Global Radiotheranostics Market

Market Size in USD Billion

USD

5.73 Billion

USD

16.58 Billion

2024

2032

USD

5.73 Billion

USD

16.58 Billion

2024

2032

| 2025 - 2032 | |

| USD 5.73 Billion | |

| USD 16.58 Billion | |

| % | |

|

Radiotheranostics Market Size

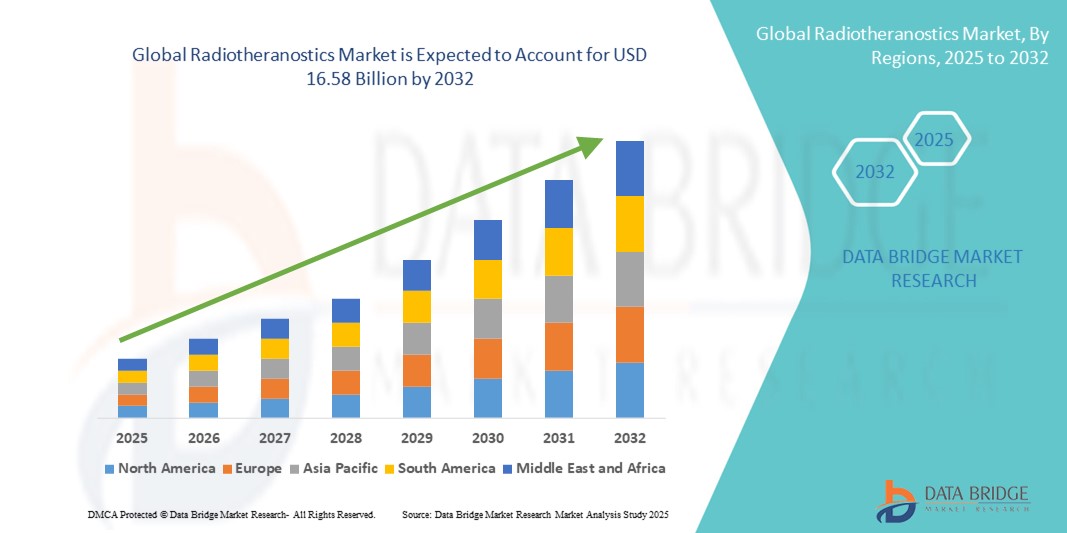

- The global radiotheranostics market size was valued at USD 5.73 billion in 2024 and is expected to reach USD 16.58 billion by 2032, at a CAGR of 14.20% during the forecast period

- The market growth is largely fueled by the increasing adoption of precision medicine and advancements in nuclear imaging technologies, driving the integration of diagnostic and therapeutic capabilities into a single radiopharmaceutical platform

- Furthermore, rising demand for targeted cancer treatment solutions that minimize damage to healthy tissues is establishing radiotheranostics as a transformative approach in oncology care. These converging factors are accelerating the uptake of radiotheranostic solutions, thereby significantly boosting the industry's growth

Radiotheranostics Market Analysis

- Radiotheranostics, offering a combination of diagnostic imaging and targeted radiotherapy using radiopharmaceuticals, are becoming increasingly vital in precision oncology and personalized medicine, particularly for cancers such as prostate cancer, neuroendocrine tumors, and thyroid cancer. These dual-purpose agents enhance patient outcomes by enabling real-time disease monitoring and highly specific treatment delivery

- The escalating demand for radiotheranostic solutions is primarily driven by the growing global burden of cancer, advancements in nuclear medicine, increased adoption of precision medicine, and the expanding pipeline of radioligand therapies. Government funding and private investments in molecular imaging and theranostics are also accelerating market growth

- North America dominated the radiotheranostics market with the largest revenue share of 43% in 2024, supported by the presence of advanced nuclear medicine infrastructure, high healthcare spending, and a strong network of key players such as Novartis (Lutathera, Pluvicto) and Bracco. The U.S. market is particularly witnessing rapid expansion due to FDA approvals of new radiotheranostic agents and increasing PET/CT scan utilization

- Asia-Pacific is expected to be the fastest-growing region in the radiotheranostics market during the forecast period, fueled by rising cancer prevalence, increasing investments in nuclear medicine capabilities, and initiatives to improve access to precision oncology, especially in China, India, and Japan

- The oncology segment dominated the radiotheranostics market with a revenue share of 87.9% in 2024, primarily driven by the high global cancer burden and increasing demand for targeted radionuclide therapies in conditions such as prostate cancer, neuroendocrine tumors, and thyroid cancer. Radiotheranostics allows for both diagnosis and therapy using the same molecular target, making it a cornerstone in personalized cancer treatment

Report Scope and Radiotheranostics Market Segmentation

|

Attributes |

Radiotheranostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Radiotheranostics Market Trends

Advancements in Precision Medicine and Integrated Imaging Technologies

- A significant and accelerating trend in the global radiotheranostics market is the increasing integration of advanced imaging and therapeutic technologies, particularly in nuclear medicine. The combination of radiopharmaceutical diagnostics and therapeutics is enabling healthcare professionals to detect, target, and treat cancers more precisely and effectively in a single clinical workflow

- For instance, radioligand therapies such as Lutetium-177 PSMA-617 (Pluvicto) and Actinium-225-based agents are being used alongside PET imaging to both locate and eliminate cancer cells in metastatic prostate and neuroendocrine tumors. These therapies, approved or in late-stage trials, represent a paradigm shift in oncology care

- Integration with AI-enabled diagnostic platforms helps enhance imaging analysis, segment tumors, predict treatment outcomes, and personalize dosage. Leading imaging systems from companies such as Siemens Healthineers, GE HealthCare, and Philips now support hybrid PET/CT and SPECT/CT systems designed specifically for radiotheranostic workflows

- Furthermore, advances in automated radiopharmaceutical production and dosimetry software allow clinicians to tailor treatments based on tumor burden and patient-specific characteristics. This integrated approach boosts treatment efficacy while reducing toxicity

- The adoption of centralized digital platforms is also transforming radiotheranostics. Hospitals and imaging centers are integrating patient data, imaging results, and therapy outcomes to improve interdisciplinary decision-making. Vendors such as Curium Pharma, Telix Pharmaceuticals, and SOFIE Biosciences are investing in AI-powered analytics to support physicians throughout the theranostic cycle

- This trend towards integrated, intelligent, and patient-specific radiopharmaceutical solutions is reshaping the future of cancer diagnostics and treatment. As global demand for targeted oncology solutions continues to rise, radiotheranostics is becoming a central pillar of precision medicine

Radiotheranostics Market Dynamics

Driver

Growing Need Due to Rising Cancer Burden and Demand for Precision Oncology

- The increasing global burden of cancer, coupled with a growing demand for targeted and personalized treatment, is a significant driver for the rising adoption of radiotheranostics solutions

- For instance, in April 2024, Telix Pharmaceuticals announced the expansion of its Illuccix (Ga-68 PSMA) diagnostic product into new markets across Asia-Pacific and Europe. This expansion reflects the growing clinical interest in combining molecular imaging and radiopharmaceutical therapy, especially in prostate and neuroendocrine cancers

- As healthcare systems seek to enhance oncology outcomes, radiotheranostics offers a compelling value proposition by enabling both precise imaging and targeted radionuclide therapy. These dual-function agents help clinicians localize tumors and deliver therapeutic isotopes directly to cancer cells while minimizing off-target damage

- Furthermore, advancements in PET/CT, SPECT/CT, and hybrid imaging technologies, coupled with increased availability of theranostic tracers (such as Lutetium-177, Actinium-225, and Iodine-131), are making radiotheranostics an integral part of modern cancer care workflows

- The convenience of personalized dosimetry, growing infrastructure of cyclotron production, and regulatory approvals for theranostic drugs in major markets are key factors propelling adoption in both clinical and research environments. In addition, the rise of centralized radio-pharmacies and dedicated theranostic centers is improving access and accelerating market penetration

Restraint/Challenge

High Infrastructure Costs and Regulatory Complexities

- Despite its promising clinical value, the high capital investment required for theranostic imaging equipment (e.g., PET/CT scanners, cyclotrons) and the infrastructure for handling radiopharmaceuticals pose challenges for widespread implementation, especially in low- and middle-income countries

- Furthermore, strict regulatory pathways and evolving compliance requirements related to radioisotope handling, patient safety, and dosimetry protocols can delay product approvals and limit the adoption of new agents

- For instance, the FDA's heightened scrutiny on radiopharmaceutical therapies has slowed market entry for emerging companies, requiring additional investment in clinical trials and safety monitoring

- Another challenge is the limited availability of trained nuclear medicine specialists, especially in emerging markets. This human resource gap can restrict the deployment and utilization of radiotheranostic systems despite infrastructure readiness

- Overcoming these challenges through international harmonization of regulatory guidelines, training programs for nuclear medicine professionals, and public-private partnerships to subsidize capital infrastructure will be critical for sustained growth in the global Radiotheranostics market

Radiotheranostics Market Scope

The market is segmented on the basis of radioisotope and application.

- By Radioisotope

On the basis of radioisotope, the Radiotheranostics market is segmented into Iodine-131, Iodine-123, Gallium-68, Lutetium-177, and Others. The Lutetium-177 segment dominated the market with the largest revenue share of 34.7% in 2024, driven by its widespread use in targeted radionuclide therapy for prostate cancer and neuroendocrine tumors. The segment's popularity is due to its effective tumor-targeting ability with minimal damage to surrounding tissues and growing clinical trial data supporting its efficacy.

The Gallium-68 segment is anticipated to witness the fastest growth rate of 22.3% from 2025 to 2032, fueled by its increasing application in PET imaging for prostate cancer and neuroendocrine tumors. Gallium-68 radiopharmaceuticals offer high diagnostic accuracy and are becoming widely available through generators, making them a cost-effective option for hospitals and imaging centers.

- By Application

On the basis of application, the radiotheranostics market is segmented into oncology and non-oncology. The Oncology segment accounted for the largest revenue share of 87.9% in 2024, primarily driven by the high global cancer burden and increasing demand for targeted radionuclide therapies in conditions such as prostate cancer, neuroendocrine tumors, and thyroid cancer. Radiotheranostics allows for both diagnosis and therapy using the same molecular target, making it a cornerstone in personalized cancer treatment.

The Non-Oncology segment is expected to grow at a CAGR of 12.5% from 2025 to 2032, driven by increasing research into theranostic approaches for cardiovascular diseases, neurological disorders, and inflammatory conditions.

Radiotheranostics Market Regional Analysis

- North America dominated the radiotheranostics market with the largest revenue share of 43% in 2024, driven by the region’s advanced nuclear medicine infrastructure, strong reimbursement policies, and early adoption of personalized medicine

- Significant investment in molecular imaging and the rising prevalence of cancer and neuroendocrine tumors have supported the integration of radiotheranostic agents in clinical practice

- The U.S. leads the region due to the presence of major pharmaceutical players, robust clinical trial activity, and increasing FDA approvals of radiotheranostic agents, such as Lutathera (lutetium Lu 177 dotatate). Collaborations between research institutions and radiopharmaceutical developers continue to drive market innovation and uptake

U.S. Radiotheranostics Market Insight

The U.S. radiotheranostics market captured the largest revenue share of 82% in 2024 within North America, fueled by significant investment in nuclear medicine technologies, radiopharmaceutical manufacturing, and personalized cancer therapies. The market is further strengthened by streamlined regulatory pathways from the FDA, favorable reimbursement frameworks from CMS, and growing adoption of theranostic approaches in prostate and neuroendocrine tumor management.

Europe Radiotheranostics Market Insight

The Europe radiotheranostics market is projected to expand at a substantial CAGR throughout the forecast period, led by expanding access to PET/CT technologies, pan-European health initiatives, and the strong presence of radiopharmaceutical manufacturers in Germany, France, and Switzerland. EMA approvals and public-private research collaborations support innovation across the region.

U.K. Radiotheranostics Market Insight

The U.K. radiotheranostics market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by NHS initiatives to improve cancer care pathways and expand radiotherapy services. Increased research funding, particularly in Oxford and London hubs, is encouraging clinical application of novel theranostic compounds.

Germany Radiotheranostics Market Insight

The Germany radiotheranostics market is expected to expand significantly, driven by its leadership in radiopharmaceutical production, nuclear medicine research, and imaging technology. Government investment in oncology diagnostics and the presence of companies such as ITM Radiopharma contribute to Germany’s role as a European hub for radiotheranostics innovation.

Asia-Pacific Radiotheranostics Market Insight

The Asia-Pacific radiotheranostics market is poised to grow at the fastest CAGR of 25.4% from 2025 to 2032, owing to rising cancer incidence, government investments in nuclear medicine infrastructure, and increasing public-private partnerships in countries such as China, India, and Japan. Growing access to PET/CT and SPECT systems is improving diagnosis and enabling broader adoption of radiotheranostic therapies.

Japan Radiotheranostics Market Insight

The Japan radiotheranostics market is expanding steadily, supported by its aging population, high cancer screening rates, and regulatory support for advanced radiopharmaceuticals. Local manufacturers and academic hospitals are accelerating clinical adoption, particularly in neuroendocrine tumor and prostate cancer treatment.

China Radiotheranostics Market Insight

The China radiotheranostics market accounted for the largest revenue share in Asia Pacific in 2024, driven by rapid urbanization, healthcare reforms, and the government’s strong emphasis on nuclear medicine. The rise of local pharmaceutical manufacturers and the increasing availability of gallium-68 and lutetium-177 isotopes are driving adoption across oncology care pathways.

Radiotheranostics Market Share

The radiotheranostics industry is primarily led by well-established companies, including:

- Novartis AG (Germany)

- Bayer AG (Germany)

- Telix Pharmaceuticals Limited (Australia)

- ITM Radiopharma (Germany)

- RadioMedix (U.S.)

- IsoTherapeutics Group, LLC (U.S.)

- Q BioMed Inc. (U.S.)

- Curium (France)

- Lilly (U.S.)

- Fusion Pharma (U.S.)

- Eckert & Ziegler (Germany)

- NMR (U.S.)

Latest Developments in Global Radiotheranostics Market

- In December 2024, Nucleus RadioPharma published a comprehensive recap of major clinical trials and early-stage radiopharmaceutical therapies in radiotheranostics, signaling growing momentum in the sector’s pipeline

- In July 2025, a peer‑reviewed article reported emerging radionuclides and molecular targets in oncology PET and theranostics, including Gallium‑68 and Lutetium‑177, underlining next‑generation precision imaging and treatment agents

- In 2025, M Health Fairview (USA) opened a state‑of‑the‑art radiotheranostics unit integrating a high‑end digital PET scanner, enhancing diagnostic throughput and cancer care capabilities

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.