Global Quick Commerce Fmcg Market

Market Size in USD Billion

USD

95.20 Billion

USD

437.44 Billion

2025

2033

USD

95.20 Billion

USD

437.44 Billion

2025

2033

| 2026 - 2033 | |

| USD 95.20 Billion | |

| USD 437.44 Billion | |

| % | |

|

Quick Commerce FMCG Market Overview

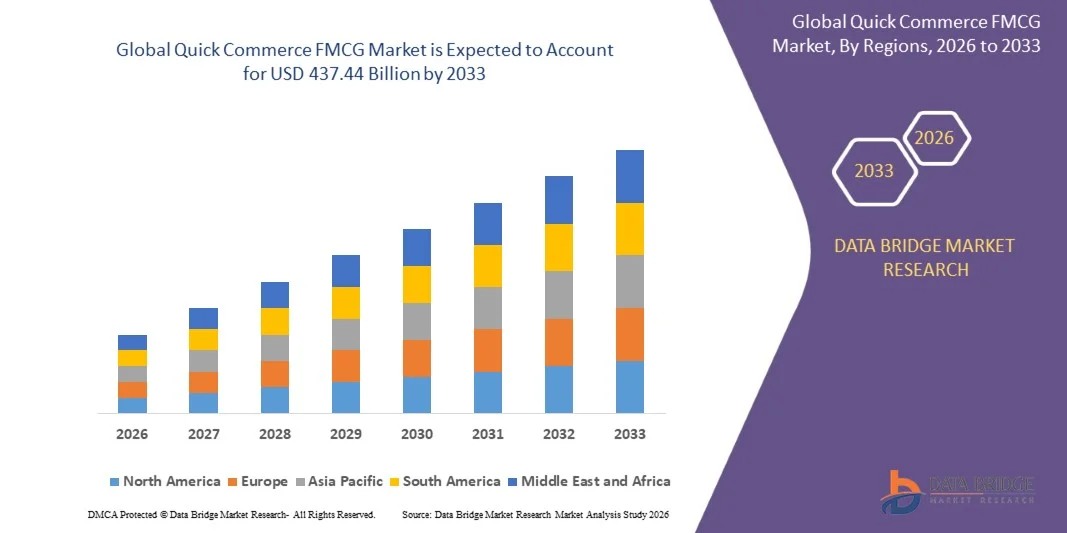

As per Data Bridge Market Research Analysis the quick commerce FMCG market was valued at USD 95.2 billion in 2025 and is projected to reach USD 437.44 billion by 2033, growing at a CAGR of 21% from 2026 to 2033. The market is experiencing consistent growth driven by rising demand for fast and convenient delivery of everyday consumer goods, rapid advancements in last-mile logistics technology and dark store infrastructure, and expanding applications across grocery, personal care, household essentials, and impulse-purchase categories.

The increasing pace of urbanization globally, combined with shifting consumer preferences toward on-demand delivery and stricter expectations around delivery speed and product availability, is compelling retailers, FMCG brands, and logistics platforms to adopt advanced quick commerce models. App-based and AI-powered fulfilment networks are replacing traditional retail and e-commerce channels in many markets, offering hyper-local, ultra-fast, and seamless purchasing environments for everyday consumer needs and last-minute household replenishment.

Market Size & Forecast

- Global Market Value (2025): USD 95.2 Billion

- Expected Market Value (2033): USD 437.44 Billion

- Forecast CAGR (2026–2033): 21%

- Leading Region in 2025: Asia-Pacific

- Fastest Growing Region: North America

Key Market Trends & Insights

- Asia-Pacific dominated the global quick commerce FMCG market with the largest revenue share of 38.62% in 2025, supported by high smartphone penetration, dense urban populations, and well-established dark store and micro-fulfilment infrastructure across China, India, and Southeast Asia.

- North America is expected to be the fastest-growing region at a CAGR of 18.4% from 2026 to 2033, fuelled by rising consumer demand for sub-30-minute delivery, increasing investments by major retail and grocery platforms, and rapid expansion of quick commerce players in Tier-1 and Tier-2 cities.

- The grocery & staples led the market with a 34.28% share in 2025, driven by high purchase frequency, perishability-driven urgency, and strong consumer preference for doorstep delivery of daily essentials.

- Personal care & beauty are the fastest-growing category, projected to register a CAGR of 21.3%, reflecting the surge in impulse-driven, app-based purchases and growing consumer reliance on quick commerce platforms for replenishment needs.

- The online segment dominated the channel category with a 62.45% revenue share in 2025, led by platform aggregators and direct-to-consumer FMCG brands leveraging AI-driven personalization and real-time inventory management.

- Instant delievery-based fulfilment accounted for 54.37% of the market share in 2025, preferred by quick commerce operators, FMCG brands, and logistics platforms that require hyper-local inventory positioning, faster pick-and-pack cycles, and optimized last-mile delivery performance.

Report Scope and Quick Commerce FMCG Market Segmentation

|

Attributes |

Quick Commerce FMCG Market Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Global Quick Commerce FMCG Market Trends

Trend: Growth in FMCG Brand Partnerships & Private Label Expansion

FMCG brands and quick commerce platforms are increasingly forging strategic partnerships to drive co-branded promotions, exclusive product launches, and priority shelf placement within dark store inventories. Leading platforms such as Blinkit, Zepto, and Swiggy Instamart are expanding their private label portfolios across grocery, personal care, and packaged food categories to improve margins and deepen consumer loyalty. The integration of real-time sales analytics enables precise assortment planning and dynamic restocking, while AI-driven personalization tools create tailored shopping experiences that closely replicate in-store browsing behavior through mobile-first interfaces.

Global Quick Commerce FMCG Market Dynamics

Key Market Driver: Surging Consumer Demand for Sub-30-Minute Delivery of Everyday Essentials

The rapid shift in consumer behaviour toward on-demand, instant gratification purchasing has created substantial demand for quick commerce platforms capable of delivering FMCG products within 10–30 minutes. The global quick commerce market was valued at approximately USD 95.2 billion in 2025 and is projected to grow to USD 437.44 billion by 2033, reflecting the accelerating adoption of dark store models, micro-fulfilment centers, and hyper-local inventory networks. FMCG brands, retail giants, and logistics-first startups are deploying quick commerce infrastructure as a core component of their omnichannel strategy, reducing dependency on traditional retail formats, compressing order-to-delivery cycles, and improving consumer retention through speed and convenience.

Key Restraint/Challenge: High Operational Costs and Unit Economics Pressure

A significant restraint in the global quick commerce FMCG market is the intense pressure on unit economics driven by high operational costs associated with dark store setup, last-mile delivery fleet management, rider incentives, and real-time inventory replenishment. Maintaining profitability at scale remains a critical challenge, as platforms must balance ultra-fast delivery commitments with rising fulfillment costs, high customer acquisition expenses, and thin FMCG margins. Smaller and emerging-market operators face additional barriers including fragmented supply chains, inconsistent cold-chain infrastructure, and regulatory uncertainty around gig-economy labor models, making sustainable scaling difficult without substantial external capital.

The rapid expansion and subsequent restructuring of platforms such as Dunzo in India and JOKR across Latin America illustrates the scale of financial commitment and operational discipline required for long-term viability in quick commerce, reflecting the broader challenge of achieving profitability beyond well-funded, high-density urban markets

Key Market Opportunity: Integration of AI and Hyper-Local Fulfilment Network Expansion

The integration of artificial intelligence in quick commerce FMCG operations presents a significant market opportunity. AI-enabled platforms can generate dynamic demand forecasts, optimize dark store inventory in real time, personalize product recommendations, and support large-scale route optimization for last-mile delivery fleets. The development of multi-category fulfilment ecosystems and app-based deployment models is further democratizing access to quick commerce, opening substantial growth opportunities across cost-sensitive and high-density markets in Asia-Pacific, Latin America, and the Middle East & Africa. India's quick commerce segment alone reported 113% year-over-year revenue growth in Q3 FY2025, underscoring the transformative potential of AI-powered, hyper-local fulfilment as the next frontier of FMCG retail.

Quick Commerce FMCG Market Scope

The global quick commerce FMCG market is segmented on the basis of product category, delivery payment, delivery and channel type.

- By Product Category

On the basis of product category, the global quick commerce FMCG market is segmented into grocery & staples, packaged food & snacks, and personal care & beauty. The Grocery & Staples segment dominated the market with a share of 38.45% in 2025, owing to high purchase frequency, daily consumption necessity, and strong consumer preference for doorstep delivery of perishable and non-perishable essentials. The widespread adoption of dark store models and micro-fulfillment centers has enabled platforms such as Blinkit, Zepto, and Getir to maintain real-time inventory of fresh produce, dairy, beverages, and household staples, ensuring consistent availability and ultra-fast replenishment. Additionally, increasing integration with AI-driven demand forecasting tools, dynamic pricing engines, and personalized recommendation systems is enhancing assortment planning, reducing wastage, and reinforcing the dominant position of the grocery & staples segment across global quick commerce markets.

The Packaged Food & Snacks segment is projected to register the fastest growth at a CAGR of 24.3% from 2026 to 2033, driven by rising impulse-purchase behavior, growing snacking culture across urban demographics, and increasing consumer reliance on quick commerce platforms for last-minute meal and snack replenishment. Advances in cold-chain micro-fulfillment infrastructure, combined with declining delivery costs and growing adoption across Tier-1 and Tier-2 cities in Asia-Pacific and Europe, are accelerating segment expansion.

- By Delivery Payment

On the basis of delivery payment, the global quick commerce FMCG market is segmented into online and cash. The Online Payment segment dominated the market with a share of 72.38% in 2025, supported by the rapid proliferation of digital wallets, UPI-based payment systems, buy-now-pay-later (BNPL) options, and integrated in-app checkout experiences across mobile-first quick commerce platforms. High adoption is driven by the increasing penetration of smartphones, rising consumer comfort with digital transactions, and seamless payment gateway integrations offered by platforms such as GoPuff, Swiggy Instamart, and Instacart. Additionally, growing investment by fintech providers, platform aggregators, and FMCG brands to enhance payment security, reduce checkout friction, and offer loyalty-linked digital payment incentives is reinforcing the leading position of the online payment segment in the global market.

The Cash on Delivery segment is expected to witness steady growth, particularly across emerging markets in South Asia, Southeast Asia, and the Middle East & Africa, where digital payment infrastructure remains underdeveloped and consumer trust in cash-based transactions remains high. Platforms operating in these regions continue to support cash payment options to drive user acquisition, expand addressable market reach, and reduce barriers to first-time adoption among price-sensitive and digitally underserved consumer segments.

- By Delivery

On the basis of delivery, the global quick commerce FMCG market is segmented into instant delivery. The Instant Delivery segment represents the defining operational pillar of the global quick commerce FMCG market, with platforms consistently targeting delivery windows of 10 to 30 minutes as the core value proposition differentiating quick commerce from traditional e-commerce and grocery delivery models. The global quick commerce market was valued at USD 244.7 billion in 2025 and is projected to reach USD 1,303.5 billion by 2033 at a CAGR of 23.5%, with instant delivery infrastructure — including hyper-local dark stores, AI-powered route optimization, and real-time rider dispatch systems — serving as the primary growth enabler. High adoption is supported by urban consumers, working professionals, and young digital-native demographics that prioritize speed, convenience, and reliability over cost, reinforcing the centrality of instant delivery across all quick commerce FMCG operations globally.

The instant delivery model is expected to witness continued acceleration through 2033, driven by increasing investments in autonomous last-mile delivery technologies, drone-based fulfillment pilots, and electric vehicle-powered delivery fleets. Additionally, the growing emphasis on sustainability, carbon-neutral logistics, and green delivery infrastructure is prompting leading platforms to innovate within the instant delivery space while maintaining speed and cost efficiency, further driving segment growth.

- By Channel Type

On the basis of channel type, the global quick commerce FMCG market is segmented into mobile application and web portal. The Mobile Application segment dominated the market with a share of 67.82% in 2025, due to its critical role in enabling seamless, on-the-go ordering experiences for urban consumers through intuitive UI/UX design, real-time order tracking, AI-driven product recommendations, and integrated loyalty and rewards programs. High adoption is driven by the exponential growth in smartphone penetration globally, increasing consumer preference for app-based shopping, and the ability of platforms to leverage push notifications, geo-targeted promotions, and personalized in-app experiences to drive repeat purchase behaviour. Additionally, established partnerships with mobile payment providers, FMCG brands, and logistics technology vendors are expanding platform reach, improving accessibility, and reinforcing the dominant position of the mobile application channel across global quick commerce markets.

The Web Portal segment is expected to witness the fastest CAGR of 19.8% from 2026 to 2033, driven by the increasing demand for flexible, multi-device ordering experiences among enterprise buyers, corporate procurement teams, and digitally active consumers who prefer browser-based interfaces for bulk or scheduled FMCG purchases. Growing investment by quick commerce platforms in responsive web design, cross-platform compatibility, and web-based loyalty integrations is enhancing the accessibility, reliability, and trust of web portal channels, further accelerating adoption across both B2C and B2B quick commerce segments.

Global Quick Commerce FMCG MarketRegional Analysis

Asia-Pacific dominated the global quick commerce FMCG market and accounted for the largest revenue share of 38.62% in 2025, supported by high smartphone penetration, dense urban populations, well-established dark store and micro-fulfilment infrastructure, and the strong presence of dominant regional platforms including Blinkit, Zepto, Swiggy Instamart, Meituan, and JD.com across China, India, and Southeast Asia. The region also benefits from rapidly expanding cold-chain logistics networks, favourable government policies supporting digital commerce, high consumer appetite for on-demand delivery, and growing FMCG brand investments in hyper-local fulfilment capabilities. Increasing focus on AI-powered inventory management, real-time route optimization, and app-based personalization continues to strengthen Asia-Pacific's leadership position in the global quick commerce FMCG market.

India Quick Commerce FMCG Market Insight

The India quick commerce FMCG market is experiencing exceptional growth, supported by rising adoption of app-based instant delivery platforms, rapid dark store network expansion across Tier-1 and Tier-2 cities, and a large, digitally engaged urban consumer base. Leading platforms including Blinkit, Zepto, and Swiggy Instamart are aggressively scaling their micro-fulfilment infrastructure, private label portfolios, and AI-driven demand forecasting capabilities to capture growing consumer demand for sub-30-minute delivery of grocery, personal care, and packaged food products. Furthermore, increasing investments by FMCG brands, venture capital firms, and strategic investors, combined with India's rapidly growing digital payments ecosystem and UPI adoption, are positioning India as one of the fastest-growing and most competitive quick commerce FMCG markets globally.

China Quick Commerce FMCG Market Insight

The China quick commerce FMCG market is growing rapidly, driven by increasing urbanization, expanding digital retail infrastructure, and rising consumer expectations for ultra-fast, reliable delivery of everyday essentials. Growing adoption of AI-enabled demand forecasting, automated fulfilment systems, and integrated super-app ecosystems — led by platforms such as Meituan, Ele.me, and Alibaba's Freshippo — is significantly boosting market demand across grocery, personal care, and packaged food categories. In addition, rising investments in autonomous delivery technologies, drone-based last-mile fulfilment pilots, and real-time inventory optimization platforms are positioning China as one of the most technologically advanced and fastest-scaling quick commerce FMCG markets globally, with the Asia-Pacific region alone contributing nearly 52% of regional digital commerce transaction volume in 2025.

U.S. Quick Commerce FMCG Market Insight

The U.S. quick commerce FMCG market is witnessing strong growth, with North America dominating the global market with a share of 33.43% in 2025, driven by rising consumer demand for on-demand delivery of grocery and household essentials, increasing investments by platforms such as GoPuff, DoorDash, Instacart, and Uber Eats in dark store expansion and AI-powered fulfilment infrastructure, and growing penetration of quick commerce across metropolitan and suburban markets. The country's mature digital retail ecosystem, combined with increasing adoption of subscription-based delivery models, BNPL payment options, and real-time inventory management technologies, is driving demand across consumer, corporate, and enterprise quick commerce applications. In addition, growing emphasis on reducing food waste, improving supply chain transparency, and enhancing last-mile delivery sustainability is accelerating platform innovation and market growth across the U.S.

Europe Quick Commerce FMCG Market Insight

The Europe quick commerce FMCG market is expanding steadily, with the region generating USD 54.90 billion in 2025 and anticipated to reach USD 115.40 billion by 2033, supported by the strong presence of established quick commerce operators including Getir, Flink, Glovo, Deliveroo, and Delivery Hero across key markets such as the U.K., Germany, Spain, and the Netherlands. The region benefits from high digital payment adoption, well-developed urban logistics infrastructure, and increasing consumer preference for convenience-driven FMCG purchasing. Continuous advancements in dark store operations, AI-driven assortment optimization, and sustainable last-mile delivery models, along with growing regulatory focus on gig-economy worker protections and green logistics, are further driving market growth across European markets.

U.K. Quick Commerce FMCG Market Insight

The U.K. quick commerce FMCG market is experiencing steady growth, supported by rising adoption of instant delivery platforms across major urban centres including London, Manchester, and Birmingham, and increasing consumer demand for fast, reliable delivery of grocery, personal care, and packaged food products. Leading platforms including Deliveroo, Zapp, and Getir are expanding their dark store footprints and FMCG product assortments to capture growing consumer appetite for sub-30-minute delivery. Furthermore, integration of AI-powered demand forecasting, real-time route optimization, and app-based loyalty programs is improving platform efficiency and consumer retention, positioning the U.K. as a key innovation and growth hub in the European quick commerce FMCG industry.

Germany Quick Commerce FMCG Market Insight

The Germany quick commerce FMCG market is expanding steadily due to the country's strong digital retail infrastructure, high consumer spending on FMCG categories, and increasing adoption of next-generation quick commerce fulfilment technologies. Platforms including Flink and Delivery Hero are increasingly investing in dark store network expansion, private label development, and AI-driven inventory management systems to meet growing consumer demand for ultra-fast delivery of everyday essentials. Continuous advancements in sustainable last-mile logistics, electric vehicle-powered delivery fleets, and real-time consumer analytics, along with strong government focus on digital commerce innovation and consumer protection, are further driving market growth in Germany.

Quick Commerce FMCG Market Share

The quick commerce FMCG industry is primarily led by well-established companies, including:

- Getir (Turkey)

- Blinkit (India)

- GoPuff (U.S.)

- Flink (Germany)

- Swiggy Instamart (India)

- Zapp (U.K.)

- Dunzo (India)

- Glovo (Spain)

- Zepto (India)

- JOKR (U.S.)

- Alibaba – Freshippo / Hema, Ele.me (China)

- BigBasket – BB Now (India)

- Deliveroo (U.K.)

- Delivery Hero – incl. Glovo, Foodora (Germany)

- DoorDash (U.S.)

- Flipkart Minutes (India)

- Instacart (U.S.)

- JD.com (China)

- Meituan (China)

- Uber Eats (U.S.)

Latest Developments in Quick Commerce FMCG Market

- In In March 2026, Blinkit (India) announced the expansion of its dark store network to over 1,000 locations across 50+ Indian cities, reinforcing its position as India's leading quick commerce FMCG platform. The expansion is supported by AI-powered demand forecasting, real-time inventory replenishment systems, and an enhanced private label product portfolio spanning grocery, personal care, and packaged food categories. This strategic scale-up strengthens Blinkit's operational infrastructure and accelerates its ability to deliver sub-10-minute FMCG fulfillment across Tier-1 and Tier-2 urban markets, further consolidating its market leadership in the Indian quick commerce ecosystem.

- In January 2026, Zepto (India) raised a significant funding round to accelerate its dark store expansion, technology infrastructure investment, and private label FMCG portfolio development across major Indian metropolitan markets. The company deepened its integration of AI-driven route optimization, real-time consumer analytics, and hyper-local assortment planning tools to improve delivery speed, reduce operational costs, and enhance consumer personalization. This development reinforces Zepto's position as one of the fastest-growing quick commerce FMCG platforms globally, with a growing focus on profitability, unit economics optimization, and sustainable last-mile delivery operations.

- In November 2025, DoorDash (U.S.) expanded its quick commerce FMCG capabilities through the launch of enhanced dark store partnerships and an upgraded instant delivery infrastructure across major U.S. metropolitan markets. The platform integrated advanced AI-powered demand prediction, real-time inventory visibility, and expanded FMCG category assortments — including grocery, personal care, and household essentials — into its DashMart fulfillment network. This development strengthens DoorDash's competitive positioning in the U.S. quick commerce FMCG market, enabling faster delivery windows, improved order accuracy, and broader consumer reach across suburban and urban delivery zones.

- In October 2025, Meituan (China) launched an upgraded AI-powered fulfillment platform for its quick commerce FMCG operations, integrating real-time demand forecasting, automated dark store replenishment, and drone-assisted last-mile delivery capabilities across key Chinese urban markets. The platform leverages machine learning algorithms to optimize product assortment, reduce delivery times, and enhance consumer personalization across grocery, packaged food, and personal care categories. This advancement reinforces Meituan's dominance in the China quick commerce FMCG market, with the country's quick commerce sector projected to reach USD 94.81 billion by 2025, growing at 7.5% annually through 2029.

- In August 2025, Getir (Turkey) announced a strategic restructuring and market refocusing initiative, concentrating its quick commerce FMCG operations on its highest-performing markets across Europe and the Middle East while investing in technology upgrades, dark store efficiency improvements, and FMCG category expansion. The company enhanced its AI-driven inventory management systems, real-time delivery tracking capabilities, and consumer loyalty programs to strengthen platform retention and improve unit economics. This strategic realignment positions Getir to achieve sustainable growth in its core markets while maintaining its status as one of the pioneering global quick commerce FMCG operators.

- In June 2025, Instacart (U.S.) expanded its quick commerce FMCG capabilities through the launch of new retail media and AI-powered personalization tools, enabling FMCG brands to deliver targeted, real-time promotions to consumers during the purchase journey. The platform also deepened integrations with major U.S. grocery and FMCG retail partners, enhancing product assortment depth, improving delivery speed, and expanding its fulfillment footprint across suburban U.S. markets. These developments reinforce Instacart's position as a leading quick commerce FMCG enablement platform, with a market valuation of USD 9.6 billion, and accelerate its growth across both B2C and retail media monetization channels.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.