Global Recyclable Barrier Packaging Materials Market

Market Size in USD Billion

USD

55.30 Billion

USD

111.81 Billion

2025

2033

USD

55.30 Billion

USD

111.81 Billion

2025

2033

| 2026 - 2033 | |

| USD 55.30 Billion | |

| USD 111.81 Billion | |

| % | |

|

Recyclable Barrier Packaging Materials Market Overview

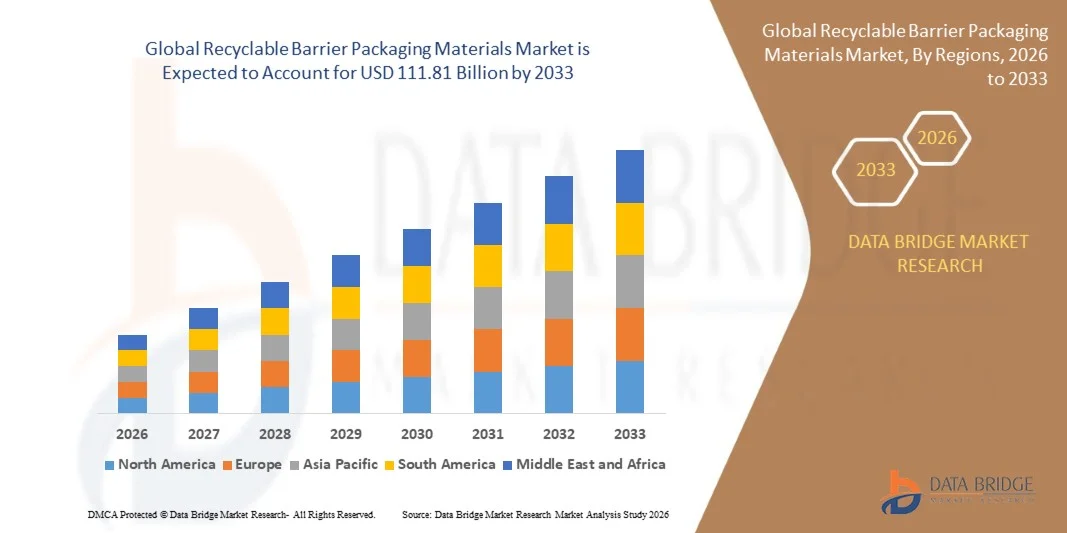

The Recyclable Barrier Packaging Materials Market was valued at USD 55.30 billion in 2025 and is projected to reach USD 111.81 billion by 2033, growing at a CAGR of 9.20% from 2026 to 2033. The market is witnessing strong growth driven by rising demand for sustainable packaging solutions, increasing regulatory pressure on single-use plastics, and rapid expansion of the food and beverage, pharmaceuticals, and personal care industries.

The growing emphasis on circular economy practices and corporate sustainability commitments is accelerating the adoption of recyclable barrier materials such as mono-material films, paper-based barrier coatings, and bio-based polymers. In addition, advancements in high-performance barrier technologies are enabling manufacturers to maintain product shelf life and protection while improving recyclability, making these materials increasingly attractive across global supply chains.

Key Market Trends & Insights

- North America dominated the recyclable barrier packaging materials market with the largest revenue share of approximately 34.6% in 2025, supported by advanced recycling infrastructure, strong adoption of mono-material packaging solutions, and high consumer awareness regarding sustainable packaging practices across commercial and industrial sectors.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of approximately 10.0% to 10.5% from 2026 to 2033. Growth is driven by rapid urbanization, expanding e-commerce and food delivery sectors, rising environmental awareness, and increasing government initiatives promoting plastic waste reduction in countries such as China, India, and Japan.

- The Plastics segment held the largest market revenue share of approximately 41.5% in 2025 driven by strong adoption of recyclable polyethylene and polypropylene-based mono-material structures across food, beverage, and personal care packaging applications. These materials are widely preferred due to their excellent barrier performance, lightweight nature, and compatibility with existing recycling infrastructure.

- The Bioplastics segment is projected to register the fastest growth at a CAGR of 11.2% from 2026 to 2033, driven by increasing demand for bio-based and compostable packaging solutions across premium food and pharmaceutical applications. Rising regulatory pressure on fossil-based plastics and growing corporate sustainability commitments are accelerating the shift toward starch-based and PLA-based barrier materials.

- The Flexible Packaging segment held the largest market revenue share of approximately 58.3% in 2025 driven by its wide usage in snack foods, frozen foods, beverages, and e-commerce packaging due to its lightweight structure, cost efficiency, and strong barrier protection capabilities. Flexible recyclable films and pouches are increasingly replacing multilayer non-recyclable formats across global supply chains.

- The Semi-Rigid Packaging segment is projected to register the fastest growth at a CAGR of 9.6% from 2026 to 2033, driven by rising adoption in dairy products, ready-to-eat meals, and pharmaceutical packaging applications. Demand is increasing for recyclable trays and containers that provide structural stability while maintaining sustainability compliance.

- The Moisture Barrier segment held the largest market revenue share of approximately 34.9% in 2025 driven by its critical role in food preservation, pharmaceutical stability, and moisture-sensitive industrial packaging applications. High-performance recyclable coatings and mono-material films are increasingly being used to replace conventional multilayer moisture-resistant structures.

- The Oxygen Barrier segment is projected to register the fastest growth at a CAGR of 10.4% from 2026 to 2033, driven by increasing demand for extended shelf life in packaged foods, beverages, and pharmaceutical products. Advanced nanocoating technologies and bio-based barrier additives are improving oxygen resistance in recyclable packaging formats.

- The Food & Beverage segment held the largest market revenue share of approximately 46.7% in 2025 driven by strong demand for sustainable packaging solutions in dairy, snacks, bakery, and ready-to-eat food categories. Increasing retail consumption and e-commerce food delivery services are further boosting adoption of recyclable barrier materials.

- The Pharmaceuticals segment is projected to register the fastest growth at a CAGR of 9.8% from 2026 to 2033, driven by rising demand for sustainable yet high-protection packaging formats for tablets, capsules, and injectable products. Strict regulatory compliance requirements and increasing adoption of recyclable blister packs and coated paper-based solutions are accelerating segment expansion.

Market Size & Forecast

- Global Market Value (2025): USD 55.30 Billion

- Expected Market Value (2033): USD 111.81 Billion

- Forecast CAGR (2026–2033): 9.20%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Recyclable Barrier Packaging Materials Market Segmentation

|

Attributes |

Recyclable Barrier Packaging Materials Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• 3M (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Recyclable Barrier Packaging Materials Market Trends

Trend: Growth In Sustainable Packaging Innovation And High-Performance Recyclable Barrier Materials

Increasing demand for sustainable packaging solutions, coupled with tightening global regulations on single-use plastics, is accelerating the shift toward recyclable barrier packaging materials across food, beverage, pharmaceutical, and personal care industries. Conventional multi-layer plastic packaging, which offers strong barrier protection but limited recyclability, is being replaced by mono-material structures and advanced recyclable coatings that maintain product integrity while improving end-of-life recyclability.

In modern food packaging systems, manufacturers are increasingly adopting recyclable polyethylene (PE) and polypropylene (PP)-based barrier films, For instance in dairy, snacks, and frozen food applications, to extend shelf life while meeting sustainability targets. In pharmaceutical packaging, recyclable high-barrier blister packs and coated paper-based solutions are being used to reduce plastic waste without compromising moisture and oxygen protection for sensitive drugs.

The rapid expansion of e-commerce and ready-to-eat food delivery services is also increasing demand for lightweight, durable, and recyclable barrier packaging that ensures product safety during long-distance transportation. In addition, regulatory frameworks such as the European Union’s Packaging and Packaging Waste Regulation (PPWR) and Extended Producer Responsibility (EPR) policies in 2025 are pushing companies to redesign packaging portfolios with at least 70–90% recyclability targets across product lines. Pilot packaging trials conducted in 2025 by major FMCG brands in Europe demonstrated a reduction of nearly 15–20% in packaging-related carbon emissions through adoption of mono-material recyclable barrier structures.

Recyclable Barrier Packaging Materials Market Dynamics

Key Market Driver: Rising Demand For Sustainable And Shelf-Stable Packaging Solutions

Industries across food, beverage, pharmaceuticals, and cosmetics are facing increasing pressure to reduce environmental impact while maintaining high product protection standards. Growing consumer awareness regarding plastic waste and sustainability is driving strong demand for recyclable barrier materials that offer moisture, oxygen, and grease resistance without relying on non-recyclable multilayer laminates.

Food and beverage companies are increasingly deploying recyclable barrier films and coated paper-based packaging for packaged meals, dairy products, and beverages to extend shelf life and reduce spoilage losses. For instance, global FMCG manufacturers have introduced recyclable mono-PE packaging formats for snack products and frozen foods in large-scale retail markets to comply with sustainability commitments.

Similarly, pharmaceutical companies are adopting recyclable blister packaging and high-barrier paper-based solutions to reduce environmental footprint while maintaining strict regulatory compliance for drug safety and stability. Expansion of organized retail and e-commerce grocery platforms is further accelerating demand for lightweight and durable recyclable packaging formats that reduce transportation costs and packaging waste.

Key Restraint/Challenge: Performance Limitations And High Transition Costs

Despite strong sustainability demand, recyclable barrier packaging materials face challenges related to performance limitations compared to traditional multilayer plastic structures. Achieving equivalent oxygen and moisture barrier performance using mono-material or recyclable coatings remains technically complex, especially for long shelf-life and high-sensitivity products.

In addition, the transition from conventional packaging systems to recyclable alternatives requires significant investment in new production technologies, material redesign, and supply chain restructuring, creating cost pressures for manufacturers. Small and mid-sized packaging converters face difficulties in adopting advanced barrier coating technologies due to high capital expenditure and limited technical expertise.

Industry performance benchmarking indicates that traditional multilayer barrier films can extend product shelf life by 20–40% more than early-generation recyclable mono-material alternatives in certain applications, limiting full-scale replacement in high-barrier requirements such as pharmaceutical and industrial packaging.

Key Market Opportunity: Expansion Of Mono-Material And Bio-Based Barrier Packaging Technologies

The increasing focus on circular economy principles and regulatory compliance is creating significant opportunities for innovation in mono-material and bio-based recyclable barrier packaging solutions. Growing investments in advanced polymer science, including polyethylene-based high-barrier coatings and biodegradable barrier layers, are enabling manufacturers to improve recyclability without sacrificing performance.

Packaging companies are increasingly collaborating with FMCG and food service brands to develop fully recyclable packaging formats that meet both sustainability and functional requirements. For instance, pilot projects in Europe and North America during 2025 have demonstrated successful commercialization of mono-PE stand-up pouches and recyclable paper-based barrier laminates with comparable performance to conventional multilayer packaging in selected applications.

In addition, rising demand from e-commerce logistics, ready-to-eat meal services, and pharmaceutical cold-chain packaging is expanding opportunities for high-performance recyclable barrier materials. Advancements in nanocoating technologies and bio-based barrier resins are further enhancing oxygen and moisture resistance, opening new growth avenues across Asia-Pacific and North America markets.

Recyclable Barrier Packaging Materials Market Scope

The market is segmented on the basis of material type, packaging type, barrier type, and end-use industry.

• By Material Type

On the basis of material type, the recyclable barrier packaging materials market is segmented into Paper & Paperboard, Plastics, Bioplastics, and Aluminum-Based Materials. The Plastics segment held the largest market revenue share of approximately 41.5% in 2025 driven by strong adoption of recyclable polyethylene and polypropylene-based mono-material structures across food, beverage, and personal care packaging applications. These materials are widely preferred due to their excellent barrier performance, lightweight nature, and compatibility with existing recycling infrastructure.

The Bioplastics segment is projected to register the fastest growth at a CAGR of 11.2% from 2026 to 2033, driven by increasing demand for bio-based and compostable packaging solutions across premium food and pharmaceutical applications. Rising regulatory pressure on fossil-based plastics and growing corporate sustainability commitments are accelerating the shift toward starch-based and PLA-based barrier materials.

• By Packaging Type

On the basis of packaging type, the market is segmented into Flexible Packaging, Rigid Packaging, and Semi-Rigid Packaging. The Flexible Packaging segment held the largest market revenue share of approximately 58.3% in 2025 driven by its wide usage in snack foods, frozen foods, beverages, and e-commerce packaging due to its lightweight structure, cost efficiency, and strong barrier protection capabilities. Flexible recyclable films and pouches are increasingly replacing multilayer non-recyclable formats across global supply chains.

The Semi-Rigid Packaging segment is projected to register the fastest growth at a CAGR of 9.6% from 2026 to 2033, driven by rising adoption in dairy products, ready-to-eat meals, and pharmaceutical packaging applications. Demand is increasing for recyclable trays and containers that provide structural stability while maintaining sustainability compliance.

• By Barrier Type

On the basis of barrier type, the market is segmented into Moisture Barrier, Oxygen Barrier, Grease Barrier, and UV Barrier. The Moisture Barrier segment held the largest market revenue share of approximately 34.9% in 2025 driven by its critical role in food preservation, pharmaceutical stability, and moisture-sensitive industrial packaging applications. High-performance recyclable coatings and mono-material films are increasingly being used to replace conventional multilayer moisture-resistant structures.

The Oxygen Barrier segment is projected to register the fastest growth at a CAGR of 10.4% from 2026 to 2033, driven by increasing demand for extended shelf life in packaged foods, beverages, and pharmaceutical products. Advanced nanocoating technologies and bio-based barrier additives are improving oxygen resistance in recyclable packaging formats.

• By End-Use Industry

On the basis of end-use industry, the market is segmented into Food & Beverage, Pharmaceuticals, Personal Care & Cosmetics, Industrial Packaging, and Others. The Food & Beverage segment held the largest market revenue share of approximately 46.7% in 2025 driven by strong demand for sustainable packaging solutions in dairy, snacks, bakery, and ready-to-eat food categories. Increasing retail consumption and e-commerce food delivery services are further boosting adoption of recyclable barrier materials.

The Pharmaceuticals segment is projected to register the fastest growth at a CAGR of 9.8% from 2026 to 2033, driven by rising demand for sustainable yet high-protection packaging formats for tablets, capsules, and injectable products. Strict regulatory compliance requirements and increasing adoption of recyclable blister packs and coated paper-based solutions are accelerating segment expansion.

Recyclable Barrier Packaging Materials Market Regional Analysis

North America Recyclable Barrier Packaging Materials Market Insight

North America dominated the recyclable barrier packaging materials market with the largest revenue share of approximately 34.6% in 2025, supported by strong demand for sustainable packaging solutions, advanced recycling infrastructure, and strict regulatory frameworks promoting circular economy practices. The region benefits from high adoption of mono-material barrier films, paper-based coatings, and recyclable flexible packaging across food, beverage, and pharmaceutical industries. In addition, increasing corporate sustainability commitments and consumer preference for eco-friendly packaging are further driving market expansion across both retail and industrial supply chains.

U.S. Recyclable Barrier Packaging Materials Market Insight

The U.S. recyclable barrier packaging materials market captured the largest revenue share within North America in 2025, driven by rapid adoption of sustainable packaging innovations across major FMCG, food delivery, and pharmaceutical companies. Strong investment in recyclable mono-PE and mono-PP structures, along with advanced coating technologies, is supporting large-scale replacement of traditional multilayer plastic packaging. In addition, growing e-commerce penetration and increasing regulatory pressure on plastic waste reduction are accelerating demand for high-performance recyclable barrier materials in both consumer and industrial applications.

Europe Recyclable Barrier Packaging Materials Market Insight

The Europe recyclable barrier packaging materials market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent environmental regulations, packaging waste reduction mandates, and strong enforcement of Extended Producer Responsibility (EPR) frameworks. The region is rapidly shifting toward fully recyclable and compostable packaging systems, supported by government-backed sustainability targets and corporate ESG commitments. Increasing adoption of mono-material films, fiber-based barrier solutions, and bio-based coatings across food and pharmaceutical packaging is further strengthening market growth.

U.K. Recyclable Barrier Packaging Materials Market Insight

The U.K. recyclable barrier packaging materials market is expected to witness steady growth from 2026 to 2033, driven by rising consumer awareness regarding plastic waste reduction and increasing demand for sustainable packaging in retail and food delivery sectors. The country’s strong focus on circular economy initiatives and packaging waste regulations is encouraging manufacturers to transition toward recyclable mono-material structures. In addition, growth in e-commerce grocery platforms and ready-to-eat food services is further boosting demand for lightweight and recyclable barrier packaging solutions.

Germany Recyclable Barrier Packaging Materials Market Insight

The Germany recyclable barrier packaging materials market is expected to witness significant growth from 2026 to 2033, supported by advanced recycling systems, strong environmental policies, and high consumer preference for sustainable packaging solutions. Germany’s well-established circular economy framework is driving widespread adoption of recyclable paper-based barrier materials and mono-material plastic films across food, beverage, and industrial packaging applications. In addition, increasing innovation in bio-based coatings and high-performance recyclable films is supporting long-term market expansion aligned with national sustainability goals.

Asia-Pacific Recyclable Barrier Packaging Materials Market Insight

The Asia-Pacific recyclable barrier packaging materials market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid urbanization, rising disposable incomes, and expanding food processing and e-commerce industries in countries such as China, India, and Japan. The region is experiencing strong demand for cost-effective and sustainable packaging solutions due to increasing environmental awareness and government initiatives promoting plastic waste reduction. In addition, APAC’s strong manufacturing base and growing export-oriented packaging industry are further accelerating adoption of recyclable barrier materials across multiple end-use sectors.

Japan Recyclable Barrier Packaging Materials Market Insight

The Japan recyclable barrier packaging materials market is expected to witness steady growth from 2026 to 2033 due to the country’s advanced recycling culture, high environmental awareness, and strong emphasis on packaging efficiency. Japan’s packaging industry is increasingly adopting mono-material recyclable films and paper-based barrier solutions to reduce plastic dependency while maintaining product protection standards. In addition, rising demand from the food, pharmaceutical, and convenience packaging sectors is supporting growth, particularly in urban retail and aging population-driven consumption patterns.

China Recyclable Barrier Packaging Materials Market Insight

The China recyclable barrier packaging materials market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rapid industrialization, strong e-commerce expansion, and increasing government focus on plastic waste reduction initiatives. China’s large-scale packaging manufacturing base and growing adoption of sustainable mono-material barrier films are supporting widespread market penetration across food, beverage, and personal care industries. In addition, rising consumer awareness and the development of smart cities and green logistics systems are further driving demand for recyclable barrier packaging solutions.

Recyclable Barrier Packaging Materials Market Share

The Recyclable Barrier Packaging Materials industry is primarily led by well-established companies, including:

• 3M (U.S.)

• Avery Dennison Corporation (U.S.)

• CCL Industries (Canada)

• Henkel AG & Co. KGaA (Germany)

• UPM (Finland)

• LINTEC Corporation (Japan)

• Mondi Group (U.K.)

• Amcor plc (Switzerland)

• Sealed Air Corporation (U.S.)

• Berry Global Inc. (U.S.)

• Constantia Flexibles (Austria)

• Coveris Holdings S.A. (U.K.)

• Huhtamaki Oyj (Finland)

• Tetra Pak (Switzerland)

• Sonoco Products Company (U.S.)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Recyclable Barrier Packaging Materials Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Recyclable Barrier Packaging Materials Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Recyclable Barrier Packaging Materials Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.