Global Retinitis Pigmentosa Treatment Market

Market Size in USD Billion

USD

12.60 Billion

USD

24.10 Billion

2024

2032

USD

12.60 Billion

USD

24.10 Billion

2024

2032

| 2025 - 2032 | |

| USD 12.60 Billion | |

| USD 24.10 Billion | |

| % | |

|

Retinitis Pigmentosa Treatment Market Size

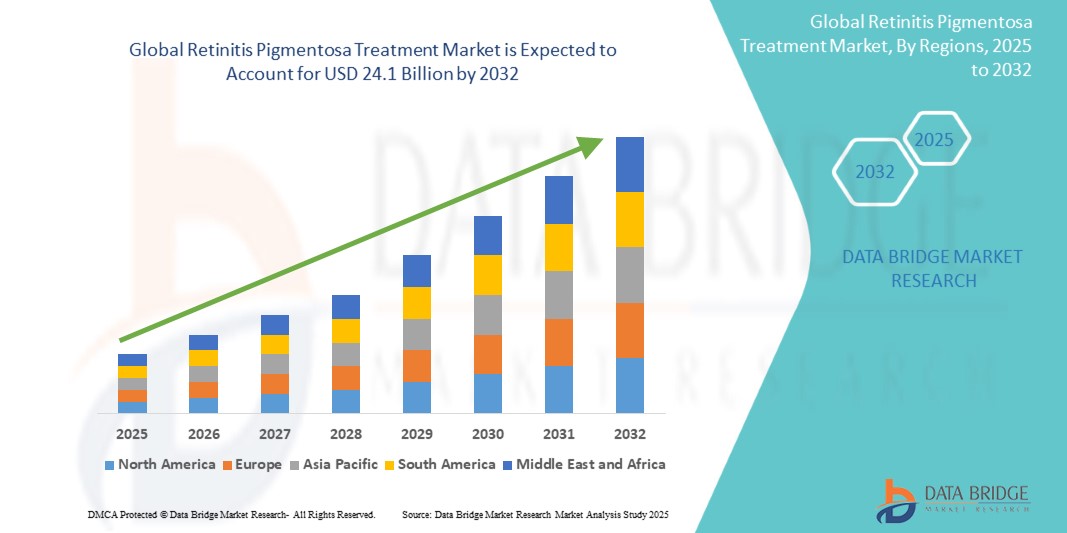

- The global retinitis pigmentosa treatment Market size was valued at USD 12.6 billion in 2024 and is expected to reach USD 24.1 billion by 2032, at a CAGR of 7.5% during the forecast period

- This growth is fueled by increasing advancements in gene therapy, rising prevalence of inherited retinal disorders, growing awareness of early diagnosis, and expanding research funding in ophthalmic diseases

Retinitis Pigmentosa Treatment Market Analysis

- Retinitis pigmentosa (RP) is a group of rare, inherited eye disorders that involve a breakdown and loss of cells in the retina, ultimately leading to progressive vision loss. The market for RP treatment is expanding rapidly due to innovations in therapeutic strategies such as gene therapy, retinal implants, stem cell therapy, and vitamin supplementation

- A significant driver for this market is the growing investment in genetic testing and personalized medicine, which is enabling earlier diagnosis and more targeted treatment approaches. The increasing availability of advanced diagnostic tools like electroretinograms and genetic screening is further enhancing disease management and prognosis

- North America currently holds the largest share of the global retinitis pigmentosa treatment market, accounting for 38.2%, owing to a well-established healthcare infrastructure, strong presence of leading biotech firms, favorable reimbursement policies, and a high rate of adoption of novel therapies such as Luxturna (voretigene neparvovec)

- Asia-Pacific is projected to witness the fastest growth in the global retinitis pigmentosa treatment market throughout the forecast period, driven by increasing awareness campaigns, improvement in genetic testing capabilities, and the growing number of patients opting for treatment in emerging economies like China and India

- The autosomal recessive segment is projected to hold the largest share in 2025, driven by its higher prevalence among RP cases globally. Autosomal recessive RP accounts for a significant portion of diagnosed cases due to the inheritance pattern involving both parents. This form often presents early in life and tends to be more severe, resulting in a greater need for early diagnosis and intervention. Ongoing genetic screening initiatives and rising awareness of hereditary eye disorders are contributing to the increased detection of autosomal recessive RP, further propelling the growth of this segment.

Report Scope and Retinitis Pigmentosa Treatment Market Segmentation

|

Attributes |

Retinitis Pigmentosa Treatment Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Retinitis Pigmentosa Treatment Market Trends

“Rising Focus on Gene Therapy and Precision Medicine”

- One prominent trend in the retinitis pigmentosa (RP) market is the increasing adoption of gene therapy and precision medicine approaches

- The growing recognition of RP as a genetically heterogeneous disorder has led to a surge in research focused on targeted, mutation-specific treatment strategies

- For instance, Spark Therapeutics' Luxturna (voretigene neparvovec), approved by the FDA, is the first gene therapy for an inherited retinal disease, offering long-term vision improvement in patients with RPE65 mutations

- This trend is transforming the RP treatment paradigm by shifting the focus from symptomatic relief to root-cause intervention, promising durable therapeutic benefits

- As more gene therapies progress through clinical trials and gain regulatory approval, the market is expected to grow substantially, especially in regions with advanced genomic infrastructure

- Overall, this trend supports a move toward earlier intervention, personalized treatment plans, and improved patient outcomes in RP care

Retinitis Pigmentosa Treatment Market Dynamics

Driver

“Growing Technological Advancements in Retinal Therapies”

- Advancements in retinal imaging, genetic testing, and therapeutic delivery methods are significantly boosting the global Global Retinitis Pigmentosa Treatment Market

- Innovations such as adeno-associated virus (AAV) vectors for gene therapy, retinal prosthetic devices (like the Argus II retinal implant), and CRISPR gene editing tools are enhancing treatment efficacy and expanding the range of treatable RP mutations

- These technological improvements allow for earlier diagnosis, better disease monitoring, and the possibility of halting or even reversing vision loss in select patients

For instance,

- Researchers are developing optogenetic therapies that can restore light sensitivity to retinal cells, representing a new frontier in RP treatment.

- The availability of non-invasive imaging tools such as optical coherence tomography (OCT) and fundus autofluorescence has also improved the early detection and monitoring of RP progression

- With continued R&D and clinical translation, these innovations are expected to drive robust market growth and elevate the standard of care in inherited retinal diseases

Opportunity

“Increased Research Funding and Global Collaborations”

- The rising investment in rare disease research and global collaboration initiatives presents significant growth opportunities for the RP market

- Public and private sector funding is accelerating the development of breakthrough therapies, while international research consortia are pooling genomic data to uncover new treatment targets

For instance,

- The Foundation Fighting Blindness has committed over $100 million in funding toward RP research, supporting gene therapy trials, stem cell innovations, and retinal implants.

- Cross-border partnerships between biotech companies, academic institutions, and regulatory bodies are speeding up the clinical development and commercialization of RP therapies

- Such collaborations enhance access to advanced diagnostics and treatments across different geographies, expanding the market footprint and improving patient access to care

- The growing global interest in orphan diseases is likely to sustain momentum and bring more RP-specific therapies to market

Restraint/Challenge

“High Cost and Limited Access to Advanced Treatments”

- A major challenge facing the RP market is the high cost of advanced therapeutic options, which limits accessibility—especially in low- and middle-income countries

- Treatments such as gene therapies, retinal implants, and specialized diagnostics are often priced at premium levels, placing them out of reach for many healthcare systems and patients

For instance,

- Luxturna is priced at over USD 850,000 per treatment course in the U.S., making affordability a key barrier to widespread adoption

- Moreover, limited infrastructure for genetic testing and specialized care further hinders early diagnosis and intervention in underserved regions

- The lack of reimbursement policies for rare disease treatments in many countries exacerbates this problem, leading to disparities in patient outcomes

- Addressing cost and accessibility issues through public health programs, patient assistance schemes, and localized manufacturing could help unlock untapped market potential and ensure more equitable care

Retinitis Pigmentosa Treatment Market Scope

The market is segmented on the basis of type, treatment, route of administration, end-users and distribution channel.

|

Segmentation |

Sub-Segmentation |

|

By Type |

|

|

By Treatment |

|

|

By Route of Administration |

|

|

By End-Users |

|

|

By Distribution Channel |

|

In 2025, the Autosomal Recessive segment is projected to dominate the market with the largest share in the Type segment

The Autosomal Recessive segment is expected to dominate the global retinitis pigmentosa treatment market with the largest share of 38.6% in 2025, attributed to its higher prevalence and earlier disease onset compared to other forms. This type is more frequently diagnosed due to its severe progression and is a major target for emerging gene therapies and clinical trials.

Despite advancements in autosomal dominant and X-linked treatment pipelines, autosomal recessive RP remains the most clinically significant form, driving higher patient volume and treatment demand. As genetic screening becomes more accessible, earlier and more accurate diagnoses are expected to further reinforce the dominance of this segment.

The Oral segment is expected to account for the largest share during the forecast period in the route of administration segment

The oral segment is expected to dominate the market with 41.2% share in 2025, attributed to its convenience, ease of administration, and higher patient compliance.

Oral therapies are particularly preferred for long-term management of RP symptoms, especially antioxidant and neuroprotective agents. With a growing emphasis on non-invasive treatment approaches, the demand for orally administered drugs is expanding. Additionally, advancements in oral drug formulations designed to cross the blood-retinal barrier efficiently are supporting the continued dominance of this route.

Retinitis Pigmentosa Treatment Market Regional Analysis

“North America Holds the Largest Share in the Retinitis Pigmentosa Treatment Market”

- North America dominates the Global retinitis pigmentosa treatment market with a share of 39.1%, supported by a strong genetic research ecosystem, advanced healthcare infrastructure, and high adoption of novel therapies, including gene therapy and retinal implants

- The United States holds a significant regional share of 81.7%, driven by the high prevalence of inherited retinal disorders, favorable regulatory pathways for orphan drugs, and the presence of leading biotech firms such as Spark Therapeutics, AGTC, and Editas Medicine

- The growing number of clinical trials and early approvals for gene therapies—such as Luxturna—have reinforced the U.S.’s leading role in retinitis pigmentosa treatment innovation. Widespread awareness, coupled with supportive reimbursement structures, has fueled patient access to emerging therapies

- Increasing investment in ophthalmic drug development, government support for rare disease research, and patient advocacy group activity have further solidified North America’s leading position in the global Global Retinitis Pigmentosa Treatment Market

“Asia-Pacific is Projected to Register the Highest CAGR in the Retinitis Pigmentosa Treatment Market”

- The Asia-Pacific region is expected to register the highest CAGR during the forecast period, driven by improving healthcare infrastructure, increasing access to genetic testing, and a rising focus on rare disease management across emerging economies

- Countries like China, India, and South Korea are becoming high-growth zones due to large patient populations, expanding retinal disease awareness programs, and the growing availability of advanced diagnostics such as electroretinograms and genetic screening

- Japan, with its robust research capabilities and government support for innovative therapies, continues to lead in early adoption of gene and regenerative therapies for retinal disorders. Japanese firms are also actively engaged in RP-related clinical trials, further boosting the region’s role in treatment development

- The increasing number of ophthalmic centers, favorable regulatory reforms for orphan drugs, and growing investment in biotech innovation are expected to significantly accelerate market growth in APAC, making it the fastest-growing region in the Global Global Retinitis Pigmentosa Treatment Market

Retinitis Pigmentosa Treatment Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Bausch Health Companies Inc. (Canada)

- Novartis AG (Switzerland)

- Sun Pharmaceutical Industries Ltd. (India)

- Allergan (Ireland)

- Astellas Pharma Inc. (Japan)

- AstraZeneca (UK)

- Johnson & Johnson Private Limited (US)

- Orphagen Pharmaceuticals, Inc (US)

- Clino Corporation (Japan)

- Spark Therapeutics, Inc (US)

- Caladrius Biosciences, Inc. (US)

- Genethon (France)

- Gensight Biologics(France)

- Grupo Ferrer International, S.A. (Spain)

- Nanovector S.r.l (Italy)

- Mimetogen Pharmaceuticals Inc. (Canada)

- Ionis Pharmaceuticals, Inc. (US)

- AGTC (US)

- MeiraGTx Limited (US)

- ReNeuron Group plc (UK)

- ProQR Therapeutics. (Netherlands)

Latest Developments in Retinitis Pigmentosa treatment market

- In January 2022, 4D Molecular Therapeutics announced that the U.S. Food and Drug Administration (FDA) has granted the fast-track designation to 4D-125 which is used to treat X-linked retinitis pigmentosa. 4D-125 is a targeted and evolved R100-based product candidate meant to deliver a functional copy of the RPGR gene to photoreceptors in the retina. It was invented at 4DMT for efficient intravitreal delivery

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.