Global Rectangular Dra Market

Market Size in USD Billion

USD

12.74 Billion

USD

39.24 Billion

2024

2032

USD

12.74 Billion

USD

39.24 Billion

2024

2032

Forecast Period |

2025 - 2032 |

Market Size (Base Year) |

USD 12.74 Billion |

Market Size (Forecast Year) |

USD 39.24 Billion |

CAGR |

% |

Major Markets Players |

|

Rectangular DRA Market Size

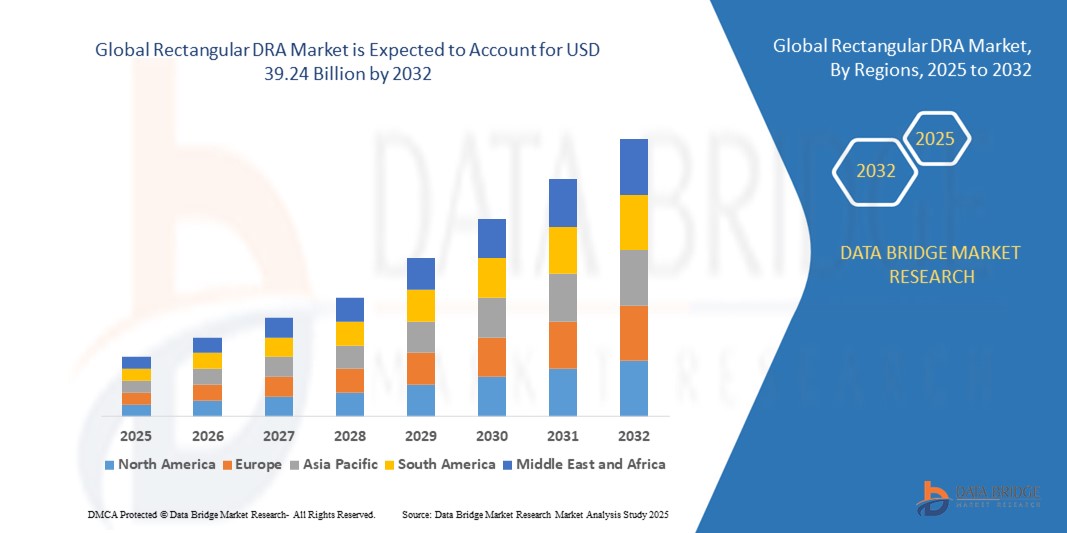

- The global rectangular DRA market size was valued at USD 12.74 billion in 2024 and is expected to reach USD 39.24 billion by 2032, at a CAGR of 15.10% during the forecast period

- The market growth is largely fuelled by increasing demand for energy-efficient solutions in water treatment and wastewater management

- Rising adoption of advanced DRA technologies across municipal and industrial sectors is driving growth

Rectangular DRA Market Analysis

- Rapid innovation in materials, design, and automation of rectangular DRA systems is improving efficiency, durability, and operational reliability

- Increasing investment in large-scale water treatment projects and wastewater recycling programs is creating substantial market opportunities

- North America dominated the rectangular DRA market with the largest revenue share of 38.50% in 2024, driven by increasing focus on energy-efficient pipeline operations, advanced fluid transport systems, and heightened awareness of cost optimization through drag reduction technologies

- Asia-Pacific region is expected to witness the highest growth rate in the global rectangular DRA market, driven by increasing urbanization, rising energy demand, and adoption of advanced pipeline technologies in countries such as China, Japan, and South Korea. The region’s expanding industrial and municipal water networks also support rapid market growth

- The Civilian segment held the largest market revenue share in 2024, driven by its widespread adoption in municipal water distribution, oil & gas pipelines, and chemical transport systems. Civilian operators favor rectangular DRA systems due to their efficiency in reducing energy consumption, improving pipeline throughput, and minimizing operational costs across various industries

Report Scope and Rectangular DRA Market Segmentation

|

Attributes |

Rectangular DRA Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Rectangular DRA Market Trends

Rising Adoption of Rectangular DRA in Industrial and Municipal Applications

• The growing adoption of rectangular DRA systems is transforming fluid flow management in pipelines by reducing frictional losses and improving flow efficiency. Their streamlined design and durability allow for enhanced operational performance, particularly in large-scale water distribution and oil & gas pipelines, resulting in energy savings and lower operational costs

• Increasing demand for energy-efficient and sustainable pipeline solutions is driving the adoption of rectangular DRA products across industrial, municipal, and utility sectors. These systems are particularly effective in regions with aging pipeline infrastructure, helping optimize flow rates and reduce pumping energy requirements

• The ease of installation and low maintenance requirements of modern rectangular DRA systems are making them attractive for both retrofit and new pipeline projects, supporting long-term operational reliability. Operators benefit from improved flow consistency, reduced wear on pumps, and lower energy expenditures

• For instance, in 2023, several municipal water authorities in Southeast Asia reported a 12% reduction in pumping energy consumption after implementing rectangular DRA systems in key pipeline networks. The improved hydraulic efficiency also reduced operational downtime and maintenance frequency

• While rectangular DRA adoption is accelerating operational efficiency, the impact depends on continued innovation, material improvements, and proper system design. Manufacturers must focus on customization and localized deployment strategies to fully capitalize on growing market demand

Rectangular DRA Market Dynamics

Driver

Increasing Focus on Energy Efficiency and Sustainable Pipeline Operations

• The rising emphasis on energy efficiency and carbon reduction is encouraging pipeline operators to adopt rectangular DRA solutions as a cost-effective means to optimize flow and reduce pumping energy. This trend is particularly strong in water, oil & gas, and chemical pipeline systems, where energy costs constitute a significant portion of operational expenditure

• Operators are increasingly aware of the financial and environmental benefits of DRA systems, including reduced operational costs, lower energy consumption, and extended pipeline life. This awareness has led to greater adoption across small, medium, and large-scale pipeline projects. In addition, improved pipeline efficiency through DRA implementation reduces wear and tear on pumps and valves, minimizing maintenance frequency and associated downtime

• Government incentives and environmental regulations are driving investments in energy-saving solutions, further accelerating market growth. From subsidized efficiency programs to mandates on reducing energy usage, supportive frameworks are promoting DRA adoption globally. Such policies also encourage private-public collaborations and infrastructure upgrades, creating a favorable environment for deploying advanced DRA technologies

• For instance, in 2022, U.S. municipal authorities implemented energy optimization programs that included rectangular DRA retrofits, boosting demand and adoption across several water distribution networks. Similar initiatives in Europe and Asia have also spurred investments in energy-efficient pipeline solutions, contributing to global market expansion

• While energy efficiency initiatives are driving the market, proper design, installation, and maintenance remain critical to achieving maximum operational benefits, emphasizing the need for skilled personnel and reliable technology. Continued R&D in DRA materials and configurations is further enhancing performance, enabling operators to optimize flow under varying pipeline conditions

Restraint/Challenge

High Initial Costs and Limited Technical Expertise in Emerging Regions

• The high upfront cost of advanced rectangular DRA systems limits accessibility for smaller pipeline operators and underfunded municipal projects. Significant investment in design, installation, and monitoring is often required, acting as a barrier to market penetration. These costs are especially challenging in developing regions, where budget constraints hinder widespread adoption despite potential long-term savings

• Many regions lack trained personnel capable of designing, installing, or maintaining DRA systems, which hinders adoption. The absence of technical expertise and supporting infrastructure reduces deployment in remote or emerging markets. In addition, insufficient training programs and limited technical support networks make it difficult for operators to optimize DRA performance or troubleshoot operational issues effectively

• Supply chain challenges and inconsistent material availability further constrain growth in certain regions. Pipeline operators often face delays in procurement and installation, leading to underutilization of DRA technology and suboptimal energy savings. Logistics disruptions and dependency on specialized suppliers can further exacerbate deployment challenges, slowing market expansion

• For instance, in 2023, several African water authorities reported limited adoption of rectangular DRA systems due to high costs and insufficient trained engineers to oversee installation and maintenance. Similar challenges were observed in parts of Southeast Asia, where limited infrastructure and technical knowledge delayed large-scale DRA implementation

• While technological improvements are enhancing durability and efficiency, addressing cost, technical expertise, and supply chain challenges remains crucial for unlocking the full potential of the global rectangular DRA market. Continued investments in training programs, modular designs, and localized production can help overcome these barriers and accelerate adoption in emerging regions

Rectangular DRA Market Scope

The market is segmented on the basis of application, technology, and frequency range.

- By Application

On the basis of application, the rectangular DRA market is segmented into Civilian and Military. The Civilian segment held the largest market revenue share in 2024, driven by its widespread adoption in municipal water distribution, oil & gas pipelines, and chemical transport systems. Civilian operators favor rectangular DRA systems due to their efficiency in reducing energy consumption, improving pipeline throughput, and minimizing operational costs across various industries.

The Military segment is expected to witness the fastest growth rate from 2025 to 2032, owing to the increasing need for advanced flow optimization and energy-efficient solutions in defense-related fluid transport and logistical operations. Military applications often demand robust, reliable, and high-performance DRA systems capable of functioning under extreme conditions, boosting market growth.

- By Technology

On the basis of technology, the market is segmented into MIMO (Multi Input Multi Output), SIMO (Single Input Multi Output), MISO (Multi Input Single Output), and SISO (Single Input Single Output). The MIMO segment held the largest revenue share in 2024, attributed to its superior performance in enhancing flow efficiency, reducing energy losses, and accommodating complex pipeline networks. MIMO-based DRAs are preferred for large-scale pipelines due to their adaptability and enhanced operational control.

The SISO segment is expected to witness the fastest growth rate from 2025 to 2032, driven by its simpler configuration, cost-effectiveness, and ease of deployment in smaller or localized pipeline systems. SISO solutions are increasingly adopted where quick installation and lower maintenance requirements are prioritized.

- By Frequency Range

On the basis of frequency range, the rectangular DRA market is segmented into Ultra-High Frequency, Super High Frequency, and Extremely High Frequency. The Ultra-High Frequency segment held the largest market revenue share in 2024, fueled by its ability to efficiently optimize flow in long-distance pipelines while reducing energy consumption. Ultra-High Frequency DRAs are favored for their high performance, stability, and suitability across diverse pipeline types.

The Extremely High Frequency segment is expected to witness the fastest growth rate from 2025 to 2032, driven by advancements in material science and technology that allow more precise energy transfer, improved drag reduction, and enhanced pipeline throughput. This segment is gaining traction in specialized industrial and defense applications.

Rectangular DRA Market Regional Analysis

• North America dominated the rectangular DRA market with the largest revenue share of 38.50% in 2024, driven by increasing focus on energy-efficient pipeline operations, advanced fluid transport systems, and heightened awareness of cost optimization through drag reduction technologies.

• Operators in the region highly value the energy savings, reduced operational costs, and improved pipeline performance offered by rectangular DRA systems.

• This widespread adoption is further supported by stringent regulations on energy efficiency, advanced infrastructure, and the presence of major pipeline operators, establishing rectangular DRA systems as a preferred solution across water, oil & gas, and chemical pipelines.

U.S. Rectangular DRA Market Insight

The U.S. rectangular DRA market captured the largest revenue share in 2024 within North America, fueled by the growing adoption of energy-saving solutions and modernization of pipeline networks. Pipeline operators are increasingly focusing on reducing pumping energy, optimizing flow, and extending pipeline lifespan. Government incentives, efficiency programs, and environmental regulations promoting reduced energy consumption further propel the market. Moreover, the integration of advanced drag reduction solutions into municipal water and industrial pipeline projects is significantly contributing to market expansion.

Europe Rectangular DRA Market Insight

The Europe rectangular DRA market is expected to witness the fastest growth rate from 2025 to 2032, primarily driven by regulatory mandates on energy efficiency, carbon reduction, and sustainable pipeline operations. Increasing investments in oil & gas, water distribution, and chemical transport infrastructure are fostering the adoption of rectangular DRA systems. European operators are also drawn to the benefits of reduced energy consumption, lower operational costs, and enhanced pipeline lifespan. The region is experiencing significant growth across industrial, municipal, and energy sectors, with DRAs being integrated into both new and existing pipeline networks.

U.K. Rectangular DRA Market Insight

The U.K. rectangular DRA market is expected to witness the fastest growth rate from 2025 to 2032, driven by rising energy efficiency initiatives and sustainability-focused pipeline projects. Concerns over operational costs, energy optimization, and environmental impact are encouraging pipeline operators to implement DRA systems. The U.K.’s adoption of advanced pipeline technologies, alongside government-backed energy-saving programs, is expected to continue stimulating market growth across municipal and industrial applications.

Germany Rectangular DRA Market Insight

The Germany rectangular DRA market is expected to witness the fastest growth rate from 2025 to 2032, fueled by the country’s emphasis on sustainable industrial operations and energy-efficient infrastructure. Germany’s highly developed pipeline networks and advanced technological capabilities promote the adoption of rectangular DRA systems, particularly in oil & gas and chemical transport applications. The integration of DRAs into new and retrofit pipeline projects, along with compliance to energy regulations, is further enhancing market growth.

Asia-Pacific Rectangular DRA Market Insight

The Asia-Pacific rectangular DRA market is expected to witness the fastest growth rate from 2025 to 2032, driven by rapid industrialization, expanding pipeline networks, and increased focus on energy conservation in countries such as China, India, and Japan. The region's growing inclination toward modernized infrastructure, supported by government incentives and sustainability initiatives, is accelerating the adoption of rectangular DRA systems. In addition, APAC emerging as a hub for pipeline manufacturing and engineering solutions is improving affordability and accessibility, driving adoption across a wider market base.

Japan Rectangular DRA Market Insight

The Japan rectangular DRA market is expected to witness the fastest growth rate from 2025 to 2032 due to the country’s strong emphasis on energy efficiency, advanced industrial infrastructure, and sustainable pipeline operations. Japanese operators are adopting DRAs to optimize flow, reduce pumping energy, and enhance system reliability. The integration of DRAs with advanced monitoring and control systems is further fueling growth, while ongoing infrastructure upgrades continue to support adoption in both municipal and industrial applications.

China Rectangular DRA Market Insight

The China rectangular DRA market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country’s rapid industrialization, large-scale pipeline projects, and increasing focus on energy conservation. China is one of the largest markets for pipeline infrastructure, and DRAs are becoming increasingly popular in water, oil & gas, and chemical transport applications. Government initiatives promoting energy efficiency, combined with domestic manufacturing capabilities, are key factors driving the market in China.

Rectangular DRA Market Share

The Rectangular DRA industry is primarily led by well-established companies, including:

- Accenture plc (U.S.)

- Qualcomm Incorporated (U.S.)

- Unity Technologies (U.S.)

- Adobe Inc. (U.S.)

- Alphabet Inc. (U.S.)

- SoftServe Inc. (U.S.)

- Northern Digital Inc. (U.S.)

- IBM Corporation (U.S.)

- Intel Corporation (U.S.)

- Cisco Systems Inc. (U.S.)

- Oracle Corporation (U.S.)

- Microsoft Corporation (U.S.)

- ARM Holdings (U.K.)

- Sage Group plc (U.K.)

- Micro Focus International (U.K.)

- Imagination Technologies (U.K.)

- BT Group plc (U.K.)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.