Global Rhabdomyolysis Treatment Market

Market Size in USD Billion

USD

3.30 Billion

USD

4.48 Billion

2024

2032

USD

3.30 Billion

USD

4.48 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.30 Billion | |

| USD 4.48 Billion | |

| % | |

|

Rhabdomyolysis Treatment Market Size

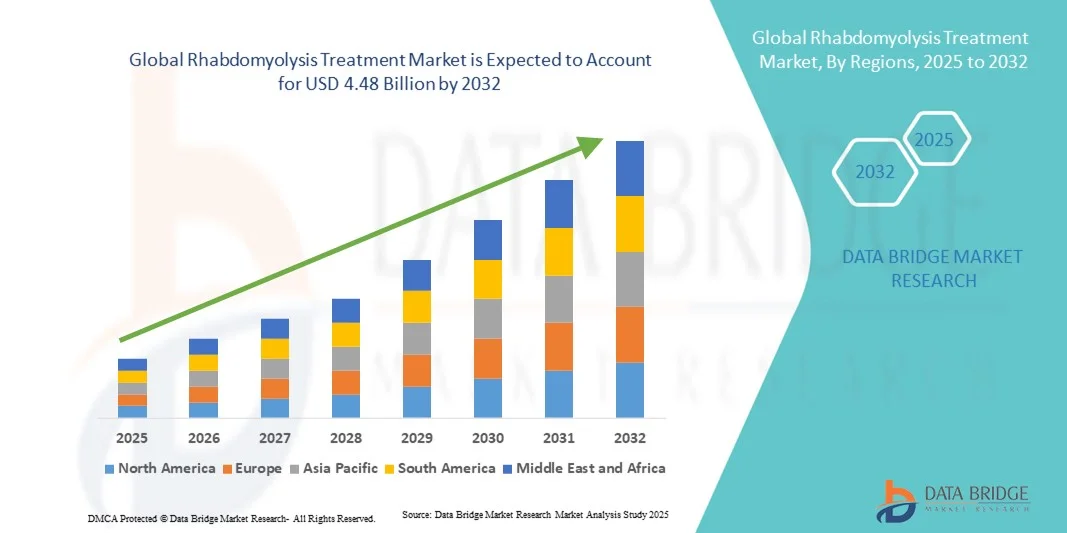

- The global rhabdomyolysis treatment market size was valued at USD 3.30 billion in 2024 and is expected to reach USD 4.48 billion by 2032, at a CAGR of 3.90% during the forecast period

- The market growth is largely fueled by the increasing prevalence of traumatic injuries, drug toxicity, and crush syndromes that lead to muscle breakdown, driving the demand for effective rhabdomyolysis treatment options. Advancements in diagnostic technologies and increased clinical awareness among healthcare professionals have further supported early detection and improved patient outcomes

- Furthermore, rising government healthcare spending, improved access to emergency and critical care services, and ongoing pharmaceutical research focused on renal protection therapies are accelerating the adoption of rhabdomyolysis treatment solutions, thereby significantly boosting the market’s growth

Rhabdomyolysis Treatment Market Analysis

- Rhabdomyolysis Treatment, encompassing medical approaches to manage muscle breakdown and prevent kidney damage, is becoming increasingly vital in modern healthcare due to the growing incidence of trauma, drug-induced muscle injuries, and metabolic disorders across both developed and emerging regions

- The escalating demand for effective rhabdomyolysis therapies is primarily fueled by rising awareness regarding early diagnosis, advancements in renal replacement technologies, and ongoing research efforts in pharmacological and supportive care solutions, which are collectively accelerating the market’s growth

- North America dominated the rhabdomyolysis treatment market with the largest revenue share of 38.5% in 2024, driven by a strong healthcare infrastructure and active R&D in therapeutic advancements

- Asia-Pacific is expected to be the fastest growing region in the rhabdomyolysis treatment market during the forecast period, projected to grow at a CAGR of 9.2%, owing to rising healthcare investment and increasing prevalence of exercise and drug-related muscle injuries

- The parenteral segment dominated with 57.8% revenue share in 2024, as most acute cases require immediate intravenous therapy for rapid fluid and medication delivery

Report Scope and Rhabdomyolysis Treatment Market Segmentation

|

Attributes |

Rhabdomyolysis Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Rhabdomyolysis Treatment Market Trends

Advancements in Early Diagnosis and Novel Therapeutic Approaches

- A significant and accelerating trend in the global rhabdomyolysis treatment market is the growing adoption of advanced diagnostic technologies and targeted therapies that enhance early detection and improve patient outcomes. Continuous innovation in biochemical assays, imaging tools, and point-of-care diagnostic methods is transforming clinical management by enabling faster identification of rhabdomyolysis and its complications, such as acute kidney injury

- For instance, the introduction of high-sensitivity creatine kinase (CK) assays and myoglobin-based rapid testing kits has allowed clinicians to assess muscle damage more precisely, facilitating early intervention. Similarly, advancements in imaging modalities, including MRI and ultrasound, are aiding in differentiating rhabdomyolysis from other musculoskeletal disorders

- The development of novel pharmacological and supportive treatment options—such as renal replacement therapies, antioxidants, and electrolyte stabilization protocols—has improved survival rates among patients with severe cases. For example, the increasing use of continuous renal replacement therapy (CRRT) in intensive care units is offering more effective management of myoglobin-induced nephropathy

- Furthermore, healthcare systems worldwide are focusing on multidisciplinary care models involving nephrologists, emergency physicians, and critical care specialists to ensure comprehensive management of rhabdomyolysis patients. These coordinated approaches are supported by the rising integration of electronic health records and clinical decision-support tools that assist in risk assessment and therapy optimization

- This trend towards early diagnosis, personalized care, and advanced therapeutic interventions is fundamentally reshaping treatment standards for rhabdomyolysis. Consequently, leading pharmaceutical and biotechnology companies are investing in clinical research to identify new biomarkers and therapeutic targets aimed at improving recovery and reducing long-term complications

- The growing emphasis on timely diagnosis, improved fluid resuscitation techniques, and preventive measures for at-risk populations is expected to further accelerate the development and adoption of innovative treatment solutions globally

Rhabdomyolysis Treatment Market Dynamics

Driver

Increasing Incidence of Muscle Injury and Growing Awareness of Early Treatment

- The rising prevalence of rhabdomyolysis caused by trauma, strenuous exercise, drug use, infections, and metabolic disorders is a major factor driving market growth. Growing awareness among healthcare providers regarding early recognition and intervention has led to improved diagnosis rates and increased demand for advanced treatment solutions

- For instance, in April 2024, several healthcare organizations launched awareness campaigns focusing on early identification of muscle breakdown symptoms and the importance of immediate medical attention to prevent kidney failure. Such initiatives are expected to drive the Rhabdomyolysis Treatment industry growth over the forecast period

- In addition, the rise in hospital admissions related to statin-induced rhabdomyolysis and crush injuries is boosting the need for effective management protocols. Continuous advancements in fluid therapy, renal support systems, and biochemical monitoring technologies are further propelling market expansion

- The global increase in physical training intensity, military activities, and occupational hazards associated with muscle stress is also contributing to the growing demand for rhabdomyolysis treatment. Moreover, the introduction of evidence-based clinical guidelines emphasizing early hydration and metabolic correction has enhanced treatment efficacy and improved patient outcomes

- Advancements in diagnostic precision, coupled with greater public health awareness and access to emergency medical care, are collectively driving the global Rhabdomyolysis Treatment market forward

Restraint/Challenge

Limited Awareness in Low-Income Regions and High Cost of Critical Care

- Limited disease awareness, underdiagnosis, and inadequate access to emergency healthcare services in developing countries represent key challenges for market growth. Many patients in low-resource settings fail to receive timely treatment, leading to high morbidity and mortality associated with acute renal failure secondary to rhabdomyolysis

- For instance, delayed recognition of exertional rhabdomyolysis in rural or underdeveloped regions often results in poor clinical outcomes, reflecting the urgent need for better diagnostic outreach and training programs

- Furthermore, the high cost of intensive care management, including renal replacement therapy and electrolyte monitoring, places a financial burden on healthcare systems and patients, particularly where medical reimbursement policies are limited. Hospitals and clinics in low- and middle-income countries face resource constraints that restrict the widespread adoption of advanced diagnostic and treatment options

- Addressing these challenges requires strategic investment in public health education, affordable point-of-care diagnostic technologies, and government initiatives aimed at strengthening emergency response systems

- While high-income nations continue to advance treatment technologies, bridging the accessibility gap in emerging economies remains a critical challenge for sustainable market growth. Enhancing awareness, improving training for healthcare professionals, and expanding access to cost-effective supportive care will be crucial in overcoming these barriers in the coming years

Rhabdomyolysis Treatment Market Scope

The market is segmented on the basis of cause, treatment, route of administration, end-users, and distribution channel.

- By Cause

On the basis of cause, the Rhabdomyolysis Treatment market is segmented into viral infections, bacterial infections, polymyositis, dermatomyositis, and others. The viral infections segment dominated the largest market revenue share of 41.8% in 2024, driven by the increasing incidence of viral illnesses such as influenza, Epstein–Barr virus, and COVID-19, which are known to trigger rhabdomyolysis in severe cases. Rising hospital admissions associated with viral-induced muscle damage, coupled with the availability of rapid diagnostic tools, have contributed to the segment’s dominance. Hospitals and specialty clinics emphasize early detection and supportive therapy, which further strengthens the demand. The growing prevalence of viral outbreaks globally, along with clinical awareness and standardized treatment protocols, continues to support the viral infections segment. Healthcare institutions prefer standardized interventions and monitoring, ensuring consistent outcomes and driving revenue. Strong research initiatives and funding for viral complications also reinforce this segment’s lead, while patient education campaigns about viral risks enhance market uptake.

The bacterial infections segment is expected to witness the fastest growth rate of 21.6% CAGR from 2025 to 2032, fueled by the rising burden of sepsis and bacterial-induced myositis in both developed and developing countries. Increasing cases of antibiotic-resistant bacterial infections have led to prolonged treatment courses, heightening the risk of rhabdomyolysis. The availability of advanced hospital monitoring systems and early intervention protocols accelerates adoption. Rising awareness among healthcare providers about bacterial complications, coupled with growing hospital admissions for severe bacterial infections, drives rapid segment growth. The development of novel antibiotics and treatment combinations enhances the efficacy of bacterial-related rhabdomyolysis management. Hospitals and specialty clinics increasingly adopt standardized treatment pathways to manage these cases efficiently. Government healthcare programs focusing on infectious disease management further boost the segment. Improved diagnostic tests and lab infrastructure ensure early detection and timely treatment, supporting high growth. Regional expansion in high-burden countries, alongside increasing insurance coverage, facilitates market penetration. Research funding for bacterial-induced muscle disorders and global awareness campaigns continues to propel growth.

- By Treatment

On the basis of treatment, the Rhabdomyolysis Treatment market is segmented into intravenous (IV) fluids, mannitol, loop diuretics, dialysis, surgery, and others. The intravenous (IV) fluids segment held the largest market revenue share of 46.3% in 2024, as IV fluids are considered the standard first-line therapy to prevent kidney injury in acute rhabdomyolysis cases. Hospitals widely adopt this intervention due to its availability, cost-effectiveness, and established treatment protocols. Rapid fluid resuscitation is critical for preventing renal complications, reinforcing its use across healthcare facilities. The growing prevalence of acute rhabdomyolysis in hospitalized patients ensures continuous demand. Clinical guidelines emphasize early and aggressive IV therapy, which supports dominance. The presence of skilled healthcare personnel to administer IV fluids safely enhances segment preference. High adoption in emergency care and intensive care units strengthens market leadership. Hospitals ensure consistent quality control and dosing accuracy, contributing to revenue stability. Educational initiatives for healthcare professionals on acute management further promote usage.

The dialysis segment is expected to witness the fastest CAGR of 23.4% from 2025 to 2032, driven by the increasing incidence of acute kidney injury caused by severe rhabdomyolysis. Dialysis is required for patients with life-threatening electrolyte imbalances and renal failure, creating high demand in specialized care centers. Advances in renal replacement therapy, including portable and home-based dialysis systems, expand accessibility. Rising geriatric population and prevalence of comorbidities increase segment adoption. Hospitals and specialized centers focus on timely initiation to improve patient outcomes. Integration of monitoring technologies improves treatment efficiency and safety. Government support for dialysis programs and reimbursement policies accelerates uptake. Clinical awareness of early intervention benefits fosters rapid adoption. Expansion in developing regions with growing healthcare infrastructure further drives growth. Research and innovation in dialysis technologies support continuous segment evolution.

- By Route of Administration

On the basis of route of administration, the Rhabdomyolysis Treatment market is segmented into oral, parenteral, and others. The parenteral segment dominated with 57.8% revenue share in 2024, as most acute cases require immediate intravenous therapy for rapid fluid and medication delivery. Hospitals and intensive care units rely on parenteral administration to ensure high bioavailability and swift therapeutic response. Acute management protocols prioritize parenteral delivery for electrolyte correction and kidney protection. Growing inpatient admissions and emergency cases reinforce segment dominance. Continuous monitoring and dosing precision in hospitals strengthen adoption. The segment benefits from standardized hospital guidelines and high clinician preference. Accessibility in tertiary care and specialized centers supports revenue growth. Patient outcomes improve with parenteral therapy, encouraging consistent clinical use. Healthcare infrastructure investment and medical staff expertise further boost segment performance.

The oral segment is expected to witness the fastest CAGR of 20.2% from 2025 to 2032, driven by increasing use of oral medications for mild rhabdomyolysis cases and post-discharge recovery. Oral diuretics and adjunctive therapies support home-based treatment plans. Telemedicine and remote patient monitoring facilitate safe oral therapy adoption. Rising patient preference for non-invasive routes accelerates segment growth. Availability of oral formulations and expanding pharmacy networks contribute to accessibility. Education campaigns for outpatient management enhance adoption. Growth is also supported by healthcare cost optimization efforts. Regional expansion in high-incidence areas boosts market penetration. Pharmaceutical innovation ensures better efficacy and safety profiles. Insurance coverage for outpatient treatment further drives oral segment adoption. Homecare integration and patient convenience remain key growth factors.

- By End-Users

On the basis of end-users, the Rhabdomyolysis Treatment market is segmented into clinics, hospitals, homecare, and others. The hospitals segment dominated with 49.6% revenue share in 2024, due to availability of ICU facilities, specialized nephrology departments, and advanced diagnostics. Hospitals manage acute cases and ensure continuous monitoring, ensuring optimal patient outcomes. High patient admission rates for severe rhabdomyolysis cases reinforce market share. Insurance coverage and institutional procurement policies support sustained growth. Hospitals implement standardized care protocols, which improves treatment efficacy. Integration of advanced monitoring technologies enhances patient safety. Large hospital networks and collaborations with specialty centers further consolidate dominance. Ongoing staff training and research initiatives strengthen hospital-based adoption. Awareness of renal complications ensures early intervention. Emergency care services prioritize hospitals for rapid response.

The homecare segment is expected to witness the fastest CAGR of 21.1% from 2025 to 2032, driven by increasing preference for home-based recovery, technological advancements in portable IV systems, and remote monitoring tools. Patients recovering from mild rhabdomyolysis or post-hospital discharge increasingly prefer home-based care. Telemedicine integration allows continuous clinical oversight. Expansion of home healthcare services and insurance support enhances adoption. Convenience, reduced hospital stay, and lower costs accelerate segment growth. Availability of trained homecare staff facilitates safe treatment. Pharmaceutical companies provide support programs for home administration. Rising patient awareness and comfort with self-care therapies boost growth. Growth in rural and suburban regions increases market reach. Partnerships with clinics and specialty centers enhance adoption. Digital health platforms support monitoring and adherence.

- By Distribution Channel

On the basis of distribution channel, the Rhabdomyolysis Treatment market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others. The hospital pharmacy segment dominated with 47.5% revenue share in 2024, benefiting from direct supply chains, institutional procurement, and integration with patient care protocols. Hospitals ensure continuous availability, quality control, and adherence to treatment protocols. Centralized purchasing supports cost efficiency. Professional guidance and monitoring during therapy reinforce safety. Hospitals maintain consistent inventory management and timely restocking, supporting high revenue share. Access to specialized medications and integration with clinical teams further strengthen dominance. Standardized procurement policies reduce errors and ensure treatment efficacy.

The online pharmacy segment is expected to witness the fastest CAGR of 22.4% from 2025 to 2032, driven by growing digital healthcare adoption, convenience in ordering medications, and improved logistics. Online platforms enable prescription verification, secure delivery, and better patient adherence. Expansion of e-pharmacy regulations and technological infrastructure boosts growth. Rising consumer preference for home delivery and contactless services enhances adoption. Availability of specialty and standard drugs online supports accessibility. Telemedicine consultations integrated with e-pharmacies accelerate segment growth. Wider geographical reach allows patients in remote areas to access treatments. Digital health trends and increased smartphone penetration further support adoption. Partnerships with hospitals and clinics provide a reliable supply network. Increasing awareness campaigns promote safe online medication usage.

Rhabdomyolysis Treatment Market Regional Analysis

- North America dominated the rhabdomyolysis treatment market with the largest revenue share of 38.5% in 2024, driven by a strong healthcare infrastructure, increasing awareness of rhabdomyolysis management, and active R&D in therapeutic advancements

- The presence of advanced diagnostic facilities, well-equipped hospitals, and specialized nephrology and critical care centers further supports early diagnosis and effective treatment

- High healthcare expenditure, robust insurance coverage, and growing adoption of clinical guidelines for fluid resuscitation and renal support are establishing North America as a key market for rhabdomyolysis therapies

U.S. Rhabdomyolysis Treatment Market Insight

The U.S. rhabdomyolysis treatment market captured the largest revenue share within North America in 2024, fueled by the availability of advanced diagnostic tools, adoption of evidence-based treatment protocols, and rising awareness among healthcare professionals. Increased focus on intensive care management, early intervention strategies, and renal replacement therapies is driving growth.

Europe Rhabdomyolysis Treatment Market Insight

The Europe rhabdomyolysis treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing healthcare infrastructure, growing awareness of early rhabdomyolysis detection, and rising prevalence of drug- and exercise-induced muscle injuries. Urbanization and rising demand for specialized care are fostering market growth across hospitals, specialty clinics, and rehabilitation centers.

U.K. Rhabdomyolysis Treatment Market Insight

The U.K. rhabdomyolysis treatment market is expected to grow at a noteworthy CAGR during the forecast period, supported by the country’s focus on critical care facilities, early diagnostic adoption, and educational campaigns on rhabdomyolysis management. The prevalence of sports- and medication-related cases further contributes to demand for effective therapeutic solutions.

Germany Rhabdomyolysis Treatment Market Insight

The Germany rhabdomyolysis treatment market is expected to expand at a considerable CAGR during the forecast period, driven by advanced hospital infrastructure, rising awareness of metabolic and drug-induced rhabdomyolysis, and increasing investment in therapeutic research. Germany’s strong emphasis on innovation and patient safety supports the adoption of renal replacement therapies and other advanced treatment modalities.

Asia-Pacific Rhabdomyolysis Treatment Market Insight

The Asia-Pacific rhabdomyolysis treatment market is poised to grow at the fastest CAGR of 9.2% during the forecast period, owing to rising healthcare investment, increasing prevalence of exercise- and drug-related muscle injuries, and expanding hospital infrastructure in countries such as China, Japan, and India. The region is witnessing greater availability of diagnostic tools, therapeutic protocols, and supportive care, driving overall market expansion.

Japan Rhabdomyolysis Treatment Market Insight

The Japan rhabdomyolysis treatment market is gaining momentum due to the country’s advanced healthcare system, rapid urbanization, and growing demand for early diagnosis and efficient therapeutic management. The aging population and rising prevalence of lifestyle-related and medication-induced rhabdomyolysis are expected to further boost market growth in both hospital and specialty care settings.

China Rhabdomyolysis Treatment Market Insight

The China rhabdomyolysis treatment market accounted for the largest revenue share in Asia-Pacific in 2024, attributed to rapid urbanization, rising middle-class population, increased healthcare expenditure, and government initiatives to improve critical care management. Expanding hospital infrastructure, increasing awareness among healthcare professionals, and adoption of evidence-based treatment protocols are key factors propelling market growth in China.

Rhabdomyolysis Treatment Market Share

The Rhabdomyolysis Treatment industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Johnson & Johnson and its affiliates (U.S.)

- Sanofi (France)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Bayer AG (Germany)

- AbbVie Inc. (U.S.)

- Hikma Pharmaceuticals PLC (U.K.)

- Fresenius Kabi AG (Germany)

- Amgen Inc. (U.S.)

- Lilly(U.S.)

- Bristol-Myers Squibb Company (U.S.)

- Eisai Co., Ltd. (Japan)

Latest Developments in Global Rhabdomyolysis Treatment Market

- In June 2023, a study published by Cures Within Reach explored the potential use of steroids as an off-label treatment to improve outcomes in pediatric patients with rhabdomyolysis. The research suggested that corticosteroids might offer benefits in reducing inflammation and muscle damage, though further clinical trials are needed to confirm their efficacy and safety in this context

- In March 2024, the 276th ENMC Workshop convened in Berlin, bringing together 21 experts to address the need for standardized clinical guidelines on rhabdomyolysis diagnosis and management. The workshop emphasized the importance of early detection, appropriate fluid therapy, and monitoring to prevent complications such as acute kidney injury. This initiative aims to harmonize treatment approaches and improve patient outcomes globally

- In April 2025, a comprehensive review published in the journal ScienceDirect provided updated insights into the pathogenesis, diagnosis, and treatment of rhabdomyolysis. The review highlighted advancements in understanding the condition's underlying mechanisms and emphasized the importance of timely intervention to reduce morbidity and mortality

- In September 2025, the Uniformed Services University of the Health Sciences released an updated Clinical Practice Guideline (CPG) for the management of exertional rhabdomyolysis. This guideline incorporates the latest evidence-based practices to optimize diagnosis, initial management, and return-to-duty decisions for military personnel affected by the condition

- In June 2025, the U.S. Military Health System reported a significant decline in exertional rhabdomyolysis cases among active-duty personnel. The total crude incidence rate dropped by nearly 10% compared to the peak observed in 2023, indicating improved prevention and management strategies. This reduction underscores the effectiveness of enhanced training protocols and awareness programs in mitigating the condition within military settings

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.