Global Restless Leg Syndrome Market

Market Size in USD Million

USD

691.55 Million

USD

1,038.20 Million

2024

2032

USD

691.55 Million

USD

1,038.20 Million

2024

2032

| 2025 - 2032 | |

| USD 691.55 Million | |

| USD 1,038.20 Million | |

| % | |

|

Restless Leg Syndrome Market Size

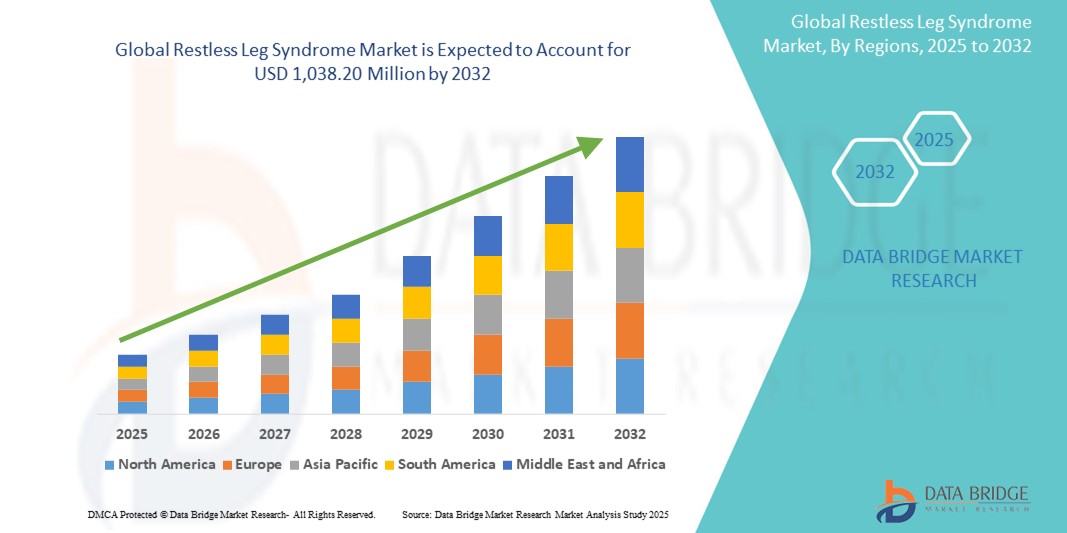

- The Global Restless Leg Syndrome Market size was valued at USD 691.55 million in 2024 and is expected to reach USD 1,038.20 million by 2032, at a CAGR of 5.21% during the forecast period

- Market growth is primarily driven by the increasing awareness and diagnosis of RLS, along with rising geriatric population and associated neurological conditions that contribute to the disorder

- In addition, the availability of pharmacological therapies such as dopaminergic agents and anti-seizure medications, combined with advancements in non-pharmacological treatment approaches, are expanding treatment accessibility and patient outcomes. These factors are collectively enhancing market adoption and driving steady expansion in the RLS treatment landscape

Restless Leg Syndrome Market Analysis

- Restless Legs Syndrome (RLS), a neurological disorder characterized by an uncontrollable urge to move the legs, is gaining medical and commercial attention due to its impact on sleep quality and daily functioning, particularly among the elderly and individuals with chronic health conditions such as diabetes and kidney disease

- The rising prevalence of primary and secondary RLS, increased awareness among healthcare providers and patients, and growing accessibility to effective pharmacological treatments such as dopaminergic agents, anti-seizure medications, and opioids are fueling demand for targeted therapies and clinical intervention

- North America dominates the global RLS market with the largest revenue share 41.6% in 2025, attributed to a well-established healthcare infrastructure, high diagnosis rates, greater awareness, and the presence of leading pharmaceutical companies. The United States, in particular, shows strong demand for both branded and generic drug formulations, supported by favorable reimbursement frameworks and clinical guidelines

- Asia-Pacific is projected to be the fastest-growing region in the RLS market during the forecast period due to rising geriatric population, increasing healthcare access, and growing awareness about neurological disorders across emerging economies like India and China

- Pharmacological therapies are expected to remain the dominant therapy type, accounting for a significant market share 76.4% in 2025, due to the availability of effective medications and continued R&D investment in drug development targeting dopamine pathways and central nervous system regulation

Report Scope and Restless Leg Syndrome Market Segmentation

|

Attributes |

Restless Leg Syndrome Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Restless Leg Syndrome Market Trends

“Shift Toward Personalized and Non-Dopaminergic Therapies”

- A significant trend shaping the global Restless Legs Syndrome (RLS) market is the growing transition from dopaminergic agents toward personalized and non-dopaminergic treatment options, driven by increasing awareness of drug-induced augmentation and long-term safety concerns

- For instance, XenoPort’s Horizant® (gabapentin enacarbil), a non-dopaminergic treatment, has gained wider acceptance in the U.S. due to its sustained efficacy and lower risk of augmentation compared to dopamine agonists

- Similarly, research into iron-based therapies for patients with low ferritin levels has expanded, with injectable iron sucrose and ferric carboxymaltose emerging as effective alternatives in treatment-resistant cases

- Moreover, neuromodulation devices, such as the Relaxis Pad, approved by the FDA, offer non-pharmacological relief by providing vibratory counter-stimulation to reduce symptoms and improve sleep quality

- Digital health is also becoming relevant, with platforms like SleepScore Labs offering symptom tracking and teleconsultations tailored to RLS management

- This shift toward individualized care, non-invasive options, and smart monitoring tools is rapidly transforming the therapeutic landscape for RLS patients.

Restless Leg Syndrome Market Dynamics

Driver

“Growing Disease Burden and Expanding Diagnostic Capabilities”

- The rising prevalence of RLS among aging populations and individuals with comorbid conditions such as diabetes, end-stage renal disease (ESRD), and anemia is a key market driver

- For instance, studies indicate that up to 30% of dialysis patients exhibit RLS symptoms, significantly affecting their quality of life and increasing healthcare visits, which is pushing for more aggressive screening and therapy

- In 2023, the Restless Legs Syndrome Foundation launched global awareness initiatives, including the “Stop the Twitch” campaign to promote earlier diagnosis and demystify RLS symptoms, particularly among general practitioners

- Additionally, the growing inclusion of RLS modules in sleep disorder diagnostic tools, such as polysomnography units and IRLSSG diagnostic criteria, is standardizing evaluation protocols across regions

- Pharmaceutical companies such as GlaxoSmithKline and Teva Pharmaceuticals are also investing in physician outreach programs and continuing medical education (CME) courses to encourage appropriate RLS diagnosis and management

- These developments are significantly expanding the diagnosed patient pool and enabling earlier treatment intervention

Restraint/Challenge

“Underdiagnosis, Limited Awareness, and Treatment Side Effects”

- A major challenge hindering the RLS market is widespread underdiagnosis, driven by misattribution of symptoms to aging, anxiety, or other sleep disorders. Many primary care providers lack specialized training in recognizing RLS symptoms, particularly in mild or intermittent cases

- For instance, a 2022 European Sleep Research Society survey found that nearly 40% of general practitioners failed to identify RLS symptoms accurately, highlighting the diagnostic gap

- Even when diagnosed, treatment with dopaminergic agents such as pramipexole or ropinirole often leads to augmentation, where symptoms worsen or spread to other body parts over time

- Case reports have shown that up to 70% of patients on long-term dopaminergic therapy experience some form of augmentation, leading to frequent medication switches or dose adjustments

- Additionally, opioid-based therapies such as methadone or oxycodone-naloxone (Targin®), while effective, raise regulatory concerns related to dependency, especially in regions like the U.S. amidst ongoing opioid control efforts

- The lack of standardized guidelines in many countries and minimal R&D into disease-modifying treatments further limits innovation and patient outcomes

- Tackling these issues will require global educational initiatives, development of augmentation-free drugs, and greater investment in public-private partnerships to improve therapeutic innovation.

Restless Leg Syndrome Market Scope

The market is segmented on the basis of type, therapy type, treatment type, drug class, route of administration, and end user.

- By Type

On the basis of type, the RLS market is segmented into Primary Restless Legs Syndrome and Secondary Restless Legs Syndrome. The Primary RLS segment holds the largest market revenue share of 61.4% in 2025, driven by its chronic, idiopathic nature and higher prevalence among middle-aged and elderly individuals. This type typically requires long-term management, resulting in consistent demand for symptom-relieving therapies

The Secondary RLS segment is expected to register the fastest growth rate of 6.3% CAGR from 2025 to 2032, fueled by the increasing incidence of contributing conditions such as iron deficiency anemia, end-stage renal disease, and pregnancy-related RLS, particularly in emerging markets where these comorbidities are more common

- By Therapy Type

Based on therapy type, the market is divided into Pharmacological Therapies and Non-Pharmacological Therapies. Pharmacological Therapies dominated the market in 2025 with largest market share owing to widespread clinical reliance on dopaminergic agents, anti-seizure medications, and opioids for symptom management.

Non-Pharmacological Therapies, including physical therapy, pneumatic compression devices, and behavioral interventions, are expected to witness increased adoption, growing at fastest CAGR as healthcare providers seek augmentation-free and side-effect-minimizing alternatives.

- By Treatment Type

The market is segmented into Medication and Surgery. Medication accounted for the largest market with largest share 2025, driven by its non-invasive nature and broad availability of approved drug classes.

Surgical interventions, though limited in use, are gaining attention in cases of medication-resistant RLS and are expected to grow moderately, particularly in developed healthcare systems with access to neuromodulation options

- By Drug Class

The drug class segment includes Dopaminergic Agents, Anti-Seizure Agents, Benzodiazepines, Opioids, and Others. Dopaminergic Agents led the market in 2025 with largest market share as they remain the first-line treatment for many moderate to severe RLS cases.

The Anti-Seizure Agents segment is expected to grow at the fastest CAGR, driven by the increasing use of gabapentin and pregabalin for their favorable side-effect profile and reduced risk of augmentation

• By Route of Administration

The market is segmented into Oral and Injectable routes. Oral administration held the dominant share in 2025, due to ease of use, better patient compliance, and availability in both branded and generic formulations.

Injectable therapies are primarily used for iron supplementation and in hospital settings for patients with severe symptoms or underlying conditions such as anemia or ESRD.

• By End User

End users in the market include Hospitals, Homecare, Specialty Clinics, and Others. Hospitals accounted for the largest revenue share in 2025, due to their role in diagnosis, complex case management, and administration of injectable therapies.

Specialty Clinics are expected to grow at the fastest CAGR. driven by an increase in sleep disorder clinics and neurology centers that focus on chronic RLS treatment plans.

Restless Leg Syndrome Market Regional Analysis

- North America dominates the global Restless Legs Syndrome (RLS) market with the largest revenue share of 41.6% in 2025, driven by a rising prevalence of neurological and sleep-related disorders, growing awareness among patients and healthcare professionals, and the availability of a wide range of effective treatment options

- Consumers in the region, particularly in the U.S., highly value early diagnosis, access to specialty care, and availability of FDA-approved therapies such as dopaminergic agents, anti-seizure medications, and iron supplements

- This widespread adoption is further supported by strong healthcare infrastructure, high healthcare spending, increasing investment in neurological research, and active advocacy by organizations like the Restless Legs Syndrome Foundation. These factors collectively reinforce North America’s position as the leading region for RLS diagnosis, treatment, and innovation

U.S. Restless Leg Syndrome Market Insight

The U.S. Restless Legs Syndrome (RLS) market captured the largest revenue share of 81% within North America in 2025, driven by increased public awareness, availability of FDA-approved treatments, and rising consultations for sleep-related and neurological disorders. The strong presence of specialty sleep centers and neurologists has contributed to higher diagnosis and treatment rates.

The growing prevalence of chronic conditions such as diabetes and end-stage renal disease (ESRD), both linked to secondary RLS, further supports the market. Additionally, patient advocacy initiatives by organizations like the Restless Legs Syndrome Foundation have improved disease visibility and early screening. Pharmaceutical companies such as Jazz Pharmaceuticals and Teva Pharmaceuticals continue to invest in extended-release formulations and combination therapies to meet evolving treatment needs

Europe Restless Leg Syndrome Market Insight

The European RLS market is projected to expand at a substantial CAGR throughout the forecast period, supported by aging populations, growing diagnosis rates of sleep and movement disorders, and a robust public healthcare infrastructure that facilitates access to neurological care.

Regulatory harmonization and widespread coverage under national health insurance programs enable patients in countries like Germany, France, and Italy to access pharmacological and non-pharmacological therapies.

Furthermore, increased investment in clinical research and public health campaigns has elevated physician awareness and diagnostic confidence. The market is seeing growth across hospital neurology departments and specialty sleep clinics, particularly in urban centers.

U.K. Restless Leg Syndrome Market Insight

The U.K. RLS market is anticipated to grow at a noteworthy CAGR over the forecast period, driven by the National Health Service (NHS) initiatives to improve diagnosis and treatment of sleep disorders.

Rising concerns about sleep deprivation and mental health are encouraging primary care providers to screen for conditions like RLS more frequently. In parallel, the growing elderly population and higher prevalence of iron-deficiency-related RLS are expanding the patient base.

The U.K. also benefits from research partnerships between academic institutions and pharmaceutical companies aimed at developing safer, augmentation-free medications.

Germany Restless Leg Syndrome Market Insight

The German RLS market is expected to expand at a considerable CAGR, supported by strong clinical expertise in neurology and sleep medicine. Germany’s advanced diagnostic infrastructure and patient education programs have enabled early intervention and effective disease management.

The country also sees active participation in global RLS clinical trials, and companies like Boehringer Ingelheim and Novartis AG operate local branches that enhance drug availability.

A strong emphasis on digital health tools—such as mobile apps for symptom tracking and medication adherence—is further fueling treatment engagement in Germany’s urban healthcare systems.

Asia-Pacific Restless Leg Syndrome Market Insight

The Asia-Pacific RLS market is projected to grow at the fastest CAGR of over 7.5% in 2025, driven by rising healthcare investments, increased life expectancy, and expanding awareness of neurological and sleep-related conditions.

Countries like India, China, and Japan are witnessing a surge in RLS diagnosis due to urbanization, improved healthcare access, and increased patient education.

Governments in the region are also promoting sleep health as part of national wellness campaigns, while domestic pharmaceutical companies are boosting affordability and availability of generic dopaminergic and anti-seizure agents.

Japan Restless Leg Syndrome Market Insight

Japan’s RLS market is gaining traction due to the country’s rapidly aging population, high prevalence of chronic diseases, and advanced healthcare system. The integration of RLS management into geriatrics and internal medicine has improved early detection rates. Japanese researchers are exploring the link between iron metabolism and RLS, driving innovation in non-dopaminergic therapies.

Additionally, the demand for patient-friendly treatments such as once-daily dosing and low-augmentation formulations is growing. Digital health platforms offering sleep monitoring are also being adopted, especially among tech-savvy and health-conscious older adults.

China Restless Leg Syndrome Market Insight

The China RLS market accounted for the largest revenue share in Asia-Pacific in 2025, fueled by rapid urbanization, increased awareness of sleep health, and healthcare reforms promoting access to neurological care.

The country’s large undiagnosed population presents a significant opportunity for pharmaceutical companies offering affordable generics and telehealth-enabled diagnostics.

Major Chinese healthcare providers are incorporating RLS screening into sleep clinics, while digital platforms like Ping An Good Doctor and WeDoctor are helping patients access care remotely. The rise of local manufacturing capabilities for dopaminergic and anti-seizure agents is further strengthening China’s position in the regional RLS market.

Restless Leg Syndrome Market Share

The Restless Leg Syndrome industry is primarily led by well-established companies, including:

- GlaxoSmithKline plc (U.K.)

- Ligand Pharmaceuticals Incorporated (U.S.)

- Jazz Pharmaceuticals, Inc. (U.S.)

- Hisamitsu Pharmaceutical Co., Inc. (Japan)

- Intas Pharmaceuticals Ltd (India)

- Serina Therapeutics (U.S.)

- Apotex Inc (Canada)

- Teva Pharmaceutical Industries Ltd (Israel)

- Mylan N.V. (U.S.)

- Glenmark Pharmaceuticals Ltd (India)

- Sun Pharmaceutical Industries Ltd (India)

- Endo Pharmaceuticals Inc. (U.S.)

- Novartis AG (Switzerland)

- Aurobindo Pharma (India)

- Zydus Cadila (India)

- Dr. Reddy’s Laboratories Ltd (India)

- Alembic Pharmaceuticals Limited (India)

- Macleods Pharmaceuticals Ltd (India)

- Unichem Laboratories (India)

- Boehringer Ingelheim International GmbH (Germany)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.