Global Reconstructive Surgery Market

Market Size in USD Billion

USD

52.99 Billion

USD

70.31 Billion

2025

2033

USD

52.99 Billion

USD

70.31 Billion

2025

2033

| 2026 - 2033 | |

| USD 52.99 Billion | |

| USD 70.31 Billion | |

| % | |

|

Reconstructive Surgery Market Overview

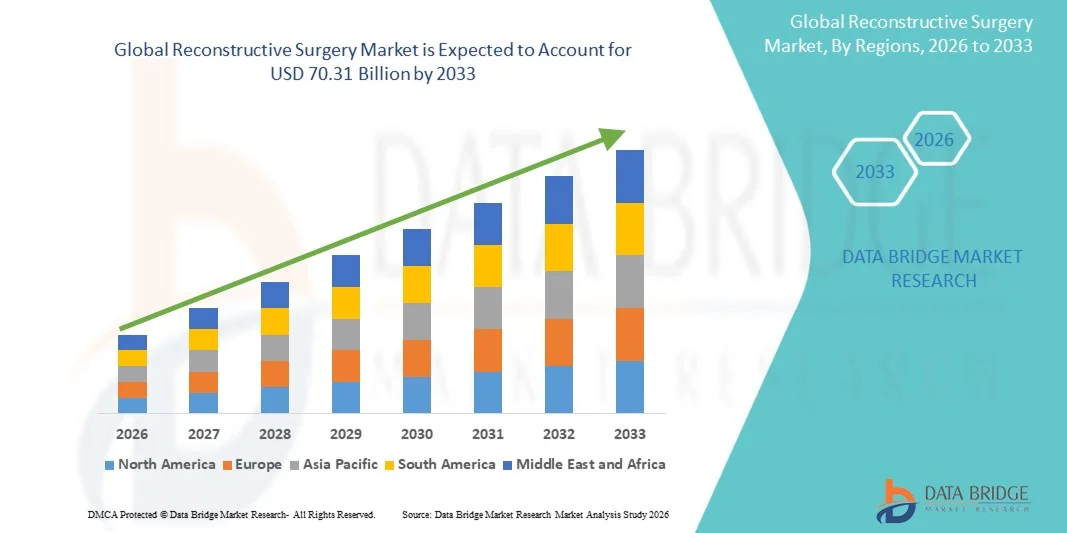

The Reconstructive Surgery Market was valued at USD 52.99 billion in 2025 and is projected to reach USD 70.31 billion by 2033, growing at a CAGR of 3.60% from 2026 to 2033. The market is experiencing steady growth driven by the rising prevalence of traumatic injuries, congenital deformities, cancer-related defects, and increasing demand for functional and aesthetic restoration procedures across healthcare systems worldwide.

The growing incidence of road accidents, burns, sports injuries, and post-oncologic reconstruction needs, particularly following breast cancer and head-and-neck cancer surgeries, is accelerating the adoption of advanced reconstructive procedures. Continuous advancements in microsurgery techniques, 3D surgical planning, tissue engineering, biocompatible implants, and regenerative medicine are enhancing surgical outcomes and expanding treatment options. In addition, increasing healthcare expenditure, improved access to specialized surgical care, and greater awareness of reconstructive interventions are encouraging hospitals, specialty clinics, and academic medical centers to invest in innovative reconstructive surgery solutions for improved patient recovery and quality of life.

Key Market Trends & Insights

- North America dominated the Reconstructive Surgery Market with the largest revenue share of 38.6% in 2025, supported by advanced healthcare infrastructure, high procedure volumes, and strong presence of specialized plastic and reconstructive surgeons.

- The Breast Reconstruction segment led the market with a 34.2% share in 2025, driven by the rising incidence of breast cancer and increasing adoption of post-mastectomy reconstructive procedures.

- Asia-Pacific is expected to be the fastest-growing region from 2026 to 2033, expanding at a CAGR of 7.9%, fueled by expanding healthcare access, rising medical tourism, increasing trauma cases, and improving surgical infrastructure in countries such as India, China, and South Korea.

- Skin Cancer are the fastest-growing indication type, projected to register a CAGR of 7.6%, reflecting the surge in the rising global incidence of melanoma and non-melanoma skin cancers.

- The Implants segment dominated the prosthetic implant category with a 46.8% revenue share in 2025, led by widespread use in breast, craniofacial, and orthopedic reconstructive procedures.

- Hospitals accounted for 55.1% of the market, preferred by the availability of advanced surgical infrastructure, multidisciplinary teams, and emergency trauma care facilities.

- The Stents segment is the fastest-growing prosthetic implant category, with a CAGR of 7.2%, driven by the increasing use in reconstructive procedures involving airway, vascular, and gastrointestinal reconstruction.

Market Size & Forecast

- Global Market Value (2025): USD 52.99 Billion

- Expected Market Value (2033): USD 70.31 Billion

- Forecast CAGR (2026–2033): 3.60%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Reconstructive Surgery Market Segmentation

|

Attributes |

Reconstructive Surgery Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Stryker (U.S.) · Johnson & Johnson Services, Inc. (U.S.) · Zimmer Biomet (U.S.) · Medtronic (Ireland) · Smith+Nephew (U.K.) · B. Braun SE (Germany) · Integra LifeSciences Holdings Corporation (U.S.) · Axogen, Inc. (U.S.) · RTI Surgical Holdings, Inc. (U.S.) · KLS Martin Group (Germany) · POLYTECH Health & Aesthetics GmbH (Germany) · GC Aesthetics plc (Ireland) · LivaNova PLC (U.K.) · Abbott (U.S.) · Alcon Inc. (Switzerland) · OsteoMed (U.S.) · Meril Life Sciences Pvt. Ltd. (India) · Tissue Regenix Group plc (U.K.) · Anika Therapeutics, Inc. (U.S.) · Establishment Labs Holdings Inc. (Luxembourg) |

|

Market Opportunities |

· Rising demand for post-trauma and accident reconstruction procedures · Expanding adoption of 3D printing and patient-specific implants · Growing integration of regenerative medicine, stem cell therapy, and bioengineered tissues |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Reconstructive Surgery Market Trends

Trend: Expansion of Advanced Microsurgery and Tissue Engineering Applications

Surgeons are increasingly adopting advanced microsurgical techniques, bioengineered grafts, and tissue engineering solutions to improve functional and aesthetic outcomes in complex reconstructive procedures across trauma, oncology, and congenital defect cases. The integration of 3D surgical planning and digital imaging enables precise preoperative mapping and improved flap survival rates. Hospitals and specialized centers are increasingly using regenerative scaffolds and biologically active materials to enhance healing efficiency, while robotic-assisted reconstruction is improving surgical accuracy and reducing complications in delicate procedures. For instance, recent use of 3D-printed bone scaffolds in craniofacial reconstruction surgeries demonstrates growing clinical adoption of personalized regenerative solutions.

Reconstructive Surgery Market Dynamics

Key Market Driver: Rising Burden of Trauma, Cancer Surgeries, and Congenital Deformities

The increasing global incidence of road accidents, burn injuries, cancer resections, and congenital abnormalities is significantly driving demand for reconstructive surgical procedures across healthcare systems. Growing breast and head-and-neck cancer cases are creating substantial post-surgical reconstruction requirements, while trauma cases from occupational and sports injuries are further expanding procedural volumes. Improved healthcare access and rising awareness of reconstructive options are also encouraging patients to opt for restorative surgeries that enhance both functionality and appearance. For instance, rising post-mastectomy breast reconstruction rates following cancer treatment highlight the growing clinical dependency on reconstructive procedures.

Key Restraint/Challenge: High Surgical Cost and Limited Access to Specialized Expertise

A major restraint in the reconstructive surgery market is the high cost of advanced surgical procedures, including microsurgery, implant-based reconstruction, and regenerative therapies, which limits accessibility in low- and middle-income regions. The requirement for highly trained reconstructive surgeons, specialized operating facilities, and long postoperative care further increases overall treatment expenses. In addition, uneven distribution of skilled professionals creates accessibility gaps in rural and underserved healthcare systems. For instance, complex microsurgical flap reconstruction procedures in trauma cases often remain restricted to tertiary care centers due to the need for highly specialized surgical expertise and infrastructure.

Key Market Opportunity: Growth in Regenerative Medicine and Patient-Specific Reconstruction Technologies

The increasing adoption of regenerative medicine, stem cell therapies, and patient-specific 3D-printed implants presents a significant opportunity for market expansion in reconstructive surgery. These innovations enable customized anatomical reconstruction, faster healing, and improved long-term functional outcomes compared to traditional methods. Advancements in biocompatible materials and digital surgical planning are further enhancing procedural precision and personalization across multiple indications. For instance, the use of patient-specific 3D-printed titanium implants in cranial defect reconstruction highlights the growing shift toward highly customized reconstructive solutions.

Reconstructive Surgery Market Scope

The reconstructive surgery market is segmented on the basis of indication, prosthetic implant, and end-user.

- By Indication

On the basis of indication, the Reconstructive Surgery Market is segmented into congenital anomalies, orthognathic surgeries, breast reconstruction, skin cancer, tissue expansion, hand surgery, lymphedema treatment, septoplasty, and others. The Breast Reconstruction segment dominated the market with a 34.2% share in 2025, driven by the rising incidence of breast cancer and increasing adoption of post-mastectomy reconstructive procedures. Growing awareness of aesthetic restoration and psychological recovery after cancer treatment is significantly contributing to demand. Advances in implant-based reconstruction and autologous tissue techniques are improving surgical outcomes and patient satisfaction. Expanding availability of specialized breast reconstruction surgeons and improved insurance coverage in developed regions further supports growth. Increasing use of combination procedures involving implants and fat grafting is also enhancing clinical adoption.

The Skin Cancer reconstruction segment is expected to witness the fastest growth at a CAGR of 7.6% from 2026 to 2033, driven by the rising global incidence of melanoma and non-melanoma skin cancers. Increasing exposure to UV radiation and aging populations are key contributing factors. Surgical excision of skin cancers often requires complex reconstructive procedures for functional and cosmetic restoration. Advances in local flap techniques, skin grafting, and bioengineered skin substitutes are improving treatment outcomes. Rising dermatology awareness programs and early diagnosis rates are further increasing reconstruction demand. Expanding outpatient surgical capabilities is also accelerating segment growth.

- By Prosthetic Implant

On the basis of prosthetic implant, the Reconstructive Surgery Market is segmented into tubes, rings, stents, implants, and others. The Implants segment dominated the market with a 46.8% share in 2025, primarily due to widespread use in breast, craniofacial, and orthopedic reconstructive procedures. These implants provide long-term structural support and improved aesthetic outcomes in complex surgeries. Continuous innovation in biocompatible materials such as silicone, titanium, and polymer-based implants is enhancing safety and durability. Surgeons increasingly prefer customized implant solutions enabled by 3D printing technologies. Strong demand from trauma reconstruction and post-cancer surgeries is further driving adoption. Growing reimbursement support in developed healthcare systems is also strengthening this segment’s dominance.

The Stents segment is expected to witness the fastest growth at a CAGR of 7.2% from 2026 to 2033, driven by increasing use in reconstructive procedures involving airway, vascular, and gastrointestinal reconstruction. Minimally invasive techniques are expanding the clinical use of stents in complex anatomical repairs. Technological advancements in biodegradable and drug-eluting stents are improving patient outcomes and reducing complications. Rising incidence of reconstructive surgeries following trauma and cancer treatment is further supporting demand. Growing preference for less invasive and faster recovery procedures is accelerating adoption. Expanding interventional radiology applications are also contributing to segment growth.

- By End-User

On the basis of end-user, the Reconstructive Surgery Market is segmented into ambulatory surgical units, hospitals, clinics, and others. The Hospitals segment dominated the market with a 55.1% share in 2025, due to the availability of advanced surgical infrastructure, multidisciplinary teams, and emergency trauma care facilities. Hospitals are the primary centers for complex reconstructive procedures requiring microsurgery and long postoperative care. High patient inflow for cancer surgeries, trauma cases, and congenital defect corrections further strengthens demand. Availability of advanced imaging, robotic-assisted surgery, and intensive care units supports superior clinical outcomes. Strong presence of specialized plastic and reconstructive surgeons also contributes to dominance. Favorable reimbursement structures in many countries enhance hospital-based adoption.

The Ambulatory Surgical Units segment is expected to witness the fastest growth at a CAGR of 8.1% from 2026 to 2033, driven by increasing preference for minimally invasive and outpatient reconstructive procedures. Advancements in surgical techniques are enabling shorter recovery times and same-day discharge for select procedures. Cost-effectiveness compared to hospital stays is encouraging patient adoption. Growing availability of specialized day-care surgical centers is expanding access to reconstructive treatments. Rising demand for cosmetic and minor reconstructive interventions is further supporting growth. Technological improvements in anesthesia and surgical precision are also accelerating the shift toward ambulatory care settings.

Reconstructive Surgery Market Regional Analysis

North America dominated the Reconstructive Surgery Market with the largest revenue share of 38.6% in 2025, supported by advanced healthcare infrastructure, high procedure volumes, and strong presence of specialized plastic and reconstructive surgeons. The region also benefits from well-established reimbursement systems, increasing prevalence of cancer-related and trauma-related reconstruction cases, and widespread adoption of advanced surgical technologies such as microsurgery and 3D-printed implants. Growing demand for breast reconstruction procedures and rising awareness of post-surgical quality-of-life improvements continue to strengthen North America’s leadership position in the global market.

U.S. Reconstructive Surgery Market Insight

The U.S. reconstructive surgery market is witnessing strong growth due to high prevalence of cancer-related surgeries, trauma cases, and congenital deformities, along with advanced healthcare infrastructure and strong reimbursement coverage. The country’s mature plastic and reconstructive surgery ecosystem, along with increasing adoption of microsurgery, 3D-printed implants, and regenerative medicine, is driving demand across hospitals, specialty clinics, and ambulatory surgical centers. In addition, growing emphasis on post-mastectomy breast reconstruction and improved patient awareness regarding functional and aesthetic recovery is accelerating procedure volumes across the nation.

Europe Reconstructive Surgery Market Insight

The Europe reconstructive surgery market remains a major contributor to global revenue, driven by strong public healthcare systems, rising cancer incidence, and high adoption of advanced surgical techniques. The widespread use of reconstructive procedures in oncology, trauma care, and congenital anomaly correction is supporting market expansion across the region. Increasing investments in surgical innovation, combined with strict healthcare quality standards and skilled surgical workforce availability, continue to enhance adoption of reconstructive procedures throughout Europe.

U.K. Reconstructive Surgery Market Insight

The U.K. reconstructive surgery market is experiencing steady growth, supported by rising demand for breast reconstruction, trauma repair, and skin cancer-related procedures. Increasing investments in NHS surgical capacity and growing adoption of minimally invasive and microsurgical techniques are contributing to market expansion. Furthermore, integration of digital surgical planning tools and improved access to specialized reconstructive care are enhancing surgical outcomes, positioning the U.K. as an important hub for advanced reconstructive procedures.

Germany Reconstructive Surgery Market Insight

The Germany reconstructive surgery market is expanding steadily due to its strong hospital infrastructure, advanced surgical capabilities, and high adoption of innovative medical technologies. Hospitals and specialized centers are increasingly utilizing reconstructive procedures for cancer recovery, trauma management, and orthopedic reconstruction. Continuous advancements in biomaterials, implant technologies, and microsurgical techniques, along with strong focus on clinical precision and patient safety, are further driving market growth in Germany.

Asia-Pacific Reconstructive Surgery Market Insight

The Asia-Pacific reconstructive surgery market is expected to witness rapid growth, driven by increasing healthcare access, rising trauma cases, and growing prevalence of cancer across countries such as China, India, and Japan. Expanding medical tourism, improving hospital infrastructure, and increasing adoption of advanced surgical technologies are supporting regional market expansion. In addition, rising awareness regarding post-surgical quality of life and increasing availability of skilled reconstructive surgeons are accelerating procedure adoption across both public and private healthcare systems.

Japan Reconstructive Surgery Market Insight

The Japan reconstructive surgery market is witnessing consistent growth due to strong healthcare infrastructure, high technological adoption, and increasing focus on advanced surgical precision. Hospitals and research institutions are increasingly using microsurgery, regenerative medicine, and 3D surgical planning for complex reconstructive procedures. Moreover, growing aging population and rising demand for post-cancer reconstruction treatments are further contributing to market growth in the country.

China Reconstructive Surgery Market Insight

The China reconstructive surgery market is growing rapidly, driven by increasing healthcare investments, rising trauma cases, and growing prevalence of cancer requiring reconstructive interventions. Expanding hospital infrastructure, rising medical tourism, and increasing adoption of advanced surgical technologies such as 3D-printed implants and tissue engineering are significantly boosting market demand. In addition, growing awareness of post-surgical reconstruction benefits and rapid expansion of specialized surgical centers are positioning China as one of the fastest-growing markets globally.

Reconstructive Surgery Market Share

The reconstructive surgery industry is primarily led by well-established companies, including:

- Stryker (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Zimmer Biomet (U.S.)

- Medtronic (Ireland)

- Smith+Nephew (U.K.)

- Braun SE (Germany)

- Integra LifeSciences Holdings Corporation (U.S.)

- Axogen, Inc. (U.S.)

- RTI Surgical Holdings, Inc. (U.S.)

- KLS Martin Group (Germany)

- POLYTECH Health & Aesthetics GmbH (Germany)

- GC Aesthetics plc (Ireland)

- LivaNova PLC (U.K.)

- Abbott (U.S.)

- Alcon Inc. (Switzerland)

- OsteoMed (U.S.)

- Meril Life Sciences Pvt. Ltd. (India)

- Tissue Regenix Group plc (U.K.)

- Anika Therapeutics, Inc. (U.S.)

- Establishment Labs Holdings Inc. (Luxembourg)

Latest Developments in Reconstructive Surgery Market

- In December 2025, the U.S. Food and Drug Administration (FDA) approved Axogen’s AVANCE® Nerve Graft as a biologic for peripheral nerve reconstruction, marking a major advancement in nerve repair and reconstructive microsurgery. The approval expands treatment options for sensory, motor, and mixed nerve injuries, eliminating the need for autografts and improving functional recovery outcomes. This milestone strengthens regenerative approaches in reconstructive surgery and supports broader clinical adoption in trauma and microsurgical procedures

- In September 2024, Axogen completed the Biologics License Application (BLA) submission for its Avance Nerve Graft to the U.S. FDA, marking a key regulatory step toward full biologic classification. The submission supports expanded clinical use of nerve repair grafts in reconstructive surgery and reflects growing momentum in regenerative nerve reconstruction technologies

- In April 2024, Axogen announced the first surgical implantation of its Avive+ Soft Tissue Matrix, a resorbable allograft designed to protect and support nerve healing during reconstructive procedures. The product is used in complex nerve trauma cases to improve healing efficiency and reduce postoperative complications. This launch reflects increasing adoption of bioresorbable materials in reconstructive microsurgery applications

- In November 2023, RTI Surgical received FDA Investigational Device Exemption (IDE) approval for its Cortiva® Allograft Dermis used in implant-based breast reconstruction. The clinical study aims to evaluate safety and effectiveness in post-mastectomy reconstruction procedures. This development highlights growing innovation in biologic dermal matrices and reinforces the shift toward improved implant-based reconstructive outcomes

- In May 2021, Johnson & Johnson MedTech continued expanding its reconstructive surgery ecosystem through advancements in surgical sutures, energy devices, and implant technologies used in plastic and reconstructive procedures. These innovations support improved surgical precision, reduced complications, and enhanced outcomes in trauma, oncology, and aesthetic reconstruction surgeries globally

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.