Global Rear Spoiler Market

Market Size in USD Billion

USD

6.17 Billion

USD

10.13 Billion

2025

2033

USD

6.17 Billion

USD

10.13 Billion

2025

2033

| 2026 - 2033 | |

| USD 6.17 Billion | |

| USD 10.13 Billion | |

| % | |

|

What is the Global Rear Spoiler Market Size and Growth Rate?

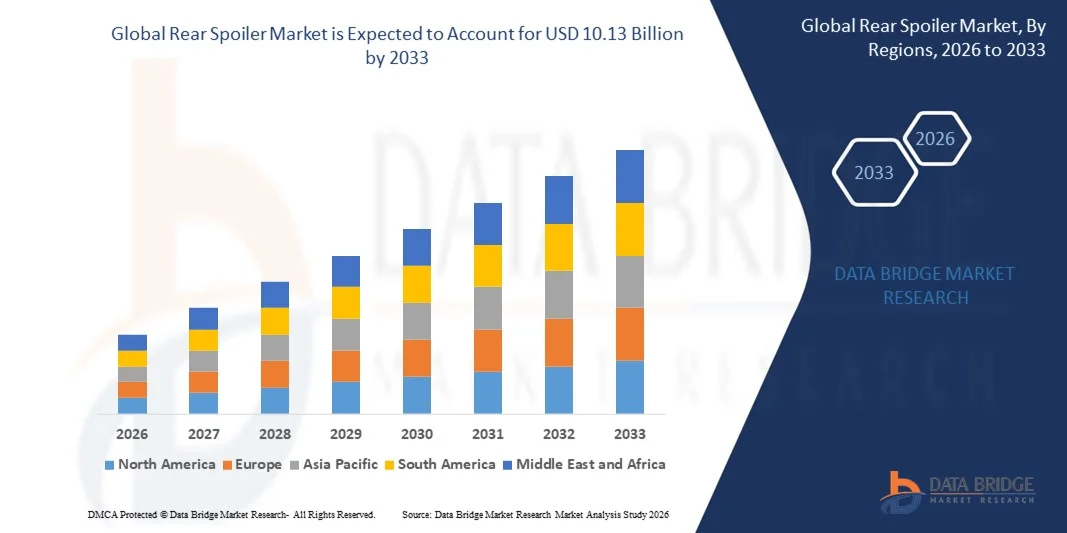

- The global rear spoiler market size was valued at USD 6.17 billion in 2025 and is expected to reach USD 10.13 billion by 2033, at a CAGR of 6.40% during the forecast period

- Growing demand for SUVs and MPVS across the globe, increasing production of vehicles along with rising demand of aesthetics, adoption of stringent norms regarding fuel economy and emission, rising preferences towards the usages of green vehicles, surging levels of investment by the market players for the growth of the automotive sector are some of the vital as well as important factors which will likely to accelerate the growth of the rear spoiler market

What are the Major Takeaways of Rear Spoiler Market?

- Increasing number of technological advancements, increasing demand of electric vehicles along with rising penetration of active spoiler which will further contribute by generating massive opportunities that will lead to the growth of the rear spoiler market

- Increasing trends of integrated roof spoilers along with less awareness among hatchback users which will likely to act as market restraints factor for the growth of the rear spoiler

- Asia-Pacific dominated the rear spoiler market with the largest revenue share of 41.6% in 2025, attributed to the strong presence of major automotive manufacturers, rising vehicle production, and growing demand for aerodynamic components across China, Japan, South Korea, and India

- North America is projected to witness the fastest growth rate of 9.7% during 2026–2033, fueled by high adoption of advanced aerodynamics in performance and electric vehicles

- The Injection Molding segment dominated the market with a revenue share of 46.7% in 2025, owing to its ability to produce complex shapes with high precision, cost-efficiency, and reduced material wastage

Report Scope and Rear Spoiler Market Segmentation

|

Attributes |

Rear Spoiler Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Rear Spoiler Market?

Growing Adoption of Lightweight Composite Materials to Enhance Vehicle Aerodynamics and Fuel Efficiency

- The Rear Spoiler market is witnessing a major trend toward the use of lightweight materials such as carbon fiber, ABS plastic, fiberglass, and polyurethane to reduce vehicle weight and improve fuel efficiency. These materials offer enhanced design flexibility and durability, supporting the rising demand for aerodynamic automotive components

- For instance, Magna International Inc. and Plastic Omnium have introduced advanced composite-based rear spoilers designed to improve downforce, reduce drag, and optimize vehicle stability in both passenger and sports vehicles

- The rising penetration of electric and hybrid vehicles (EVs) has further accelerated demand for aerodynamic designs that enhance energy efficiency and extend vehicle range

- Automakers are increasingly integrating active aerodynamic technologies, such as adjustable rear spoilers, to balance performance and efficiency dynamically

- The growing focus on sustainability and lightweight manufacturing is encouraging OEMs to adopt recyclable materials and eco-friendly production processes

- As the automotive industry evolves toward efficiency, sustainability, and smart aerodynamics, the use of advanced composite rear spoilers will remain a defining trend shaping future market dynamics

What are the Key Drivers of Rear Spoiler Market?

- The increasing demand for fuel-efficient and high-performance vehicles is one of the primary drivers of the rear spoiler market. Automakers are prioritizing aerodynamic efficiency to meet stringent emission regulations and improve vehicle stability at higher speeds

- For instance, in 2025, Porsche AG integrated adaptive aerodynamic systems, including retractable spoilers, in its latest sports car lineup to enhance performance and control

- The rise in EV production and the focus on extended battery range have led to greater adoption of rear spoilers for drag reduction and aerodynamic optimization

- Technological advancements in aerodynamic testing, simulation tools, and 3D printing are enabling manufacturers to design more precise, efficient, and customizable spoilers

- The growing popularity of SUVs, sports cars, and performance vehicles globally is driving higher demand for aesthetic and functional spoiler designs

- As consumer preference shifts toward sporty design and efficiency, the global rear spoiler market is expected to experience sustained growth supported by innovation and emission compliance goals

Which Factor is Challenging the Growth of the Rear Spoiler Market?

- Fluctuations in raw material costs, particularly for carbon fiber and polyurethane composites, pose a major challenge for rear spoiler manufacturers

- For instance, during 2024–2025, the surge in carbon fiber prices and supply chain disruptions impacted global production costs, delaying product deliveries across OEMs

- Intense competition among OEMs and aftermarket suppliers has led to price pressures and reduced profit margins in the market

- The high initial manufacturing and tooling costs associated with composite spoilers also hinder adoption among budget and mid-range vehicle manufacturers

- Strict regulatory and crash safety compliance standards require extensive testing, adding to development time and cost

- To overcome these challenges, market players are focusing on process optimization, material innovation, and strategic partnerships with OEMs to ensure cost efficiency, quality assurance, and competitive differentiation

How is the Rear Spoiler Market Segmented?

The market is segmented on the basis of technology, material, fuel, vehicle, distribution channel, design, and system type.

- By Technology

On the basis of technology, the rear spoiler market is segmented into Blow Molding, Injection Molding, and Reaction Injection Molding. The Injection Molding segment dominated the market with a revenue share of 46.7% in 2025, owing to its ability to produce complex shapes with high precision, cost-efficiency, and reduced material wastage. This process is extensively used for mass production of lightweight, durable spoilers in passenger and commercial vehicles.

The Reaction Injection Molding segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing demand for aerodynamic designs and advanced polymer materials in high-performance and luxury vehicles. Automakers are increasingly adopting RIM technology to achieve superior surface finish, dimensional stability, and weight reduction, which enhances overall fuel efficiency and vehicle aesthetics, aligning with the global trend toward sustainable automotive manufacturing.

- By Material

Based on material, the rear spoiler market is segmented into ABS Plastic, Fiberglass, Carbon Fiber, and Sheet Metal. The ABS Plastic segment dominated the market with the largest share of 39.5% in 2025, attributed to its cost-effectiveness, easy moldability, and high impact resistance. ABS spoilers are widely used in mass-market passenger vehicles due to their lightweight nature and ability to be seamlessly painted or textured to match vehicle aesthetics.

The Carbon Fiber segment is expected to register the fastest CAGR during 2026–2033, fueled by rising adoption in premium and sports cars where high strength-to-weight ratio and superior performance are essential. Increasing focus on electric and performance vehicles, coupled with growing OEM partnerships for sustainable composite materials, continues to drive carbon fiber usage in next-generation aerodynamic spoiler systems globally.

- By Fuel

On the basis of fuel, the rear spoiler market is segmented into ICE (Internal Combustion Engine), BEV (Battery Electric Vehicle), and Others (Hybrid). The ICE segment dominated the market with a revenue share of 63.8% in 2025, supported by the extensive use of spoilers in traditional gasoline and diesel-powered vehicles for enhanced stability and reduced drag. The presence of large-scale production facilities and established distribution networks further boosts demand.

The BEV segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing adoption of electric vehicles across major markets such as the U.S., China, and Europe. Electric vehicle manufacturers are integrating active and lightweight spoilers to enhance aerodynamics, improve range efficiency, and support eco-friendly vehicle designs — a trend strongly supported by global sustainability initiatives and emission reduction mandates.

- By Vehicle

Based on vehicle type, the rear spoiler market is segmented into Compact Passenger Cars, Mid-Sized Passenger Cars, Premium Passenger Cars, Luxury Passenger Cars, Light Commercial Vehicles, and Heavy Commercial Vehicles. The Mid-Sized Passenger Cars segment dominated the market with a revenue share of 34.2% in 2025, owing to strong consumer demand and widespread OEM integration of aerodynamic components for fuel efficiency and style enhancement.

The Luxury Passenger Cars segment is anticipated to witness the fastest CAGR during 2026–2033, propelled by the increasing inclusion of active and electronically adjustable spoilers to enhance performance and aesthetics. Continuous innovation in adaptive aerodynamics and growing consumer preference for sporty, high-performance models are fueling market expansion within this segment globally.

- By Distribution Channel

On the basis of distribution channel, the rear spoiler market is segmented into OEM and Aftermarket. The OEM segment dominated the market with a revenue share of 58.1% in 2025, driven by the increasing integration of factory-fitted spoilers by automakers to meet regulatory fuel efficiency and safety standards. OEMs focus on offering aerodynamic enhancements as part of design differentiation and vehicle branding strategies.

The Aftermarket segment is projected to grow at the fastest CAGR from 2026 to 2033, supported by growing vehicle customization trends and replacement demand for performance upgrades. The surge in online retail platforms, coupled with the availability of lightweight, easy-to-install spoilers, continues to drive aftermarket growth across emerging and developed automotive markets.

- By Design

Based on design, the rear spoiler market is segmented into Strips and Free Standing Wing. The Free Standing Wing segment dominated the market with the largest share of 54.3% in 2025, owing to its superior aerodynamic performance and ability to enhance downforce and vehicle stability at high speeds. It is widely adopted in sports, luxury, and performance vehicles.

The Strips segment is anticipated to record the fastest CAGR from 2026 to 2033, attributed to the rising adoption in compact and mid-range passenger vehicles. These spoilers offer lightweight construction, cost-effectiveness, and ease of installation, making them ideal for OEM and aftermarket applications aimed at improving aesthetics and minor aerodynamic benefits.

- By System Type

On the basis of system type, the rear spoiler market is segmented into Passive Spoiler and Active Spoiler. The Passive Spoiler segment dominated the market with a revenue share of 68.6% in 2025, primarily due to its simplicity, lower manufacturing cost, and widespread use across compact and mid-sized vehicles. It provides consistent aerodynamic stability without requiring electronic control systems.

The Active Spoiler segment is expected to grow at the fastest CAGR during 2026–2033, driven by increasing adoption in luxury and electric vehicles. These systems automatically adjust angle and position based on driving conditions, improving fuel efficiency, safety, and high-speed control. Technological advancements in sensor integration and lightweight actuators are further expanding active spoiler applications across modern vehicle platforms.

Which Region Holds the Largest Share of the Rear Spoiler Market?

- Asia-Pacific dominated the rear spoiler market with the largest revenue share of 41.6% in 2025, attributed to the strong presence of major automotive manufacturers, rising vehicle production, and growing demand for aerodynamic components across China, Japan, South Korea, and India. Increasing consumer preference for sporty vehicle aesthetics and improved fuel efficiency has boosted spoiler installation in both OEM and aftermarket channels

- Automakers in the region are investing heavily in lightweight materials such as ABS plastic and carbon fiber to enhance performance and reduce emissions. The rise of electric vehicle manufacturing hubs and expanding automotive exports further strengthen regional dominance

- Favorable government policies promoting electric mobility, technological innovation, and sustainable automotive design continue to position Asia-Pacific as the global leader in the rear spoiler market

China Rear Spoiler Market Insight

China represents the largest contributor to the Asia-Pacific rear spoiler market, supported by its robust automotive production base and extensive EV ecosystem. Domestic manufacturers such as BYD Auto, Geely, and SAIC Motor are integrating aerodynamic designs to improve range and energy efficiency in electric models. Technological advancements in injection molding and lightweight carbon fiber materials are driving production efficiency. Growing investments in premium and mid-segment passenger vehicles, coupled with government incentives for low-emission cars, are reinforcing China’s leadership in both OEM and aftermarket spoiler segments.

India Rear Spoiler Market Insight

India is emerging as one of the fastest-growing markets in Asia-Pacific, driven by rising passenger car sales, expansion of local automotive manufacturing, and increasing consumer demand for sporty and fuel-efficient designs. Government initiatives such as “Make in India” and the Automotive Mission Plan 2026 are fostering domestic production of advanced automotive components. OEMs are integrating aerodynamic spoilers in compact and mid-sized cars to comply with emission norms and enhance visual appeal. Continuous investment in lightweight composite materials and growing aftermarket demand for customization are further propelling market growth.

North America Rear Spoiler Market Insight

North America is projected to witness the fastest growth rate of 9.7% during 2026–2033, fueled by high adoption of advanced aerodynamics in performance and electric vehicles. Strong automotive innovation in the U.S. and Canada, combined with rising demand for active spoilers in premium car models, supports regional expansion. The growing presence of electric vehicle manufacturers, alongside investments in sustainable lightweight materials, is reshaping the market landscape. Increasing consumer interest in customization and aftermarket accessories further boosts the demand for carbon fiber and ABS-based spoilers.

U.S. Rear Spoiler Market Insight

The U.S. dominates the North American rear spoiler market, driven by technological innovation, luxury vehicle demand, and the presence of leading automakers such as Ford Motor Company, General Motors, and Tesla Inc. Active and adaptive spoiler technologies are gaining traction in electric and high-performance vehicles to improve aerodynamics and range. Manufacturers are focusing on recyclable materials, smart actuators, and precision molding to comply with sustainability and performance standards. The growing popularity of sporty car models and EV adoption is expected to maintain the U.S. market’s upward trajectory.

Canada Rear Spoiler Market Insight

Canada contributes steadily to the North American rear spoiler market, supported by growing vehicle production, electric mobility adoption, and the rising popularity of aftermarket customization. Increasing consumer awareness of fuel efficiency and aesthetic enhancement drives spoiler installations in compact and mid-sized cars. The government’s initiatives to promote clean mobility and advanced manufacturing are encouraging local production of sustainable components. OEM collaborations with research institutions are further enhancing innovation in aerodynamic efficiency and lightweight materials within Canada’s automotive sector.

Europe Rear Spoiler Market Insight

Europe holds a significant share in the global rear spoiler market, driven by the presence of premium automakers such as BMW, Mercedes-Benz, Volkswagen, and Porsche. Demand for high-performance, lightweight spoilers integrated with smart actuation systems continues to rise across luxury and sports vehicles. Stringent EU emission standards and a strong focus on sustainability are accelerating the adoption of recyclable materials such as carbon fiber composites. The growing EV market, coupled with continuous innovation in active aerodynamics, is positioning Europe as a key hub for advanced spoiler technologies.

Germany Rear Spoiler Market Insight

Germany leads the European rear spoiler market, supported by its strong automotive manufacturing base and technological expertise in aerodynamics. OEMs are heavily investing in precision molding and carbon fiber integration to enhance performance and reduce drag. High R&D spending and advanced engineering facilities enable the production of spoilers tailored for premium and electric vehicles. The country’s emphasis on design innovation and environmental compliance further strengthens its role as a European leader in aerodynamic automotive components.

U.K. Rear Spoiler Market Insight

The U.K. market continues to expand, driven by the growth of electric vehicle manufacturing and rising demand for performance-oriented automotive designs. Domestic automakers and aftermarket suppliers are focusing on sustainable materials, 3D printing, and digital modeling to create lightweight spoiler solutions. The country’s commitment to zero-emission mobility and the surge in customized vehicle upgrades are fueling demand across both OEM and aftermarket segments. These developments are expected to sustain the U.K.’s growing influence within the European Rear Spoiler market.

Which are the Top Companies in Rear Spoiler Market?

The rear spoiler industry is primarily led by well-established companies, including:

- Magna International Inc. (Canada)

- Plastic Omnium (France)

- AUDI AG (Germany)

- Dr. Ing. h.c. F. Porsche AG (Germany)

- AISIN SEIKI Co., Ltd. (Japan)

- SMP Deutschland GmbH (Germany)

- POLYTEC HOLDING AG (Austria)

- Thai Rung Union Car Public Company Limited (Thailand)

- REHAU Incorporated (Germany)

- SRG Global (U.S.)

- ALBAR INDUSTRIES (U.S.)

- PU Tech Industry (Malaysia)

- INOAC CORPORATION (Japan)

- Mercedes-AMG GmbH (Germany)

- Changzhou Huawei Mold Co., Ltd. (China)

- DAR Spoilers (U.S.)

- Hamann GmbH (Germany)

- SEIBON CARBON (U.S.)

- Dawn Enterprises, Inc. (U.S.)

- BUGATTI AUTOMOBILES S.A.S. (France)

What are the Recent Developments in Global Rear Spoiler Market?

- In August 2024, Magna International unveiled an innovative lightweight rear spoiler made from advanced composite materials to enhance vehicle aerodynamics and minimize carbon emissions. The design specifically targets electric and hybrid vehicles, aligning with the industry’s growing sustainability goals. This development reinforces Magna’s commitment to improving fuel efficiency and reducing vehicle weight, strengthening its leadership in eco-friendly automotive components

- In June 2024, Plastic Omnium introduced a new generation of rear spoilers developed using recyclable and sustainable materials to support green manufacturing practices. The innovation focuses on minimizing plastic waste and meeting stringent environmental standards without compromising performance or design flexibility. This advancement highlights the company’s proactive approach to sustainability and its drive to deliver high-quality aerodynamic solutions for modern vehicles

- In January 2024, Plastic Omnium, through its PO-Rein joint venture, initiated the construction of a high-pressure hydrogen vessel mega-plant in Jiading, Shanghai. Scheduled for operation in 2026, the facility will produce up to 60,000 hydrogen storage systems annually for China’s commercial vehicle market. This strategic expansion marks a significant milestone in Plastic Omnium’s journey toward hydrogen mobility and sustainable transportation solutions

- In February 2023, Magna announced an investment exceeding $470 million to expand its operations across Ontario, Canada, including a new battery enclosures facility in Brampton. The expansion supports production for the Ford F-150 Lightning and future OEM programs, boosting Magna’s role in the electric vehicle supply chain. This move strengthens the company’s manufacturing capabilities and commitment to advancing EV technology in North America

- In October 2022, Valeo and SRG Global entered into a strategic alliance to deliver the next generation of exterior illuminated front panels for the automotive industry. The collaboration combines Valeo’s lighting expertise with SRG Global’s surface finishing capabilities to create advanced, aesthetic, and functional exterior systems. This partnership underscores both companies’ dedication to innovation and enhancing the visual and functional appeal of modern vehicles

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.