Global Pterygium Drug Market

Market Size in USD Million

USD

343.30 Million

USD

555.48 Million

2025

2033

USD

343.30 Million

USD

555.48 Million

2025

2033

| 2026 - 2033 | |

| USD 343.30 Million | |

| USD 555.48 Million | |

| % | |

|

Pterygium Drug Market Size

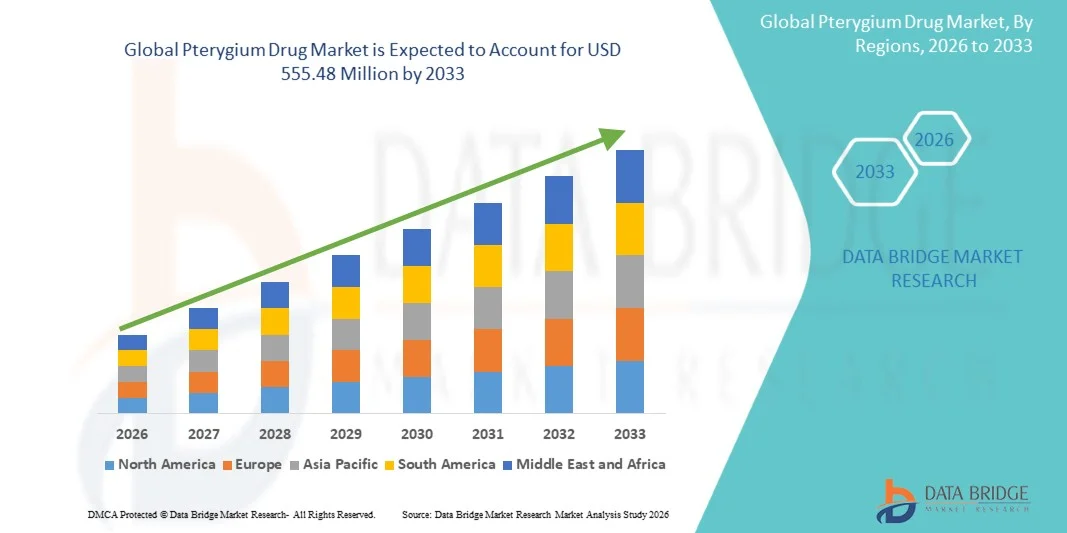

- The global Pterygium Drug market size was valued at USD 343.30 Million in 2025 and is expected to reach USD 555.48 Million by 2033, at a CAGR of 6.20% during the forecast period

- The market growth is largely fueled by the increasing prevalence of pterygium, rising exposure to environmental risk factors such as UV radiation and dust, and growing awareness regarding early diagnosis and treatment, leading to higher demand for effective therapeutic solutions

- Furthermore, increasing focus on non-surgical treatment options, advancements in anti-inflammatory and anti-fibrotic drug development, and rising patient preference for minimally invasive care are establishing pterygium drugs as essential components in ophthalmic treatment. These converging factors are accelerating the uptake of pterygium drug solutions, thereby significantly boosting the market’s growth

Pterygium Drug Market Analysis

- Pterygium drugs, including anti-inflammatory agents, lubricants, and emerging anti-fibrotic therapies, are increasingly important in ophthalmic care due to their role in managing symptoms, reducing recurrence, and improving patient outcomes in both early-stage and post-surgical cases

- The escalating demand for pterygium drug solutions is primarily driven by increasing exposure to UV radiation, rising prevalence of eye disorders in tropical and subtropical regions, and growing awareness regarding early diagnosis and non-surgical management options

- North America dominated the pterygium drug market with the largest revenue share of approximately 37.9% in 2025, supported by advanced healthcare infrastructure, higher diagnosis rates, and strong presence of ophthalmic drug manufacturers

- Asia-Pacific is expected to be the fastest-growing region in the pterygium drug market during the forecast period, with a projected CAGR of 8.7%, driven by increasing patient population, rising awareness of eye health, and growing access to ophthalmic care in countries such as China, India, and Southeast Asia

- The eye drops segment dominated the largest market revenue share of 66.4% in 2025, driven by ease of administration and widespread clinical preference

Report Scope and Pterygium Drug Market Segmentation

|

Attributes |

Pterygium Drug Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Novartis AG (Switzerland) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Pterygium Drug Market Trends

“Rising Adoption of Pharmacological Treatments and Minimally Invasive Therapies”

- A significant and accelerating trend in the global pterygium drug market is the increasing shift toward pharmacological management and minimally invasive treatment approaches, aimed at reducing recurrence rates and improving patient outcomes. This trend is being driven by growing awareness regarding early-stage treatment and the limitations associated with surgical excision alone.

- For instance, in 2024, Novartis AG expanded research on anti-inflammatory ophthalmic formulations targeting pterygium-related inflammation, highlighting the increasing focus on drug-based interventions for ocular surface disorders.

- The market is witnessing rising demand for anti-inflammatory drugs, lubricating eye drops, and immunomodulators that help alleviate irritation, redness, and progression of pterygium.

- Increasing preference for non-surgical treatment options among patients, especially in early-stage conditions, is supporting the growth of drug-based therapies.

- Advancements in ophthalmic drug delivery systems, such as sustained-release eye drops and nanotechnology-based formulations, are improving drug efficacy and patient compliance.

- The integration of combination therapies, including corticosteroids and anti-VEGF agents, is gaining traction to minimize recurrence following surgical procedures.

- Pharmaceutical companies are investing in the development of targeted therapies that address underlying inflammatory and degenerative pathways associated with pterygium.

- Growing awareness campaigns by healthcare organizations regarding eye health and UV protection are encouraging early diagnosis and treatment adoption.

- The increasing prevalence of ocular disorders due to environmental factors such as UV exposure, dust, and pollution is further accelerating demand for effective drug therapies.

- This trend toward preventive care, improved drug formulations, and patient-centric treatment approaches is reshaping the global Pterygium Drug market landscape

Pterygium Drug Market Dynamics

Driver

“Increasing Prevalence of Ocular Disorders and Growing Awareness of Eye Health”

- The rising prevalence of pterygium and other ocular surface disorders, particularly in regions with high UV exposure, is a major driver for the growth of the Pterygium Drug market. Increasing awareness about eye health and early treatment is further contributing to market expansion

- For instance, in 2025, World Health Organization highlighted the growing burden of preventable eye diseases globally, emphasizing the need for early intervention and treatment solutions, including pharmacological therapies

- Increasing exposure to environmental risk factors such as sunlight, wind, and dust is contributing to a higher incidence of pterygium worldwide

- Rising awareness among patients regarding the importance of early diagnosis and treatment is encouraging the use of drug therapies to manage symptoms effectively

- Growing geriatric population, which is more susceptible to ocular conditions, is further driving demand for pterygium drugs

- Improved access to ophthalmic care and diagnostic facilities is enabling timely treatment and boosting prescription rates

- Increasing healthcare expenditure in developing and developed countries is supporting the adoption of advanced ophthalmic treatments

- The expansion of pharmaceutical distribution channels, including retail pharmacies and online platforms, is improving drug accessibility

- Ongoing research and development activities are leading to the introduction of more effective and targeted therapies

- Supportive government initiatives and public health programs focused on vision care are further accelerating market growth

Restraint/Challenge

“Limited Drug Efficacy in Advanced Cases and High Treatment Costs”

- The limited effectiveness of pharmacological treatments in advanced stages of pterygium remains a significant challenge, as surgical intervention is often required in severe cases, restricting the overall scope of drug-based management

- For instance, clinical observations and ophthalmology studies indicate that while lubricants and anti-inflammatory drugs provide symptomatic relief, they do not completely eliminate fibrovascular growth, leading to recurrence in certain patients

- The high cost associated with advanced ophthalmic formulations and combination therapies can act as a barrier, particularly in low- and middle-income regions

- Lack of awareness in rural and underdeveloped areas may delay diagnosis and treatment, limiting market penetration

- Potential side effects associated with long-term use of corticosteroids, such as increased intraocular pressure, may restrict their usage

- Variability in treatment outcomes across different patient groups can affect physician confidence in drug-based approaches

- Limited availability of targeted therapies specifically approved for pterygium treatment remains a key gap in the market

- Regulatory challenges and lengthy approval timelines for new ophthalmic drugs can slow down product launches

- Patient non-compliance with prolonged treatment regimens may impact therapeutic effectiveness

- Addressing these challenges through innovation in drug development, improved affordability, and increased awareness will be crucial for sustained market growth

Pterygium Drug Market Scope

The market is segmented on the basis of disease type, stages, treatment, formulation, mode of purchase, population type, end user, and distribution channel.

• By Disease Type

On the basis of disease type, the Pterygium Drug market is segmented into progressive pterygium and atrophic pterygium. The progressive pterygium segment dominated the largest market revenue share of 57.6% in 2025, driven by its higher severity and need for active medical intervention. Patients with progressive pterygium often require continuous treatment due to increasing corneal invasion and vision impairment. Ophthalmologists prioritize early treatment in progressive cases to prevent complications. Rising awareness about eye health and early diagnosis contributes to segment growth. Hospitals and specialty clinics report higher patient inflow for progressive cases. Increasing exposure to UV radiation globally supports prevalence. Demand for effective pharmacological management boosts adoption. Pharmaceutical companies focus on targeted therapies for progressive stages. Integration of diagnostic imaging enhances detection rates. Government health programs promoting eye care strengthen treatment access. Expanding geriatric population further drives demand. The segment benefits from higher treatment adherence and repeat prescriptions.

The atrophic pterygium segment is expected to witness the fastest CAGR of 14.8% from 2026 to 2033, driven by increasing early-stage diagnosis and preventive treatment approaches. Growing awareness among patients leads to earlier medical consultation. Adoption of lubricants and mild therapies supports segment expansion. Technological advancements in ophthalmic diagnostics improve detection. Increasing healthcare access in emerging markets accelerates growth. Physicians recommend early treatment to avoid progression into severe stages. Expansion of outpatient ophthalmology services boosts adoption. Rising environmental factors such as dust and pollution contribute to prevalence. Pharmaceutical companies develop mild and maintenance therapies for atrophic cases. Government initiatives for vision care support early-stage treatment. Growing telemedicine adoption enhances accessibility. Increasing use of OTC products further supports segment growth.

• By Stages

On the basis of stages, the Pterygium Drug market is segmented into Stage 1, Stage 2, Stage 3, and Stage 4. The Stage 2 segment dominated the largest market revenue share of 34.8% in 2025, driven by the higher diagnosis rate at this moderate stage where symptoms become more noticeable. Patients in Stage 2 often experience irritation, redness, and mild visual disturbance, prompting medical consultation. This stage represents a critical point where pharmacological treatment is most effective, leading to higher drug adoption. Increased awareness and routine eye examinations contribute to early-to-mid stage detection. The segment also benefits from the availability of effective topical therapies that can control progression. Healthcare professionals often recommend drug-based management at this stage to avoid surgical intervention. Rising environmental exposure to dust and UV rays is increasing the incidence of Stage 2 cases. The segment’s dominance is further supported by improved accessibility to ophthalmic care. Growing patient compliance with prescribed treatments also plays a role. In addition, insurance coverage for early treatment supports adoption. These combined factors maintain its leading position.

The Stage 3 segment is anticipated to witness the fastest CAGR of 7.5% from 2026 to 2033, driven by increasing progression of untreated cases and delayed diagnosis in developing regions. Stage 3 is associated with more pronounced symptoms, including significant visual impairment, leading to higher treatment demand. The rising burden of advanced ocular conditions is contributing to segment growth. Patients at this stage often require aggressive pharmacological therapy alongside surgical consideration. Increasing awareness about complications is driving treatment uptake. Technological advancements in diagnostic imaging are enabling better identification of advanced stages. The segment is also benefiting from growing healthcare infrastructure in emerging markets. In addition, rising geriatric population is more prone to advanced stages. Pharmaceutical innovations targeting severe inflammation are supporting growth. Government initiatives promoting eye health are also contributing. These factors collectively drive rapid expansion of the segment.

• By Treatment

On the basis of treatment, the Pterygium Drug market is segmented into artificial tears/topical lubricants and steroid eye drops. The artificial tears/topical lubricants segment dominated the largest market revenue share of 61.2% in 2025, driven by widespread usage for symptom relief and long-term management. These treatments are commonly prescribed for dryness, irritation, and inflammation. Patients prefer lubricants due to ease of use and minimal side effects. High availability across retail and online pharmacies supports accessibility. Ophthalmologists recommend lubricants as first-line therapy. Increasing environmental exposure to irritants boosts demand. Pharmaceutical companies offer a wide range of formulations to cater to patient needs. Rising awareness about preventive eye care contributes to adoption. Lubricants are widely used in both early and advanced stages. Growth in OTC availability enhances market penetration. Increasing aging population supports demand for regular usage. The segment benefits from affordability and repeat purchases.

The steroid eye drops segment is expected to witness the fastest CAGR of 15.6% from 2026 to 2033, driven by increasing need for anti-inflammatory treatment in progressive cases. Steroids provide rapid relief from inflammation and redness. Physicians prescribe steroid drops for moderate-to-severe conditions. Rising clinical research on improved steroid formulations boosts adoption. Development of safer and low-side-effect variants enhances patient acceptance. Hospitals and specialty clinics drive prescription growth. Increasing prevalence of severe pterygium cases supports demand. Pharmaceutical companies focus on combination therapies for better outcomes. Expanding healthcare infrastructure in emerging markets accelerates access. Patient awareness about effective treatment options increases adoption. Regulatory approvals for new formulations support market growth. Growing demand for targeted therapies further strengthens the segment.

• By Formulation

On the basis of formulation, the Pterygium Drug market is segmented into eye drops, eye ointments, and others. The eye drops segment dominated the largest market revenue share of 66.4% in 2025, driven by ease of administration and widespread clinical preference. Eye drops are convenient for both short-term and long-term treatment. Patients prefer drops due to quick absorption and minimal discomfort. High availability across pharmacies enhances accessibility. Pharmaceutical companies focus on advanced drop formulations with improved stability. Increasing demand for preservative-free drops supports growth. Ophthalmologists widely prescribe drops as primary therapy. Rising prevalence of eye disorders boosts usage. Technological advancements in drop delivery systems improve compliance. Growing awareness of eye care supports adoption. Eye drops are suitable for all age groups, enhancing penetration. Strong distribution networks ensure consistent availability globally.

The eye ointments segment is expected to witness the fastest CAGR of 13.9% from 2026 to 2033, driven by increasing use in severe and nighttime treatment. Ointments provide prolonged drug contact with the ocular surface. Physicians recommend ointments for advanced cases requiring sustained relief. Increasing adoption in hospital settings supports growth. Pharmaceutical innovation improves formulation consistency and effectiveness. Rising demand for combination therapies enhances usage. Patients with chronic symptoms prefer ointments for long-lasting relief. Growth in specialty clinics boosts prescription rates. Expanding healthcare access in emerging regions supports adoption. Increasing awareness of alternative formulations contributes to market expansion. Improved packaging and delivery systems enhance convenience. Rising prevalence of severe pterygium conditions further accelerates growth.

• By Mode of Purchase

On the basis of mode of purchase, the Pterygium Drug market is segmented into prescription and over the counter (OTC). The prescription segment dominated the largest market revenue share of 63.7% in 2025, driven by the need for clinical supervision and accurate diagnosis. Most steroid-based and advanced treatments require medical prescriptions. Hospitals and specialty clinics drive prescription volumes. Physicians ensure appropriate dosage and monitoring. Increasing awareness about eye health encourages medical consultation. Pharmaceutical companies collaborate with healthcare providers for product adoption. Regulatory frameworks support prescription-based distribution. Rising prevalence of moderate-to-severe cases boosts demand. Integration with healthcare systems ensures accessibility. Patient trust in prescribed medications enhances adherence. Expanding insurance coverage supports prescription usage. Growth in ophthalmology services strengthens the segment.

The OTC segment is expected to witness the fastest CAGR of 16.2% from 2026 to 2033, driven by increasing consumer preference for self-medication and easy access to lubricants. OTC products are widely available across retail and online platforms. Patients use OTC solutions for mild symptoms and preventive care. Growing awareness campaigns promote self-care practices. Expansion of e-commerce platforms enhances accessibility. Pharmaceutical companies invest in OTC product marketing. Rising urbanization and lifestyle changes increase demand. Emerging markets show rapid adoption due to affordability. Regulatory approvals for OTC products support growth. Convenience and cost-effectiveness drive consumer preference. Increasing use in early-stage treatment accelerates expansion.

• By Population Type

On the basis of population type, the Pterygium Drug market is segmented into geriatric and adults. The geriatric segment dominated the largest market revenue share of 58.9% in 2025, driven by higher prevalence of eye disorders in aging populations. Older individuals are more susceptible to pterygium due to prolonged UV exposure. Increasing global aging population supports segment growth. Healthcare providers prioritize treatment in elderly patients. Availability of specialized ophthalmic care enhances adoption. Government healthcare programs for elderly care boost accessibility. Rising awareness among older adults contributes to diagnosis. Pharmaceutical companies focus on age-friendly formulations. Hospitals report higher patient volumes in geriatric groups. Increasing chronic disease burden supports regular treatment. Technological advancements improve treatment outcomes. The segment benefits from consistent medication usage.

The adult segment is expected to witness the fastest CAGR of 14.5% from 2026 to 2033, driven by increasing exposure to environmental factors such as UV radiation, dust, and pollution. Growing screen time and lifestyle changes contribute to eye disorders. Awareness campaigns encourage early diagnosis among adults. Expansion of occupational health programs supports treatment. Increasing healthcare access in urban areas boosts adoption. Pharmaceutical companies target adult populations with preventive therapies. Rising demand for OTC products supports growth. Technological advancements in diagnosis improve detection rates. Increasing health consciousness drives treatment uptake. Growth in telemedicine services enhances accessibility. Expanding workforce population further accelerates demand.

• By End User

On the basis of end user, the Pterygium Drug market is segmented into hospitals, specialty clinics, home healthcare, and others. The hospitals segment dominated the largest market revenue share of 49.6% in 2025, driven by availability of advanced diagnostic tools and specialized ophthalmologists. Hospitals manage moderate-to-severe cases effectively. Increasing patient trust in hospital-based treatment supports growth. Integration with insurance systems enhances accessibility. Hospitals provide comprehensive care including diagnosis and therapy. Government healthcare programs strengthen hospital infrastructure. Rising clinical trials in hospital settings boost adoption. Advanced imaging and treatment technologies improve outcomes. Collaboration with pharmaceutical companies supports new therapy adoption. Expanding hospital networks in emerging markets drives growth. Continuous medical education improves treatment quality. The segment benefits from strong patient inflow and service capabilities.

The home healthcare segment is expected to witness the fastest CAGR of 15.3% from 2026 to 2033, driven by increasing preference for at-home treatment and self-administration. Patients prefer homecare for convenience and cost-effectiveness. Telemedicine platforms provide guidance and monitoring. Rising adoption of OTC and easy-to-use medications supports growth. Pharmaceutical companies develop user-friendly formulations. Increasing aging population drives demand for homecare solutions. Expansion of digital health tools enhances patient engagement. Emerging markets show rapid adoption due to limited hospital access. Insurance coverage for homecare supports growth. Patient awareness programs encourage self-management. Growing demand for remote healthcare services accelerates expansion.

• By Distribution Channel

On the basis of distribution channel, the Pterygium Drug market is segmented into retail pharmacies, hospital pharmacies, online pharmacies, and others. The hospital pharmacies segment dominated the largest market revenue share of 52.8% in 2025, driven by direct access to prescribed medications and clinical supervision. Hospital pharmacies ensure proper storage and handling of ophthalmic drugs. Integration with hospital systems enhances patient care. Physicians prefer hospital dispensing for critical treatments. Increasing hospital visits support segment growth. Pharmaceutical companies collaborate with hospitals for distribution. Regulatory compliance ensures quality and safety. Availability of advanced therapies strengthens dominance. Patient counseling services improve adherence. Expansion of hospital infrastructure supports accessibility. Strong supply chain networks ensure availability.

The online pharmacies segment is expected to witness the fastest CAGR of 17.1% from 2026 to 2033, driven by increasing digitalization and e-commerce adoption. Online platforms provide convenient access to medications. Patients prefer home delivery and competitive pricing. Rising smartphone and internet penetration supports growth. Integration with telemedicine services enhances adoption. Pharmaceutical companies partner with e-commerce platforms for distribution. Expanding logistics networks improve delivery efficiency. Awareness of online healthcare services increases usage. Emerging markets show rapid adoption of digital platforms. Secure payment and prescription verification systems boost trust. Growing demand for chronic therapy management accelerates expansion.

Pterygium Drug Market Regional Analysis

- North America dominated the pterygium drug market with the largest revenue share of approximately 37.9% in 2025, supported by advanced healthcare infrastructure, higher diagnosis rates, and a strong presence of ophthalmic drug manufacturers. For instance, in 2024, Bausch + Lomb expanded its ophthalmic product portfolio in the U.S., enhancing the availability of prescription eye drops and anti-inflammatory treatments for ocular surface disorders, including pterygium. The region benefits from a well-established network of ophthalmologists and eye care clinics, enabling early diagnosis and timely treatment

- High healthcare expenditure and favorable reimbursement policies encourage the adoption of advanced pharmacological therapies. Increasing awareness regarding eye health and UV protection contributes to early-stage treatment uptake. The presence of leading pharmaceutical companies drives continuous research and development activities

- Growing adoption of combination therapies, including lubricants and corticosteroids, supports improved patient outcomes. Strong clinical research infrastructure facilitates the introduction of innovative ophthalmic drugs. Increasing prevalence of ocular disorders due to aging populations further drives demand for treatment. Digital health platforms and teleophthalmology services are improving access to care and supporting market growth

U.S. Pterygium Drug Market Insight

The U.S. pterygium drug market captured the largest revenue share in 2025 within North America, driven by advanced R&D capabilities, high awareness levels, and strong healthcare infrastructure. For instance, in 2025, Alcon Inc. strengthened its ophthalmic drug distribution network across the U.S., improving accessibility to anti-inflammatory and lubricating eye treatments. The country benefits from a high concentration of ophthalmologists and specialized eye care centers, ensuring early diagnosis and treatment. Rising prevalence of eye disorders linked to environmental exposure and aging is increasing demand for effective therapies. Strong insurance coverage and reimbursement frameworks further support treatment adoption. Increasing use of prescription eye drops and post-surgical care medications is contributing to market growth. Ongoing clinical trials and innovation in ophthalmology are introducing new therapeutic options. Patient awareness programs and digital health tools are enhancing treatment adherence. The expansion of retail and online pharmacies is improving drug accessibility.

Europe Pterygium Drug Market Insight

The Europe pterygium drug market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by advanced healthcare systems, increasing awareness of ocular diseases, and rising demand for effective treatments. For instance, in 2024, Novartis AG expanded its ophthalmology portfolio across key European countries, improving access to anti-inflammatory eye treatments. The region benefits from strong regulatory frameworks and government healthcare support. Increasing prevalence of eye conditions due to aging populations is contributing to demand growth. High investment in research and innovation is supporting the development of advanced therapies. Expansion of ophthalmology clinics and specialized treatment centers is improving patient access. Rising awareness regarding preventive eye care is encouraging early diagnosis. Favorable reimbursement policies are supporting drug adoption. Increasing use of combination therapies is enhancing treatment effectiveness.

U.K. Pterygium Drug Market Insight

The U.K. pterygium drug market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by strong healthcare infrastructure and increasing awareness of eye health. For instance, in 2023, National Health Service expanded access to ophthalmic treatments through hospital and community care programs, supporting early diagnosis and management of ocular conditions. Growing demand for effective and affordable treatments is driving market expansion. Increasing adoption of prescription eye drops and anti-inflammatory drugs is improving patient outcomes. Rising geriatric population is contributing to higher disease prevalence. Strong government initiatives for vision care are supporting market growth. Expansion of telemedicine services is improving access to ophthalmic consultations. Increasing availability of biosimilars is enhancing affordability. Clinical research activities are supporting the development of new therapies.

Germany Pterygium Drug Market Insight

The Germany pterygium drug market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced healthcare infrastructure and strong focus on innovation. For instance, in 2024, Bayer AG continued investment in ophthalmology research, supporting the development of effective treatments for ocular surface diseases. Increasing awareness regarding eye health is encouraging early diagnosis and treatment. High healthcare expenditure supports access to advanced therapies. Strong physician network ensures effective treatment delivery. Growing prevalence of age-related eye conditions is driving demand. Government reimbursement policies support patient access to medications. Expansion of specialized eye care centers is improving treatment availability. Adoption of innovative drug delivery systems is enhancing patient compliance.

Asia-Pacific Pterygium Drug Market Insight

Asia-Pacific pterygium drug market is expected to be the fastest-growing region in the Pterygium Drug market during the forecast period, with a projected CAGR of 8.7%, driven by increasing patient population, rising awareness of eye health, and expanding access to ophthalmic care. For instance, in 2025, Sun Pharmaceutical Industries Ltd. expanded its ophthalmic product offerings across India and Southeast Asia, improving access to affordable eye care treatments. Rising exposure to environmental risk factors such as UV radiation and pollution is increasing disease prevalenc. Growing healthcare investments and improving infrastructure are enhancing treatment accessibility. Increasing awareness campaigns are encouraging early diagnosis and treatment. Expansion of pharmaceutical distribution networks is improving drug availability. Rising disposable incomes are enabling patients to access advanced treatments. Growth in medical tourism is supporting regional market expansion. Increasing number of ophthalmologists and eye care centers is improving patient care. Government initiatives promoting vision care are further accelerating market growth

Japan Pterygium Drug Market Insight

The Japan pterygium drug market is gaining momentum due to increasing healthcare awareness, aging population, and demand for advanced ophthalmic treatments. For instance, in 2024, Santen Pharmaceutical Co., Ltd. expanded its ophthalmic drug portfolio, supporting treatment of ocular surface disorders. High healthcare standards ensure early diagnosis and effective management. Strong insurance coverage improves patient access to therapies. Increasing adoption of advanced drug formulations enhances treatment outcomes. Expansion of clinical research is supporting innovation. Growing use of digital healthcare solutions is improving monitoring and adherence. Government support for chronic disease management is driving market growth.

China Pterygium Drug Market Insight

The China pterygium drug market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s large patient population, increasing healthcare access, and rising awareness. For instance, in 2024, China Resources Pharmaceutical Group expanded distribution of ophthalmic drugs across urban and rural areas, improving treatment accessibility. Rapid urbanization and environmental factors are increasing disease prevalence. Growing middle-class population is improving affordability of treatments. Government healthcare reforms are supporting access to eye care services. Expansion of hospitals and specialty clinics is enhancing patient reach. Increasing clinical research activity is supporting new drug development. Rising awareness campaigns are encouraging early diagnosis. Availability of affordable generics is boosting market penetration.

Pterygium Drug Market Share

The Pterygium Drug industry is primarily led by well-established companies, including:

• Novartis AG (Switzerland)

•Bausch Health Companies Inc. (Canada)

• Alcon Inc. (Switzerland)

• Pfizer Inc. (U.S.)

• Sun Pharmaceutical Industries Ltd. (India)

• Santen Pharmaceutical Co., Ltd. (Japan)

• Johnson & Johnson Vision (U.S.)

• Regeneron Pharmaceuticals, Inc. (U.S.)

• Roche Holding AG (Switzerland)

• Teva Pharmaceutical Industries Ltd. (Israel)

• Aurobindo Pharma Limited (India)

• Cipla Limited (India)

• FDC Limited (India)

• Akorn, Inc. (U.S.)

Latest Developments in Global Pterygium Drug Market

- In August 2022, researchers and ophthalmology centers reported increasing clinical adoption of topical anti-inflammatory and immunomodulatory therapies such as cyclosporine A as adjunct treatment following pterygium surgery, demonstrating improved outcomes in reducing recurrence rates and inflammation compared to conventional approaches

- In March 2023, clinical studies highlighted the growing use of anti-vascular endothelial growth factor (anti-VEGF) therapies and combination drug regimens alongside surgical excision, reflecting a shift toward pharmacological strategies aimed at minimizing recurrence and improving long-term treatment efficacy

- In July 2023, ophthalmology research initiatives emphasized the increasing utilization of mitomycin C-based adjunct drug therapy in pterygium management, with ongoing improvements in dosing protocols and delivery techniques to enhance safety while maintaining strong anti-fibrotic effects

- In April 2024, industry reports indicated accelerated development of novel drug delivery systems, including sustained-release ocular formulations and targeted topical therapies, aimed at improving drug bioavailability and reducing dosing frequency in pterygium treatment

- In June 2025, market analysis highlighted increased R&D investments by major ophthalmic pharmaceutical companies such as Alcon, Novartis, and Bausch Health to develop advanced anti-inflammatory and anti-fibrotic drug therapies, driving innovation and expanding the therapeutic pipeline for pterygium management

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.