Global Radiosurgery Systems Neurology Devices Market

Market Size in USD Billion

USD

1.99 Billion

USD

2.96 Billion

2024

2032

USD

1.99 Billion

USD

2.96 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.99 Billion | |

| USD 2.96 Billion | |

| % | |

|

Radiosurgery Systems (Neurology Devices) Market Size

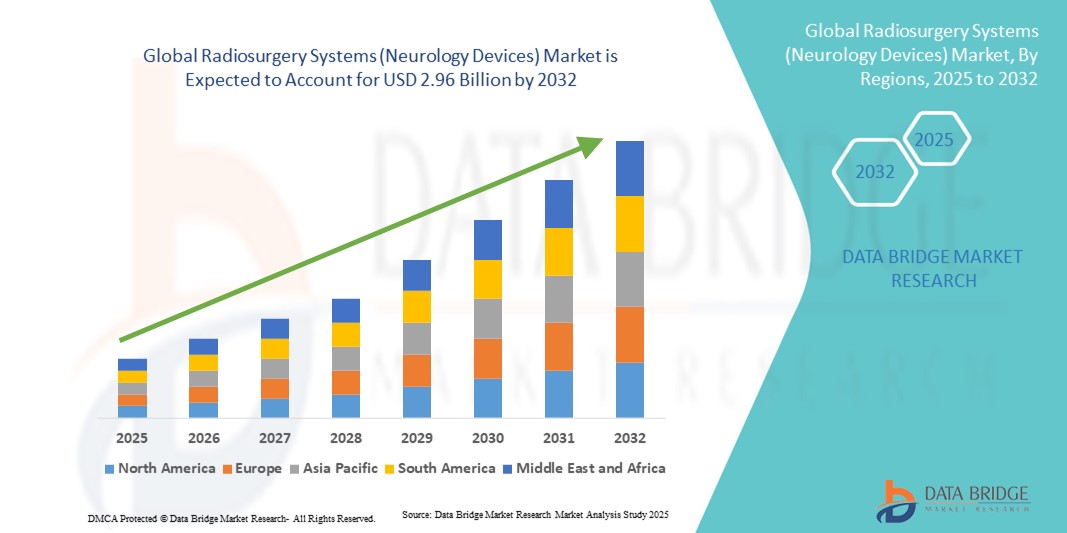

- The global radiosurgery systems (neurology devices) market size was valued at USD 1.99 billion in 2024 and is expected to reach USD 2.96 billion by 2032, at a CAGR of 5.11% during the forecast period

- The market growth is largely fueled by the increasing prevalence of neurological disorders, rising demand for minimally invasive treatment options, and advancements in precision radiosurgery technologies, leading to improved patient outcomes and procedural efficiency

- Furthermore, growing investments in healthcare infrastructure, rising adoption of advanced imaging and targeting systems, and increasing awareness among physicians and patients about non-invasive neurosurgical interventions are accelerating the uptake of radiosurgery systems (neurology devices) solutions, thereby significantly boosting the industry's growth

Radiosurgery Systems (Neurology Devices) Market Analysis

- Radiosurgery Systems (Neurology Devices) are critical medical devices designed to deliver precise, high-dose radiation to targeted areas in the brain and spine, offering minimally invasive treatment options for tumors, vascular malformations, and functional neurological disorders. Their growing adoption is driven by the increasing prevalence of neurological conditions, rising awareness of non-invasive treatment methods, and advancements in imaging and targeting technologies

- The escalating demand for radiosurgery systems is primarily fueled by expanding healthcare infrastructure, the rising number of specialized neurosurgeries centers, and growing investment in advanced medical technologies. Hospitals and diagnostic centers are increasingly prioritizing radiosurgery solutions for their precision, reduced patient recovery times, and ability to treat complex conditions with minimal side effects.

- North America dominated the radiosurgery systems (neurology devices) market with the largest revenue share of 39.7% in 2024, characterized by advanced healthcare infrastructure, high awareness of neurological disorders, and the strong presence of key medical device manufacturers. The U.S. leads the regional market due to widespread adoption of radiosurgery technologies in hospitals, specialized neurosurgery centers, and research institutions, supported by favorable reimbursement policies and increasing investment in neurology-focused healthcare facilities

- Asia-Pacific is expected to be the fastest growing region in the radiosurgery systems (neurology devices) market during the forecast period due to increasing healthcare investments, rising prevalence of neurological disorders, growing number of neurosurgeries centers, and increasing awareness of non-invasive treatment options in countries such as China, India, and Japan

- The Deep Brain Stimulation (DBS) segment dominated the radiosurgery systems (neurology devices) market with the largest revenue share of 46% in 2024, primarily due to its efficacy in treating Parkinson’s disease, essential tremor, and dystonia. DBS is increasingly favored over pharmacological therapy for long-term management of movement disorders, leading to higher adoption in neurology clinics and hospitals

Report Scope and Radiosurgery Systems (Neurology Devices) Market Segmentation

|

Attributes |

Radiosurgery Systems (Neurology Devices) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Radiosurgery Systems (Neurology Devices) Market Trends

Growing Adoption of Minimally Invasive Neurological Treatments

- A significant and accelerating trend in the global radiosurgery systems (neurology devices) market is the increasing adoption of minimally invasive treatments for neurological disorders. These systems provide high precision targeting of tumors, vascular malformations, and functional neurological conditions without the need for open surgery, reducing patient recovery time and procedural risks

- For instance, hospitals and specialized neurosurgery centers are increasingly integrating Gamma Knife and CyberKnife systems into their treatment protocols, allowing for precise, non-invasive therapy for complex brain and spinal conditions

- Advancements in imaging technologies, such as high-resolution MRI and CT guidance, are enhancing the accuracy and safety of radiosurgery procedures, contributing to higher clinical adoption and improved patient outcomes

- The growing preference for non-invasive therapies among patients, combined with rising awareness of effective neurological treatment options, is driving increased demand for radiosurgery systems globally

- Manufacturers are focusing on developing compact, versatile, and high-precision systems suitable for both large hospital settings and specialized neurosurgery centers, expanding accessibility to advanced neurological care

- Technological improvements in real-time imaging, treatment planning, and radiation delivery are continuously enhancing treatment precision, efficiency, and safety, encouraging healthcare providers to invest in next-generation radiosurgery solutions

- Overall, the trend towards minimally invasive, patient-friendly, and precise neurological treatment solutions is reshaping clinical practice and driving sustained market growth worldwide

Radiosurgery Systems (Neurology Devices) Market Dynamics

Driver

Growing Need Due to Rising Neurological Disorder Prevalence and Advanced Treatment Adoption

- The increasing prevalence of neurological disorders, such as brain tumors, epilepsy, and movement disorders, coupled with the rising adoption of minimally invasive and precise treatment modalities, is a significant driver for the heightened demand for radiosurgery systems

- For instance, in April 2024, leading medical device manufacturers announced advancements in stereotactic radiosurgery platforms, integrating real-time imaging, robotic precision, and enhanced targeting capabilities. Such innovations by key companies are expected to accelerate the growth of the Radiosurgery Systems (Neurology Devices) industry in the forecast period

- As healthcare providers increasingly prioritize accuracy and patient safety, radiosurgery systems offer features such as non-invasive treatment, minimal recovery time, and highly targeted therapy, providing a compelling alternative to conventional surgical interventions

- Furthermore, the growing emphasis on outpatient neurology care, combined with increasing investments in hospital infrastructure and advanced neurosurgical centers, is driving adoption of radiosurgery systems across multiple healthcare settings

- The convenience of reduced procedure times, improved patient outcomes, and integration with advanced imaging and planning software are key factors propelling the adoption of radiosurgery systems in both hospitals and specialized neurology clinics. The trend towards precision medicine and the availability of user-friendly systems further contribute to market growth

Restraint/Challenge

High Initial Costs and Regulatory Complexities

- The high cost of acquiring and maintaining advanced radiosurgery systems poses a significant challenge to broader market penetration, particularly in developing regions or for smaller healthcare facilities

- In addition, stringent regulatory requirements and lengthy approval processes for neurology devices can delay market entry and limit the adoption of new systems

- Addressing these challenges through scalable financing models, leasing options, and enhanced post-market support is crucial for increasing accessibility. Companies are also focusing on training programs, service agreements, and streamlined regulatory compliance to reassure healthcare providers

- While prices for certain entry-level radiosurgery systems are gradually decreasing, premium systems with advanced robotic-assisted technologies, real-time imaging, and multi-modality integration continue to have high upfront costs, which can slow adoption in cost-sensitive markets

- Limited skilled personnel to operate advanced radiosurgery systems is a significant barrier, as specialized training is required for safe and effective treatment delivery. Shortages of trained neuro-oncologists, neurosurgeons, and radiation therapists can hinder adoption, particularly in smaller or rural hospitals

- Integration challenges with existing hospital infrastructure and imaging systems can also restrict the implementation of new radiosurgery solutions. Compatibility issues, need for system upgrades, and interoperability requirements can increase deployment time and costs

- Overcoming these barriers through government incentives, public-private partnerships, workforce training programs, and ongoing innovation in cost-effective, precise treatment solutions will be vital for sustained market growth in the radiosurgery systems sector

Radiosurgery Systems (Neurology Devices) Market Scope

The market is segmented on the basis of device type, neuro-surgery devices, neuro-stimulation devices, and end user.

- By Device Type

On the basis of device type, the radiosurgery systems (neurology devices) market is segmented into CSF Management Devices, CSF Shunt Devices, CSF Drainage Devices, and Interventional Neurology Devices. The CSF Shunt Devices segment dominated the largest market revenue share of 42.5% in 2024, driven by their crucial role in managing hydrocephalus and other cerebrospinal fluid-related disorders. These devices are widely adopted in hospitals and specialized neurology clinics due to their ability to effectively regulate intracranial pressure, improving patient outcomes and reducing complications. The segment benefits from ongoing technological innovations, such as programmable shunts that allow individualized therapy adjustments, boosting clinician confidence and patient compliance. In addition, rising global awareness about hydrocephalus and increasing neurosurgery procedure volumes further propel this segment.

The interventional neurology devices segment is expected to witness the fastest CAGR of 20.8% from 2025 to 2032, owing to the growing trend toward minimally invasive procedures. These devices enable precise interventions with reduced recovery times and lower complication rates, making them increasingly preferred by neurosurgeons and patients alike. Technological advancements such as robotic-assisted navigation, real-time imaging, and improved device ergonomics are accelerating adoption. The increasing availability of advanced healthcare infrastructure in emerging markets, coupled with rising awareness of non-surgical treatment options, is further boosting the segment’s growth.

- By Neuro-Surgery Devices

On the basis of neuro-surgery devices, the radiosurgery systems (neurology devices) market is segmented into neuro-endoscopes, stereotactic systems, ultrasonic aspirators, and aneurysm clips. The Stereotactic Systems segment held the largest market revenue share of 44% in 2024, driven by its unmatched precision in targeting deep or small brain lesions. These systems minimize damage to surrounding tissues, enabling safe treatment of tumors, vascular malformations, and functional neurosurgery procedures. Their widespread adoption is supported by technological improvements in imaging integration, robotic navigation, and software-assisted planning. Increasing neurosurgical procedural volumes in both developed and emerging regions, combined with rising investment in hospital infrastructure, further strengthens this segment’s market dominance.

The neuro-endoscopes segment is projected to witness the fastest CAGR of 19.5% from 2025 to 2032, fueled by the rising preference for minimally invasive neurosurgical techniques. These devices allow surgeons to access hard-to-reach areas of the brain with enhanced visualization and precision, reducing patient recovery time and surgical risks. Integration with high-definition imaging, navigation systems, and flexible instrument designs is increasing their usability and adoption. Growing demand in pediatric neurosurgery and expanding neurosurgery centers in emerging markets are additional factors driving this rapid growth.

- By Neuro-Stimulation Devices

On the basis of neuro-stimulation devices, the radiosurgery systems (neurology devices) market is segmented into spinal cord stimulation, deep brain stimulation, sacral nerve stimulation, vagus nerve stimulation, and gastric nerve stimulation. The Deep Brain Stimulation (DBS) segment dominated the largest revenue share of 46% in 2024, primarily due to its efficacy in treating Parkinson’s disease, essential tremor, and dystonia. DBS is increasingly favored over pharmacological therapy for long-term management of movement disorders, leading to higher adoption in neurology clinics and hospitals. Continuous technological advancements, including smaller implantable devices and enhanced programming capabilities, further contribute to market dominance. Increasing patient awareness and clinician preference for durable treatment options reinforce the segment’s leading position.

The spinal cord stimulation segment is expected to witness the fastest CAGR of 21% from 2025 to 2032, driven by rising incidences of chronic pain and growing preference for non-opioid pain management strategies. Technological improvements, such as rechargeable and wireless stimulators, allow greater patient comfort and treatment customization. Expanding awareness about neuromodulation therapies and increasing reimbursement coverage for chronic pain management procedures support rapid adoption. In addition, growing investments in outpatient neuromodulation centers further accelerate the segment’s growth trajectory.

- By End User

On the basis of end user, the radiosurgery systems (neurology devices) market is segmented into hospitals, neurology clinics, ambulatory care centers, and others. The hospitals segment accounted for the largest market revenue share of 48% in 2024, driven by high procedure volumes, availability of advanced imaging and surgical infrastructure, and the presence of specialized neurology departments. Hospitals are the primary adopters of comprehensive radiosurgery systems integrating device types, neuro-surgery tools, and neuro-stimulation solutions. Rising investments in state-of-the-art medical facilities and growing patient inflow further solidify hospital dominance in the market.

The neurology clinics segment is anticipated to witness the fastest CAGR of 22% from 2025 to 2032, owing to the expansion of specialized outpatient centers providing focused care for neurological disorders. Patients increasingly prefer clinics for convenience, faster scheduling, and personalized treatment. Technological advancements, such as compact radiosurgery and neuro-stimulation systems suitable for outpatient use, support rapid adoption. Government initiatives promoting outpatient neurology care, coupled with increasing patient awareness about minimally invasive treatment options, further drive this segment’s growth.

Radiosurgery Systems (Neurology Devices) Market Regional Analysis

- North America dominated the radiosurgery systems (neurology devices) market with the largest revenue share of 39.7% in 2024, characterized by advanced healthcare infrastructure, high awareness of neurological disorders, and the strong presence of key medical device manufacturers

- The market due to widespread adoption of radiosurgery technologies in hospitals, specialized neurosurgery centers, and research institutions, supported by favorable reimbursement policies and increasing investment in neurology-focused healthcare facilities

- The region’s market growth is further strengthened by the increasing prevalence of neurological conditions and the growing preference for minimally invasive, precise treatment modalities. High healthcare expenditure, availability of trained neurosurgeons, and strong government support for advanced medical technologies also contribute to the dominance of North America in this market

U.S. Radiosurgery Systems (Neurology Devices) Market Insight

The U.S. radiosurgery systems (neurology devices) market captured the largest revenue share within North America in 2024, driven by the rapid adoption of advanced radiosurgery systems in clinical settings. Hospitals and specialized neurosurgery centers are increasingly investing in high-precision equipment to treat brain and spinal disorders non-invasively. The U.S. market is further fueled by extensive research initiatives, collaboration between medical device companies and academic institutions, and supportive reimbursement frameworks for radiosurgery procedures.

Europe Radiosurgery Systems (Neurology Devices) Market Insight

The Europe radiosurgery systems (neurology devices) market is projected to grow at a substantial CAGR during the forecast period, supported by rising healthcare expenditure, increasing awareness of non-invasive neurosurgical treatments, and government initiatives promoting advanced medical technologies. Countries such as Germany, France, and Italy are witnessing significant investments in hospital infrastructure, facilitating the adoption of radiosurgery systems across public and private healthcare facilities. Enhanced precision, reduced patient recovery times, and integration with diagnostic imaging solutions are key factors driving market growth in Europe.

U.K. Radiosurgery Systems (Neurology Devices) Market Insight

The U.K. radiosurgery systems (neurology devices) market is anticipated to grow at a noteworthy CAGR, driven by increasing prevalence of neurological disorders, rising demand for minimally invasive neurosurgical solutions, and advancements in radiosurgery technology. Growing patient awareness and the expansion of private neurology centers are further propelling the adoption of radiosurgery systems. Government-backed healthcare programs supporting the use of advanced treatment options are also contributing to market growth.

Germany Radiosurgery Systems (Neurology Devices) Market Insight

Germany radiosurgery systems (neurology devices) market is expected to witness considerable growth in the radiosurgery systems market due to the country’s strong healthcare infrastructure, focus on medical innovation, and high demand for precision neurosurgery. Hospitals and research institutions are increasingly adopting radiosurgery technologies for treating complex neurological conditions. Furthermore, initiatives promoting sustainable and technologically advanced medical equipment are driving adoption in both public and private healthcare sectors.

Asia-Pacific Radiosurgery Systems (Neurology Devices) Market Insight

The Asia-Pacific radiosurgery systems (neurology devices) market is expected to grow at the fastest CAGR during the forecast period, driven by increasing healthcare investments, rising prevalence of neurological disorders, expanding number of neurosurgery centers, and growing awareness of non-invasive treatment options in countries such as China, India, and Japan. Rising government initiatives supporting advanced medical technologies, coupled with expanding hospital infrastructure and increasing healthcare expenditure, are key factors propelling market growth in the region.

Japan Radiosurgery Systems (Neurology Devices) Market Insight

Japan’s radiosurgery systems (neurology devices) market is gaining momentum due to the country’s high-tech healthcare environment, rapid urbanization, and increasing demand for minimally invasive neurological treatments. Hospitals are increasingly investing in advanced radiosurgery systems to improve patient outcomes and reduce hospital stay durations. The aging population is also contributing to higher demand for precise and non-invasive treatment options in both clinical and research settings.

China Radiosurgery Systems (Neurology Devices) Market Insight

The China radiosurgery systems (neurology devices) market accounted for the largest revenue share in Asia-Pacific in 2024, supported by rapid urbanization, rising healthcare investments, growing prevalence of neurological disorders, and increasing awareness of non-invasive radiosurgery options. Expansion of hospital networks, government support for advanced medical technologies, and strong domestic manufacturing of neurosurgical devices are further fueling market growth. Increasing accessibility to high-quality treatment options across urban and semi-urban regions is also driving adoption.

Radiosurgery Systems (Neurology Devices) Market Share

The radiosurgery systems (neurology devices) industry is primarily led by well-established companies, including:

- Accuray Incorporated (U.S.)

- Siemens Healthineers AG (Germany)

- Brainlab SE (Germany)

- ViewRay, Inc. (U.S.)

- Best Theratronics Ltd. (Canada)

- Huiheng Medical, Inc. (China)

- MASEP Medical Science & Technology Development Co., Ltd. (China)

- Neusoft Medical Systems Co., Ltd. (China)

- ZAP Surgical Systems, Inc. (U.S.)

- Mevion Medical Systems (U.S.)

- Nordion Inc. (Canada)

- Hitachi, Ltd. (Japan)

- Mitsubishi Electric Corporation (Japan)

Latest Developments in Global Radiosurgery Systems (Neurology Devices) Market

- In March 2025, ZAP Surgical Systems, Inc. introduced the ZAP-Axon Radiosurgery Planning System, a new software platform dedicated to the company's ZAP-X Gyroscopic Radiosurgery system. Designed to simplify, accelerate, and enhance treatment planning, Axon aims to set new benchmarks in radiosurgery brain tumor treatments. The system was pending FDA 510(k) clearance at the time and was expected to be available in Spring 2025

- In June 2025, a clinical study published in the journal Cureus reported two cases of meningioma patients treated with the novel radiosurgical device ZAP-X stereotactic radiosurgery. This study demonstrated the effectiveness of the ZAP-X system in treating skull base meningiomas, showcasing its potential in neurosurgical applications

- In April 2025, Accuray announced that new data on the clinical use of the CyberKnife System reinforced the device's broad-based radiation treatment capabilities for central nervous system (CNS) conditions. The studies showcased the versatility and effectiveness of the CyberKnife System in treating various neurological disorders

- In November 2023, radiation oncologists at the University of Alabama at Birmingham Heersink School of Medicine and Vanderbilt University Medical Center shared their pioneering experiences using Varian platforms for stereotactic radiosurgery (SRS). This collaboration highlighted the growing adoption of frameless radiosurgery programs in the U.S. for treating essential tremors

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.