Global Recloser Controller Substation Automation Market

Market Size in USD Billion

USD

1.20 Billion

USD

2.37 Billion

2024

2032

USD

1.20 Billion

USD

2.37 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.20 Billion | |

| USD 2.37 Billion | |

| % | |

|

Recloser Controller Substation Automation Market Size

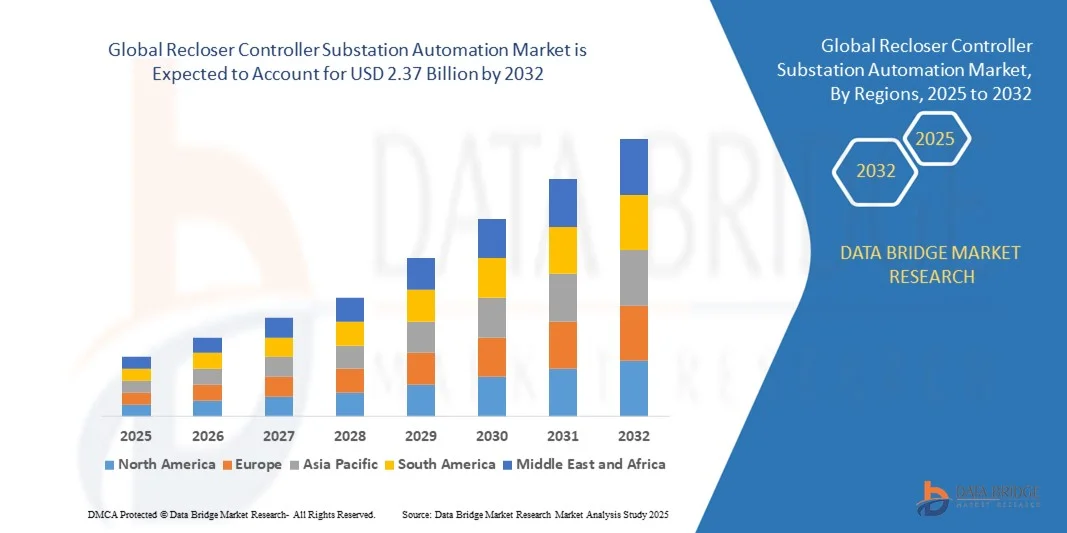

- The global recloser controller substation automation market size was valued at USD 1.20 billion in 2024 and is expected to reach USD 2.37 billion by 2032, at a CAGR of 8.90% during the forecast period

- The market growth is largely fuelled by the rising demand for reliable power distribution systems, increasing focus on grid modernization, and the growing integration of smart grid technologies

- The expansion of renewable energy generation and the need for efficient fault detection and isolation systems further support market development

Recloser Controller Substation Automation Market Analysis

- The recloser controller substation automation market is witnessing significant growth owing to the increasing deployment of intelligent electronic devices (IEDs) and digital substations across utilities and industrial sectors

- Growing emphasis on minimizing power outages and improving operational efficiency is accelerating the adoption of automated recloser controllers that enable quick fault response and grid restoration

- North America dominated the recloser controller substation automation market with the largest revenue share of 38.42% in 2024, driven by ongoing grid modernization initiatives, rapid adoption of digital substations, and increasing investments in smart grid infrastructure

- Asia-Pacific region is expected to witness the highest growth rate in the global recloser controller substation automation market, driven by large-scale infrastructure development, increasing renewable energy integration, and modernization of transmission and distribution networks across emerging economies such as China and India

- The SCADA segment held the largest market revenue share in 2024, driven by the growing demand for centralized monitoring and control systems in substations. SCADA systems provide enhanced visibility, real-time fault management, and remote operation capabilities, enabling utilities to improve grid stability and operational efficiency

Report Scope and Recloser Controller Substation Automation Market Segmentation

|

Attributes |

Recloser Controller Substation Automation Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Recloser Controller Substation Automation Market Trends

Integration Of Artificial Intelligence (AI) And Machine Learning (ML) For Predictive Grid Management

- The integration of AI and ML technologies is transforming the recloser controller substation automation landscape by enabling predictive maintenance, real-time fault detection, and intelligent decision-making. These technologies help utilities anticipate failures, optimize network reliability, and minimize outage durations, ensuring consistent power delivery across critical infrastructures. Moreover, AI-based controllers enhance grid visibility by processing massive data streams from sensors and IoT devices, facilitating faster response to grid disturbances

- The growing complexity of modern power grids and the shift toward digital substations are accelerating the adoption of intelligent recloser controllers with embedded analytics. Utilities are leveraging ML algorithms to analyze grid behavior, predict potential disruptions, and implement corrective measures automatically, reducing operational risks and maintenance costs. In addition, data-driven decision-making allows operators to prioritize system upgrades and plan maintenance schedules more efficiently

- The rising demand for self-healing grid systems is further boosting interest in AI-based automation, which enables faster fault isolation and system restoration. This contributes to improved grid efficiency, enhanced service continuity, and better resilience against external disturbances such as storms or equipment faults. AI-enhanced reclosers can dynamically reconfigure power distribution in real time, ensuring consistent energy supply even under fluctuating load conditions

- For instance, in 2023, several North American utility providers implemented AI-driven recloser controllers integrated with SCADA and IoT platforms, resulting in up to a 25% reduction in outage duration and improved network stability during high-demand periods. These implementations showcased how automation can significantly enhance energy delivery performance while reducing the dependency on manual fault intervention. The successful deployment of such systems is encouraging global utilities to accelerate AI adoption in substation operations

- While AI and ML are revolutionizing substation automation, their success relies on robust data infrastructure, cybersecurity frameworks, and skilled workforce availability. Manufacturers and utilities must collaborate to develop interoperable, secure, and scalable automation solutions that meet evolving energy sector requirements. Furthermore, investments in workforce training and policy frameworks will be essential to fully harness the potential of intelligent grid automation technologies

Recloser Controller Substation Automation Market Dynamics

Driver

Rising Demand For Reliable Power Supply And Grid Modernization

- The global push toward smart grid modernization is driving the demand for advanced recloser controller systems capable of providing automated fault management and rapid power restoration. Utilities are investing heavily in digital substations to enhance operational reliability and minimize power interruptions. The modernization initiatives also focus on incorporating renewable energy sources into the grid, requiring adaptive and intelligent recloser solutions

- Increasing electricity demand from industrial, commercial, and residential sectors is pressuring utilities to adopt intelligent recloser controllers that ensure network stability and efficient load management. These systems enable real-time monitoring and quick fault isolation, reducing downtime and improving service quality. As urbanization continues, the demand for uninterrupted power supply is further boosting investment in automation and fault-tolerant infrastructure

- Government initiatives promoting sustainable power infrastructure and resilience are further accelerating market growth. National grid modernization programs in regions such as North America, Europe, and Asia-Pacific are encouraging utilities to deploy recloser automation technologies at scale. Moreover, policy-driven funding and smart city programs are supporting utilities in adopting digital control systems that enhance reliability and energy efficiency

- For instance, in 2023, the U.S. Department of Energy launched initiatives to upgrade aging grid infrastructure with advanced recloser and feeder automation systems to enhance power reliability and grid flexibility. These programs aim to strengthen the resilience of the national grid and integrate renewable sources such as solar and wind power. Similar initiatives are being replicated in emerging economies focusing on digital transformation in the energy sector

- While growing demand for resilient and efficient power systems drives market expansion, sustained adoption will depend on cost optimization, interoperability, and integration with renewable energy management platforms. The transition to intelligent substations requires alignment of digital standards and continuous innovation in data communication technologies. Ensuring system compatibility and operational safety will remain central to large-scale modernization efforts

Restraint/Challenge

High Implementation Costs And Cybersecurity Vulnerabilities In Automated Systems

- The initial capital investment required for deploying recloser controllers and automation infrastructure poses a challenge for small and regional utility providers. The cost of smart sensors, communication modules, and control units increases total deployment expenses, limiting adoption in cost-sensitive markets. Moreover, the need for specialized installation expertise and maintenance training further adds to the overall financial burden

- Cybersecurity concerns associated with interconnected and automated substations are also a major challenge. As utilities adopt digital systems with IoT connectivity, the risk of unauthorized access, data breaches, and operational disruptions rises, necessitating continuous security monitoring and system updates. A single cyber incident can lead to significant financial losses and grid instability, making cybersecurity investments a critical priority

- The integration of new recloser automation systems with existing legacy grid setups often involves technical and compatibility issues, leading to extended installation timelines and higher operational risks during transition phases. Retrofitting older systems demands specialized engineering support and precise calibration to prevent system conflicts or downtime. This limits large-scale upgrades in regions with outdated electrical infrastructure

- For instance, in 2023, several utilities in Europe reported delays in substation automation projects due to high system integration costs and cybersecurity compliance requirements imposed by regulatory authorities. The need to ensure end-to-end encryption and data integrity increased the cost and complexity of these deployments. Such challenges highlight the necessity of standardized protocols and cross-vendor collaboration to streamline integration

- While automation offers long-term efficiency and reliability benefits, addressing cost barriers, standardizing protocols, and strengthening cybersecurity frameworks remain critical to ensure safe and cost-effective market expansion. Governments and private stakeholders must collaborate to provide funding assistance and policy support for digital infrastructure. Achieving a balance between innovation, affordability, and security will be vital for widespread adoption

Recloser Controller Substation Automation Market Scope

The global recloser controller substation automation market is segmented on the basis of module, communication, types, end-user, and stage.

- By Module

On the basis of module, the recloser controller substation automation market is segmented into IED, RTU, BCU, and SCADA. The SCADA segment held the largest market revenue share in 2024, driven by the growing demand for centralized monitoring and control systems in substations. SCADA systems provide enhanced visibility, real-time fault management, and remote operation capabilities, enabling utilities to improve grid stability and operational efficiency.

The IED segment is expected to witness the fastest growth rate from 2025 to 2032, driven by the rising deployment of intelligent electronic devices that facilitate automation, predictive maintenance, and fault detection. IEDs are increasingly used for smart grid applications, allowing seamless communication between control systems and field equipment while reducing response time and manual intervention.

- By Communication

On the basis of communication, the market is segmented into wire and wireless. The wire segment dominated the market in 2024, supported by its reliability, high data transmission rate, and lower latency in critical substation operations. Wired communication systems are preferred in high-voltage substations where stable connectivity and minimal interference are essential for safety and efficiency.

The wireless segment is expected to register the fastest growth from 2025 to 2032 due to the growing integration of IoT and cloud-based platforms in smart grids. Wireless communication offers flexibility, scalability, and cost-effectiveness in remote or hard-to-reach substations, enabling real-time data sharing and seamless automation across diverse grid environments.

- By Types

On the basis of types, the market is segmented into transmission and distribution. The distribution segment accounted for the largest market share in 2024, owing to the increasing focus on automation of medium- and low-voltage distribution networks to improve fault detection and power restoration. Distribution-level automation enhances operational efficiency and reduces downtime for end consumers.

The transmission segment is expected to grow at a notable rate from 2025 to 2032, fuelled by modernization initiatives in high-voltage transmission systems and the integration of renewable energy sources. The use of advanced recloser controllers in transmission substations supports grid resilience and stability under varying load conditions.

- By End-User

On the basis of end-user, the market is segmented into utility and industry. The utility segment held the dominant share in 2024, driven by rising investments in smart grid projects and the need to reduce outage durations. Utilities are increasingly adopting recloser controllers to ensure continuous power delivery and meet growing consumer expectations for reliability.

The industry segment is expected to grow at a notable rate from 2025 to 2032 due to the adoption of automation technologies in manufacturing plants and industrial facilities. Industries are deploying intelligent recloser controllers to ensure operational safety, prevent downtime, and optimize energy usage across production lines.

- By Stage

On the basis of stage, the market is segmented into retrofit and new. The retrofit segment captured the largest revenue share in 2024, as utilities focus on upgrading existing grid infrastructure with intelligent automation technologies. Retrofitting existing substations with recloser controllers enhances reliability, extends asset lifespan, and supports digital transformation initiatives.

The new segment is anticipated to witness the fastest growth from 2025 to 2032, driven by the rapid expansion of transmission and distribution networks, especially in emerging economies. New substation projects are increasingly designed with automation and smart recloser systems from inception, ensuring higher operational efficiency and future-ready grid performance.

Recloser Controller Substation Automation Market Regional Analysis

- North America dominated the recloser controller substation automation market with the largest revenue share of 38.42% in 2024, driven by ongoing grid modernization initiatives, rapid adoption of digital substations, and increasing investments in smart grid infrastructure

- The region’s utilities are focusing on enhancing operational efficiency and reducing outage times through advanced recloser controllers integrated with IoT, AI, and SCADA systems

- High technological maturity, government funding for renewable integration, and the growing emphasis on automation and resilience are further supporting market expansion across both urban and rural distribution networks

U.S. Recloser Controller Substation Automation Market Insight

The U.S. recloser controller substation automation market captured the largest revenue share in 2024 within North America, supported by the country’s accelerated investments in modernizing its aging power infrastructure. Rising electricity demand and increased emphasis on grid reliability have prompted utilities to deploy intelligent recloser controllers capable of automated fault detection and isolation. Moreover, federal initiatives such as the Grid Modernization Initiative are encouraging digital automation adoption, improving real-time monitoring and operational flexibility across substations.

Europe Recloser Controller Substation Automation Market Insight

The Europe recloser controller substation automation market is expected to witness the fastest growth rate from 2025 to 2032, fuelled by stringent regulatory standards on energy reliability and the transition toward smart energy networks. European utilities are investing in recloser controllers that support data analytics, remote operation, and advanced fault management. The region’s focus on decarbonization and integration of renewable sources such as wind and solar is creating strong demand for automation systems that enhance grid stability and flexibility.

U.K. Recloser Controller Substation Automation Market Insight

The U.K. recloser controller substation automation market is expected to witness the fastest growth rate from 2025 to 2032, driven by the nation’s push for digital grid modernization and renewable integration. The adoption of intelligent controllers capable of managing distributed generation and real-time load balancing is on the rise. Furthermore, government efforts toward developing self-healing and resilient power grids are supporting the deployment of automated systems, ensuring reliability across critical infrastructure and reducing power disruption frequency.

Germany Recloser Controller Substation Automation Market Insight

The Germany recloser controller substation automation market is expected to witness the fastest growth rate from 2025 to 2032, driven by the country’s strong commitment to energy transition (Energiewende) and sustainable grid innovation. German utilities are increasingly investing in advanced automation technologies to manage complex grid operations and integrate renewable power sources efficiently. The emphasis on cybersecurity, interoperability, and predictive maintenance solutions further supports the widespread deployment of intelligent recloser controllers across the transmission and distribution networks.

Asia-Pacific Recloser Controller Substation Automation Market Insight

The Asia-Pacific recloser controller substation automation market is expected to witness the fastest growth rate from 2025 to 2032, supported by rising electricity demand, rapid urbanization, and substantial investments in smart grid development in countries such as China, Japan, and India. Expanding industrialization and government-backed initiatives for digital infrastructure modernization are driving adoption. The region’s increasing focus on reducing power losses, improving fault recovery, and ensuring reliable distribution networks further strengthens market growth potential.

Japan Recloser Controller Substation Automation Market Insight

The Japan recloser controller substation automation market is expected to witness the fastest growth rate from 2025 to 2032, propelled by technological innovation, energy efficiency goals, and the need for resilient power systems. Japan’s utilities are emphasizing the deployment of AI- and IoT-enabled recloser controllers to improve fault diagnostics, predictive maintenance, and operational automation. In addition, the country’s efforts to integrate renewable energy sources into its distribution networks are boosting demand for intelligent and adaptive substation automation solutions.

China Recloser Controller Substation Automation Market Insight

The China recloser controller substation automation market accounted for the largest market revenue share in Asia-Pacific in 2024, supported by extensive government investments in grid modernization and the ongoing expansion of renewable energy projects. As part of its Smart Grid and New Infrastructure initiatives, China is rapidly adopting intelligent recloser controllers for improved fault response and network reliability. The presence of leading domestic manufacturers, coupled with the expansion of rural electrification programs, continues to accelerate the market’s development across transmission and distribution segments.

Recloser Controller Substation Automation Market Share

The Recloser Controller Substation Automation industry is primarily led by well-established companies, including:

• Crompton Greaves Consumer Electricals Limited (India)

• Schweitzer Engineering Laboratories, Inc. (U.S.)

• Honeywell International Inc. (U.S.)

• NovaTech, LLC (U.S.)

• ADI Engineering, Inc. (U.S.)

• Advanced Control Systems, Inc. (U.S.)

• Advantech Co., Ltd. (Taiwan)

• AMETEK Power Instruments (U.S.)

• Eaton (Ireland)

• Schneider Electric (France)

• General Electric (U.S.)

• Siemens (Germany)

• ABB (Switzerland)

• Trilliant Holdings Inc. (U.S.)

• GRIDNET (U.S.)

• Larsen & Toubro Limited (India)

• Power System Engineering, Inc. (U.S.)

• JSC Yamal LNG (Russia)

• CGGlobal (India)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.