Global Pseudobulbar Treatment Market

Market Size in USD Billion

USD

2.74 Billion

USD

5.58 Billion

2025

2033

USD

2.74 Billion

USD

5.58 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.74 Billion | |

| USD 5.58 Billion | |

| % | |

|

Pseudobulbar Treatment Market Overview

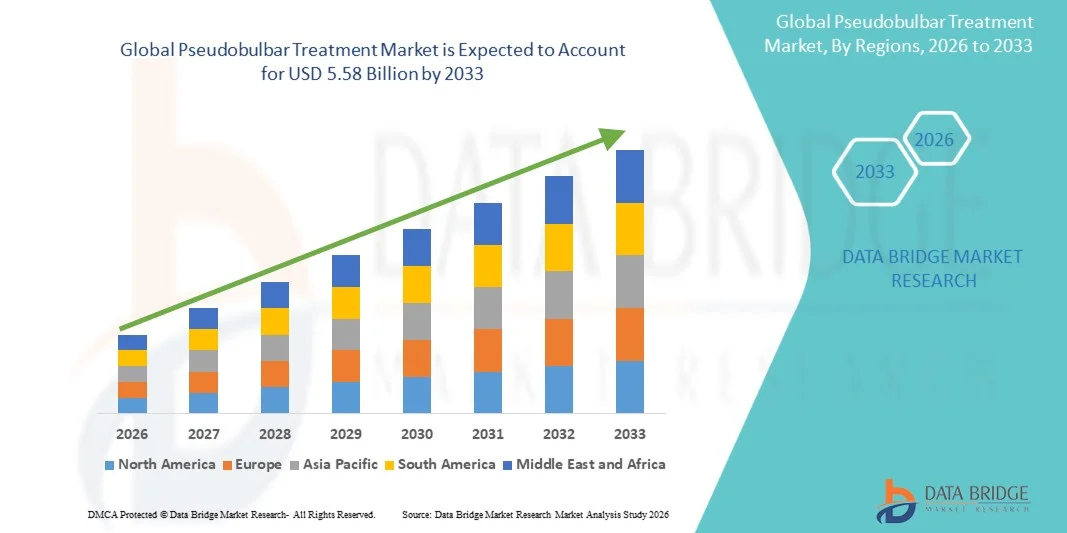

The Pseudobulbar Treatment Market was valued at USD 2.74 billion in 2025 and is projected to reach USD 5.58 billion by 2033, growing at a CAGR of 9.30% from 2026 to 2033. The market is experiencing consistent growth driven by rising prevalence of neurological disorders such as multiple sclerosis, amyotrophic lateral sclerosis (ALS), stroke-related complications, and traumatic brain injuries, all of which are strongly associated with pseudobulbar affect (PBA). Increasing awareness among neurologists regarding emotional dysregulation disorders is improving diagnosis rates and expanding treatment adoption across hospitals and specialty clinics. The growing availability of FDA-approved therapies such as dextromethorphan/quinidine (Nuedexta) has significantly improved symptom management and patient quality of life. Rising geriatric population globally is further increasing the burden of neurodegenerative diseases linked to PBA. Expanding healthcare infrastructure in emerging economies is improving access to neurological care and specialty treatment. Increasing clinical research focused on central nervous system (CNS) disorders is supporting drug development pipelines. Growing adoption of antidepressants and off-label therapies continues to support treatment demand. Improved reimbursement coverage in developed markets is enhancing patient access to branded therapies. Rising awareness campaigns by neurology associations are reducing underdiagnosis of PBA. Increasing hospital neurology admissions is further supporting market expansion. Overall, growing disease burden and therapeutic advancements are key growth drivers.

The increasing diagnosis of underlying neurological conditions combined with improved screening for emotional dysregulation disorders is further accelerating market growth. Rising incidence of stroke and neurodegenerative diseases worldwide is creating a larger patient pool requiring long-term symptomatic management. Growing adoption of targeted therapies such as sigma-1 receptor agonists and serotonin pathway modulators is improving treatment outcomes. Expansion of neurology-focused specialty centers is increasing early-stage diagnosis and treatment initiation. Technological advancements in CNS drug delivery systems are improving therapeutic efficacy. Increasing use of tele-neurology and digital health platforms is supporting remote diagnosis and patient monitoring. Pharmaceutical companies are investing heavily in rare neurological disorder drug development. Clinical trials exploring novel neuro-modulatory agents are expanding globally. Growing physician preference for combination therapies is improving symptom control rates. Rising patient and caregiver awareness is reducing stigma associated with emotional outbursts. Increasing collaboration between academic institutes and pharma companies is accelerating innovation. Overall, expanding diagnosis rates and therapeutic innovation are driving sustained market growth.

Key Market Trends & Insights

- North America dominated the Pseudobulbar Treatment Market with the largest revenue share of 38.26% in 2025, supported by advanced healthcare infrastructure, strong reimbursement policies, high diagnosis rates of neurological disorders such as ALS, multiple sclerosis, stroke, and traumatic brain injury, and the presence of leading neurology centers and specialty hospitals. The region also benefits from strong adoption of approved therapies such as dextromethorphan-quinidine, increasing use of antidepressants for symptomatic management, and growing awareness of pseudobulbar affect among clinicians, contributing to early diagnosis and treatment uptake.

- The Injections segment dominated the market with a share of 67% in 2025, due to the dominance of biologic therapies administered via injectable routes.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.6% from 2026 to 2033, fueled by rising incidence of neurological disorders, improving healthcare infrastructure, increasing awareness of pseudobulbar affect, and expanding access to neurological care in countries such as China, India, and Japan. Growing healthcare expenditure, expanding hospital networks, and improved diagnosis of stroke- and MS-related complications are further accelerating regional market growth.

- Prescription Drugs dominated the market with a 72.18% share in 2025, driven by widespread use of approved therapies such as dextromethorphan-quinidine and off-label antidepressants used for symptomatic management of pseudobulbar affect.

- Medication dominated the market with a 78.45% share in 2025, driven by strong reliance on pharmacological treatment as the primary approach for managing emotional lability associated with neurological conditions. Occupational therapy also plays a supportive role in patient rehabilitation and behavioral management.

- Tablets dominated the market with a 71.03% share in 2025, supported by the high availability of oral fixed-dose medications and ease of long-term outpatient management.

- Hospitals dominated the market with a 54.67% share in 2025, driven by high diagnosis rates, access to neurologists, and availability of prescription-based therapies for neurological conditions. Specialty clinics are also expanding steadily due to increasing focus on long-term neurological care.

Market Size & Forecast

- Global Market Value (2025): USD 2.74 Billion

- Expected Market Value (2033): USD 5.58 Billion

- Forecast CAGR (2026–2033): 9.30%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Pseudobulbar Treatment Market Segmentation

|

Attributes |

Pseudobulbar Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Pfizer Inc. (U.S.) · Avanir Pharmaceuticals (U.S.) · Otsuka Pharmaceutical Co., Ltd. (Japan) · Teva Pharmaceutical Industries Ltd. (Israel) · Sun Pharmaceutical Industries Ltd. (India) · Viatris Inc. (U.S.) · Novartis AG (Switzerland) · Johnson & Johnson (Janssen Pharmaceuticals) (U.S.) · Merck & Co., Inc. (U.S.) · Bristol Myers Squibb (U.S.) · Eli Lilly and Company (U.S.) · AbbVie Inc. (U.S.) · Roche Holding AG (Switzerland) · AstraZeneca plc (U.K.) · Sanofi S.A. (France) · Amneal Pharmaceuticals Inc. (U.S.) · Lupin Limited (India) · Dr. Reddy’s Laboratories Ltd. (India) · Alkem Laboratories Ltd. (India) · Cipla Ltd. (India) · H. Lundbeck A/S (Denmark) · Hetero Labs Ltd. (India) · Zydus Lifesciences Ltd. (India) · Eisai Co., Ltd. (Japan) · Sumitomo Pharma Co., Ltd. (Japan) · Bausch Health Companies Inc. (Canada) · Amgen Inc. (U.S.) · Neurocrine Biosciences, Inc. (U.S.) · ACADIA Pharmaceuticals Inc. (U.S.) · Biogen Inc. (U.S.) · Aurobindo Pharma Ltd. (India) · Torrent Pharmaceuticals Ltd. (India) · Glenmark Pharmaceuticals Ltd. (India) · Intas Pharmaceuticals Ltd. (India) |

|

Market Opportunities |

· Expansion of Targeted CNS Therapeutics and Novel Drug Development · Increasing Adoption of Digital Neurology and Telemedicine-Based Diagnosis · Rising Demand in Aging Population and Expanding Neurological Disorder Burden |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Pseudobulbar Treatment Market Trends

Trend: Rising Adoption of Targeted Pharmacological Therapies for Pseudobulbar Affect (PBA)

The Pseudobulbar Treatment Market is witnessing a growing shift toward targeted pharmacological management of pseudobulbar affect associated with neurological conditions such as amyotrophic lateral sclerosis (ALS), multiple sclerosis (MS), stroke, and traumatic brain injury (TBI). The only FDA-approved therapy specifically indicated for PBA, dextromethorphan-quinidine (Nuedexta), continues to be widely adopted, with clinical studies showing significant reduction in uncontrolled laughing and crying episodes in affected patients. Increasing off-label use of antidepressants such as SSRIs and tricyclic antidepressants is also contributing to broader symptomatic management. Neurologists are increasingly recognizing PBA as a distinct neurological condition rather than a psychiatric disorder, improving diagnosis rates and treatment adoption globally.

Pseudobulbar Treatment Market Dynamics

Key Market Driver: Rising Prevalence of Neurological Disorders Associated with PBA

The increasing global burden of neurological disorders such as stroke, multiple sclerosis, Parkinson’s disease, and ALS is a major driver of the Pseudobulbar Treatment market. Stroke alone affects over 12 million people annually worldwide, and a significant proportion of post-stroke patients develop pseudobulbar affect symptoms. Improved survival rates in neurodegenerative conditions have also increased the patient pool requiring long-term symptomatic management.

Growing awareness among neurologists and primary care physicians, along with improved diagnostic recognition of emotional lability symptoms, is accelerating treatment adoption. Clinical guidelines in North America and Europe increasingly recommend pharmacological intervention for moderate to severe PBA, further strengthening demand for approved therapies.

Key Restraint/Challenge: Underdiagnosis and Overlap with Psychiatric Disorders

A key challenge in the market is the underdiagnosis and misclassification of pseudobulbar affect, as symptoms are often confused with depression, bipolar disorder, or other psychiatric conditions. This leads to delayed or inappropriate treatment initiation.

In addition, limited awareness in developing regions and lack of standardized diagnostic tools restrict early identification of PBA patients. Even in developed healthcare systems, variability in clinical recognition among general practitioners versus neurologists contributes to inconsistent treatment rates. Cost considerations for branded therapies such as dextromethorphan-quinidine also limit accessibility in lower-income populations, despite its proven clinical efficacy.

Key Market Opportunity: Expansion of Neurology Care Infrastructure and Combination Therapy Approaches

The Pseudobulbar Treatment market presents strong growth opportunities through expansion of neurology care infrastructure and increasing integration of multidisciplinary treatment approaches. Growing establishment of stroke rehabilitation centers, neuro-rehabilitation clinics, and long-term care facilities is improving diagnosis and treatment access for PBA patients.

Research is also expanding into serotonin-modulating agents and glutamate pathway therapies, aiming to improve emotional regulation in neurological patients. Increasing use of digital neurology tools, telemedicine-based psychiatric-neurological assessments, and improved post-stroke care pathways in countries such as the U.S., Germany, Japan, and China are further expanding treatment accessibility. In addition, rising healthcare expenditure in emerging economies and improving insurance coverage for neurological disorders are expected to significantly increase adoption of approved and off-label therapies over the coming years, creating a strong growth outlook for the Pseudobulbar Treatment Market.

Pseudobulbar Treatment Market Scope

The Pseudobulbar Treatment market is segmented on the basis of simulation type, vehicle type, training application, end user, hardware components, software components, training mode, integration & connectivity, deployment and support & services.

- By Type

On the basis of type, the global Neuromyelitis Optica Spectrum Disorder (NMOSD) market is segmented into Neuromyelitis Optica Spectrum Disorder with Aquaporin-4 Antibodies and Neuromyelitis Optica Spectrum Disorder without Aquaporin-4 Antibodies. The Neuromyelitis Optica Spectrum Disorder with Aquaporin-4 Antibodies segment dominated the market with a share of 35% in 2025, due to its higher diagnostic prevalence and strong clinical association with severe relapsing neurological symptoms. This subtype is more widely identified in clinical practice through advanced antibody testing, enabling targeted biologic therapies and improved treatment outcomes. Increasing awareness among neurologists and improved diagnostic accuracy through serological testing are further strengthening segment dominance. In addition, rising adoption of FDA-approved targeted therapies for AQP4-positive patients is accelerating treatment uptake globally. Expanding clinical research focused on antibody-mediated inflammatory mechanisms is also contributing to higher market share. Moreover, growing hospital-based screening programs are improving early detection rates. Pharmaceutical companies are increasingly focusing on precision therapies for this subtype. Enhanced reimbursement coverage for biologic treatments is further supporting growth.

The Neuromyelitis Optica Spectrum Disorder without Aquaporin-4 Antibodies segment is expected to register the fastest growth with a CAGR of 6% from 2026 to 2033, driven by increasing recognition of seronegative NMOSD cases. Advancements in diagnostic imaging and biomarker research are improving identification of antibody-negative patients. Expanding clinical trials targeting alternative immune pathways are supporting treatment innovation. Growing physician awareness of atypical NMOSD presentations is boosting diagnosis rates. In addition, increasing use of MRI-based confirmation techniques is improving clinical classification. Rising unmet medical needs in seronegative patients are driving pharmaceutical R&D investments. The development of broader immunosuppressive therapies is supporting segment expansion. Increasing healthcare expenditure in emerging economies is also contributing to growth. Adoption of personalized neurology treatment approaches is further accelerating demand.

- By Treatment Type

On the basis of treatment type, the global NMOSD market is segmented into Medication, Plasma Exchange Therapy, and Immunoglobulin Therapy. The Medication segment dominated the market with a share of X67% in 2025, driven by the widespread use of immunosuppressants and monoclonal antibodies for long-term relapse prevention. Drugs such as eculizumab, inebilizumab, and satralizumab are increasingly being used as first-line therapies. Rising preference for targeted biologic drugs is improving treatment outcomes and reducing relapse frequency. Expanding approvals of novel biologics are strengthening medication dominance. Increasing hospital prescriptions for maintenance therapy is further supporting segment growth. Strong clinical guidelines recommending early immunotherapy initiation are boosting adoption. Pharmaceutical innovation in complement inhibition therapies is enhancing efficacy. Growing patient awareness about disease relapse prevention is also supporting market expansion. Improved insurance coverage for biologics is increasing accessibility.

The Plasma Exchange Therapy segment is expected to witness the fastest growth at a CAGR of 5% from 2026 to 2033, due to its effectiveness in managing acute NMOSD attacks. Increasing use in steroid-refractory patients is driving adoption. Hospitals are expanding apheresis infrastructure to support neurological emergency care. Rising incidence of severe relapse cases is boosting demand. Clinical guidelines recommending plasma exchange for acute attacks are strengthening utilization. Technological improvements in apheresis systems are enhancing safety and efficiency. Growing availability of specialized neurology centers is improving access. Increasing physician preference for rapid symptom control therapies is supporting growth. Expanding critical care capabilities in emerging regions is further accelerating adoption.

- By Route of Administration

On the basis of route of administration, the market is segmented into Oral, Parenteral, and Others. The Parenteral segment dominated the market with a share of 25% in 2025, due to the widespread use of injectable biologics and monoclonal antibodies in NMOSD management. Most advanced therapies targeting immune pathways are administered intravenously or subcutaneously. Hospitals prefer parenteral drugs for faster bioavailability and controlled dosing. Increasing adoption of hospital-based infusion therapies is driving segment dominance. Rising availability of self-injectable biologics is improving patient compliance. Strong pipeline of injectable immunotherapies is supporting growth. Clinical preference for rapid therapeutic action in acute cases is strengthening demand. Expanding infusion center infrastructure is further boosting adoption. Insurance coverage for biologic injections is increasing accessibility.

The Oral segment is expected to register the fastest CAGR of 8.00% from 2026 to 2033, driven by increasing development of oral immunomodulatory therapies. Pharmaceutical companies are focusing on convenient long-term treatment options. Rising patient preference for non-invasive administration is supporting growth. Expanding clinical trials for oral small-molecule drugs is accelerating innovation. Improved adherence rates with oral therapies are boosting demand. Growing outpatient management of NMOSD is supporting adoption. Advancements in blood-brain barrier penetrating drugs are enhancing efficacy. Increasing healthcare accessibility in emerging markets is also contributing to growth.

- By Dosage Form

On the basis of dosage form, the market is segmented into Tablets, Injections, and Others. The Injections segment dominated the market with a share of 67% in 2025, due to the dominance of biologic therapies administered via injectable routes. Most monoclonal antibody treatments for NMOSD are available in injectable formulations. Hospitals prefer injections for acute and maintenance treatment phases. Rapid therapeutic action of injectable drugs is supporting dominance. Increasing adoption of subcutaneous biologics is improving patient convenience. Strong clinical efficacy of injectable immunotherapies is driving usage. Expanding biologics pipeline is reinforcing segment leadership. Rising hospital infusion practices are supporting demand. Improved reimbursement policies for injectable biologics are strengthening adoption.

The Tablets segment is expected to witness the fastest growth at a CAGR of 8.00% from 2026 to 2033, driven by increasing development of oral small-molecule immunotherapies. Patient preference for convenient home-based treatment is accelerating demand. Growing shift toward outpatient care is supporting adoption. Pharmaceutical R&D in oral immunomodulators is expanding rapidly. Improved drug safety profiles are increasing acceptance. Expanding access in developing regions is boosting growth. Increasing focus on long-term maintenance therapy is supporting tablet usage. Enhanced adherence compared to injections is further driving demand.

- By End-Users

On the basis of end-users, the market is segmented into Hospitals, Specialty Clinics, Homecare, and Others. The Hospitals segment dominated the market with a share of 34% in 2025, due to high patient inflow for diagnosis, acute relapse management, and biologic infusion therapies. Hospitals provide advanced diagnostic imaging and antibody testing facilities. Availability of neurology specialists is supporting treatment accuracy. Increasing hospitalization rates for acute NMOSD attacks are driving demand. Strong infrastructure for plasma exchange and biologic infusion is reinforcing dominance. Government healthcare funding is supporting hospital-based treatment. Rising preference for multidisciplinary care is boosting adoption. Expanding tertiary care centers is strengthening segment growth.

The Specialty Clinics segment is expected to witness the fastest CAGR of 5.6% from 2026 to 2033, driven by growing demand for outpatient neurology care. Increasing shift toward decentralized healthcare delivery is supporting growth. Specialty clinics offer faster diagnosis and personalized treatment plans. Rising availability of neurologists in private practice is boosting adoption. Cost-effective treatment compared to hospitals is driving patient preference. Expanding clinic-based infusion services is supporting growth. Improved awareness of NMOSD is increasing outpatient visits. Growth of private healthcare infrastructure is further accelerating segment expansion.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Retail Pharmacy, Online Pharmacy, and Others. The Hospital Pharmacy segment dominated the market with a share of 56% in 2025, due to the high dependence on hospital-based drug dispensing for biologics and acute therapies. Most NMOSD treatments are administered under hospital supervision. Strong integration with inpatient care systems is supporting dominance. Availability of high-cost biologics in hospital pharmacies is reinforcing usage. Increasing infusion-based treatment cycles is boosting demand. Strict prescription control in hospital settings is driving distribution. Rising hospital admissions for relapse management is supporting growth. Government procurement programs are further strengthening segment leadership.

The Online Pharmacy segment is expected to witness the fastest CAGR of 6.8% from 2026 to 2033, driven by increasing digital healthcare adoption. Rising demand for home delivery of maintenance medications is supporting growth. Expanding telemedicine platforms are enabling remote prescriptions. Growing patient preference for convenience is accelerating adoption. Increasing penetration of e-pharmacy platforms in emerging markets is boosting access. Improved regulatory frameworks for online drug sales are supporting expansion. Digitalization of healthcare supply chains is strengthening distribution efficiency. Rising chronic disease management at home is further driving demand.

Pseudobulbar Treatment Market Regional Analysis

North America dominated the Pseudobulbar Treatment Market and accounted for the largest revenue share of 38.26% in 2025, supported by advanced healthcare infrastructure, strong reimbursement policies, high diagnosis rates of neurological disorders such as ALS, multiple sclerosis, stroke, and traumatic brain injury, and the presence of leading neurology centers and specialty hospitals. The region also benefits from strong adoption of approved therapies such as dextromethorphan-quinidine, increasing use of SSRIs and other antidepressants for symptomatic management, and growing awareness of pseudobulbar affect among clinicians, which is improving early diagnosis and treatment uptake across healthcare systems.

U.S. Pseudobulbar Treatment Market Insight

The U.S. Pseudobulbar Treatment market is witnessing strong growth due to high prevalence of neurological disorders such as stroke, ALS, multiple sclerosis, and traumatic brain injury, which are strongly associated with pseudobulbar affect. The country benefits from advanced neurology care infrastructure, strong insurance coverage, and widespread availability of FDA-approved therapy dextromethorphan-quinidine (Nuedexta). Increasing awareness among neurologists and rehabilitation specialists is improving diagnosis rates, while strong clinical research activity in neurodegenerative and post-stroke emotional disorders continues to support treatment innovation and adoption.

Europe Pseudobulbar Treatment Market Insight

The Europe Pseudobulbar Treatment market remains a significant contributor to global revenue, driven by well-established healthcare systems, rising neurological disease burden, and increasing access to advanced pharmacological therapies across countries such as Germany, France, and the U.K. The region benefits from structured neurology care pathways, improved recognition of pseudobulbar affect in post-stroke and neurodegenerative patients, and expanding use of antidepressants and combination pharmacotherapy for symptom control. Strong clinical research participation in neurological disorders further supports market expansion across Europe.

U.K. Pseudobulbar Treatment Market Insight

The U.K. Pseudobulbar Treatment market is experiencing steady growth due to the high burden of stroke and neurodegenerative disorders and strong diagnostic capabilities within the National Health Service (NHS). Increasing recognition of pseudobulbar affect among neurologists and rehabilitation specialists is improving early diagnosis and treatment rates. The country benefits from access to advanced pharmacological therapies, including dextromethorphan-quinidine and antidepressants used for symptomatic management, along with strong participation in neurological research and clinical studies focused on post-stroke and motor neuron disease-related emotional disorders.

Germany Pseudobulbar Treatment Market Insight

The Germany Pseudobulbar Treatment market is expanding steadily due to its advanced healthcare infrastructure, strong neurology specialization, and high prevalence of neurological conditions such as stroke, multiple sclerosis, and Parkinson’s disease. Hospitals and specialty neurology centers are increasingly focusing on early identification of pseudobulbar affect and adoption of evidence-based pharmacological treatments. Strong reimbursement systems, access to innovative neurological drugs, and active participation in European clinical research initiatives further support market growth in Germany.

Asia-Pacific Pseudobulbar Treatment Market Insight

The Asia-Pacific Pseudobulbar Treatment market is expected to be the fastest-growing region at a CAGR of 7.6% from 2026 to 2033, driven by rising incidence of neurological disorders, improving healthcare infrastructure, increasing awareness of pseudobulbar affect, and expanding access to neurological care across China, India, and Japan. Growing healthcare expenditure, expanding hospital networks, and improved diagnosis of stroke-related and multiple sclerosis-related complications are further accelerating regional market growth. In addition, increasing adoption of antidepressant therapies and improving access to neurology specialists are supporting treatment uptake across emerging economies.

Japan Pseudobulbar Treatment Market Insight

The Japan Pseudobulbar Treatment market is witnessing steady growth due to its aging population, increasing burden of neurodegenerative disorders, and strong neurology care infrastructure. Hospitals and specialty neurology centers are increasingly recognizing pseudobulbar affect in patients with stroke, ALS, and Parkinson’s disease, leading to improved diagnosis rates. The country’s advanced healthcare system and strong access to pharmacological therapies, including antidepressants and approved neurological treatments, continue to support market expansion.

China Pseudobulbar Treatment Market Insight

The China Pseudobulbar Treatment market is growing rapidly, driven by rising incidence of neurological disorders, expanding healthcare infrastructure, and increasing awareness of pseudobulbar affect among clinicians. Improved access to diagnostic imaging and neurological assessment tools is supporting earlier identification of patients with post-stroke and neurodegenerative complications. In addition, expanding hospital networks, rising healthcare expenditure, and increasing availability of antidepressant-based therapies are strengthening market growth, positioning China as one of the fastest-growing NMOSD-related neurological treatment markets globally.

Pseudobulbar Treatment Market Share

The Pseudobulbar Treatment industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Avanir Pharmaceuticals (U.S.)

- Otsuka Pharmaceutical Co., Ltd. (Japan)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Viatris Inc. (U.S.)

- Novartis AG (Switzerland)

- Johnson & Johnson (Janssen Pharmaceuticals) (U.S.)

- Merck & Co., Inc. (U.S.)

- Bristol Myers Squibb (U.S.)

Latest Developments in Pseudobulbar Treatment Market

- In October 2021, Avanir Pharmaceuticals (Otsuka Holdings) expanded clinical research on dextromethorphan/quinidine (Nuedexta) for broader neuropsychiatric indications, including agitation and affective dysregulation in neurological disorders. The company continued evaluating extended applications beyond pseudobulbar affect, leveraging its sigma-1 receptor agonist and NMDA antagonist mechanism. This development reflects growing interest in repositioning PBA therapies for related neurological and behavioral conditions such as ALS and multiple sclerosis–associated symptoms

- In May 2022, the U.S. FDA-supported clinical and pharmacological research highlighted expanding use of dextromethorphan-based combination therapies for central nervous system disorders, including pseudobulbar affect and related mood dysregulation conditions. The period also marked increased clinical attention toward optimizing serotonergic and glutamatergic modulation therapies for emotional incontinence in neurodegenerative diseases

- In August 2022, Axsome Therapeutics received FDA approval for dextromethorphan/bupropion (Auvelity) for major depressive disorder, marking a significant milestone for dextromethorphan-based neuropsychiatric drug platforms. Although not directly indicated for PBA, this approval strengthened the broader therapeutic validation of dextromethorphan pharmacology, supporting renewed R&D interest in pseudobulbar affect and related emotional dysregulation disorders

- In November 2022, peer-reviewed clinical publications further reinforced the therapeutic effectiveness of dextromethorphan/quinidine (Nuedexta) in reducing pseudobulbar affect episodes, showing significant reduction in episode frequency in ALS and multiple sclerosis patients. These findings strengthened its position as the only FDA-approved therapy specifically targeting PBA symptoms

- In October 2025, clinical neurology references reaffirmed pseudobulbar affect as a persistent unmet medical need in ALS, multiple sclerosis, and dementia populations, with ongoing emphasis on improving access to FDA-approved therapies and expanding early diagnosis rates. Continued reliance on dextromethorphan/quinidine as the cornerstone therapy reflects limited competition but growing research into next-generation serotonergic and NMDA-modulating agents

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.