Global Radiation Therapy For Head And Neck Cancer Market

Market Size in USD Billion

USD

1.10 Billion

USD

1.85 Billion

2025

2033

USD

1.10 Billion

USD

1.85 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.10 Billion | |

| USD 1.85 Billion | |

| % | |

|

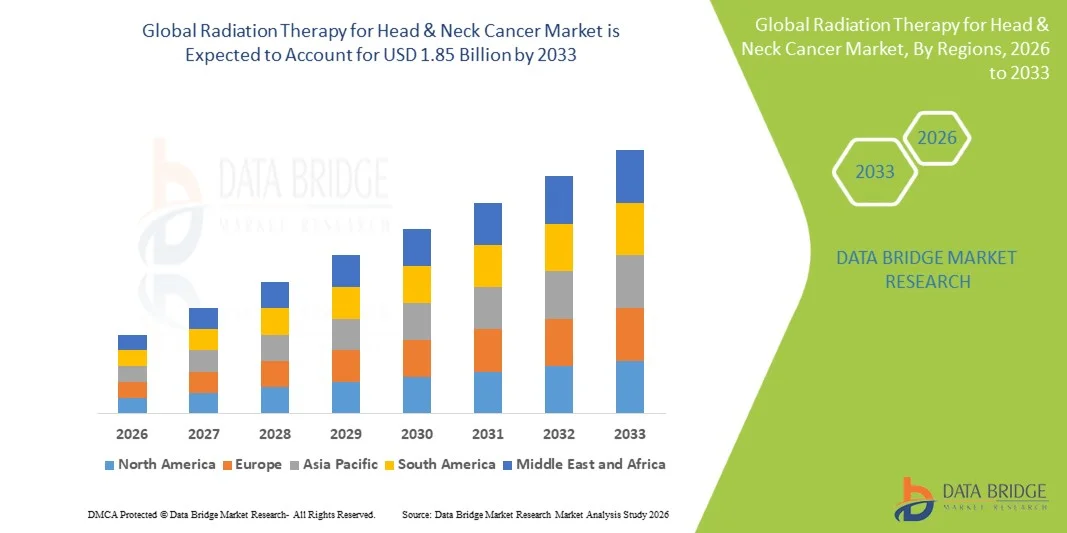

Radiation Therapy for Head & Neck Cancer Market Size

- The global radiation therapy for head & neck cancer market size was valued at USD 1.10 billion in 2025and is expected to reach USD 1.85 billion by 2033, at a CAGR of 6.0% during the forecast period

- Market growth is primarily driven by the rising incidence of head and neck cancers, particularly linked to tobacco use, alcohol consumption, and HPV-related oropharyngeal cancers, along with increasing adoption of advanced precision radiotherapy techniques

- In addition, the shift toward organ-preserving cancer treatments, growing use of image-guided and adaptive radiotherapy systems, and improvements in treatment planning accuracy and survival outcomes are significantly supporting market expansion

Radiation Therapy for Head & Neck Cancer Market Analysis

- Radiation therapy plays a critical role in the treatment of head and neck cancers due to its ability to target tumors precisely while preserving surrounding healthy tissues, especially in anatomically complex regions such as the oral cavity and larynx.

- The demand is strongly influenced by the rising burden of oral, oropharyngeal, and nasopharyngeal cancers, with HPV-associated cancers showing a notable increase globally

- Technological evolution in radiotherapy—particularly LINAC-based systems, IGRT, and adaptive radiotherapy platforms—has improved treatment precision, reduced toxicity, and enhanced patient outcomes

- North America dominated the global radiation therapy for head & neck cancer market in 2025, accounting for the largest revenue share of 38.7%, supported by advanced cancer care infrastructure, high adoption of precision radiotherapy systems, and a strong presence of leading oncology technology providers

- Asia-Pacific is expected to be the fastest-growing region in the global radiation therapy for head & neck cancer market due to rising cancer incidence, expanding healthcare access, and government investments in oncology infrastructure

- External Beam Radiation Therapy (EBRT) dominated the global radiation therapy for head & neck cancer market, accounting for the largest share of 70.8% in 2025, driven by its widespread clinical adoption, high precision in tumor targeting, and effectiveness in treating a wide range of head & neck cancers in both curative and palliative settings

Report Scope and Radiation Therapy for Head & Neck Cancer Market Segmentation

|

Attributes |

Radiation Therapy for Head & Neck Cancer Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· Expansion of proton therapy and heavy ion therapy centers · Growing adoption of AI-powered treatment planning systems · Increasing demand for hypofractionated and personalized radiotherapy protocols |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Radiation Therapy for Head & Neck Cancer Market Trends

“Shift Toward Precision, Image-Guided, and Adaptive Radiotherapy”

- A key trend shaping the radiation therapy for head & neck cancer market is the shift toward high-precision radiation delivery systems that minimize damage to surrounding critical structures such as salivary glands, spinal cord, and oral tissues

- Technologies such as IGRT, adaptive radiotherapy, and MRI-guided radiotherapy are increasingly being adopted to dynamically adjust treatment based on tumor response and anatomical changes

- The rise of proton therapy systems is improving dose conformity, especially in pediatric and complex head & neck cancer cases

- Integration of AI-driven treatment planning software is improving workflow efficiency, dose optimization, and clinical decision-making

- There is increasing focus on hypofractionated radiotherapy, reducing treatment sessions while maintaining clinical effectiveness

- Growing emphasis on patient quality of life and functional preservation (speech, swallowing, and aesthetics) is shaping treatment strategies

Radiation Therapy for Head & Neck Cancer Market Dynamics

Driver

“Rising Incidence of Head & Neck Cancers and Technological Advancements”

- Increasing prevalence of head and neck cancers driven by tobacco consumption, alcohol use, and HPV infections is a major growth driver

- For instance, HPV-positive oropharyngeal cancers are rising globally, particularly in younger populations, increasing demand for advanced radiotherapy solutions

- Advancements in LINAC systems, proton therapy, and image-guided radiotherapy are improving survival outcomes and reducing side effects

- Growing adoption of organ-preserving cancer treatment strategies is increasing reliance on precision radiation therapy

- Expanding oncology infrastructure in emerging markets is improving access to advanced radiotherapy systems

Restraint/Challenge

“High Cost of Advanced Radiotherapy Systems and Limited Access in Developing Regions”

- High installation and maintenance costs of proton therapy and MRI-guided systems limit adoption in low- and middle-income countries

- Complex infrastructure requirements, including radiation shielding and specialized facilities, increase capital investment burden

- Shortage of trained radiation oncologists and medical physicists impacts optimal utilization of advanced systems

- Variability in reimbursement policies across regions further restricts patient access to advanced therapies

- Limited awareness and late-stage diagnosis in some regions reduce treatment effectiveness and adoption rates

Radiation Therapy for Head & Neck Cancer Market Scope

The market is segmented on the basis of type of radiation therapy, technology, cancer type, and end user.

- By Type of Radiation Therapy

On the basis of type of radiation therapy, the global radiation therapy for head & neck cancer market is segmented into External Beam Radiation Therapy (EBRT), Internal Radiation Therapy (Brachytherapy), and Systemic Radiation Therapy. The EBRT segment dominated the market with a market share of 70.8% in 2025, driven by its widespread clinical adoption, high precision in tumor targeting, and strong effectiveness in treating a wide range of head & neck cancers. EBRT is widely preferred due to its non-invasive nature, ability to spare surrounding healthy tissues, and compatibility with advanced techniques such as IMRT and IGRT.

The systemic radiation therapy segment is expected to witness the fastest growth during the forecast period, driven by its expanding clinical application in advanced and metastatic head & neck cancer cases where localized radiation alone is insufficient. Increasing research into targeted radionuclide therapies and combination approaches with immunotherapy is further supporting the adoption of systemic radiation therapy. In addition, its potential in improving outcomes for recurrent and treatment-resistant cancers is contributing to growing clinical interest and future market expansion.

- By Technology Segment

On the basis of technology, the global radiation therapy for head & neck cancer market is segmented into Linear Accelerators (LINAC-based systems), Proton Therapy Systems, Tomotherapy systems, Image-Guided Radiotherapy (IGRT systems), Adaptive radiotherapy platforms, and MRI-guided radiation therapy. The LINAC-based systems segment dominated the market in 2025, driven by its extensive global installation base, cost-effectiveness, and widespread clinical use across hospitals and cancer centers.

The proton therapy systems segment is expected to witness the fastest growth during the forecast period, driven by superior dose precision, reduced toxicity to surrounding tissues, and increasing adoption in complex head & neck cancer cases. Growing investments in proton therapy facilities and rising clinical evidence supporting better long-term outcomes are further accelerating segment expansion.

- By Cancer Type

On the basis of cancer type, the global radiation therapy for head & neck cancer market is segmented into oral cavity cancer, oropharyngeal cancer (HPV-driven cases), laryngeal cancer, nasopharyngeal cancer, hypopharyngeal cancer, and salivary gland tumors. The oropharyngeal cancer segment dominated the market in 2025, driven by the rising incidence of HPV-related cases and strong reliance on radiation therapy for organ preservation.

The nasopharyngeal cancer segment is expected to witness the fastest growth during the forecast period, supported by higher prevalence in Asia-Pacific regions, increasing awareness, and improving access to advanced radiotherapy technologies that enhance treatment precision and survival outcomes.

- By End User

On the basis of end user, the global radiation therapy for head & neck cancer market is segmented into hospitals, cancer specialty centers, ambulatory radiotherapy centers, and academic & research institutes. The hospitals segment dominated the market in 2025, driven by high patient inflow, availability of advanced radiotherapy infrastructure, and integrated oncology departments.

The ambulatory radiotherapy centers segment is expected to witness the fastest growth during the forecast period, driven by the rising shift toward outpatient cancer care, increasing demand for cost-effective treatment settings, and expanding availability of compact and advanced radiation therapy systems outside hospital environments.

Radiation Therapy for Head & Neck Cancer Market Regional Analysis

- North America dominated the global radiation therapy for head & neck cancer market in 2025, accounting for the largest revenue share of 38.7%, supported by advanced cancer care infrastructure, high adoption of precision radiotherapy systems, and a strong presence of leading oncology technology providers

- The region benefits from strong reimbursement frameworks and favorable insurance coverage for advanced cancer treatments, which significantly improve patient access to high-cost radiotherapy technologies

- Increasing prevalence of head & neck cancers, particularly HPV-associated oropharyngeal cancers, along with high awareness of early diagnosis and screening programs, is further supporting sustained demand for radiation therapy across the region

U.S. Radiation Therapy for Head & Neck Cancer Market Insight

The U.S. radiation therapy for head & neck cancer market is driven by a high burden of head and neck cancers, particularly HPV-related oropharyngeal cases, along with strong access to advanced oncology care. The country’s well-established healthcare infrastructure, widespread adoption of precision radiotherapy technologies such as LINAC-based systems, IGRT, and proton therapy, and strong reimbursement support are key factors driving market growth. In addition, increasing use of outpatient cancer care and continuous technological advancements in treatment planning and delivery are further strengthening market expansion in the U.S.

Europe Radiation Therapy for Head & Neck Cancer Market Insight

The Europe radiation therapy for head & neck cancer market is experiencing steady growth, driven by the rising incidence of head and neck cancers and increasing adoption of advanced precision radiotherapy technologies. The region benefits from well-established public healthcare systems, strong emphasis on early cancer diagnosis, and widespread availability of modern treatment facilities. Growing utilization of techniques such as IMRT, IGRT, and adaptive radiotherapy is improving treatment outcomes while reducing side effects. In addition, supportive reimbursement policies and increasing investments in oncology infrastructure are further contributing to the expansion of radiation therapy adoption across major European countries.

U.K. Radiation Therapy for Head & Neck Cancer Market Insight

The U.K. radiation therapy for head & neck cancer market is growing steadily, supported by strong national cancer care programs and increasing focus on early diagnosis and effective treatment of head and neck cancers. The presence of a well-structured public healthcare system enables wide access to advanced radiotherapy techniques, including IMRT and IGRT, across major treatment centers. Rising incidence of HPV-related oropharyngeal cancers and growing emphasis on organ-preserving treatment approaches are further driving demand. In addition, continuous upgrades in radiotherapy infrastructure and expanding use of outpatient oncology services are strengthening market growth in the country.

Germany Radiation Therapy for Head & Neck Cancer Market Insight

The Germany radiation therapy for head & neck cancer market is witnessing steady growth, supported by strong healthcare infrastructure and a high focus on advanced cancer treatment technologies. The country’s emphasis on precision medicine and early cancer detection is driving the adoption of advanced radiotherapy systems such as LINAC-based platforms, IGRT, and adaptive radiotherapy. Increasing prevalence of head and neck cancers, along with rising demand for organ-preserving treatment approaches, is further supporting market expansion. In addition, continuous investments in oncology research and integration of innovative treatment planning systems are enhancing the efficiency and accuracy of radiation therapy across Germany.

Asia-Pacific Radiation Therapy for Head & Neck Cancer Market Insight

The Asia-Pacific radiation therapy for head & neck cancer market is witnessing rapid growth, driven by the rising incidence of head and neck cancers, increasing exposure to risk factors such as tobacco use and air pollution, and improving access to oncology care. Expanding healthcare infrastructure, particularly in countries such as China, India, and Japan, is accelerating the adoption of advanced radiotherapy technologies including LINAC-based systems, IGRT, and proton therapy. Growing government initiatives to strengthen cancer diagnosis and treatment capabilities, along with rising healthcare expenditure and awareness about early cancer detection, are further supporting market expansion across the region.

Japan Radiation Therapy for Head & Neck Cancer Market Insight

The Japan radiation therapy for head & neck cancer market is growing steadily, supported by a rapidly aging population and a relatively high prevalence of head and neck cancers. The country’s strong focus on advanced healthcare technologies is driving the adoption of precision radiotherapy systems such as LINAC-based platforms, IGRT, and MRI-guided radiotherapy. Increasing emphasis on minimally invasive, organ-preserving cancer treatments is further supporting demand for radiation therapy. In addition, well-established hospital infrastructure, strong integration of innovation in clinical oncology practices, and ongoing advancements in treatment accuracy and patient safety are contributing to market growth in Japan.

India Radiation Therapy for Head & Neck Cancer Market Insight

The India radiation therapy for head & neck cancer market is expanding rapidly, driven by a high burden of head and neck cancers linked to tobacco consumption, alcohol use, and rising environmental risk factors. Increasing awareness of early cancer diagnosis, improving access to oncology care, and growing investments in healthcare infrastructure are supporting wider adoption of radiation therapy across hospitals and cancer centers. The availability of cost-effective LINAC-based systems and expanding presence of specialized oncology facilities are further accelerating treatment uptake. In addition, government initiatives to strengthen cancer care services and rising penetration of advanced radiotherapy technologies are contributing to sustained market growth in India.

Radiation Therapy for Head & Neck Cancer Market Share

The Radiation therapy for head & neck cancer industry is primarily led by well-established companies, including:

- Siemens Healthineers AG (Germany)

- Elekta AB (Sweden)

- Accuray Incorporated (U.S.)

- Hitachi Ltd. (Japan)

- Brainlab AG (Germany)

- RaySearch Laboratories (Sweden)

- Mevion Medical Systems (U.S.)

- Canon Inc. (Japan)

- United Imaging Healthcare (China)

- GE HealthCare (U.S.)

- Panacea Medical Technologies Pvt. Ltd. (India)

What are the Recent Developments in Global Radiation Therapy for Head & Neck Cancer Market?

- In September 2025, Accuray Incorporated introduced the Accuray Stellar radiotherapy solution, a next-generation configuration of the Radixact system designed to enhance precision treatment delivery and workflow efficiency in complex cancer cases, including head & neck cancers, with emphasis on adaptive and AI-supported planning

- In October 2025, Elekta AB showcased its latest adaptive radiotherapy innovations, including the Elekta Unity MR-Linac and Evo CT-Linac systems, highlighting advancements in real-time tumor tracking and image-guided radiation therapy to improve precision in head & neck cancer treatment

- In 2025, Varian (Siemens Healthineers) continued expansion of its AI-driven radiotherapy ecosystem, integrating advanced treatment planning and IGRT solutions such as TrueBeam and Halcyon systems, improving precision dose delivery and workflow efficiency in head & neck cancer treatment

- In March 2026, GE HealthCare and other radiation oncology players contributed to the growing adoption of image-guided and adaptive radiotherapy systems, driven by increasing demand for precision cancer treatment and expansion of oncology centers globally, particularly for complex tumor sites like head and neck cancers

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.