Global Radiopharmaceutical Oncology Therapy Market

Market Size in USD Billion

USD

5.43 Billion

USD

15.92 Billion

2025

2033

USD

5.43 Billion

USD

15.92 Billion

2025

2033

| 2026 - 2033 | |

| USD 5.43 Billion | |

| USD 15.92 Billion | |

| % | |

|

Radiopharmaceutical Oncology Therapy Market Size

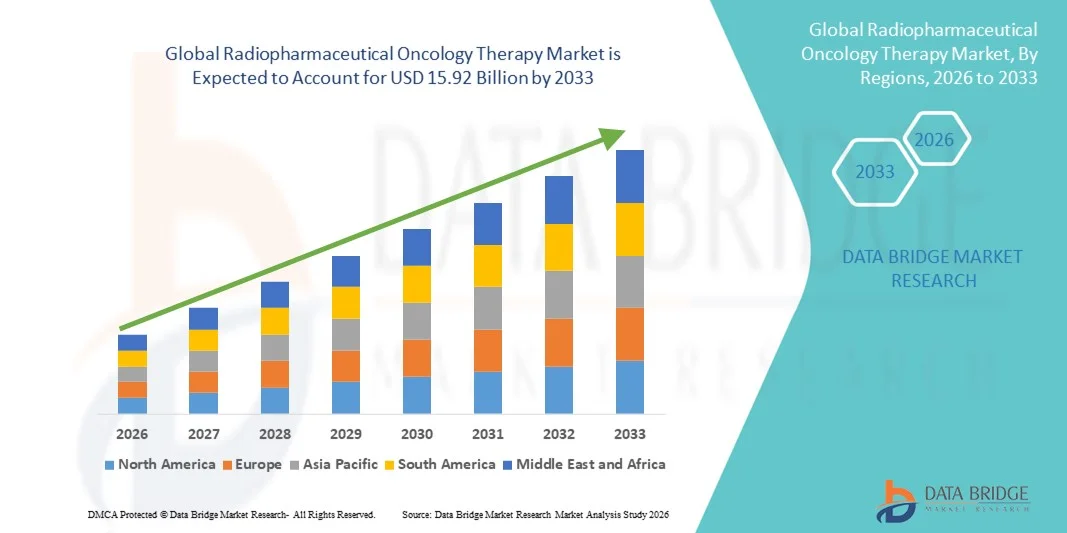

- The global radiopharmaceutical oncology therapy market size was valued at USD 5.43 billion in 2025 and is expected to reach USD 15.92 billion by 2033, at a CAGR of 14.40% during the forecast period

- The market growth is largely fueled by the increasing prevalence of cancer worldwide, rising demand for targeted and precision oncology treatments, and continuous advancements in nuclear medicine technologies, leading to greater adoption of radiopharmaceutical-based therapies across specialized cancer care centers and hospitals. Expanding clinical research in targeted radionuclide therapy and growing regulatory approvals for novel radiotherapeutics are further strengthening market expansion

- Furthermore, the rising preference for minimally invasive and highly targeted treatment approaches that deliver radiation directly to cancer cells while minimizing damage to surrounding healthy tissues is establishing radiopharmaceutical oncology therapy as a transformative modality in modern cancer care. Increasing investments in oncology infrastructure, expanding production capabilities for medical isotopes, and strategic collaborations between pharmaceutical and nuclear medicine companies are accelerating the uptake of radiopharmaceutical oncology therapy solutions, thereby significantly boosting overall industry growth

Radiopharmaceutical Oncology Therapy Market Analysis

- Radiopharmaceutical oncology therapy, which utilizes targeted radioactive isotopes to diagnose and treat various types of cancers, is becoming an integral component of precision oncology care across hospitals and specialized cancer treatment centers due to its ability to selectively destroy tumor cells while minimizing damage to surrounding healthy tissues. Advancements in targeted radionuclide therapy, alpha- and beta-emitting isotopes, and companion diagnostics are further strengthening its clinical adoption

- The escalating demand for radiopharmaceutical oncology therapies is primarily fueled by the rising global cancer burden, increasing preference for minimally invasive targeted treatment options, expanding clinical evidence supporting radioligand therapy, and growing investments in nuclear medicine infrastructure. In addition, regulatory approvals of novel radiotherapeutics and strategic collaborations between pharmaceutical and isotope manufacturing companies are accelerating market growth

- North America dominated the radiopharmaceutical oncology therapy market with the largest revenue share of approximately 42.3% in 2025, supported by advanced healthcare infrastructure, strong presence of leading radiopharmaceutical manufacturers, favorable reimbursement frameworks, and high adoption of innovative cancer therapies. The U.S. continues to experience substantial growth in targeted radionuclide therapy utilization, driven by increasing clinical trials and rapid commercialization of new radioligand treatments

- Asia-Pacific is expected to be the fastest-growing region in the Radiopharmaceutical Oncology Therapy market during the forecast period, projected to register a CAGR of approximately 12.6%, driven by rising cancer incidence, improving nuclear medicine capabilities, expanding healthcare investments, and increasing awareness regarding advanced oncology treatment options across emerging economies

- The Beta Emitters segment dominated the largest market revenue share of 62.7% in 2025, driven by their widespread clinical use in targeted cancer therapy and well-established regulatory approvals

Report Scope and Radiopharmaceutical Oncology Therapy Market Segmentation

|

Attributes |

Radiopharmaceutical Oncology Therapy Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Radiopharmaceutical Oncology Therapy Market Trends

Advancement of Targeted Radioligand and Precision Oncology Therapies

- A significant and accelerating trend in the global radiopharmaceutical oncology therapy market is the development of targeted radioligand therapies that precisely bind to cancer-specific biomarkers, delivering radiation directly to tumor cells while minimizing damage to surrounding healthy tissues

- This precision-based approach is transforming oncology treatment paradigms, particularly for prostate cancer, neuroendocrine tumors, and metastatic malignancies.

- For instance, Novartis AG has expanded the global adoption of radioligand therapies such as Lutetium-177–based treatments for advanced prostate cancer, demonstrating improved progression-free survival in clinical settings. Such targeted therapies are gaining regulatory approvals across North America, Europe, and Asia-Pacific, significantly expanding market penetration.

- In addition, increasing integration of theranostics—combining diagnostic imaging and therapeutic radiopharmaceuticals—is strengthening personalized cancer treatment strategies. The growing use of PET imaging to identify suitable candidates for radioligand therapy ensures optimized dosing and better treatment outcomes

- This shift toward biomarker-driven, personalized oncology solutions is reshaping the global radiopharmaceutical oncology therapy landscape

Radiopharmaceutical Oncology Therapy Market Dynamics

Driver

Rising Global Cancer Burden and Demand for Minimally Invasive Therapies

- The rising global prevalence of cancer is a primary driver of the radiopharmaceutical oncology therapy market

- Increasing incidence of prostate cancer, thyroid cancer, and neuroendocrine tumors, particularly among aging populations, is accelerating the demand for advanced treatment modalities that offer targeted action with reduced systemic toxicity

- For instance, according to data published by the World Health Organization, cancer remains one of the leading causes of mortality worldwide, prompting governments and healthcare providers to invest heavily in innovative treatment technologies, including nuclear medicine–based therapies

- This growing disease burden directly supports the expansion of radiopharmaceutical treatment centers globally

- Furthermore, patients and clinicians are increasingly favoring minimally invasive and targeted therapeutic approaches over conventional chemotherapy and external beam radiation due to improved safety profiles and better quality-of-life outcomes

- Expanding healthcare infrastructure, increasing reimbursement support in developed markets, and ongoing clinical trials are further propelling global adoption

Restraint/Challenge

High Treatment Costs and Complex Regulatory Frameworks

- Despite strong growth potential, the radiopharmaceutical oncology therapy market faces challenges related to high treatment costs and complex regulatory requirements

- The production, transportation, and administration of radiopharmaceuticals require specialized infrastructure, strict radiation safety protocols, and highly trained personnel, contributing to elevated overall treatment expenses

- For instance, radioligand therapies utilizing isotopes such as Lutetium-177 require dedicated nuclear medicine facilities and controlled supply chains, limiting availability in low- and middle-income countries. These logistical and infrastructure constraints restrict equitable global access to advanced therapies

- In addition, stringent regulatory approval pathways for radioactive medicinal products can delay commercialization timelines. Variability in reimbursement frameworks across countries further complicates market expansion

- Addressing these challenges through expanded isotope production capacity, strategic partnerships, improved reimbursement models, and streamlined regulatory processes will be critical to ensuring sustained global growth of the radiopharmaceutical oncology therapy market

Radiopharmaceutical Oncology Therapy Market Scope

The market is segmented on the basis of product type and application.

- By Product Type

On the basis of product type, the Global Radiopharmaceutical Oncology Therapy market is segmented into Alpha Emitters and Beta Emitters. The Beta Emitters segment dominated the largest market revenue share of 62.7% in 2025, driven by their widespread clinical use in targeted cancer therapy and well-established regulatory approvals. Beta-emitting radiopharmaceuticals are extensively utilized in the treatment of thyroid cancer, bone metastases, and neuroendocrine tumors. Their deeper tissue penetration capability makes them suitable for treating larger tumor masses. Increasing adoption of targeted radionuclide therapy in developed healthcare systems further strengthens segment dominance. Strong clinical evidence supporting therapeutic efficacy and safety also boosts physician preference. Moreover, the availability of commercially approved beta-emitting products across major markets enhances accessibility. Rising cancer prevalence globally continues to fuel demand. Expanding nuclear medicine infrastructure and growing investment in oncology research further support sustained growth of this segment.

The Alpha Emitters segment is anticipated to witness the fastest growth rate of 14.8% CAGR from 2026 to 2033, fueled by increasing research advancements and growing interest in precision oncology. Alpha particles deliver high-energy radiation with minimal damage to surrounding healthy tissues, making them highly effective for targeted cancer treatment. Their shorter path length improves safety profiles, particularly in metastatic and resistant cancers. Rising approvals of novel alpha-emitting therapies are accelerating adoption across oncology centers. Expanding clinical trials and strong pipeline development further support rapid expansion. In addition, increasing awareness among oncologists regarding targeted radionuclide therapy is driving uptake. Growing investments from pharmaceutical and biotechnology companies continue to strengthen the future outlook of this segment.

- By Application

On the basis of application, the Global Radiopharmaceutical Oncology Therapy market is segmented into Prostate Cancer and Bone Metastasis. The Prostate Cancer segment accounted for the largest market revenue share of 54.3% in 2025, driven by the rising global incidence of prostate cancer and increasing adoption of targeted radioligand therapies. Radiopharmaceuticals have shown strong clinical outcomes in metastatic castration-resistant prostate cancer (mCRPC), significantly improving survival rates. Growing availability of PSMA-targeted therapies further supports segment dominance. Increasing screening programs and early diagnosis initiatives also contribute to higher treatment volumes. Favorable reimbursement policies in developed markets strengthen product accessibility. Continuous innovation in personalized cancer therapy enhances long-term growth prospects. Expanding geriatric population, particularly in North America and Europe, further supports rising demand.

The Bone Metastasis segment is projected to witness the fastest CAGR of 12.6% from 2026 to 2033, driven by the increasing prevalence of metastatic cancers such as breast, lung, and prostate cancer spreading to bones. Radiopharmaceutical therapies are widely used for pain palliation and targeted tumor control in metastatic bone disease. Rising cancer burden worldwide significantly contributes to segment expansion. Advancements in targeted alpha and beta therapies improve treatment efficacy and safety. Growing focus on improving quality of life for advanced cancer patients further accelerates adoption. Increasing investments in nuclear medicine facilities across emerging markets also strengthen the segment’s growth trajectory during the forecast period.

Radiopharmaceutical Oncology Therapy Market Regional Analysis

- North America dominated the radiopharmaceutical oncology therapy market with the largest revenue share of approximately 42.3% in 2025, supported by advanced healthcare infrastructure, strong presence of leading radiopharmaceutical manufacturers, favorable reimbursement frameworks, and high adoption of innovative cancer therapies

- The region benefits from well-established nuclear medicine networks and widespread availability of PET and SPECT imaging systems. Increasing prevalence of prostate cancer and neuroendocrine tumors continues to drive demand for targeted radionuclide therapy. Strong regulatory support and faster approval pathways encourage commercialization of novel radioligand therapies. The presence of global pharmaceutical leaders and biotechnology innovators strengthens product pipelines

- Expanding clinical trials focusing on PSMA-targeted and alpha-emitting therapies further accelerate market expansion. Investments in isotope production and radiopharmacy distribution enhance supply chain reliability. Rising healthcare expenditure and growing physician preference for precision oncology solutions reinforce market leadership. Continuous technological advancements in radiolabeling and targeted delivery systems also contribute to sustained regional dominance throughout the forecast period

U.S. Radiopharmaceutical Oncology Therapy Market Insight

The U.S. radiopharmaceutical oncology therapy market captured approximately 84% revenue share within North America in 2025, driven by high adoption of advanced targeted radionuclide therapies and strong oncology research infrastructure. The country leads in clinical trials focused on PSMA-based radioligand treatments and alpha-emitter innovations. Increasing FDA approvals and rapid commercialization of breakthrough therapies significantly propel growth. Favorable reimbursement policies and structured oncology treatment pathways improve patient access. Rising prostate cancer incidence and expanding applications in metastatic cancers further boost demand. Strong collaboration between academic institutions and pharmaceutical companies accelerates research translation. Advanced imaging integration enhances therapy planning and monitoring outcomes. Growing investments in nuclear medicine facilities and isotope production capacity strengthen market stability. Increasing patient awareness regarding personalized oncology solutions continues to support long-term expansion in the U.S.

Europe Radiopharmaceutical Oncology Therapy Market Insight

The Europe radiopharmaceutical oncology therapy market is projected to expand at a substantial CAGR of approximately 9.8% during the forecast period, driven by rising cancer prevalence and increasing investment in nuclear medicine capabilities. Western European countries maintain strong radiopharmaceutical manufacturing ecosystems and structured cancer care programs. Government-supported healthcare systems improve accessibility to advanced oncology treatments. Growing demand for minimally invasive targeted therapies encourages clinical adoption. Technological advancements in radiolabeling and isotope handling improve treatment precision. Collaborative research initiatives across the European Union accelerate innovation. Expansion of hospital-based radiopharmacies enhances supply reliability. Rising geriatric population and increasing screening programs further contribute to demand. The integration of precision medicine strategies across oncology centers strengthens the region’s long-term growth outlook.

U.K. Radiopharmaceutical Oncology Therapy Market Insight

The U.K. radiopharmaceutical oncology therapy market is anticipated to grow at a noteworthy CAGR of approximately 9.2%, supported by expanding cancer screening initiatives and investments in advanced oncology treatments. The National Health Service (NHS) continues to enhance access to targeted radionuclide therapies. Rising incidence of prostate and thyroid cancers supports increasing therapy utilization. Academic research institutions actively participate in clinical trials for innovative radioligand therapies. Government funding for precision oncology strengthens treatment adoption. Expansion of nuclear medicine departments and cyclotron facilities improves isotope availability. Structured patient referral pathways support therapy integration into routine oncology care. Increasing clinician awareness and demand for personalized cancer treatment options contribute to sustained market expansion.

Germany Radiopharmaceutical Oncology Therapy Market Insight

The Germany radiopharmaceutical oncology therapy market is expected to expand at a considerable CAGR of approximately 10.1%, driven by strong healthcare infrastructure and high adoption of advanced medical technologies. Germany maintains one of Europe’s largest nuclear medicine networks with advanced PET/CT capabilities. Rising cancer burden and aging population stimulate therapy demand. Investments in radiopharmaceutical research and domestic isotope production strengthen supply security. Favorable reimbursement frameworks and structured oncology registries improve patient access. Collaboration between research institutes and pharmaceutical manufacturers accelerates product development. Increasing focus on early diagnosis and precision oncology further boosts utilization. Continuous technological innovation and sustainability initiatives reinforce Germany’s significant contribution to European market growth.

Asia-Pacific Radiopharmaceutical Oncology Therapy Market Insight

The Asia-Pacific radiopharmaceutical oncology therapy market is poised to grow at the fastest CAGR of approximately 12.6% from 2026 to 2033, driven by rising cancer incidence, improving nuclear medicine capabilities, and expanding healthcare investments across emerging economies. Rapid urbanization and growing middle-class populations enhance access to advanced oncology treatments. Governments across China, Japan, India, and South Korea are strengthening cancer care infrastructure and isotope production capacity. Increasing awareness regarding targeted radionuclide therapy supports market penetration. Growing participation in international clinical trials accelerates technology transfer and innovation. Expansion of private healthcare providers and medical tourism further supports adoption. Improvements in diagnostic imaging infrastructure enhance therapy planning and monitoring. As healthcare modernization progresses, the Asia-Pacific region is expected to remain the fastest-growing contributor to global market expansion.

China Radiopharmaceutical Oncology Therapy Market Insight

China radiopharmaceutical oncology therapy market accounted for the largest revenue share within the Asia-Pacific radiopharmaceutical oncology therapy market in 2025, driven by rapid expansion of oncology infrastructure and rising cancer incidence. The country is witnessing significant growth in prostate, liver, and lung cancer cases, increasing demand for advanced targeted therapies. Strong government support for nuclear medicine development and domestic isotope production enhances supply capabilities. Expansion of PET/CT imaging installations and radiopharmacy centers improves accessibility to radioligand therapies. Increasing investments from domestic pharmaceutical manufacturers and collaborations with global oncology players accelerate innovation. Regulatory reforms are streamlining drug approvals, supporting faster commercialization of novel alpha- and beta-emitting therapies. Growing healthcare expenditure and expanding insurance coverage further strengthen adoption. In addition, China’s focus on precision medicine and hospital modernization continues to drive integration of advanced radionuclide treatments. With ongoing infrastructure development and clinical research expansion, China is expected to maintain a leading position in the regional market throughout the forecast period.

Japan Radiopharmaceutical Oncology Therapy Market Insight

Japan radiopharmaceutical oncology therapy market is projected to grow at a steady CAGR of approximately 11.4% during the forecast period, supported by its advanced healthcare system and strong nuclear medicine expertise. The country has a high cancer burden, particularly among its aging population, which drives demand for targeted oncology therapies. Japan maintains well-established radiopharmaceutical manufacturing and cyclotron facilities, ensuring reliable isotope availability. Increasing clinical adoption of PSMA-targeted and other radioligand therapies supports market growth. Government initiatives promoting precision medicine and advanced cancer care enhance accessibility. Strong collaboration between academic institutions and pharmaceutical companies accelerates innovation in alpha- and beta-emitter therapies. Integration of advanced imaging technologies improves therapy planning and monitoring efficiency. Rising awareness among clinicians regarding minimally invasive and targeted treatment approaches further strengthens adoption. With continuous technological advancements and growing investment in oncology research, Japan remains a key contributor to Asia-Pacific market expansion.

Radiopharmaceutical Oncology Therapy Market Share

The Radiopharmaceutical Oncology Therapy industry is primarily led by well-established companies, including:

- Novartis AG (Switzerland)

- Bayer AG (Germany)

- Eli Lilly and Company (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- Curium Pharma (France)

- Lantheus Holdings, Inc. (U.S.)

- Telix Pharmaceuticals Limited (Australia)

- Eckert & Ziegler SE (Germany)

- NorthStar Medical Radioisotopes, LLC (U.S.)

- Cardinal Health, Inc. (U.S.)

- GE HealthCare Technologies Inc. (U.S.)

- Bracco Imaging S.p.A. (Italy)

- ITM Isotope Technologies Munich SE (Germany)

- Fusion Pharmaceuticals Inc. (Canada)

- Orano Med (France)

- Jubilant Radiopharma (U.S.)

- Advanced Accelerator Applications (France)

- POINT Biopharma Global Inc. (U.S.)

Latest Developments in Global Radiopharmaceutical Oncology Therapy Market

- In December 2021, the radiopharmaceutical Gallium (68Ga) gozetotide (also known as ^68Ga-PSMA-11) was approved for medical use in the United States, becoming the first FDA-approved PET imaging agent that targets prostate-specific membrane antigen (PSMA) for detecting prostate cancer lesions, enabling more precise cancer staging and treatment planning

- In March 2022, Novartis AG’s radioligand therapy Pluvicto (lutetium-177 vipivotide tetraxetan) received U.S. FDA approval for the treatment of PSMA-positive metastatic castration-resistant prostate cancer (mCRPC), establishing a new targeted oncology therapy that delivers radiation directly to tumor cells while sparing healthy tissue

- In May 2023, clinical research announced in pivotal radiopharmaceutical oncology studies achieved topline Phase III results for 177Lu-PNT2002, a PSMA-targeted radioligand therapy designed to treat metastatic prostate cancer. These results underscored significant efficacy in advanced prostate cancer patients after progression on androgen receptor pathway inhibitor therapy

- In March 2025, Novartis AG announced that the U.S. FDA expanded the indication for its targeted radioligand therapy Pluvicto (lutetium-177 vipivotide tetraxetan) to include patients with PSMA-positive metastatic castration-resistant prostate cancer who are eligible to delay chemotherapy following androgen receptor inhibitor treatment, significantly broadening the patient population eligible for this precision therapy

- In March 2025, Telix Pharmaceuticals received U.S. FDA approval for Gozellix, a radiopharmaceutical imaging agent using ^68Ga for PET scanning of PSMA-positive lesions in men with prostate cancer, offering longer shelf life and extended distribution to support precise tumor detection and staging

- In June 2025, Novartis AG reported that its targeted radioligand therapy Pluvicto demonstrated clinical effectiveness in slowing progression of metastatic prostate cancer in earlier disease settings that still respond to hormone therapy, suggesting future regulatory submissions for expanded indications beyond advanced stages

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.