Global Renal Biomarker Market

Market Size in USD Million

CAGR :

%

USD

377.82 Million

USD

683.92 Million

2025

2033

USD

377.82 Million

USD

683.92 Million

2025

2033

| 2026 –2033 | |

| USD 377.82 Million | |

| USD 683.92 Million | |

| % | |

|

Renal Biomarker Market Size

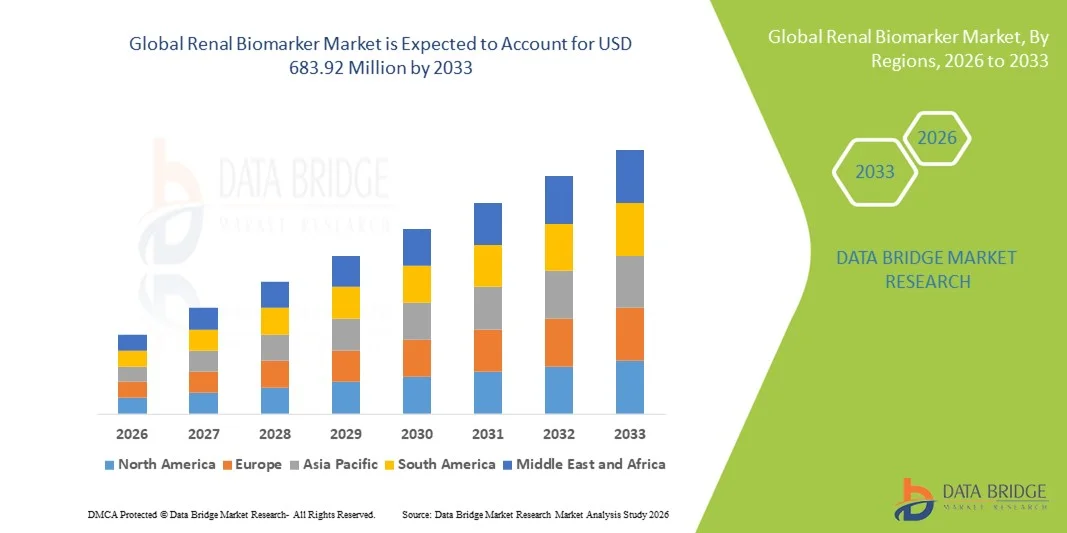

- The global renal biomarker market size was valued at USD 377.82 million in 2025 and is expected to reach USD 683.92 million by 2033, at a CAGR of 7.70% during the forecast period

- The market growth is primarily driven by increasing prevalence of kidney-related disorders, rising awareness of early disease detection, and technological advancements in diagnostic tools for renal health

- In addition, growing demand for non-invasive, accurate, and rapid biomarkers for monitoring kidney function in clinical and research settings is positioning renal biomarkers as essential tools in personalized medicine. These factors are collectively accelerating the adoption of renal biomarker solutions, thereby fueling significant growth in the market

Renal Biomarker Market Analysis

- Renal biomarkers, providing diagnostic and prognostic insights into kidney function and disease, are increasingly essential in clinical practice and research due to their accuracy, non-invasive nature, and ability to support personalized treatment plans in both acute and chronic kidney conditions

- The rising demand for renal biomarkers is primarily driven by the increasing prevalence of chronic kidney disease (CKD) and acute kidney injury (AKI), growing awareness of early disease detection, and the integration of advanced biomarker panels in routine diagnostics

- North America dominated the renal biomarker market with the largest revenue share of 37.2% in 2025, attributed to a well-established healthcare infrastructure, high adoption of advanced diagnostic technologies, and significant investments by key industry players in biomarker development and clinical validation. The U.S. leads in biomarker testing, supported by collaborations between biotech firms and research institutions focusing on innovative renal disease detection assays

- Asia-Pacific is expected to be the fastest growing region in the renal biomarker market during the forecast period due to increasing healthcare expenditures, rising incidence of kidney disorders, and expanding diagnostic facilities in urban and semi-urban areas

- Creatinine segment dominated the renal biomarker market by marker type with a market share of 42.3% in 2025, driven by its widespread use in assessing kidney function, ease of measurement, and established clinical utility in both hospital and diagnostic laboratory settings

Report Scope and Renal Biomarker Market Segmentation

|

Attributes |

Renal Biomarker Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Renal Biomarker Market Trends

Advancement in Multiplex and Non-Invasive Testing

- A significant and accelerating trend in the global renal biomarker market is the development of multiplex assays and non-invasive testing platforms that enable simultaneous detection of multiple kidney biomarkers from a single sample, enhancing diagnostic efficiency and patient comfort

- For instance, multiplex ELISA panels allow clinicians to assess creatinine, BUN, Cystatin C, and NGAL levels in one assay, reducing turnaround time and sample volume requirements

- Integration of non-invasive urine- or saliva-based biomarker assays with automated analysis systems is gaining traction, offering early detection and monitoring without the need for frequent blood draws

- Advanced assay platforms coupled with cloud-based data analytics facilitate real-time patient monitoring, enabling clinicians to track disease progression and adjust therapies more effectively

- Development of wearable biosensors for continuous kidney function monitoring is emerging, allowing real-time insights and proactive disease management

- AI-driven predictive analytics for renal biomarker data is increasingly being adopted to anticipate disease progression and guide personalized treatment plans

- This trend toward rapid, multiplexed, and patient-friendly renal biomarker testing is reshaping expectations for kidney disease diagnostics, driving companies such as Bio-Rad and Siemens Healthineers to innovate with user-friendly and high-throughput assay solutions

- The demand for highly accurate, non-invasive, and comprehensive biomarker assays is growing rapidly across hospitals, diagnostic laboratories, and research centers, as early intervention becomes critical for preventing kidney disease progression

Renal Biomarker Market Dynamics

Driver

Rising Prevalence of Kidney Disorders and Early Diagnosis Awareness

- The increasing prevalence of chronic kidney disease (CKD) and acute kidney injury (AKI), combined with growing awareness of the importance of early detection, is a significant driver of heightened demand for renal biomarkers

- For instance, the U.S. National Kidney Foundation reported a rise in CKD cases, prompting hospitals and diagnostic labs to adopt advanced biomarker panels for timely diagnosis and intervention

- As clinicians and researchers prioritize early detection, renal biomarkers offer highly sensitive and specific measurements, enabling accurate disease staging and monitoring progression

- Furthermore, integration of biomarkers in routine health check-ups and clinical trials is making them indispensable tools in personalized medicine and research-focused patient management

- The convenience of rapid assays, automated testing, and the ability to combine multiple markers in a single platform further propels adoption in both clinical and research settings, supporting improved patient outcomes and operational efficiency

- Growing collaborations between biotech firms and research institutions to develop novel renal biomarkers is accelerating market expansion and innovation

- Increasing government and private funding for kidney disease research is driving the adoption of advanced biomarker solutions across clinical and research applications

Restraint/Challenge

High Cost and Regulatory Barriers

- The relatively high cost of advanced renal biomarker assays compared to traditional kidney function tests poses a challenge for widespread adoption, especially in developing regions or smaller diagnostic facilities

- For instance, premium multiplex ELISA kits and automated assay platforms often require significant upfront investment in equipment and consumables, limiting accessibility

- Regulatory compliance for clinical use of novel biomarkers involves rigorous validation and approvals, delaying market entry and increasing operational complexity for manufacturers

- Addressing these challenges requires manufacturers to optimize assay costs, simplify workflows, and provide robust clinical validation data to meet regulatory standards efficiently

- While costs are gradually decreasing and awareness is improving, price sensitivity and stringent approval processes remain significant barriers to the faster adoption of renal biomarker solutions globally

- Limited availability of trained personnel and standardized protocols for renal biomarker testing in certain regions can hinder market growth

- Variability in biomarker performance across different populations and sample types necessitates extensive clinical validation, adding complexity and time to market adoption

Renal Biomarker Market Scope

The market is segmented on the basis of marker type, assay platform type, application, and end-user.

- By Marker Type

On the basis of marker type, the renal biomarker market is segmented into Creatinine, blood urea nitrogen (BUN), cystatin C, neutrophil gelatinase-associated lipocalin (NGAL), and others. The Creatinine segment dominated the market with the largest revenue share of 42.3% in 2025, driven by its widespread use in routine kidney function tests and well-established clinical relevance. Hospitals and diagnostic laboratories extensively rely on creatinine measurements for monitoring glomerular filtration rate (GFR) and detecting early kidney impairment. Its ease of measurement, standardization across laboratories, and integration into automated assay platforms further enhance adoption. Creatinine assays are cost-effective, compatible with a range of diagnostic systems, and frequently included in comprehensive metabolic panels, reinforcing their dominance in clinical workflows. Established awareness among clinicians regarding creatinine as a key renal function indicator contributes to sustained demand globally.

The NGAL segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing clinical recognition of NGAL as an early biomarker for acute kidney injury (AKI) and its role in predicting disease progression. NGAL assays offer higher sensitivity than traditional markers, enabling timely intervention and improved patient outcomes. Its adoption is growing in research studies and hospitals focused on high-risk patients, such as those in intensive care units. The integration of NGAL into multiplex panels with creatinine and BUN enhances diagnostic accuracy. Rising investment in novel biomarker development and validation further accelerates NGAL adoption. Increasing physician awareness and growing demand for precision diagnostics contribute to its rapid growth trajectory.

- By Assay Platform Type

On the basis of assay platform type, the market is segmented into enzyme-linked immunosorbent assay (ELISA), enzymatic assay, turbidimetric immunoassay, and others. The ELISA segment dominated the market in 2025 due to its high sensitivity, specificity, and ability to quantify multiple renal biomarkers simultaneously. ELISA platforms are widely adopted in both clinical and research laboratories for protein biomarkers such as NGAL and Cystatin C, providing reproducible and reliable results. Automation and compatibility with high-throughput testing further enhance ELISA’s prominence. Hospitals and diagnostic labs favor ELISA for its versatility, standardization, and ability to integrate into multiplex panels. Strong industry support, including commercially available kits from established suppliers, ensures widespread availability and continued dominance.

The Turbidimetric Immunoassay segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its rapid turnaround time, cost-effectiveness, and suitability for routine clinical testing. Turbidimetric assays allow high-throughput measurement of renal biomarkers such as Cystatin C in large patient populations. Their automation potential and compatibility with existing laboratory instruments make them appealing for hospital laboratories. Growing awareness of their clinical utility in early CKD detection is increasing adoption. Expanding diagnostic infrastructure in emerging markets also supports faster growth of turbidimetric platforms.

- By Application

On the basis of application, the market is segmented into diagnosis and disease progression monitoring, and research. The Diagnosis and Disease Progression Monitoring segment dominated in 2025 due to increasing prevalence of chronic kidney disease (CKD) and acute kidney injury (AKI) globally. Biomarkers are critical for early detection, risk stratification, and monitoring therapeutic efficacy, making this segment the primary revenue contributor. Hospitals and diagnostic labs heavily rely on biomarkers for patient management and treatment planning. Integration of advanced biomarker panels into routine clinical workflows enhances adoption. Increasing physician awareness of early intervention benefits reinforces the segment’s dominance

The Research segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by expanding clinical trials and biomarker discovery studies targeting renal disorders. Research institutions are increasingly adopting multiplex and high-sensitivity assays to identify novel biomarkers for personalized medicine. Growing investments from pharmaceutical and biotech companies in kidney disease research support rapid adoption. Technological advancements, such as AI-driven biomarker analysis, are enhancing research efficiency. Collaborative projects between academia and industry further accelerate market growth in this segment.

- By End-User

On the basis of end-user, the market is segmented into hospitals, diagnostic laboratories, and others. The Hospitals segment dominated in 2025 due to the high volume of patient testing and the critical need for timely diagnosis and monitoring of kidney function in clinical settings. Hospitals utilize renal biomarker assays for inpatient and outpatient management, including ICU monitoring for AKI and routine CKD evaluations. Integration of automated testing systems and electronic health record (EHR) compatibility supports widespread adoption. Clinicians’ trust in standardized biomarker panels reinforces hospitals as the leading end-user.

The Diagnostic Laboratories segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing outsourcing of kidney function tests, expansion of private lab networks, and growing demand for high-throughput, specialized biomarker testing. Laboratories are adopting advanced assay platforms to meet the needs of research institutions, hospitals, and private clinics. Rising awareness of early detection benefits among patients and physicians fuels laboratory-based testing. Investment in laboratory automation and multiplex platforms accelerates adoption. Emerging markets with expanding diagnostic infrastructure contribute to the rapid growth of this segment.

Renal Biomarker Market Regional Analysis

- North America dominated the renal biomarker market with the largest revenue share of 37.2% in 2025, attributed to a well-established healthcare infrastructure, high adoption of advanced diagnostic technologies, and significant investments by key industry players in biomarker development and clinical validation

- Hospitals and diagnostic laboratories in the region prioritize the use of renal biomarkers for early detection, disease monitoring, and personalized treatment planning, reflecting the strong clinical utility of these assays

- This widespread adoption is further supported by high healthcare expenditure, extensive research and development initiatives, and the presence of key industry players investing in innovative assay platforms, establishing renal biomarkers as essential tools in clinical practice and research

U.S. Renal Biomarker Market Insight

The U.S. renal biomarker market captured the largest revenue share of 79% in 2025 within North America, driven by the high prevalence of chronic kidney disease (CKD) and acute kidney injury (AKI) and early adoption of advanced diagnostic technologies. Healthcare providers are increasingly prioritizing early detection and monitoring of kidney disorders through sensitive biomarker assays. The growing focus on personalized medicine, integration of multiplex assays, and the adoption of automated platforms in hospitals and diagnostic laboratories further propel the market. In addition, strong research initiatives and collaborations between biotech companies and academic institutions are expanding the availability and utility of renal biomarkers.

Europe Renal Biomarker Market Insight

The Europe renal biomarker market is projected to grow at a substantial CAGR during the forecast period, fueled by increasing prevalence of kidney disorders, stringent healthcare regulations, and rising demand for early diagnostic solutions. Hospitals and diagnostic laboratories are adopting biomarker assays to enhance disease management and treatment outcomes. Urbanization, higher healthcare expenditure, and awareness programs targeting kidney health are fostering adoption. The market is expanding across hospital-based testing, private diagnostic labs, and research centers, with emphasis on non-invasive, high-sensitivity assays for improved patient care.

U.K. Renal Biomarker Market Insight

The U.K. renal biomarker market is expected to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of kidney health, early diagnosis initiatives, and the rising burden of CKD and AKI. Healthcare institutions and diagnostic labs are integrating biomarker testing into routine patient management and preventive healthcare programs. The U.K.’s robust healthcare infrastructure, coupled with supportive government policies for diagnostic innovation, promotes adoption. Growing interest in personalized treatment approaches and the use of multiplex assays in clinical research further supports market growth.

Germany Renal Biomarker Market Insight

The Germany renal biomarker market is anticipated to expand at a considerable CAGR during the forecast period, driven by advanced healthcare infrastructure, emphasis on early detection, and high adoption of precision diagnostics. Hospitals and research institutions are increasingly utilizing renal biomarkers for monitoring disease progression and therapy response. Germany’s focus on innovation, clinical validation, and quality standards encourages uptake of novel biomarkers. Integration with automated laboratory systems and research platforms is boosting efficiency. Increasing demand for non-invasive assays and high-sensitivity detection methods is further fueling market growth.

Asia-Pacific Renal Biomarker Market Insight

The Asia-Pacific renal biomarker market is poised to grow at the fastest CAGR of 23% during the forecast period of 2026 to 2033, driven by rising prevalence of kidney disorders, expanding healthcare infrastructure, and increasing awareness of early disease detection. Countries such as China, Japan, and India are witnessing growing adoption of high-sensitivity and multiplex biomarker assays in hospitals and diagnostic laboratories. Government initiatives supporting healthcare digitalization and kidney health programs are accelerating market penetration. In addition, increasing investment in clinical research and growing availability of cost-effective biomarker assays are contributing to rapid adoption across the region.

Japan Renal Biomarker Market Insight

The Japan renal biomarker market is gaining momentum due to the country’s aging population, high healthcare standards, and emphasis on early diagnosis and disease monitoring. Hospitals and diagnostic laboratories are increasingly adopting renal biomarkers to provide timely intervention and personalized treatment for kidney disorders. The integration of automated assay platforms and multiplex testing enhances efficiency and patient care. Research institutions are also leveraging biomarkers for clinical trials and novel biomarker discovery. Increasing government focus on preventive healthcare and chronic disease management supports sustained market growth.

India Renal Biomarker Market Insight

The India renal biomarker market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, rising prevalence of kidney disorders, and growing healthcare awareness. The expanding middle class and increasing access to diagnostic services are driving adoption across hospitals, diagnostic laboratories, and research centers. Government initiatives promoting kidney health and preventive care, along with affordable biomarker assay options, are supporting market expansion. Strong presence of domestic diagnostic companies and growing clinical research activities further enhance the growth potential in India.

Renal Biomarker Market Share

The Renal Biomarker industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- F. Hoffmann‑La Roche Ltd (Switzerland)

- Beckman Coulter, Inc. (U.S.)

- BIOMÉRIEUX (France)

- Thermo Fisher Scientific Inc. (U.S.)

- Randox Laboratories Ltd (U.K.)

- Siemens Healthineers AG (Germany)

- BioPorto Diagnostics A/S (Denmark)

- Gentian Diagnostic (Norway)

- Proteomics International (Australia)

- SphingoTec GmbH (Germany)

- QIAGEN (Netherlands)

- BD (U.S.)

- DiaSorin S.p.A. (Italy)

- EKF Diagnostics Holdings plc (U.K.)

- Ortho Clinical Diagnostics Holdings plc (U.S.)

- Quidel Corporation (U.S.)

- Bio‑Rad Laboratories, Inc. (U.S.)

- Diaxonhit (France)

- Nexelis (Canada)

What are the Recent Developments in Global Renal Biomarker Market?

- In September 2025, BioPorto A/S confirmed that its ProNephro AKI (NGAL) acute kidney injury test has been made available to U.S. clinical chemistry laboratories via Roche’s automated cobas c 501 analyzers, marking a significant step for AKI biomarker adoption in hospital and diagnostic settings

- In August 2025, BioPorto A/S announced that ProNephro AKI™ (NGAL) a renal biomarker test for early acute kidney injury (AKI) detection is now commercially available to U.S. laboratories through a collaboration with Roche Diagnostics and is the first AKI biomarker test cleared for pediatric use (ages ~3 months to 21 years), enabling earlier identification of kidney injury compared to traditional serum creatinine measures

- In October 2024, SphingoTec GmbH entered into a partnership with Beckman Coulter Diagnostics to integrate its Proenkephalin 119‑159 (penKid) renal function biomarker assay into Beckman Coulter’s immunoassay analyzers, expanding global AKI and kidney function diagnostic capabilities via high‑throughput testing platforms

- In October 2024, BioPorto A/S entered a global distribution partnership with Beckman Coulter, Inc. for its NGAL renal biomarker tests, enabling broader international availability on Beckman Coulter chemistry analyzers and expanding early AKI diagnostics worldwide

- In February 2024, BioPorto A/S expanded its collaboration with Roche Diagnostics to broaden global distribution and platform support for its NGAL‑based acute kidney injury test—including enhanced use across Roche’s chemistries following earlier FDA clearance and clinical certifications for pediatric AKI risk assessment

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.