Global Reprographic Paper Market

Market Size in USD Billion

USD

89.87 Billion

USD

116.52 Billion

2025

2033

USD

89.87 Billion

USD

116.52 Billion

2025

2033

| 2026 - 2033 | |

| USD 89.87 Billion | |

| USD 116.52 Billion | |

| % | |

|

Reprographic Paper Market Overview

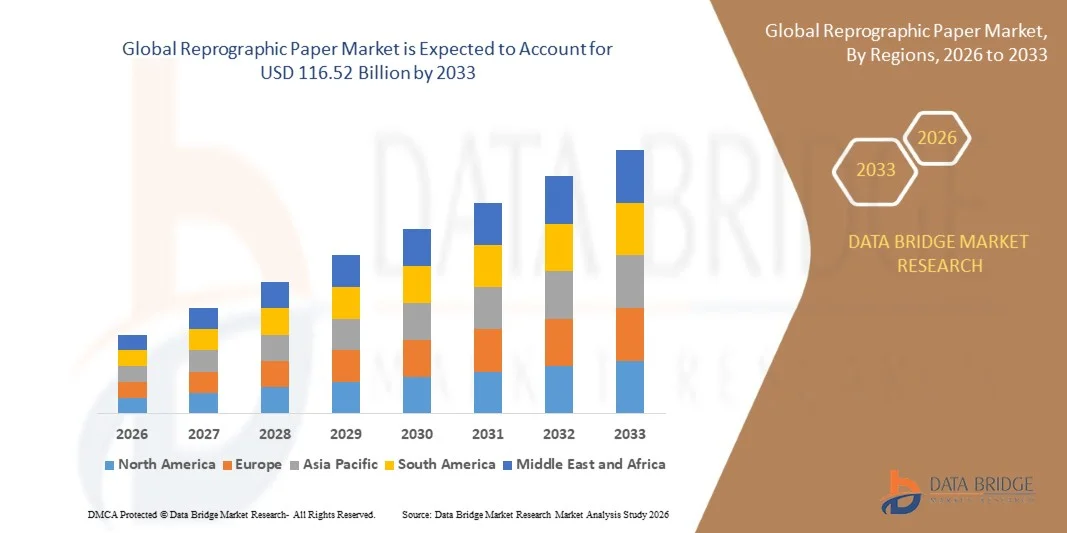

The Reprographic Paper Market was valued at USD 89.87 billion in 2025 and is projected to reach USD 116.52 billion by 2033, growing at a CAGR of 3.30% from 2026 to 2033. The market is experiencing steady growth driven by sustained demand for printing and copying applications across educational institutions, corporate offices, government organizations, and commercial printing facilities, along with increasing consumption of high-quality paper products in developing economies.

The continued expansion of educational infrastructure, administrative documentation requirements, and business communication activities is supporting consistent demand for reprographic paper worldwide. Despite ongoing digital transformation initiatives, paper remains essential for official records, legal documentation, academic materials, invoices, manuals, and office printing applications. Manufacturers are increasingly focusing on producing high-brightness, jam-resistant, and environmentally sustainable paper grades that improve printing performance while meeting evolving environmental standards. In addition, growing investments in sustainable forestry practices, recycled paper production, and eco-friendly manufacturing technologies are strengthening market development across both mature and emerging economies.

Key Market Trends & Insights

- North America dominated the reprographic paper market with the largest revenue share of 35.84% in 2025, supported by strong demand from corporate offices, educational institutions, government agencies, and commercial printing facilities, as well as the presence of established paper manufacturers and advanced printing infrastructure.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 4.1% from 2026 to 2033. Growth is driven by expanding educational infrastructure, increasing literacy rates, rapid urbanization, growing business activities, and rising paper consumption across developing economies such as China and India.

- The 30-90 GSM segment held the largest market revenue share of approximately 52.6% in 2025 driven by its extensive use in office printing, photocopying, educational materials, and business documentation. Papers within this weight range provide an optimal balance between print quality, durability, and cost-effectiveness, making them the preferred choice for high-volume printing applications globally.

- The 91-120 GSM segment is projected to register the fastest growth at a CAGR of 3.9% from 2026 to 2033, driven by increasing demand for premium-quality documents, corporate reports, marketing materials, and professional printing applications. Growing preference for higher-opacity and enhanced print-performance papers is supporting segment expansion.

- The Finished segment held the largest market revenue share of approximately 68.4% in 2025 driven by its widespread use in copier paper, office stationery, educational printing, and commercial documentation. Finished papers offer superior print clarity, toner adhesion, and compatibility with a broad range of printing equipment, supporting their dominant market position.

- The Glazed segment is projected to register the fastest growth at a CAGR of 3.7% from 2026 to 2033, driven by increasing demand for premium print applications, high-quality image reproduction, and specialized commercial printing requirements. Enhanced surface smoothness and improved visual appeal are encouraging adoption across select printing applications.

- The Untapped segment held the largest market revenue share of approximately 74.1% in 2025 driven by its extensive use in standard office printing, copying, educational materials, and commercial document production. Its broad compatibility with printers and copiers, combined with ease of handling and lower cost, continues to support strong demand across end-use sectors.

- The Taped segment is projected to register the fastest growth at a CAGR of 3.8% from 2026 to 2033, driven by increasing utilization in engineering drawings, large-format printing, architectural documentation, and specialized technical applications. Growing demand for organized document management and continuous-feed printing systems is contributing to segment growth.

- The Magazines segment held the largest market revenue share of approximately 36.8% in 2025 driven by continuous demand from publishing companies, advertising agencies, and commercial printing firms. High-volume magazine production and marketing publications continue to generate significant consumption of reprographic paper despite increasing digital media adoption.

- The Architectural Designs segment is projected to register the fastest growth at a CAGR of 4.2% from 2026 to 2033, driven by increasing construction activities, infrastructure development projects, and demand for large-format technical drawings. Growing investments in urban development and engineering projects are accelerating the use of reprographic paper for blueprinting and design documentation applications.

Market Size & Forecast

- Global Market Value (2025): USD 89.87 Billion

- Expected Market Value (2033): USD 116.52 Billion

- Forecast CAGR (2026–2033): 3.30%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Reprographic Paper Market Segmentation

|

Attributes |

Reprographic Paper Key Market Insights |

|

Segments Covered |

· By Weight: <30 GSM, 30-90 GSM, 91-120 GSM, 121-180 GSM and 180 GSM · By Finish Type: Glazed and Finished · By ProductType: Taped and Untapped · By Application: Catalogues, Magazines, Architectural Designs and Others |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Domtar Corporation (U.S.) |

|

Market Opportunities |

• Increasing Demand For Sustainable And Recycled Reprographic Paper Products • Expansion Of Educational Institutions And Commercial Printing Activities In Emerging Economies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Reprographic Paper Market Trends

Trend: Rising Adoption Of Sustainable And High-Performance Paper Products

Growing environmental awareness and increasing corporate sustainability commitments are driving demand for eco-friendly reprographic paper across educational institutions, offices, commercial printing facilities, and government organizations. Businesses are increasingly seeking paper products manufactured from certified sustainable forestry sources and recycled fiber content to reduce environmental impact while maintaining print quality and operational efficiency. This trend is encouraging paper manufacturers to invest in advanced production technologies that improve brightness, durability, and print performance while lowering resource consumption.

Large corporations and public institutions are adopting sustainable procurement policies, For instance prioritizing Forest Stewardship Council (FSC)-certified and recycled paper products, to support environmental goals and regulatory compliance. In addition, advancements in paper coating and manufacturing processes are enabling the production of lightweight, high-opacity papers that reduce raw material usage without compromising performance. Educational institutions and commercial printing companies continue to generate substantial demand for reprographic paper despite increasing digitization initiatives.

The expansion of hybrid work environments and growing demand for high-quality printed documentation are also supporting market stability. In addition, leading paper producers are increasing investments in renewable energy-powered production facilities and circular economy initiatives. Industry reports indicate that recycled paper utilization rates in several European paper mills exceeded 70% during 2024, highlighting the growing importance of sustainable paper manufacturing practices across the industry.

Reprographic Paper Market Dynamics

Key Market Driver: Continued Demand From Education, Corporate, And Commercial Printing Sectors

Educational institutions, government agencies, corporate offices, and commercial printing businesses continue to rely heavily on reprographic paper for documentation, communication, recordkeeping, and administrative activities. Although digital transformation is progressing globally, printed materials remain essential for contracts, legal records, educational content, reports, invoices, and operational workflows, supporting consistent demand for reprographic paper products.

Schools, universities, and training centers are major consumers of reprographic paper, For instance for examination materials, learning resources, and administrative documentation. Similarly, businesses continue to utilize paper for official correspondence, internal records, and customer-facing documents. Commercial printing companies also contribute significantly to demand through production of manuals, catalogs, brochures, and promotional materials.

Furthermore, growing literacy rates, expanding educational infrastructure, and rising office-based activities in emerging economies are creating additional growth opportunities. Industry assessments conducted during 2024 indicated that global office paper consumption remained above 75 million metric tons annually despite increasing adoption of digital document management systems, demonstrating the continued importance of reprographic paper across multiple end-use sectors.

Key Restraint/Challenge: Accelerating Digitalization And Paperless Work Environments

The rapid adoption of digital technologies, cloud-based document management platforms, and electronic communication systems is reducing dependence on printed documents across many industries. Organizations are increasingly implementing paperless initiatives to improve efficiency, reduce operational costs, and support sustainability objectives, creating challenges for long-term growth in reprographic paper consumption.

Educational institutions, corporations, and government agencies are investing in digital learning platforms, e-signature technologies, and electronic recordkeeping systems that reduce printing requirements. In addition, environmental concerns regarding deforestation, paper waste generation, and carbon emissions are encouraging businesses to limit paper usage where possible. Rising raw material and energy costs further create pricing pressures across the paper manufacturing value chain.

Commercial studies indicate that office printing volumes in several developed economies have declined by approximately 15–20% over the past five years due to increasing adoption of digital workflows, presenting a significant challenge for traditional reprographic paper manufacturers.

Key Market Opportunity: Expansion Of Recycled Paper And Sustainable Production Technologies

Growing environmental regulations and increasing consumer preference for sustainable products are creating significant opportunities for manufacturers focused on recycled reprographic paper and environmentally responsible production methods. Organizations across public and private sectors are increasingly incorporating sustainability criteria into procurement decisions, driving demand for eco-friendly paper products.

Paper manufacturers are investing in advanced recycling technologies, For instance closed-loop fiber recovery systems and water-efficient production processes, to improve resource utilization and reduce environmental impact. The development of high-quality recycled paper grades that offer comparable brightness, printability, and durability to virgin-fiber products is expanding market acceptance across commercial and institutional applications.

In addition, rising demand for certified sustainable paper products in North America, Europe, and Asia-Pacific is creating opportunities for premium product differentiation. Investments in renewable energy integration and carbon reduction initiatives are further strengthening market potential. Industry sustainability programs implemented during 2025 reported that modern recycled paper manufacturing facilities were able to reduce water consumption by approximately 30–40% compared to conventional production methods, highlighting substantial growth opportunities within the sustainable reprographic paper segment.

Reprographic Paper Market Scope

The market is segmented on the basis of weight, finish type, product type, and application.

- By Weight

On the basis of weight, the reprographic paper market is segmented into <30 GSM, 30-90 GSM, 91-120 GSM, 121-180 GSM, and >180 GSM. The 30-90 GSM segment held the largest market revenue share of approximately 52.6% in 2025 driven by its extensive use in office printing, photocopying, educational materials, and business documentation. Papers within this weight range provide an optimal balance between print quality, durability, and cost-effectiveness, making them the preferred choice for high-volume printing applications globally.

The 91-120 GSM segment is projected to register the fastest growth at a CAGR of 3.9% from 2026 to 2033, driven by increasing demand for premium-quality documents, corporate reports, marketing materials, and professional printing applications. Growing preference for higher-opacity and enhanced print-performance papers is supporting segment expansion.

- By Finish Type

On the basis of finish type, the reprographic paper market is segmented into Glazed and Finished. The Finished segment held the largest market revenue share of approximately 68.4% in 2025 driven by its widespread use in copier paper, office stationery, educational printing, and commercial documentation. Finished papers offer superior print clarity, toner adhesion, and compatibility with a broad range of printing equipment, supporting their dominant market position.

The Glazed segment is projected to register the fastest growth at a CAGR of 3.7% from 2026 to 2033, driven by increasing demand for premium print applications, high-quality image reproduction, and specialized commercial printing requirements. Enhanced surface smoothness and improved visual appeal are encouraging adoption across select printing applications.

- By Product Type

On the basis of product type, the reprographic paper market is segmented into Taped and Untapped. The Untapped segment held the largest market revenue share of approximately 74.1% in 2025 driven by its extensive use in standard office printing, copying, educational materials, and commercial document production. Its broad compatibility with printers and copiers, combined with ease of handling and lower cost, continues to support strong demand across end-use sectors.

The Taped segment is projected to register the fastest growth at a CAGR of 3.8% from 2026 to 2033, driven by increasing utilization in engineering drawings, large-format printing, architectural documentation, and specialized technical applications. Growing demand for organized document management and continuous-feed printing systems is contributing to segment growth.

- By Application

On the basis of application, the reprographic paper market is segmented into Catalogues, Magazines, Architectural Designs, and Others. The Magazines segment held the largest market revenue share of approximately 36.8% in 2025 driven by continuous demand from publishing companies, advertising agencies, and commercial printing firms. High-volume magazine production and marketing publications continue to generate significant consumption of reprographic paper despite increasing digital media adoption.

The Architectural Designs segment is projected to register the fastest growth at a CAGR of 4.2% from 2026 to 2033, driven by increasing construction activities, infrastructure development projects, and demand for large-format technical drawings. Growing investments in urban development and engineering projects are accelerating the use of reprographic paper for blueprinting and design documentation applications.

Reprographic Paper Market Regional Analysis

North America Reprographic Paper Market Insight

North America dominated the reprographic paper market with the largest revenue share of 35.84% in 2025, supported by strong demand from corporate offices, educational institutions, government agencies, and commercial printing facilities. Despite increasing digitalization, the region continues to generate significant demand for printing and copying paper due to extensive documentation requirements, regulatory recordkeeping, and business communication activities. The presence of established paper manufacturers, advanced printing infrastructure, and growing adoption of sustainable paper products further supports market growth across the region.

U.S. Reprographic Paper Market Insight

The U.S. reprographic paper market captured the largest revenue share in 2025 within North America, fueled by substantial paper consumption across offices, educational institutions, legal services, healthcare organizations, and commercial printing companies. Businesses continue to rely on printed materials for contracts, reports, invoices, and administrative documentation. The growing demand for recycled and certified sustainable paper products, combined with investments in advanced paper manufacturing technologies, is further contributing to market expansion across the country.

Europe Reprographic Paper Market Insight

The Europe reprographic paper market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by increasing demand for environmentally sustainable paper products and strong regulatory support for responsible forestry and recycling practices. Businesses and public institutions across the region are adopting certified and recycled paper products to align with sustainability objectives. The presence of a mature publishing industry and growing demand for premium printing applications continue to support market development throughout Europe.

U.K. Reprographic Paper Market Insight

The U.K. reprographic paper market is expected to witness the fastest growth rate from 2026 to 2033, driven by sustained demand from educational institutions, government organizations, and commercial printing companies. The country's emphasis on sustainable procurement policies and recycled paper usage is encouraging adoption of environmentally friendly reprographic paper products. In addition, continued demand for educational materials, publishing applications, and office documentation is expected to support market growth.

Germany Reprographic Paper Market Insight

The Germany reprographic paper market is expected to witness the fastest growth rate from 2026 to 2033, fueled by the country's strong industrial base, advanced paper manufacturing sector, and growing focus on sustainable production practices. Germany remains one of Europe's leading consumers and producers of paper products, supporting demand across commercial printing, publishing, and business applications. The increasing adoption of recycled paper and resource-efficient manufacturing technologies is further strengthening market expansion.

Asia-Pacific Reprographic Paper Market Insight

The Asia-Pacific reprographic paper market is expected to witness the fastest growth rate from 2026 to 2033, supported by expanding educational infrastructure, increasing literacy rates, rapid urbanization, and growing business activities across developing economies. Rising office paper consumption and growing demand for printed educational materials in countries such as China, India, and Japan are contributing significantly to market growth. Furthermore, the region's expanding paper manufacturing capacity and cost-competitive production capabilities are strengthening its market position.

Japan Reprographic Paper Market Insight

The Japan reprographic paper market is expected to witness the fastest growth rate from 2026 to 2033 due to the country's strong publishing industry, advanced printing technologies, and continued demand for high-quality paper products. Japanese consumers and businesses place significant emphasis on print quality and documentation standards, supporting stable demand for reprographic paper. The increasing adoption of environmentally sustainable paper products and efficient paper recycling systems is also contributing to market growth.

China Reprographic Paper Market Insight

The China reprographic paper market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country's large educational sector, extensive manufacturing base, and rapidly growing commercial activities. China remains one of the world's largest producers and consumers of paper products, generating substantial demand for printing, copying, publishing, and office applications. The expansion of educational institutions, increasing business documentation requirements, and continued investments in modern paper production facilities are key factors propelling the market in China.

Reprographic Paper Market Share

The Reprographic Paper industry is primarily led by well-established companies, including:

• Domtar Corporation (U.S.)

• NIPPON PAPER INDUSTRIES CO., LTD. (Japan)

• Sappi Europe SA (Belgium)

• Reprotech Co. Ltd. (Japan)

• Asian Reprographics Private Limited. (India)

• Zauba Technologies & Data Services Private Limited. (India)

• AXIS VERSATILE SDN. BHD. (Malaysia)

• Ebul Packaging Pty Ltd (Australia)

• Longyouxian Jinlong Paper Co., Ltd. (China)

• Kaily Packaging Pte Ltd (Singapore)

• FORLIT, A.S. (Czech Republic)

• Stora Enso (Finland)

• Mayr-Melnhof Karton AG (Austria)

• Packaging Corporation of America (U.S.)

• Amcor plc (Switzerland)

• Mondi (U.K.)

• Sappi (South Africa)

• Sonoco Products Company (U.S.)

Latest Developments in Reprographic Paper Market

- In February 2026, Stora Enso, Product Launch, introduced a next-generation low-carbon reprographic paper portfolio manufactured using renewable energy and sustainably sourced fiber. The development is aimed at reducing the environmental footprint of office and commercial printing while supporting corporate sustainability goals. The launch strengthens the company's position in the premium sustainable paper segment and accelerates the industry's transition toward greener printing solutions.

- In September 2025, Domtar Corporation, Capacity Expansion, announced investments to enhance production efficiency and increase output of high-quality reprographic paper products across its North American operations. The initiative is expected to improve supply reliability, meet growing institutional demand, and strengthen the company's competitive presence in the commercial printing and office paper market.

- In June 2024, NIPPON PAPER INDUSTRIES CO., LTD., Product Development, launched an advanced recycled reprographic paper range featuring improved brightness and print performance. The new product line supports environmentally responsible printing practices while maintaining high operational efficiency, helping expand adoption of recycled paper across corporate and educational sectors.

- In March 2024, Sappi Europe SA, Sustainability Initiative, expanded its certified sustainable paper portfolio by increasing the use of responsibly sourced fiber and resource-efficient manufacturing processes. The initiative enhances product appeal among environmentally conscious customers and supports growing demand for certified paper products across Europe's printing and publishing industries.

- In July 2023, Mondi, Product Launch, introduced a lightweight reprographic paper manufactured from FSC-certified raw materials. The product was designed to reduce material consumption and environmental impact in high-volume printing applications while maintaining print quality and durability. The launch reinforced sustainable sourcing practices and supported increasing market demand for eco-friendly printing solutions.

- In October 2022, Sonoco Products Company, Strategic Investment, invested in advanced paper processing and packaging technologies to improve production efficiency and paper quality. The development enhanced operational capabilities, strengthened product competitiveness, and supported the growing requirement for high-performance paper products across commercial and industrial printing applications.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Reprographic Paper Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Reprographic Paper Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Reprographic Paper Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.