Global Radiation Dose Optimisation Software Market

Market Size in USD Million

USD

241.76 Million

USD

682.44 Million

2025

2033

USD

241.76 Million

USD

682.44 Million

2025

2033

| 2026 - 2033 | |

| USD 241.76 Million | |

| USD 682.44 Million | |

| % | |

|

Radiation Dose Optimisation Software Market Size

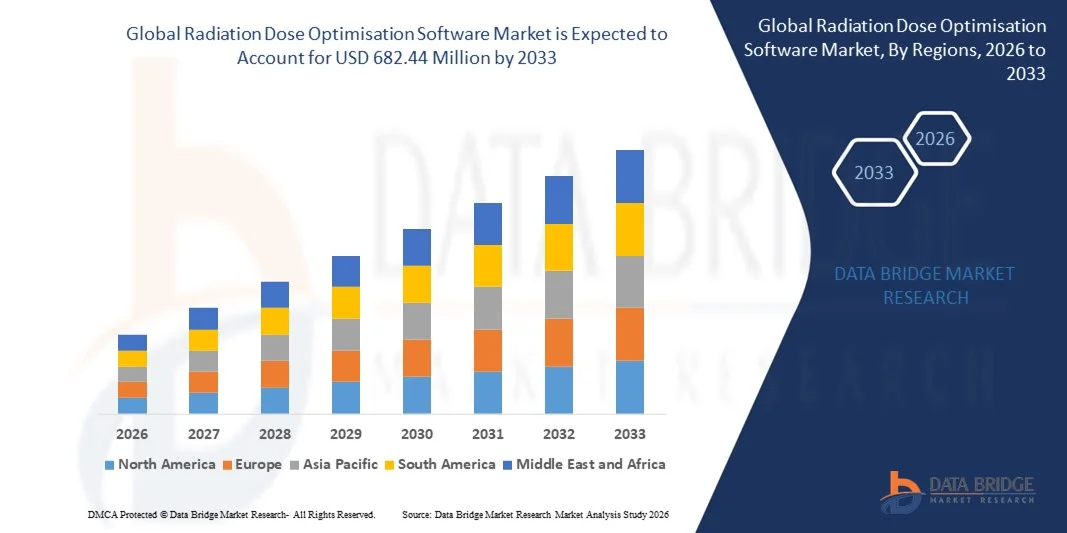

- The global radiation dose optimisation software market size was valued at USD 241.76 million in 2025 and is expected to reach USD 682.44 million by 2033, at a CAGR of 13.85% during the forecast period

- The market growth is largely fuelled by the rising adoption of diagnostic imaging procedures such as CT scans, fluoroscopy, and interventional radiology, increasing the need to monitor and reduce radiation exposure

- Increasing regulatory emphasis on patient safety and radiation dose monitoring, along with stringent healthcare compliance requirements, is accelerating the adoption of dose optimisation software

Radiation Dose Optimisation Software Market Analysis

- The market is witnessing strong demand due to the increasing focus of healthcare providers on improving patient safety, enhancing imaging quality, and ensuring compliance with radiation safety standards

- Continuous technological advancements, including cloud-based platforms and AI-driven dose management systems, are improving workflow efficiency and supporting widespread adoption across hospitals and diagnostic imaging centres

- North America dominated the radiation dose optimisation software market with the largest revenue share in 2025, driven by the strong presence of advanced healthcare infrastructure, increasing adoption of diagnostic imaging systems, and strict regulatory requirements for radiation safety

- Asia-Pacific region is expected to witness the highest growth rate in the global radiation dose optimisation software market, driven by increasing healthcare investments, rising adoption of advanced imaging technologies, and government initiatives supporting digital healthcare transformation

- The Software segment held the largest market revenue share in 2025 driven by the increasing adoption of dedicated dose monitoring platforms that enable real-time tracking, analysis, and reporting of radiation exposure. These software solutions help healthcare providers improve patient safety, ensure regulatory compliance, and optimise imaging protocols, making them essential for modern radiology departments

Report Scope and Radiation Dose Optimisation Software Market Segmentation

|

Attributes |

Radiation Dose Optimisation Software Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Radiation Dose Optimisation Software Market Trends

Increasing Adoption Of AI-Enabled And Cloud-Based Dose Management Solutions

- The growing integration of artificial intelligence and cloud computing is significantly shaping the radiation dose optimisation software market, as healthcare providers increasingly seek automated tools to monitor, analyse, and reduce patient radiation exposure. These solutions help improve diagnostic accuracy, enhance workflow efficiency, and ensure compliance with radiation safety standards. This trend strengthens adoption across hospitals, imaging centres, and diagnostic facilities, encouraging vendors to develop advanced and scalable software platforms

- Rising demand for efficient radiology workflow management and patient safety has accelerated the implementation of dose optimisation software in CT, fluoroscopy, and interventional imaging procedures. Healthcare providers are actively investing in digital health technologies to enhance operational efficiency and reduce risks associated with excessive radiation exposure. This has also led to collaborations between software developers and healthcare institutions to improve system integration and clinical performance

- Digital transformation in healthcare and the shift toward cloud-based infrastructure are influencing purchasing decisions, with organisations prioritising scalable, real-time, and remote-accessible dose monitoring platforms. These factors are helping healthcare providers improve compliance reporting, optimise imaging protocols, and enhance patient care outcomes. Companies are increasingly emphasising interoperability and analytics capabilities to strengthen their competitive positioning and expand adoption

- For instance, in 2024, GE HealthCare in the U.S. and Siemens Healthineers in Germany expanded their radiation dose management software portfolios with advanced analytics and cloud-enabled features. These solutions were introduced to help healthcare providers improve dose tracking, regulatory compliance, and workflow efficiency. The platforms were widely implemented across hospitals and diagnostic centres, improving operational efficiency and patient safety

- While adoption of radiation dose optimisation software is increasing, sustained market growth depends on continuous technological innovation, integration with imaging equipment, and cost-effective deployment. Software providers are focusing on enhancing AI capabilities, improving interoperability, and ensuring compliance with evolving regulatory standards to support broader implementation

Radiation Dose Optimisation Software Market Dynamics

Driver

Increasing Focus On Patient Safety And Radiation Exposure Monitoring

- Growing emphasis on patient safety and radiation protection is a major driver for the radiation dose optimisation software market. Healthcare providers are increasingly adopting dose monitoring solutions to minimise radiation risks, ensure regulatory compliance, and improve diagnostic accuracy. This trend is also encouraging investment in advanced dose management technologies and analytics platforms

- Expanding use of diagnostic imaging procedures such as CT scans, mammography, and fluoroscopy is influencing market growth. Radiation dose optimisation software helps healthcare providers monitor exposure levels, optimise imaging protocols, and improve patient outcomes. The increasing prevalence of chronic diseases and the rising need for diagnostic imaging are further strengthening demand

- Healthcare organisations are actively implementing dose management solutions through digital transformation initiatives, regulatory compliance programs, and patient safety strategies. These efforts are supported by increasing government regulations and quality standards related to radiation safety. Partnerships between healthcare providers and software companies are also improving system capabilities and adoption rates

- For instance, in 2023, Philips Healthcare in the Netherlands and Canon Medical Systems Corporation in Japan expanded their dose management software integration with imaging systems. This expansion followed rising demand for automated radiation monitoring and compliance solutions. Both companies highlighted improved patient safety and workflow efficiency as key benefits

- Although increasing patient safety initiatives support market growth, widespread adoption depends on cost considerations, system integration, and training requirements. Continued investment in healthcare IT infrastructure and advanced analytics will be essential to sustain long-term market expansion

Restraint/Challenge

High Implementation Costs And Integration Complexity

- The high cost of implementing radiation dose optimisation software remains a key challenge, particularly for small and mid-sized healthcare facilities. Initial investment, software licensing, and infrastructure upgrades contribute to increased financial burden. Integration with existing imaging systems can also increase operational complexity

- Limited technical expertise and training requirements can restrict adoption, particularly in developing healthcare systems. Healthcare providers may face challenges in implementing, managing, and maintaining advanced dose monitoring platforms. This can slow adoption rates and delay digital transformation initiatives

- System compatibility and interoperability challenges also impact market growth, as healthcare facilities use multiple imaging devices and IT systems. Ensuring seamless integration and consistent performance requires additional investment and technical support. Data security and compliance requirements further add to implementation complexity

- For instance, in 2024, healthcare providers in India and Brazil reported slower adoption due to high implementation costs and integration challenges with legacy imaging systems. Budget constraints and lack of skilled professionals were additional barriers. These factors also limited adoption among smaller diagnostic centres

- Overcoming these challenges will require cost-effective software solutions, improved interoperability, and enhanced training programs. Collaboration between software providers, healthcare organisations, and regulatory bodies can help support adoption. Furthermore, advancements in cloud-based deployment and scalable platforms will be critical to improving accessibility and supporting long-term growth of the global radiation dose optimisation software market

Radiation Dose Optimisation Software Market Scope

The market is segmented on the basis of component, modality, application, and end-user.

- By Component

On the basis of component, the radiation dose optimisation software market is segmented into Software, Automatic, Manual, Services, Education & Training, and Support. The Software segment held the largest market revenue share in 2025 driven by the increasing adoption of dedicated dose monitoring platforms that enable real-time tracking, analysis, and reporting of radiation exposure. These software solutions help healthcare providers improve patient safety, ensure regulatory compliance, and optimise imaging protocols, making them essential for modern radiology departments.

The Services segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the rising demand for implementation, integration, training, and maintenance services. Healthcare facilities increasingly rely on service providers to ensure efficient deployment, system optimisation, and staff training, which helps maximise the effectiveness and usability of dose optimisation solutions.

- By Modality

On the basis of modality, the radiation dose optimisation software market is segmented into Computed Tomography and Nuclear Medicine. The Computed Tomography segment held the largest market revenue share in 2025 driven by the high volume of CT imaging procedures and the relatively higher radiation doses associated with CT scans. Dose optimisation software plays a critical role in monitoring and reducing radiation exposure while maintaining diagnostic image quality, supporting its widespread adoption in CT imaging.

The Nuclear Medicine segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing use of nuclear imaging for disease diagnosis and treatment monitoring. The need for accurate dose tracking and regulatory compliance is encouraging healthcare providers to implement advanced dose management solutions in nuclear medicine applications.

- By Application

On the basis of application, the radiation dose optimisation software market is segmented into Oncology, Cardiology, and Orthopaedic. The Oncology segment held the largest market revenue share in 2025 driven by the extensive use of imaging procedures such as CT scans and nuclear imaging for cancer diagnosis, treatment planning, and monitoring. Dose optimisation software helps minimise radiation risks for cancer patients who require repeated imaging, supporting its strong adoption in oncology.

The Cardiology segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing use of fluoroscopy and interventional imaging in cardiac procedures. Healthcare providers are adopting dose optimisation software to improve patient safety and ensure optimal radiation management during complex cardiovascular interventions.

- By End-User

On the basis of end-user, the radiation dose optimisation software market is segmented into Hospitals and Others. The Hospitals segment held the largest market revenue share in 2025 driven by the high volume of diagnostic imaging procedures and the availability of advanced imaging infrastructure. Hospitals are major adopters of dose optimisation software as they prioritise patient safety, regulatory compliance, and workflow efficiency.

The Others segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing adoption of dose management solutions in diagnostic imaging centres and specialty clinics. These facilities are implementing advanced software to enhance imaging safety, improve operational efficiency, and comply with evolving radiation safety standards.

Radiation Dose Optimisation Software Market Regional Analysis

- North America dominated the radiation dose optimisation software market with the largest revenue share in 2025, driven by the strong presence of advanced healthcare infrastructure, increasing adoption of diagnostic imaging systems, and strict regulatory requirements for radiation safety

- Healthcare providers in the region highly prioritise patient safety, regulatory compliance, and workflow efficiency, encouraging the adoption of advanced dose monitoring and optimisation platforms across hospitals and imaging centres

- This widespread adoption is further supported by high healthcare spending, rapid digital transformation, and the presence of leading medical technology companies, establishing radiation dose optimisation software as an essential solution for modern radiology practices

U.S. Radiation Dose Optimisation Software Market Insight

The U.S. radiation dose optimisation software market captured the largest revenue share in 2025 within North America, fuelled by the rapid adoption of healthcare IT solutions and increasing use of diagnostic imaging procedures. Healthcare providers are increasingly focusing on improving patient safety and ensuring compliance with radiation exposure regulations. The growing integration of AI-based imaging platforms, cloud-enabled dose monitoring systems, and advanced analytics tools is further accelerating market growth. In addition, strong government regulations and continuous technological innovation are supporting widespread adoption across healthcare facilities.

Europe Radiation Dose Optimisation Software Market Insight

Europe is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by strict regulatory frameworks related to radiation protection and increasing focus on patient safety. The rising adoption of digital healthcare technologies and increasing imaging volumes are encouraging healthcare providers to implement dose optimisation software. In addition, growing investments in healthcare infrastructure and increasing awareness regarding radiation exposure risks are supporting regional market expansion across hospitals and diagnostic centres.

U.K. Radiation Dose Optimisation Software Market Insight

The U.K. radiation dose optimisation software market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing adoption of digital radiology solutions and strong regulatory emphasis on radiation safety. Healthcare providers are actively implementing dose monitoring platforms to enhance patient care and improve compliance. In addition, the country’s advanced healthcare system and growing adoption of AI-enabled medical technologies are supporting market growth.

Germany Radiation Dose Optimisation Software Market Insight

The Germany radiation dose optimisation software market is expected to witness the fastest growth rate from 2026 to 2033, fuelled by increasing focus on advanced medical imaging and patient safety. Germany’s well-established healthcare infrastructure and strong emphasis on technological innovation are promoting adoption of advanced dose management solutions. In addition, increasing integration of digital health platforms and regulatory compliance requirements are further contributing to market expansion.

Asia-Pacific Radiation Dose Optimisation Software Market Insight

The Asia-Pacific radiation dose optimisation software market is expected to witness the fastest growth rate from 2026 to 2033, driven by expanding healthcare infrastructure, increasing diagnostic imaging volumes, and rising awareness regarding radiation safety. The region’s growing adoption of advanced healthcare IT systems, supported by government initiatives and healthcare modernisation programs, is accelerating market growth. In addition, the increasing number of hospitals and diagnostic centres is contributing to wider adoption.

Japan Radiation Dose Optimisation Software Market Insight

The Japan radiation dose optimisation software market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s advanced healthcare technologies and strong focus on patient safety. Healthcare providers are increasingly implementing advanced dose monitoring systems to improve diagnostic efficiency and reduce radiation risks. In addition, increasing adoption of AI-based imaging technologies and digital healthcare platforms is supporting market growth.

China Radiation Dose Optimisation Software Market Insight

The China radiation dose optimisation software market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rapid healthcare infrastructure development and increasing adoption of diagnostic imaging systems. China is emerging as a major healthcare technology market, with hospitals increasingly implementing advanced software solutions to improve patient safety and operational efficiency. The growing focus on healthcare modernisation and digital transformation is further accelerating market expansion.

Radiation Dose Optimisation Software Market Share

The Radiation Dose Optimisation Software industry is primarily led by well-established companies, including:

- Bayer AG (Germany)

- General Electric Company (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Siemens Healthcare GmbH (Germany)

- FUJIFILM Holdings Corporation (Japan)

- Canon Inc. (Japan)

- PACSHealth, LLC (U.S.)

- Sectra AB (Sweden)

- Bracco Imaging S.p.A (Italy)

- Qaelum (Belgium)

- Agfa-Gevaert Group (Belgium)

- Novarad Corporation (U.S.)

- Volpara Health Limited (New Zealand)

- Guerbet (France)

- Medsquare (France)

- Medic Vision Imaging Solutions, Ltd (Israel)

- INFINITT Healthcare Co., Ltd (South Korea)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.