Global Rare Hemophilia Factors Market

Market Size in USD Billion

USD

99.89 Billion

USD

160.41 Billion

2025

2033

USD

99.89 Billion

USD

160.41 Billion

2025

2033

| 2026 - 2033 | |

| USD 99.89 Billion | |

| USD 160.41 Billion | |

| % | |

|

Rare Hemophilia Factors Market Overview

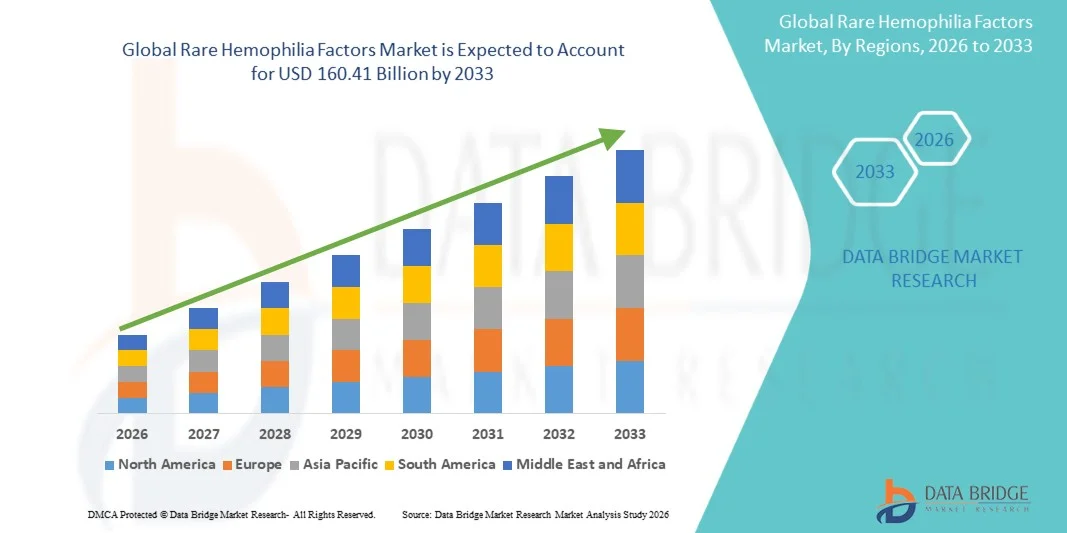

The Rare Hemophilia Factors Market was valued at USD 99.89 billion in 2025 and is projected to reach USD 160.41 billion by 2033, growing at a CAGR of 6.10% from 2026 to 2033. The market is experiencing consistent growth driven by rising prevalence of rare bleeding disorders, increasing demand for advanced clotting factor replacement therapies, rapid advancements in recombinant and gene-based treatments, and expanding access to specialized hemophilia care worldwide.

The growing need for effective management of rare hemophilia factor deficiencies, combined with increasing awareness, improved diagnostic capabilities, and rising adoption of prophylactic treatment approaches, is encouraging healthcare providers and patients to adopt advanced therapies. Recombinant factor concentrates, extended half-life products, and emerging gene therapy approaches are transforming rare hemophilia management by reducing bleeding episodes, improving quality of life, and providing more personalized treatment options. Increasing investments by pharmaceutical companies in innovative therapies, regulatory approvals for novel factor products, and expansion of specialized treatment centers are further accelerating the growth of the Rare Hemophilia Factors Market.

Key Market Trends & Insights

- North America dominated the Rare Hemophilia Factors Market with the largest revenue share of 39.6% in 2025, supported by advanced healthcare infrastructure, high diagnosis rates of rare bleeding disorders, strong presence of leading coagulation factor manufacturers, favorable reimbursement policies, and increasing adoption of advanced recombinant and extended half-life factor replacement therapies. The region also benefits from well-established hemophilia treatment centers, increasing availability of genetic testing, and growing investments in innovative therapies such as gene therapy and personalized treatment approaches.

- The Factor VII segment dominated the market with the largest share of 66% in 2025, owing to increasing diagnosis of rare bleeding disorders, rising demand for factor replacement therapies, and growing adoption of recombinant Factor VII products for managing bleeding episodes.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 9.1% from 2026 to 2033, fueled by increasing awareness regarding rare bleeding disorders, improving access to specialized hematology care, rising healthcare expenditure, expansion of hemophilia treatment centers, and growing adoption of advanced factor replacement therapies in countries such as China, India, Japan, and South Korea.

- Gene Therapy and Advanced Biologic Therapies are the fastest-growing treatment approach, projected to register a CAGR of 12.4%, reflecting increasing demand for long-term treatment solutions that reduce dependence on regular factor replacement therapy. Advancements in genetic medicine, clinical trials for hemophilia gene therapies, and growing investments in next-generation treatment platforms are accelerating segment growth.

- Hemophilia A Treatment segment dominates the rare hemophilia factors category with a 64.7% revenue share in 2025, led by the higher patient population compared with other rare hemophilia types, increasing utilization of Factor VIII replacement therapies, and rising adoption of recombinant and extended half-life products to improve treatment outcomes.

Market Size & Forecast

- Global Market Value (2025): USD 99.89 Billion

- Expected Market Value (2033): USD 160.41 Billion

- Forecast CAGR (2026–2033): 6.10%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Rare Hemophilia Factors Market Segmentation

|

Attributes |

Rare Hemophilia Factors Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Takeda Pharmaceutical Company (Japan) |

|

Market Opportunities |

· Increasing Adoption of Recombinant and Extended Half-Life Factor Therapies · Growing Potential of Gene Therapy and Novel Treatment Approaches · Expansion of Hemophilia Care Infrastructure in Emerging Markets |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Rare Hemophilia Factors Market Trends

Trend: Rising Adoption of Personalized and Advanced Factor Replacement Therapies

Healthcare providers are increasingly adopting personalized treatment approaches for rare hemophilia disorders to improve bleeding control, reduce treatment burden, and enhance patient quality of life. The growing use of genetic testing, molecular diagnostics, and individualized treatment planning is enabling clinicians to select appropriate factor replacement strategies based on patient-specific disease characteristics. The adoption of recombinant coagulation factors, extended half-life therapies, and non-factor replacement approaches is transforming the management of rare hemophilia conditions by reducing infusion frequency and improving long-term disease control. According to global hemophilia care trends, approximately 400,000 people worldwide are estimated to live with hemophilia, with a significant proportion requiring lifelong management through advanced therapies. Recent developments in gene therapy and next-generation biologics are further reshaping the treatment landscape, with companies focusing on durable treatment options that may reduce dependence on regular factor replacement therapy.

Rare Hemophilia Factors Market Dynamics

Key Market Driver: Increasing Prevalence of Rare Bleeding Disorders and Growing Adoption of Advanced Factor Replacement Therapies

The rising diagnosis of rare hemophilia disorders, increasing awareness of inherited bleeding conditions, and expansion of specialized hematology care are creating strong demand for Rare Hemophilia Factors globally. Hemophilia A and Hemophilia B remain among the most common inherited bleeding disorders, driven by mutations affecting Factor VIII and Factor IX production. Healthcare systems across North America, Europe, and Asia-Pacific are increasingly investing in hemophilia treatment centers, genetic screening programs, and improved access to recombinant and extended half-life factor therapies. For instance, the growing adoption of extended half-life recombinant Factor VIII and Factor IX products has improved treatment convenience by reducing infusion frequency compared with conventional replacement therapies. In addition, increasing government initiatives, patient support programs, and improvements in diagnosis rates are accelerating the adoption of advanced coagulation factor products worldwide.

Key Restraint/Challenge: High Cost of Advanced Hemophilia Therapies and Limited Access in Emerging Markets

A major challenge in the Rare Hemophilia Factors Market is the high cost associated with recombinant factors, extended half-life therapies, and emerging gene-based treatments. The production of advanced coagulation therapies requires complex biotechnology manufacturing, strict quality control processes, and specialized distribution systems, resulting in significant treatment costs. In addition, many rare hemophilia therapies require lifelong administration, increasing the overall healthcare burden for patients and healthcare systems. Limited availability of specialized hematology centers, shortage of trained healthcare professionals, and unequal access to reimbursement programs continue to restrict adoption in low- and middle-income countries. Advanced therapies such as gene therapy also involve substantial upfront costs, creating affordability challenges despite their potential long-term benefits.

Key Market Opportunity: Expansion of Gene Therapy, Digital Health, and Next-Generation Hemophilia Treatment Platforms

The integration of gene therapy, precision medicine, and digital healthcare solutions presents a significant growth opportunity for the Rare Hemophilia Factors market. Researchers and biotechnology companies are increasingly developing one-time or long-duration treatment approaches aimed at reducing dependence on frequent factor infusions. For example, the approval and commercialization of gene therapies for hemophilia A and B represent a major advancement in the treatment landscape by offering the possibility of sustained factor expression in eligible patients. In addition, digital health platforms, remote monitoring tools, and patient management technologies are improving treatment adherence and enabling personalized care models. Increasing investments in biotechnology research, expansion of specialized treatment infrastructure, and growing adoption of advanced therapies across Asia-Pacific, Latin America, and the Middle East are expected to create new market opportunities.

Rare Hemophilia Factors Market Scope

The Rare Hemophilia Factors market is segmented on the basis of type and application.

- By Type

On the basis of type, the Rare Hemophilia Factors Market is segmented into Factor I, Factor II, Factor V, Factor VII, Factor X, Factor XI, and Factor XIII. The Factor VII segment dominated the market with the largest share of 66% in 2025, owing to increasing diagnosis of rare bleeding disorders, rising demand for factor replacement therapies, and growing adoption of recombinant Factor VII products for managing bleeding episodes. Factor VII deficiency, although rare, requires specialized treatment approaches, and the availability of advanced recombinant therapies has improved patient outcomes. Increasing awareness among healthcare providers, expansion of hemophilia treatment centers, and advancements in coagulation factor manufacturing are supporting segment growth. In addition, rising investments by pharmaceutical companies in rare disease therapies are strengthening the adoption of Factor VII-based treatments globally.

The Factor XIII segment is expected to witness the fastest growth at a CAGR from 2026 to 2033, driven by increasing recognition of congenital Factor XIII deficiency and growing demand for targeted replacement therapies. Factor XIII deficiency requires lifelong management due to the risk of severe bleeding complications, creating demand for specialized factor concentrates. Advancements in recombinant protein technologies, improved diagnostic screening, and increasing access to rare bleeding disorder treatments are expected to accelerate segment expansion. Furthermore, growing focus on personalized medicine and development of innovative coagulation therapies is creating new opportunities for Factor XIII treatment adoption.

- By Application

On the basis of application, the Rare Hemophilia Factors Market is segmented into Fresh Frozen Plasma, Factor Concentrates, Cryoprecipitate, and Others. The Factor Concentrates segment dominated the market with the largest share of 55% in 2025, supported by increasing preference for targeted replacement therapies, improved safety profiles, and growing adoption in hemophilia management. Factor concentrates provide specific clotting factor replacement and reduce dependence on plasma-derived therapies, making them a preferred treatment option among patients and healthcare providers. The segment is further supported by rising availability of recombinant factor products, extended half-life therapies, and prophylactic treatment approaches. Increasing healthcare investments, improved diagnosis rates, and expansion of specialized hemophilia care facilities are further driving segment growth.

The Factor Concentrates segment is expected to register the fastest CAGR from 2026 to 2033, driven by increasing demand for advanced clotting factor therapies, rising adoption of recombinant and extended half-life products, and growing focus on reducing bleeding frequency among rare hemophilia patients. Continuous innovation by biotechnology companies in developing safer and more effective factor replacement solutions is accelerating market expansion. In addition, increasing awareness regarding early diagnosis, improving reimbursement support in developed markets, and rising healthcare infrastructure development in emerging regions are expected to create significant growth opportunities for factor concentrate-based therapies.

Rare Hemophilia Factors Market Regional Analysis

North America dominated the Rare Hemophilia Factors Market and accounted for the largest revenue share of 39.6% in 2025, supported by advanced healthcare infrastructure, high diagnosis rates of rare bleeding disorders, strong presence of leading coagulation factor manufacturers, favorable reimbursement policies, and increasing adoption of advanced recombinant and extended half-life factor replacement therapies. The region also benefits from well-established hemophilia treatment centers, increasing availability of genetic testing, and growing investments in innovative therapies such as gene therapy and personalized treatment approaches. Rising healthcare expenditure, strong research activities, and early adoption of next-generation hemophilia treatments continue to strengthen North America’s leadership position in the global market.

U.S. Rare Hemophilia Factors Market Insight

The U.S. Rare Hemophilia Factors market is witnessing strong growth due to increasing prevalence and diagnosis of inherited bleeding disorders, expanding access to specialized hemophilia treatment centers, and rising adoption of advanced factor replacement therapies. The country’s strong biotechnology and pharmaceutical ecosystem, along with the presence of leading coagulation factor manufacturers, is driving innovation in recombinant factors, extended half-life products, and gene therapy approaches. In addition, favorable reimbursement frameworks, increasing genetic testing availability, and growing investments in personalized medicine are accelerating the adoption of advanced hemophilia treatment solutions across the country.

Europe Rare Hemophilia Factors Market Insight

The Europe Rare Hemophilia Factors market remains a major contributor to global revenue, driven by strong healthcare systems, increasing adoption of advanced hemophilia management strategies, and growing investments in rare disease treatment infrastructure. Countries across the region are focusing on improving diagnosis rates, expanding access to specialized hematology centers, and supporting innovative therapies for rare bleeding disorders. The increasing use of recombinant coagulation factors, extended half-life therapies, and personalized treatment approaches is supporting market expansion. In addition, government-supported rare disease programs and clinical research initiatives continue to enhance the adoption of advanced hemophilia treatments across Europe.

U.K. Rare Hemophilia Factors Market Insight

The U.K. Rare Hemophilia Factors market is experiencing steady growth, supported by the presence of specialized hemophilia care networks, increasing adoption of advanced coagulation therapies, and strong focus on rare disease management. The country’s healthcare system is actively integrating genetic testing, personalized treatment strategies, and innovative factor replacement therapies into clinical practice. Increasing research activities in gene therapy, improving patient monitoring systems, and rising availability of advanced treatment options are contributing to market development. Furthermore, collaborations between healthcare institutions and biotechnology companies are supporting innovation in hemophilia care across the U.K.

Germany Rare Hemophilia Factors Market Insight

The Germany Rare Hemophilia Factors market is expanding steadily due to its advanced healthcare infrastructure, strong pharmaceutical industry, and increasing adoption of innovative hematology treatments. The country has well-established specialized treatment centers and advanced diagnostic capabilities supporting early identification and management of rare bleeding disorders. Growing investments in biotechnology research, recombinant factor development, and personalized medicine are driving market growth. In addition, Germany’s strong focus on healthcare innovation and access to advanced therapies is supporting the expansion of Rare Hemophilia Factors solutions.

Asia-Pacific Rare Hemophilia Factors Market Insight

The Asia-Pacific Rare Hemophilia Factors market is expected to witness rapid growth at a CAGR of 9.1% from 2026 to 2033, driven by increasing awareness regarding rare bleeding disorders, improving access to specialized hematology care, rising healthcare expenditure, expansion of hemophilia treatment centers, and growing adoption of advanced factor replacement therapies in countries such as China, India, Japan, and South Korea. The region is experiencing improvements in disease diagnosis, increasing government initiatives for rare disease management, and rising investments in healthcare infrastructure. Furthermore, expanding availability of recombinant therapies, increasing adoption of genetic testing, and growing focus on personalized treatment approaches are creating significant growth opportunities across emerging markets.

Japan Rare Hemophilia Factors Market Insight

The Japan Rare Hemophilia Factors market is witnessing consistent growth due to the country’s advanced healthcare system, increasing focus on rare disease management, and high adoption of innovative medical technologies. Japan has strong diagnostic capabilities and specialized hematology centers supporting effective treatment of hemophilia patients. Rising adoption of recombinant coagulation factors, extended half-life therapies, and personalized treatment approaches is contributing to market expansion. In addition, increasing research activities in biotechnology and regenerative medicine are supporting the development of next-generation hemophilia treatment solutions.

China Rare Hemophilia Factors Market Insight

The China Rare Hemophilia Factors market is growing rapidly, driven by increasing awareness of rare bleeding disorders, expanding healthcare infrastructure, rising government focus on improving rare disease care, and increasing access to advanced treatment options. Growing investments in healthcare modernization, expansion of specialized hematology centers, and improving availability of diagnostic technologies are supporting market growth. In addition, increasing adoption of recombinant factor therapies, rising collaborations between domestic and international biotechnology companies, and growing focus on innovative treatments such as gene therapy are positioning China as one of the fastest-growing markets for Rare Hemophilia Factors globally.

Rare Hemophilia Factors Market Share

The Rare Hemophilia Factors industry is primarily led by well-established companies, including:

- Takeda Pharmaceutical Company (Japan)

- CSL Limited (Australia)

- Bayer AG (Germany)

- Novo Nordisk (Denmark)

- Pfizer Inc. (U.S.)

- Sanofi (France)

- Octapharma AG (Switzerland)

- Grifols S.A. (Spain)

- BioMarin Pharmaceutical Inc. (U.S.)

- Sobi (Sweden)

- F. Hoffmann-La Roche (Switzerland)

- Chugai Pharmaceutical (Japan)

- Kedrion Biopharma (Italy)

- LFB SA (France)

- CSL Behring (Australia)

- Novo Nordisk Hemophilia Biologics (Denmark)

- uniQure (Netherlands)

- Spark Therapeutics (U.S.)

- Pfizer Rare Disease (U.S.)

- Catalyst Biosciences (U.S.)

- HEMA Biologics (U.S.)

- Genentech (U.S.)

- Johnson & Johnson Innovative Medicine (U.S.)

- BPL Plasma (United Kingdom)

- Kamada Ltd. (Israel)

- Centogene (Germany)

- Aptevo Therapeutics (U.S.)

- Alnylam Pharmaceuticals (U.S.)

- Silence Therapeutics (United Kingdom)

- CRISPR Therapeutics (Switzerland)

- Editas Medicine (U.S.)

- Intellia Therapeutics (U.S.)

- Genzyme (U.S.)

Latest Developments in Rare Hemophilia Factors Market

- In August 2022, the U.S. FDA approved Rebinyn (coagulation Factor IX recombinant) developed by Novo Nordisk for the treatment and prevention of bleeding episodes in hemophilia B patients. The approval expanded access to extended half-life factor IX replacement therapy, allowing improved prophylactic management and reducing treatment burden compared with conventional factor IX products. This development highlighted the growing shift toward advanced recombinant factor concentrates for rare bleeding disorders

- In February 2023, Sanofi and its partner announced regulatory approval of ALTUVIIIO (efanesoctocog alfa), a next-generation recombinant Factor VIII therapy, by the U.S. FDA for hemophilia A treatment. The therapy was designed to provide sustained Factor VIII activity with once-weekly prophylaxis, addressing limitations associated with frequent infusions of traditional factor replacement therapies. This launch represented a major advancement in extended half-life hemophilia treatments

- In October 2023, BioMarin continued commercialization efforts for ROCTAVIAN (valoctocogene roxaparvovec), the first FDA-approved gene therapy for adults with severe hemophilia A. The therapy introduced a one-time gene therapy approach aimed at increasing production of functional Factor VIII and reducing dependence on regular factor replacement therapy. This milestone accelerated interest in gene-based approaches within the rare hemophilia treatment landscape

- In April 2024, Pfizer announced U.S. FDA approval of BEQVEZ (fidanacogene elaparvovec-dzkt), a one-time gene therapy for adults with hemophilia B. The therapy uses an adeno-associated virus vector to deliver a functional Factor IX gene, helping patients produce their own Factor IX and potentially reducing long-term treatment requirements. The approval strengthened the role of gene therapy as an emerging alternative to lifelong factor replacement

- In June 2024, Sanofi presented new clinical data for ALTUVIIIO and fitusiran at the International Society on Thrombosis and Haemostasis (ISTH) Congress, highlighting continued progress in hemophilia treatment innovation. The data demonstrated sustained bleed protection with ALTUVIIIO and supported the potential of fitusiran as a novel prophylactic approach for hemophilia A and B patients, including those with inhibitors. These developments reinforced the industry focus on reducing bleeding frequency and improving patient convenience

- In October 2024, the U.S. FDA approved Hympavzi (marstacimab-hncq) developed by Pfizer as a novel prophylactic treatment for hemophilia A and B. Hympavzi became the first treatment in its class targeting the tissue factor pathway inhibitor mechanism, offering a non-factor approach to reducing bleeding episodes. The approval represented a shift beyond traditional clotting factor replacement therapies toward alternative biological strategies

- In December 2024, Novo Nordisk received U.S. FDA approval for Alhemo (concizumab-mtci), a once-daily prophylactic injection for preventing bleeding episodes in hemophilia patients. The therapy introduced a new treatment approach designed to reduce bleeding events in patients with hemophilia A or B with inhibitors, expanding options for individuals with complex treatment needs

- In March 2025, the U.S. FDA approved Qfitlia (fitusiran) developed by Sanofi as the first antithrombin-lowering therapy for routine prophylaxis in hemophilia A and B patients with or without inhibitors. The treatment uses a novel mechanism to reduce bleeding frequency and can be administered less frequently than many existing therapies, addressing the need for convenient long-term management options in hemophilia care

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.