Global Radiopharmaceutical Cdmo Market

Market Size in USD Billion

USD

2.18 Billion

USD

6.26 Billion

2025

2033

USD

2.18 Billion

USD

6.26 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 2.18 Billion |

Market Size (Forecast Year) |

USD 6.26 Billion |

CAGR |

% |

Major Markets Players |

|

Radiopharmaceutical CDMO Market Overview

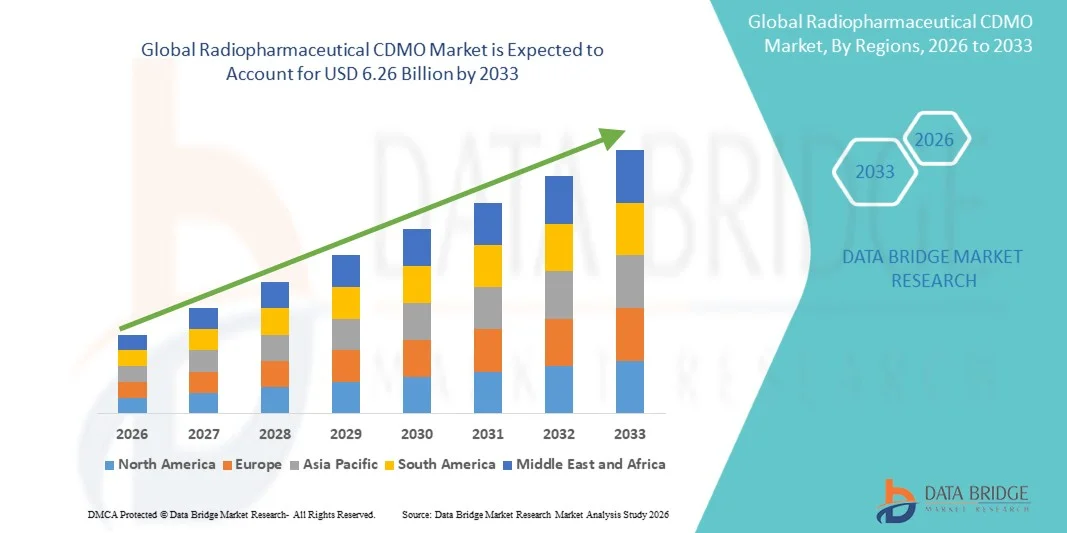

The Radiopharmaceutical CDMO Market was valued at USD 2.18 billion in 2025 and is projected to reach USD 6.26 billion by 2033, growing at a CAGR of 14.10% from 2026 to 2033. The market is experiencing consistent growth driven by rising demand for outsourced radiopharmaceutical development and manufacturing services, increasing adoption of targeted radiopharmaceutical therapies, and growing investments in nuclear medicine infrastructure and precision oncology. The expansion of pharmaceutical and biotechnology pipelines, combined with the increasing complexity of radiopharmaceutical production, is encouraging companies to collaborate with specialized CDMO providers for cost-effective development, regulatory support, and scalable manufacturing capabilities.

The rising prevalence of cancer and other chronic diseases, along with advancements in diagnostic imaging and therapeutic radiopharmaceuticals, is accelerating demand for reliable CDMO partners. Radiopharmaceutical CDMOs are enabling pharmaceutical companies to overcome challenges related to radioactive material handling, specialized facilities, regulatory compliance, and supply chain management. Increasing adoption of personalized medicine, theranostics, and next-generation radioisotope technologies is further supporting market expansion across North America, Europe, and emerging healthcare markets.

Key Market Trends & Insights

- North America dominated the Radiopharmaceutical CDMO Market with the largest revenue share of 38.2% in 2025, supported by advanced nuclear medicine infrastructure, strong presence of radiopharmaceutical manufacturers, increasing outsourcing by pharmaceutical companies, and significant investments in precision oncology and targeted radiopharmaceutical therapies. The region benefits from established regulatory frameworks, expanding nuclear medicine adoption, and growing demand for specialized CDMO partners offering development, manufacturing, and distribution capabilities.

- The radiopharmaceutical manufacturing services segment dominated the market with a 48.62% share in 2025, owing to increasing outsourcing of complex radioactive drug production activities by pharmaceutical and biotechnology companies.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 10.1% from 2026 to 2033, fueled by increasing cancer incidence, expanding nuclear medicine infrastructure, rising investments in radiopharmaceutical production facilities, and growing adoption of advanced diagnostic and therapeutic imaging technologies across China, India, Japan, and South Korea.

- The pharmaceutical & biotechnology companies segment dominated the market by End User with a 55.6% share in 2025, owing to increasing reliance on specialized CDMO providers for radiopharmaceutical development, regulatory support, manufacturing scale-up, and global distribution. Growing investment in radiopharmaceutical pipelines by biotech and pharmaceutical companies is accelerating outsourcing activities.

Market Size & Forecast

- Global Market Value (2025): USD 2.18 Billion

- Expected Market Value (2033): USD 6.26 Billion

- Forecast CAGR (2026–2033): 14.10%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Radiopharmaceutical CDMO Market Segmentation

|

Attributes |

Radiopharmaceutical CDMO Key Market Insights |

|

Segments Covered |

· By Service Type: Radiopharmaceutical Development Services, Radiopharmaceutical Manufacturing Services, Packaging & Distribution Services · By Radioisotope Type: Diagnostic Radioisotopes, Therapeutic Radioisotopes, Theranostic Radioisotopes · By End User: Pharmaceutical & Biotechnology Companies, Research Institutes & Academic Organizations, Hospitals & Nuclear Medicine Centers |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Curium Pharma (France) |

|

Market Opportunities |

· Expansion of Targeted Radiopharmaceutical Therapies and Theranostics · Growing Demand for Specialized Radiopharmaceutical Manufacturing Infrastructure · Integration of Advanced Technologies and Expansion in Emerging Markets |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Radiopharmaceutical CDMO Market Trends

Trend: Rising Outsourcing of Radiopharmaceutical Development and Manufacturing Activities

The Radiopharmaceutical CDMO Market is witnessing a significant shift toward outsourcing as pharmaceutical and biotechnology companies increasingly collaborate with specialized contract development and manufacturing organizations to accelerate radiopharmaceutical innovation and commercialization. The complexity of handling radioactive materials, stringent regulatory requirements, specialized GMP facilities, and the need for advanced isotope production capabilities are encouraging companies to rely on experienced CDMO partners. The growing adoption of targeted radiopharmaceutical therapies, particularly in oncology, is further increasing demand for specialized manufacturing support. Radioisotopes such as lutetium-177 and actinium-225 are gaining attention due to their applications in precision cancer treatment and theranostic approaches. In recent years, companies have expanded radiopharmaceutical production capabilities, invested in isotope supply chains, and developed advanced manufacturing infrastructure to support the growing clinical pipeline of radiopharmaceutical products.

Radiopharmaceutical CDMO Market Dynamics

Key Market Driver: Increasing Demand for Targeted Radiopharmaceutical Therapies and Nuclear Medicine Applications

The rising prevalence of cancer and increasing adoption of personalized medicine are major factors driving demand for radiopharmaceutical CDMO services. Pharmaceutical and biotechnology companies are investing heavily in radioligand therapies and targeted radionuclide treatments that require specialized manufacturing, packaging, and distribution capabilities. The expansion of nuclear medicine centers, increased adoption of PET and SPECT imaging, and growing clinical development of therapeutic radioisotopes are creating significant opportunities for CDMO providers. For example, the approval and commercialization of targeted radiopharmaceutical therapies based on lutetium-177 have accelerated investments in specialized manufacturing facilities and global supply chain capabilities. Companies are increasingly partnering with CDMOs to overcome production complexity, ensure regulatory compliance, and support global commercialization of radiopharmaceutical products.

Key Restraint/Challenge: Complex Manufacturing Requirements and Regulatory Challenges

A major challenge for the Radiopharmaceutical CDMO Market is the complexity associated with radioactive material handling, manufacturing, and distribution. Radiopharmaceutical production requires highly specialized facilities, strict radiation safety protocols, regulatory approvals, and skilled technical expertise. In addition, the short half-life of many radioisotopes creates logistical challenges related to production scheduling, storage, transportation, and timely delivery to healthcare facilities. High capital investment requirements for cyclotrons, isotope production systems, hot cells, and GMP manufacturing infrastructure can limit entry for smaller organizations. Continuous regulatory compliance across different regions also increases operational complexity for CDMO providers.

Key Market Expansion of Theranostics and Advanced Radioisotope Manufacturing Platforms

The integration of advanced radioisotope technologies, precision oncology, and theranostic approaches presents significant growth opportunities for the radiopharmaceutical CDMO market. Theranostic radioisotopes enable simultaneous disease diagnosis and targeted treatment, supporting personalized patient management and improved therapeutic outcomes. CDMO companies are increasingly investing in advanced manufacturing platforms, isotope production capabilities, and global distribution networks to support growing demand for radiopharmaceutical therapies. For instance, increasing investments in actinium-225 production, lutetium-177 supply expansion, and next-generation radioligand therapy pipelines are creating new opportunities for specialized CDMO providers. The continued growth of oncology-focused pharmaceutical pipelines and expansion of nuclear medicine infrastructure across North America, Europe, and Asia-Pacific are expected to accelerate adoption of radiopharmaceutical CDMO services through 2033.

Radiopharmaceutical CDMO Market Scope

The radiopharmaceutical CDMO market is segmented on the basis of service type, radioisotope type, and end user.

- By Service Type

On the basis of service type, the Radiopharmaceutical CDMO Market is segmented into radiopharmaceutical development services, radiopharmaceutical manufacturing services, and packaging & distribution services. The radiopharmaceutical manufacturing services segment dominated the market with a 48.62% share in 2025, owing to increasing outsourcing of complex radioactive drug production activities by pharmaceutical and biotechnology companies. The segment benefits from growing demand for GMP-compliant manufacturing facilities, specialized isotope handling capabilities, and scalable production support for clinical and commercial radiopharmaceutical products. Increasing adoption of targeted radionuclide therapies and the expansion of oncology pipelines are encouraging companies to partner with CDMOs for reliable manufacturing capacity. In addition, manufacturing services help overcome challenges related to radioactive material management, regulatory compliance, and specialized infrastructure requirements, strengthening segment dominance across global markets.

The Radiopharmaceutical Development Services segment is expected to witness the fastest growth at a CAGR of 10.2% from 2026 to 2033, driven by increasing demand for early-stage development support, formulation optimization, and clinical trial assistance for novel radiopharmaceutical candidates. Growing investments in precision oncology, theranostic platforms, and next-generation radioisotopes are encouraging pharmaceutical companies to collaborate with CDMOs during drug development stages. Advances in radiochemistry, molecular targeting technologies, and personalized medicine approaches are further accelerating demand for specialized development capabilities. In addition, increasing research activities focused on alpha emitters, beta emitters, and diagnostic imaging agents are expected to create strong growth opportunities for development service providers.

- By Radioisotope Type

On the basis of radioisotope type, the Radiopharmaceutical CDMO Market is segmented into diagnostic radioisotopes, therapeutic radioisotopes, and theranostic radioisotopes. The diagnostic radioisotopes segment dominated the market with a 45.73% share in 2025, supported by widespread use of imaging agents in nuclear medicine procedures such as PET and SPECT scans. The segment continues to benefit from increasing demand for early disease detection, cardiovascular imaging, and cancer diagnosis applications. Growing healthcare infrastructure development, rising adoption of molecular imaging technologies, and increasing availability of diagnostic radiopharmaceuticals are supporting market expansion. In addition, established clinical usage, broader accessibility, and increasing demand for non-invasive diagnostic procedures reinforce the leading position of diagnostic radioisotopes in the market.

The theranostic radioisotopes segment is projected to register the fastest growth at a CAGR of 11.1% from 2026 to 2033, driven by rising adoption of personalized medicine approaches that combine diagnostic imaging and targeted therapy. Theranostic platforms enable patient-specific treatment selection and monitoring, particularly in oncology applications such as prostate cancer and neuroendocrine tumors. Increasing research investments in targeted radionuclide therapy, growing approvals of advanced radiopharmaceutical products, and expanding clinical pipelines are accelerating segment growth. Furthermore, pharmaceutical companies are increasingly partnering with CDMOs to develop and manufacture complex theranostic products, creating significant opportunities for specialized radiopharmaceutical service providers.

- By End User

On the basis of end user, the Radiopharmaceutical CDMO Market is segmented into pharmaceutical & biotechnology companies, research institutes & academic organizations, and hospitals & nuclear medicine centers. The pharmaceutical & biotechnology companies segment dominated the market with a 56.84% share in 2025, due to increasing reliance on outsourcing partners for radiopharmaceutical development, manufacturing, and regulatory support. Pharmaceutical companies are increasingly collaborating with CDMOs to access specialized facilities, reduce development costs, and accelerate commercialization timelines. The growing number of radiopharmaceutical drug candidates, expansion of oncology pipelines, and increasing investment in targeted therapies are driving demand from this segment. In addition, outsourcing allows companies to overcome challenges associated with radioactive material handling, compliance requirements, and production scalability, strengthening the dominance of pharmaceutical and biotechnology companies.

The Research Institutes & Academic Organizations segment is expected to witness the fastest growth at a CAGR of 10.5% from 2026 to 2033, driven by increasing research activities in nuclear medicine, molecular imaging, and novel radioisotope development. Academic institutions and research organizations are expanding collaborations with CDMOs to support preclinical studies, clinical research, and innovation in radiopharmaceutical technologies. Growing government funding for nuclear medicine research, advancements in radiochemistry, and rising focus on cancer therapeutics are supporting segment expansion. In addition, increasing partnerships between research institutions, biotechnology companies, and CDMO providers are creating new opportunities for technology transfer, clinical development, and commercialization of innovative radiopharmaceutical solutions.

Radiopharmaceutical CDMO Market Regional Analysis

North America dominated the Radiopharmaceutical CDMO Market and accounted for the largest revenue share of 38.2% in 2025, supported by advanced nuclear medicine infrastructure, strong presence of radiopharmaceutical manufacturers, increasing outsourcing by pharmaceutical companies, and significant investments in precision oncology and targeted radiopharmaceutical therapies. The region benefits from established regulatory frameworks, expanding adoption of nuclear medicine, and growing demand for specialized CDMO partners offering radiopharmaceutical development, GMP manufacturing, packaging, and distribution capabilities. Increasing investments in targeted radionuclide therapies and advanced radioisotope production facilities are further strengthening market growth across the region.

U.S. Radiopharmaceutical CDMO Market Insight

The U.S. radiopharmaceutical CDMO market is witnessing strong growth due to increasing demand for targeted cancer therapies, rising adoption of nuclear medicine procedures, and growing outsourcing activities by pharmaceutical and biotechnology companies. The country’s advanced healthcare infrastructure, strong presence of radiopharmaceutical innovators, and expanding precision oncology ecosystem are driving demand for specialized CDMO services. Increasing investments in radioisotope production capabilities, including technologies supporting therapeutic isotopes such as lutetium-177 and actinium-225, are further accelerating market expansion.

Europe Radiopharmaceutical CDMO Market Insight

The Europe radiopharmaceutical CDMO market remains a major contributor to global revenue, driven by strong nuclear medicine capabilities, increasing adoption of radiopharmaceutical therapies, and growing demand for outsourced manufacturing solutions. The region benefits from well-established healthcare systems, regulatory support for advanced therapies, and increasing investments in radiopharmaceutical production infrastructure. Rising adoption of PET and SPECT imaging technologies, along with growing clinical development of targeted radionuclide therapies, is supporting market growth across European countries.

U.K. Radiopharmaceutical CDMO Market Insight

The U.K. radiopharmaceutical CDMO market is experiencing steady growth, supported by increasing investments in nuclear medicine research, expanding clinical applications of radiopharmaceuticals, and growing collaboration between pharmaceutical companies and specialized manufacturing providers. The country’s strong research ecosystem and focus on precision medicine are encouraging development and commercialization of advanced radiopharmaceutical products. Increasing demand for reliable production and distribution networks for short half-life radioisotopes is further contributing to market expansion.

Germany Radiopharmaceutical CDMO Market Insight

The Germany radiopharmaceutical CDMO market is expanding steadily due to the country’s strong pharmaceutical manufacturing base, advanced healthcare infrastructure, and increasing adoption of nuclear medicine solutions. Pharmaceutical companies and research institutions are increasingly collaborating with CDMO providers for radiopharmaceutical development, production, and regulatory support. Growing investments in radiopharmaceutical research, oncology treatments, and isotope supply capabilities are further driving market growth in Germany.

Asia-Pacific Radiopharmaceutical CDMO Market Insight

The Asia-Pacific radiopharmaceutical CDMO market is expected to witness rapid growth at a CAGR of 10.1% from 2026 to 2033, fueled by increasing cancer incidence, expanding nuclear medicine infrastructure, rising investments in radiopharmaceutical production facilities, and growing adoption of advanced diagnostic and therapeutic imaging technologies across China, India, Japan, and South Korea. The region is experiencing increasing demand for specialized radiopharmaceutical manufacturing services as healthcare systems expand access to nuclear medicine and precision oncology treatments.

Japan Radiopharmaceutical CDMO Market Insight

The Japan radiopharmaceutical CDMO market is witnessing consistent growth due to increasing adoption of nuclear medicine, advanced healthcare infrastructure, and rising demand for targeted radiopharmaceutical therapies. The country’s strong research capabilities and focus on precision medicine are supporting the development of innovative radiopharmaceutical products. Growing investments in radioisotope production, diagnostic imaging, and therapeutic applications are further contributing to market expansion in Japan.

China Radiopharmaceutical CDMO Market Insight

The China radiopharmaceutical CDMO market is growing rapidly, driven by increasing cancer burden, expanding nuclear medicine facilities, government support for healthcare innovation, and rising investments in radiopharmaceutical manufacturing capabilities. Growing adoption of PET imaging, targeted radionuclide therapies, and advanced oncology treatments is boosting demand for specialized CDMO services. Increasing efforts to strengthen domestic radioisotope production and improve radiopharmaceutical supply chains are positioning China as one of the fastest-growing markets for radiopharmaceutical CDMO services globally.

Radiopharmaceutical CDMO Market Share

The radiopharmaceutical CDMO industry is primarily led by well-established companies, including:

- Curium Pharma (France)

- Bracco S.p.A. (Italy)

- NorthStar Medical Radioisotopes (U.S.)

- Eckert & Ziegler (Germany)

- NTP Radioisotopes SOC Ltd (South Africa)

- ITM Isotope Technologies Munich SE (Germany)

- Telix Pharmaceuticals (Australia)

- Novartis (Switzerland)

- Bayer AG (Germany)

- Lantheus Holdings (U.S.)

- POINT Biopharma (Canada/U.S.)

- Fusion Pharmaceuticals (Canada/U.S.)

- Cardinal Health (U.S.)

- Jubilant Radiopharma (India/U.S.)

- IsoTherapeutics Group (U.S.)

- Triad Isotopes (U.S.)

- RayzeBio (U.S.)

- RadioMedix (U.S.)

- Nucleus RadioPharma (U.S.)

- Vivo Biopharma (U.S.)

- Alliance Medical (U.K.)

- IBA Group (Belgium)

- Eczacıbaşı-Monrol Nuclear Products (Turkey)

- Advanced Accelerator Applications (Switzerland)

- Polatom (Poland)

- Shine Technologies (U.S.)

- Blue Earth Diagnostics (U.K.)

- Alpha-9 Theranostics (U.S.)

- Actinium Pharmaceuticals (U.S.)

- Cellectar Biosciences (U.S.)

- OncoBeta (Germany)

- Radiopharm Theranostics (Australia)

Latest Developments in Radiopharmaceutical CDMO Market

- In March 2024, PharmaLogic Holdings Corp., a radiopharmaceutical CDMO and radiopharmacy solutions provider, announced a strategic collaboration with Intermountain Health to develop and expand access to novel radiopharmaceuticals through a new cGMP-grade research, production, and distribution facility in Salt Lake City, Utah. The facility was designed to support development and manufacturing of advanced radiopharmaceutical products for cancer and other disease applications, strengthening PharmaLogic’s position in outsourced radiopharmaceutical development and manufacturing services

- In April 2024, PharmaLogic Holdings Corp. announced the opening of its new radiopharmaceutical production and research facility in Cincinnati, Ohio, expanding its CDMO capabilities for diagnostic and therapeutic radiopharmaceutical development. The new cyclotron-based facility was established to increase production capacity and support the development of novel radiopharmaceutical compounds for oncology, neurological, and cardiovascular applications. This expansion highlights the growing demand for specialized radiopharmaceutical manufacturing infrastructure and outsourced CDMO solutions

- In May 2024, PharmaLogic Holdings Corp. announced the opening of its renovated radiopharmaceutical production and research facility in Bronx, New York. The facility was upgraded with advanced equipment to support radiopharmaceutical manufacturing and research activities, enabling expanded production capabilities and supporting innovation in molecular imaging and targeted radiopharmaceutical development. The investment reflects increasing industry focus on strengthening regional manufacturing networks for radiopharmaceutical supply

- In October 2024, NorthStar Medical Radioisotopes unveiled its radiopharmaceutical contract development and manufacturing facility in Beloit, Wisconsin. The facility was developed as a large-scale CDMO platform supporting production and manufacturing of medical radioisotopes including Actinium-225 (Ac-225), Lutetium-177 (Lu-177), Copper-64 (Cu-64), Copper-67 (Cu-67), and Indium-111 (In-111). The expansion marked a significant step toward improving domestic radioisotope supply and supporting growing demand for therapeutic radiopharmaceuticals

- In October 2024, PharmaLogic Holdings Corp. announced the opening of its radiopharmaceutical production and research facility in Los Angeles, California. The facility expansion included advanced cyclotron and laboratory capabilities to support development and manufacturing of next-generation radiopharmaceutical products. The investment aimed to improve access to radiopharmaceutical solutions and strengthen collaboration with healthcare providers and researchers in the region

- In September 2024, Novartis announced further investment plans to expand radiopharmaceutical manufacturing capabilities, including development of new manufacturing infrastructure and expansion of existing facilities to support radioligand therapy production. The investment highlighted the growing importance of dedicated radiopharmaceutical manufacturing capacity as pharmaceutical companies scale targeted cancer therapies and secure supply chains

- In April 2025, Lantheus Holdings completed the acquisition of Evergreen Theragnostics, a clinical-stage radiopharmaceutical company with radioligand therapy manufacturing infrastructure and CDMO capabilities. The acquisition expanded Lantheus’ capabilities in theranostic development and strengthened its position in radiopharmaceutical manufacturing and outsourced production services. This development reflects increasing consolidation and investment activity in the radiopharmaceutical CDMO ecosystem

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.