitals and emerging healthcare systems.

For instance, in many developing countries across Asia, Africa, and parts of Latin America, limited availability of PSMA PET scanners and centralized radiotracer production leads to long waiting times, high out-of-pocket expenses for patients, and reduced access to advanced diagnostic imaging, slowing overall market penetration despite rising disease burden.

Key Market Opportunity: Expansion of Radiopharmaceutical Production and Distribution Networks

The growing development of localized radiopharmaceutical manufacturing and distribution infrastructure presents a major opportunity for market expansion. Since most PET tracers have short half-lives, efficient regional production and supply chains are essential to ensure timely diagnostic imaging. Investments in cyclotrons, automated synthesis units, and hospital-based radiopharmacies are improving accessibility and reducing dependency on imports.

For instance, increasing establishment of regional PSMA tracer production centers in Europe and Asia-Pacific is enabling same-day or next-day scan availability, reducing logistical delays, lowering costs, and significantly improving access to advanced prostate cancer diagnostics in both urban and semi-urban healthcare facilities.

Prostate Cancer Nuclear Medicine Diagnostics Market Scope

The prostate cancer nuclear medicine diagnostics market is segmented on the basis of type, product, and application

- By Type

On the basis of type, the Prostate Cancer Nuclear Medicine Diagnostics Market is segmented into Single Photon Emission Computed Tomography (SPECT) and Positron Emission Computed Tomography (PET). The PET segment dominated the market with a 72.6% share in 2025, driven by its superior sensitivity, higher spatial resolution, and strong ability to detect early metastatic and recurrent prostate cancer. PET imaging provides functional and molecular-level insights that significantly improve staging accuracy compared to SPECT. Its widespread integration with CT and MRI systems enhances diagnostic precision and clinical workflow efficiency. Increasing adoption of PSMA PET tracers has further strengthened its clinical relevance in oncology. Strong guideline support and reimbursement coverage in developed markets are also reinforcing its dominance. Continuous technological advancements in hybrid imaging systems are further expanding its utilization across hospitals and diagnostic centers.

The SPECT segment is the fastest-growing, registering a CAGR of 7.1% from 2026 to 2033, driven by its relatively lower cost and wider accessibility in resource-constrained healthcare systems. SPECT remains widely used for basic bone scans in prostate cancer patients, particularly in regions where PET infrastructure is limited. Continuous improvements in SPECT imaging resolution and hybrid SPECT/CT systems are enhancing diagnostic performance. Expanding healthcare infrastructure in emerging economies is supporting adoption. Increasing demand for cost-effective diagnostic alternatives is also contributing to growth. In addition, SPECT remains an important entry-level nuclear imaging modality in many secondary hospitals, sustaining its rapid expansion in developing regions.

- By Product

On the basis of product, the market is segmented into F-18, C-11, and Ga-68 PSMA radiotracers. The Ga-68 PSMA segment dominated the market with a 48.3% share in 2025, owing to its high diagnostic accuracy, strong tumor specificity, and excellent ability to detect prostate cancer lesions even at low PSA levels. Its generator-based production allows on-site availability without requiring cyclotrons, making it highly practical for hospital-based imaging centers. Widespread clinical adoption across Europe and North America further supports its leadership position. Inclusion in major oncology guidelines and strong regulatory approvals have reinforced its standard use in PSMA PET imaging. Its efficiency in improving staging and recurrence detection outcomes makes it highly preferred in clinical practice. Continuous expansion of PSMA-based diagnostic protocols is further strengthening its dominance in nuclear medicine workflows.

The F-18 segment is the fastest-growing, with a CAGR of 8.9% from 2026 to 2033, driven by its longer half-life, superior image quality, and ability to support centralized production and wider distribution networks. F-18-labeled PSMA tracers allow large-scale commercial distribution, making them highly suitable for regions with limited radiopharmacy infrastructure. Increasing adoption of F-18 PSMA PET imaging in North America and Asia-Pacific is accelerating growth. Strong clinical performance in detecting both primary and metastatic prostate cancer is boosting physician preference. Expanding investments in cyclotron facilities and radiotracer manufacturing are further supporting adoption. In addition, improved logistics and broader accessibility compared to Ga-68 are making F-18 tracers a key growth driver in global nuclear medicine diagnostics.

- By Application

On the basis of application, the market is segmented into Hospitals, Clinics, and Others (diagnostic imaging centers, research institutes, and academic centers). The Hospital segment dominated the market with a 64.1% share in 2025, driven by high patient inflow, availability of advanced PET/CT and PET/MRI systems, and strong integration of nuclear medicine into oncology care pathways. Hospitals serve as primary centers for complex prostate cancer diagnosis, staging, and treatment planning. Presence of multidisciplinary cancer care teams improves clinical decision-making and diagnostic accuracy. Favorable reimbursement systems in developed regions further strengthen hospital-based adoption. Continuous investment in advanced imaging infrastructure is enhancing operational efficiency. Hospitals also benefit from established radiopharmaceutical supply chains and trained nuclear medicine specialists. Their role as referral hubs ensures consistent diagnostic volumes across regions.

The “Others” segment (diagnostic imaging centers and research institutes) is the fastest-growing, with a CAGR of 8.5% from 2026 to 2033, driven by increasing decentralization of advanced imaging services and rising demand for outpatient diagnostic facilities. Independent imaging centers are expanding access to PSMA PET scans, particularly in regions with limited hospital capacity. Research institutes are increasingly adopting nuclear imaging for clinical trials and theranostic research applications. Lower waiting times and cost efficiency are attracting a growing number of patients. Expanding collaborations between pharmaceutical companies and academic centers are accelerating innovation in radiopharmaceutical development. Mobile and satellite PET/CT units are improving access in semi-urban and underserved regions. Increasing focus on early cancer detection and personalized medicine is further boosting growth in this segment.

Prostate Cancer Nuclear Medicine Diagnostics Market Regional Analysis

North America dominated the Prostate Cancer Nuclear Medicine Diagnostics Market with the largest revenue share of 38.92% in 2025, supported by high prostate cancer prevalence, advanced PET imaging infrastructure, and strong reimbursement frameworks for nuclear medicine procedures. The region also benefits from early adoption of PSMA PET imaging, strong presence of leading radiopharmaceutical companies, and well-established oncology care networks. Increasing clinical integration of precision diagnostics, growing use of next-generation PSMA tracers, and rising investments in molecular imaging technologies continue to strengthen North America’s leadership position in the global market.

U.S. Prostate Cancer Nuclear Medicine Diagnostics Market Insight

The U.S. prostate cancer nuclear medicine diagnostics market is witnessing strong growth due to high prostate cancer prevalence, advanced PET/CT and PET/MRI infrastructure, and strong reimbursement support for nuclear medicine procedures. The country’s well-established oncology ecosystem, early adoption of PSMA PET imaging, and presence of leading radiopharmaceutical companies are driving demand across hospitals and cancer centers. In addition, growing emphasis on precision oncology, expanding clinical use of next-generation PSMA tracers, and increasing investment in theranostic approaches are accelerating market adoption across diagnostic and research applications.

Europe Prostate Cancer Nuclear Medicine Diagnostics Market Insight

The Europe prostate cancer nuclear medicine diagnostics market remains a major contributor to global revenue, driven by strong healthcare infrastructure, widespread adoption of PSMA PET imaging, and supportive regulatory frameworks for radiopharmaceuticals. The region benefits from advanced nuclear medicine facilities, strong research collaborations, and high integration of molecular imaging into oncology pathways. Increasing investments in next-generation radiotracers, growing use of PET/CT in prostate cancer staging, and strong clinical guideline support continue to enhance market expansion across Europe.

U.K. Prostate Cancer Nuclear Medicine Diagnostics Market Insight

The U.K. prostate cancer nuclear medicine diagnostics market is experiencing steady growth, supported by increasing adoption of PSMA PET imaging in public healthcare systems and rising investment in nuclear medicine infrastructure. Growing demand for early and accurate prostate cancer diagnosis is driving integration of PET/CT into clinical pathways. Furthermore, expansion of radiopharmaceutical production capabilities, strong clinical research activity, and increasing focus on precision diagnostics are positioning the U.K. as a key contributor within the European market.

Germany Prostate Cancer Nuclear Medicine Diagnostics Market Insight

The Germany prostate cancer nuclear medicine diagnostics market is expanding steadily due to strong clinical research capabilities, advanced hospital infrastructure, and high adoption of PET-based imaging technologies. German healthcare institutions are increasingly utilizing PSMA PET for staging, recurrence detection, and therapy monitoring in prostate cancer patients. Continuous investment in radiopharmaceutical innovation, strong collaboration between academic centers and industry players, and growing focus on molecular imaging precision are further driving market growth in Germany.

Asia-Pacific Prostate Cancer Nuclear Medicine Diagnostics Market Insight

The Asia-Pacific prostate cancer nuclear medicine diagnostics market is expected to witness rapid growth, driven by rising prostate cancer incidence, improving healthcare infrastructure, and increasing adoption of advanced imaging technologies across China, India, and Japan. Growing awareness of early cancer detection, expanding nuclear medicine facilities, and rising investments in PET/CT systems are supporting regional market expansion. In addition, increasing government focus on healthcare modernization and growing availability of radiotracers are accelerating adoption across both urban and semi-urban healthcare centers.

Japan Prostate Cancer Nuclear Medicine Diagnostics Market Insight

The Japan prostate cancer nuclear medicine diagnostics market is witnessing consistent growth due to strong technological adoption in healthcare, high-quality imaging infrastructure, and increasing use of PSMA PET imaging in oncology care. Japanese hospitals and research institutes are actively integrating advanced nuclear medicine techniques for early detection and treatment monitoring. In addition, rising focus on precision medicine, strong regulatory support for radiopharmaceuticals, and continuous innovation in imaging technologies are further contributing to market expansion in Japan.

China Prostate Cancer Nuclear Medicine Diagnostics Market Insight

The China prostate cancer nuclear medicine diagnostics market is growing rapidly, driven by increasing prostate cancer incidence, expanding healthcare infrastructure, and rising adoption of PET/CT imaging systems. Strong government investments in oncology care, growing establishment of nuclear medicine departments, and increasing availability of PSMA radiotracers are significantly boosting market demand. In addition, rapid technological advancements, expanding radiopharmaceutical production capabilities, and rising awareness of early cancer detection are positioning China as one of the fastest-growing markets globally.

Prostate Cancer Nuclear Medicine Diagnostics Market Share

The prostate cancer nuclear medicine diagnostics industry is primarily led by well-established companies, including:

- Siemens Healthineers AG (Germany)

- GE HealthCare (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Bracco Imaging S.p.A. (Italy)

- Bayer AG (Germany)

- Novartis AG (Switzerland)

- Lantheus Holdings, Inc. (U.S.)

- Telix Pharmaceuticals Limited (Australia)

- Curium Pharma (France)

- Eckert & Ziegler SE (Germany)

- Nordic Nanovector ASA (Norway)

- ITM Isotope Technologies Munich SE (Germany)

- Blue Earth Diagnostics Ltd (U.K.)

- Advanced Accelerator Applications (France)

- Cardinal Health, Inc. (U.S.)

- Nihon Medi-Physics Co., Ltd. (Japan)

- SOFIE Biosciences (U.S.)

Latest Developments in Prostate Cancer Nuclear Medicine Diagnostics Market

- In January 2025, Novartis received FDA approval for an expanded indication of Pluvicto (Lu-177 PSMA therapy), allowing use in earlier lines of treatment for metastatic castration-resistant prostate cancer patients. This expansion increased the importance of PSMA PET imaging for earlier patient identification and treatment planning. It strengthened the integration of diagnostic and therapeutic nuclear medicine applications in oncology. The development further accelerated demand for PSMA-based imaging workflows in hospitals and cancer centers

- In June 2023, the National Comprehensive Cancer Network (NCCN) updated its prostate cancer clinical guidelines to recommend PSMA PET imaging as a preferred modality for staging and biochemical recurrence assessment. This marked a major clinical shift from conventional CT and bone scan-based diagnostics toward advanced molecular imaging. The update significantly increased physician confidence and adoption of PSMA PET in routine oncology decision-making. It also supported broader reimbursement acceptance across healthcare systems

- In March 2022, Novartis announced FDA approval of Pluvicto (Lu-177 vipivotide tetraxetan), the first targeted radioligand therapy for PSMA-positive metastatic castration-resistant prostate cancer. Although a therapeutic product, it is directly linked with nuclear medicine diagnostics as PSMA PET imaging is required for patient selection. The approval marked a major milestone in theranostics, integrating diagnosis and targeted treatment within nuclear medicine workflows. It significantly increased demand for PSMA PET imaging infrastructure and radiotracer availability

- In December 2021, Telix Pharmaceuticals announced FDA approval of Illuccix (Gallium Ga-68 PSMA-11 kit), enabling preparation of PSMA PET imaging agents for prostate cancer diagnostics. The approval expanded access to generator-based radiotracers, reducing dependency on cyclotron infrastructure and improving availability in nuclear medicine departments. Illuccix played a key role in scaling PSMA PET imaging across multiple clinical settings. The development supported wider adoption of precision oncology diagnostics in both urban and regional healthcare facilities

- In May 2021, Lantheus received U.S. FDA approval for Pylarify (piflufolastat F 18), a PSMA-targeted PET imaging agent for prostate cancer detection. The launch marked a major advancement in nuclear medicine diagnostics by enabling highly accurate identification of prostate cancer lesions in both initial staging and recurrence cases. Pylarify’s F-18 isotope offered a longer half-life, allowing broader distribution and improved accessibility compared to earlier tracers. Its approval significantly accelerated the shift toward molecular imaging in routine oncology practice. The development strengthened PSMA PET adoption across hospitals and imaging centers in the United States

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.