Global Rigid Industrial Packaging Market

Market Size in USD Billion

USD

61.19 Billion

USD

86.68 Billion

2025

2033

USD

61.19 Billion

USD

86.68 Billion

2025

2033

| 2026 - 2033 | |

| USD 61.19 Billion | |

| USD 86.68 Billion | |

| % | |

|

Rigid Industrial Packaging Market Overview

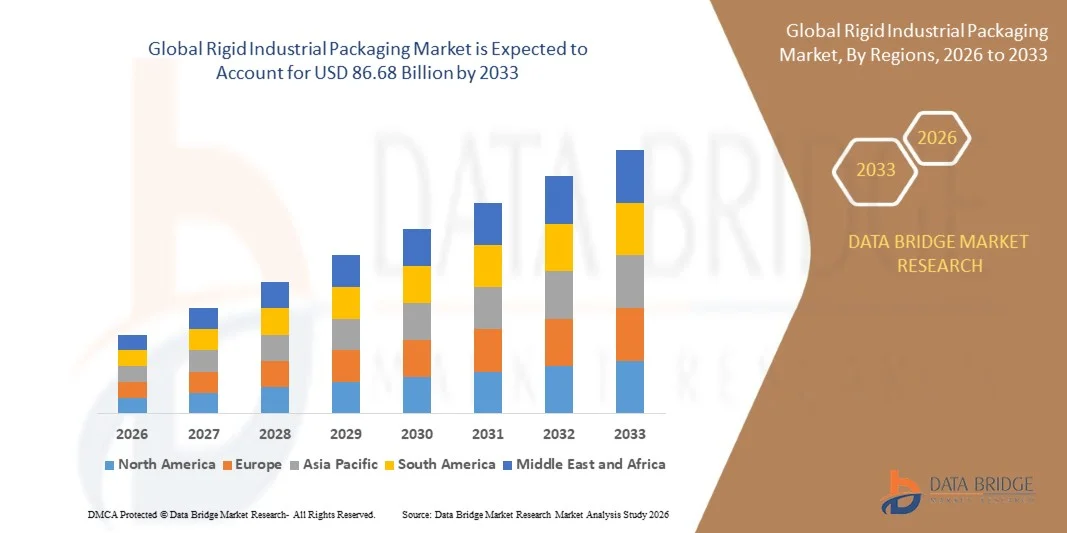

The Rigid Industrial Packaging Market was valued at USD 61.19 Billion in 2025 and is projected to reach USD 86.68 Billion by 2033, growing at a CAGR of 4.45% from 2026 to 2033. The market is experiencing consistent growth driven by rising demand for safe, durable, and efficient bulk packaging solutions across chemicals, oil and lubricants, pharmaceuticals, food and beverages, and industrial manufacturing sectors. Expanding global trade, increasing industrial production, and growing adoption of reusable and recyclable packaging formats such as drums and rigid IBCs are further supporting market expansion across developed and emerging economies.

The increasing emphasis on supply chain efficiency, product safety, and regulatory compliance in handling hazardous and sensitive materials is significantly driving demand for rigid industrial packaging solutions. In addition, the shift toward sustainable packaging practices and circular economy models is encouraging the adoption of recyclable plastics, metal containers, and reconditioned packaging systems. Advancements in material engineering, lightweight container design, and smart tracking technologies are further enhancing operational efficiency and strengthening market growth globally.

Key Market Trends & Insights

- Asia-Pacific dominated the Rigid Industrial Packaging Market with the largest revenue share of 42% in 2025, supported by large-scale manufacturing activity, strong chemical and petrochemical production, and high demand from industrial logistics and export-oriented supply chains

- The plastic segment led the market with a 55.2% share in 2025, driven by its lightweight nature, corrosion resistance, and cost-effective manufacturing

- North America is expected to be the fastest-growing region at a CAGR of 4.5% from 2026 to 2033, fueled by strong demand from chemicals, oil & lubricants, pharmaceuticals, and food processing industries

- Rigid IBCs are the fastest-growing product type, projected to register a CAGR of 12.6% from 2026 to 2033, supported by rising preference for efficient bulk liquid handling solutions in high-volume industrial operations

- The drums segment dominated the product type category with a 41.8% revenue share in 2025, led by extensive usage in bulk transportation of chemicals, lubricants, and industrial liquids across global supply chains

- Chemicals and solvents accounted for 33.6% of the market in 2025, preferred by extensive use of rigid containers for safe storage and transportation of hazardous and non-hazardous chemical products

- The pharmaceuticals and medical devices segment is the fastest-growing end user category, with a CAGR of 11.9% from 2026 to 2033, driven by rising demand for secure and contamination-free packaging of sensitive medical materials

Market Size & Forecast

- Global Market Value (2025): USD 61.19 Billion

- Expected Market Value (2033): USD 86.68 Billion

- Forecast CAGR (2026–2033): 4.45%

- Leading Region in 2025: Asia-Pacific

- Fastest Growing Region: North America

Report Scope and Rigid Industrial Packaging Market Segmentation

|

Attributes |

Rigid Industrial Packaging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Amcor plc (Switzerland) · Coveris (Austria) · Berry Global Inc. (U.S.) · ALPLA-Werke Alwin Lehner GmbH & Co KG (Austria) · Sonoco Products Company (U.S.) · Sealed Air Corporation (U.S.) · Silgan Holdings Inc. (U.S.) · PLASTIPAK HOLDINGS, INC. (U.S.) · Holmen AB (Sweden) · Mondi plc (U.K.) · Sirap Group (Italy) · Tetra Pak International S.A. (Switzerland) · WestRock Company (U.S.) · RESILUX NV (Belgium) · Ardagh Group S.A. (Luxembourg) · Consolidated Container Company (U.S.) · Ball Corporation (U.S.) · DS Smith plc (U.K.) · Georgia-Pacific LLC (U.S.) · Greif, Inc. (U.S.) |

|

Market Opportunities |

· Expansion of Sustainable and Recyclable Packaging Solutions · Growing Adoption of Intermediate Bulk Containers · Rising Use of Smart Tracking and Automation in Packaging |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Rigid Industrial Packaging Market Trends

Trend: Increasing Adoption of Reusable and Circular Packaging Systems

Rigid industrial packaging is witnessing a strong shift toward reusable and circular packaging systems driven by sustainability targets, cost optimization, and stricter environmental regulations across global manufacturing and logistics industries. Companies are increasingly adopting reconditioned steel drums, reusable intermediate bulk containers (IBCs), and returnable packaging pools to reduce material consumption and lifecycle costs. This transition is particularly strong in chemical, lubricant, and industrial liquid supply chains where repeated usage improves efficiency and compliance.

Mauser Packaging Solutions operates one of the largest global reconditioning and collection networks for industrial packaging, supporting closed-loop systems across Europe and North America.

Rigid Industrial Packaging Market Dynamics

Key Market Driver: Rising Demand for Durable and Compliant Bulk Packaging Solutions

The growing need for safe, durable, and regulation-compliant packaging for hazardous and high-value industrial materials is significantly driving demand for rigid industrial packaging solutions. Industries such as chemicals, petrochemicals, and pharmaceuticals require high-strength drums and IBCs to ensure leak-proof storage, transport safety, and regulatory compliance across global supply chains. Increasing international trade in industrial liquids and raw materials further strengthens demand for standardized packaging formats.

Companies such as Greif and Sonoco Products Company are expanding their high-performance drum and container portfolios to meet stringent UN certification and chemical handling standards across global markets.

Key Restraint/Challenge: Raw Material Price Volatility Impacting Production Costs

Fluctuations in raw material prices, particularly for steel, aluminum, and polyethylene, are creating cost pressures for rigid industrial packaging manufacturers and affecting profit margins across the value chain. Since rigid packaging production is highly dependent on petrochemical-based resins and metal inputs, global supply disruptions and energy price volatility directly impact manufacturing costs. This challenge is further intensified by rising transportation and energy expenses across industrial logistics networks.

Berry Global Inc. and ALPLA are actively focusing on material optimization and lightweight packaging innovations to partially offset raw material cost fluctuations and maintain pricing stability.

Key Market Opportunity: Growing Adoption of Intermediate Bulk Containers

The increasing adoption of intermediate bulk containers (IBCs) presents a major growth opportunity in the rigid industrial packaging market, driven by demand for efficient, stackable, and reusable bulk liquid handling solutions. IBCs offer improved space utilization, reduced logistics costs, and enhanced safety for transporting chemicals, food-grade liquids, and pharmaceutical intermediates. Their reusable design also supports sustainability initiatives and circular economy adoption across industrial supply chains.

SCHÜTZ and Greif are significantly expanding their IBC manufacturing and recycling capacities globally to meet rising demand from chemical and industrial distribution sectors.

Rigid Industrial Packaging Market Scope

The rigid industrial packaging market is segmented on the basis of product type, material type, and end user.

- By Product Type

On the basis of product type, the Rigid Industrial Packaging Market is segmented into drums, rigid IBCs, pails, bulk boxes, and others. The Drums segment dominated the market with the largest share of 41.8% in 2025, driven by extensive usage in bulk transportation of chemicals, lubricants, and industrial liquids across global supply chains. Their high durability, compatibility with hazardous materials, and cost efficiency in storage and logistics strengthen widespread adoption. Strong demand from petrochemical and manufacturing industries further supports segment leadership. Expanding cross-border trade of industrial liquids continues to reinforce its dominant position.

The Rigid IBCs segment is projected to register the fastest growth at a CAGR of 12.6% from 2026 to 2033, driven by rising preference for efficient bulk liquid handling solutions in high-volume industrial operations. Their reusable structure, stackability, and reduced transportation costs make them suitable for modern logistics optimization. Increasing adoption across chemicals, food-grade liquids, and pharmaceutical intermediates is accelerating demand. Advancements in smart tracking and automated handling systems further enhance deployment potential in global supply chains. Growing sustainability focus is also supporting transition from single-use containers.

- By Material Type

On the basis of material type, the Rigid Industrial Packaging Market is segmented into plastic, metal, paper and wood, and fibre. The Plastic segment dominated the market with a share of 55.2% in 2025, supported by its lightweight nature, corrosion resistance, and cost-effective manufacturing. High compatibility with chemicals and lubricants makes plastic the preferred choice for industrial storage and transportation. Continuous innovation in high-density polyethylene and polypropylene materials strengthens durability and safety performance. Expanding industrial production and export activities further reinforce its dominant position.

The Fibre segment is projected to register the fastest growth at a CAGR of 11.4% from 2026 to 2033, driven by increasing shift toward sustainable and recyclable packaging solutions. Rising environmental regulations and corporate sustainability goals are encouraging adoption of fibre-based rigid packaging alternatives. Its biodegradability and lower carbon footprint make it suitable for eco-conscious industries such as food and pharmaceuticals. Improvements in strength and moisture resistance technologies are expanding application scope. Growing demand for green packaging materials continues to accelerate segment expansion.

- By End User

On the basis of end user, the Rigid Industrial Packaging Market is segmented into chemicals and solvents, oil and lubricants, agriculture and horticulture, automotive, building and construction, food and beverages, pharmaceuticals and medical devices, and others. The Chemicals and Solvents segment dominated the market with a share of 33.6% in 2025, driven by extensive use of rigid containers for safe storage and transportation of hazardous and non-hazardous chemical products. Strong demand from industrial manufacturing and export-oriented chemical production supports sustained consumption. Strict safety regulations regarding leak-proof and contamination-free packaging further strengthen adoption. Expanding global chemical trade continues to reinforce its leading position.

The Pharmaceuticals and Medical Devices segment is projected to register the fastest growth at a CAGR of 11.9% from 2026 to 2033, driven by rising demand for secure and contamination-free packaging of sensitive medical materials. Increasing global healthcare expenditure and pharmaceutical production expansion are supporting higher packaging requirements. Rigid packaging solutions ensure product integrity, stability, and compliance with regulatory standards. Advancements in sterile packaging technologies and traceability systems are further accelerating adoption. Growing focus on safe drug distribution networks continues to drive segment expansion.

Rigid Industrial Packaging Market Regional Analysis

Asia-Pacific dominated the rigid industrial packaging market and accounted for the largest revenue share of 42% in 2025, supported by large-scale manufacturing activity, strong chemical and petrochemical production, and high demand from industrial logistics and export-oriented supply chains. The region benefits from cost-efficient packaging manufacturing, expanding industrial output, and strong consumption across chemicals, oil & lubricants, agriculture, and food processing sectors. Rapid urbanization, rising cross-border trade, and increasing adoption of durable bulk packaging solutions are further accelerating regional market expansion. Growth in industrial automation and expanding warehousing infrastructure continue to reinforce Asia-Pacific’s leadership position.

China Rigid Industrial Packaging Market Insight

China held the largest share in the Asia-Pacific Rigid Industrial Packaging market in 2025, driven by its dominant chemical manufacturing base, large-scale industrial production, and extensive export activities. The country’s strong petrochemical, automotive, and food processing industries are major consumers of drums, rigid IBCs, and bulk containers for safe and efficient logistics. Advanced manufacturing capabilities and large domestic demand for industrial raw materials further strengthen market penetration. In addition, continuous expansion of industrial parks and logistics networks is reinforcing China’s position as a global hub for rigid industrial packaging production and consumption.

India Rigid Industrial Packaging Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, driven by rapid expansion in chemicals, pharmaceuticals, agriculture, and food processing industries. Increasing industrialization, rising export activities, and growing adoption of standardized bulk packaging solutions are significantly supporting market growth. Demand for cost-effective and durable packaging formats such as drums and rigid IBCs is increasing across mid-sized and large manufacturing units. In addition, government initiatives supporting manufacturing expansion and supply chain modernization are accelerating long-term market development.

Europe Rigid Industrial Packaging Market Insight

The Europe Rigid Industrial Packaging market is expanding steadily, supported by strong demand from chemicals, automotive, pharmaceuticals, and industrial manufacturing sectors. The region benefits from strict regulatory standards for safe chemical handling and sustainable packaging practices, which are driving adoption of reusable and recyclable rigid packaging solutions. Increasing focus on circular economy initiatives and sustainable logistics is further encouraging demand for advanced material-based packaging systems. In addition, strong presence of established chemical industries and cross-border trade within the EU is supporting consistent market growth.

Germany Rigid Industrial Packaging Market Insight

Germany accounted for the largest share in the Europe Rigid Industrial Packaging market in 2025, driven by its strong chemical, automotive, and industrial manufacturing base. The country has a highly developed logistics and export infrastructure that extensively relies on drums, bulk boxes, and rigid containers for safe material handling. High adoption of advanced packaging technologies and strong focus on sustainability and recyclability further strengthen demand. In addition, the presence of leading chemical manufacturers and industrial suppliers reinforces Germany’s leadership position in the regional market.

U.K. Rigid Industrial Packaging Market Insight

The U.K. market is supported by growing demand from pharmaceuticals, food processing, chemicals, and industrial distribution sectors. Increasing emphasis on safe storage and transportation of sensitive materials is driving adoption of high-quality rigid packaging solutions. Rising focus on sustainable packaging practices and regulatory compliance is further encouraging the use of recyclable and reusable packaging formats. In addition, expansion of e-commerce-driven industrial supply chains and third-party logistics services is supporting steady market growth.

North America Rigid Industrial Packaging Market Insight

North America is projected to grow at the fastest CAGR of 4.5% from 2026 to 2033, driven by strong demand from chemicals, oil & lubricants, pharmaceuticals, and food processing industries. Increasing adoption of advanced logistics systems and bulk packaging automation is significantly enhancing operational efficiency across supply chains. Rising preference for durable, reusable, and compliance-driven packaging solutions is further accelerating market expansion. In addition, growing investments in sustainable packaging materials and circular economy initiatives are boosting regional demand.

U.S. Rigid Industrial Packaging Market Insight

The U.S. accounted for the largest share in the North America Rigid Industrial Packaging market in 2025, supported by strong industrial production, advanced chemical manufacturing, and large-scale distribution networks. The country has extensive usage of drums, rigid IBCs, and bulk containers across petrochemical, pharmaceutical, and food industries. Increasing focus on workplace safety regulations and hazardous material handling standards is further strengthening demand. In addition, strong presence of leading packaging manufacturers and advanced logistics infrastructure reinforces the U.S. leadership position in the regional market.

Rigid Industrial Packaging Market Share

The rigid industrial packaging industry is primarily led by well-established companies, including:

- Amcor plc (Switzerland)

- Coveris (Austria)

- Berry Global Inc. (U.S.)

- ALPLA-Werke Alwin Lehner GmbH & Co KG (Austria)

- Sonoco Products Company (U.S.)

- Sealed Air Corporation (U.S.)

- Silgan Holdings Inc. (U.S.)

- PLASTIPAK HOLDINGS, INC. (U.S.)

- Holmen AB (Sweden)

- Mondi plc (U.K.)

- Sirap Group (Italy)

- Tetra Pak International S.A. (Switzerland)

- WestRock Company (U.S.)

- RESILUX NV (Belgium)

- Ardagh Group S.A. (Luxembourg)

- Consolidated Container Company (U.S.)

- Ball Corporation (U.S.)

- DS Smith plc (U.K.)

- Georgia-Pacific LLC (U.S.)

- Greif, Inc. (U.S.)

Latest Developments in Rigid Industrial Packaging Market

- In 2024, Greif announced its agreement to acquire Ipackchem Group, strengthening its position in the high-performance rigid industrial packaging market, particularly in barrier and specialty container solutions used for agrochemicals, flavors, and specialty chemicals. The acquisition enhances Greif’s access to advanced fluorination and multilayer barrier technologies, improving product safety, durability, and chemical resistance in demanding applications. It also expands the company’s presence in premium and regulated packaging segments where compliance and performance standards are strict. Overall, this development intensifies competition in specialty rigid packaging and accelerates consolidation in high-value industrial packaging solutions

- In 2024, SCHÜTZ expanded its global IBC production and recycling network, significantly reinforcing its leadership in intermediate bulk containers by increasing manufacturing capacity across key regions and improving global supply responsiveness. This expansion supports rising demand from chemicals, food-grade liquids, and industrial logistics sectors by ensuring better availability of reusable and standardized bulk packaging systems. The strengthening of closed-loop recycling infrastructure enhances sustainability performance and reduces lifecycle costs for end users. Overall, it is accelerating the global shift toward reusable, efficient, and environmentally responsible rigid industrial packaging solutions

- In 2023, Mauser Packaging Solutions expanded its circular economy and reconditioning operations, strengthening its position in sustainable rigid industrial packaging by enhancing reuse, recycling, and lifecycle management services for steel drums and IBCs. This expansion allows industrial customers in chemicals, lubricants, and manufacturing sectors to reduce packaging costs while complying with stricter environmental regulations. It also improves global availability of reconditioned packaging assets, supporting supply chain continuity and operational efficiency. Overall, the initiative is driving broader adoption of circular packaging models across industrial end-use industries

- In 2023, Berry Global increased investments in sustainable rigid packaging solutions, reinforcing its position in recyclable and lightweight industrial packaging materials through advancements in resin technologies and circular manufacturing systems. This initiative supports improved environmental compliance and reduced carbon footprint across chemical, industrial, and consumer supply chains. It also enhances demand for reusable and recyclable rigid packaging formats as industries shift toward sustainability-focused operations. Overall, the development is contributing to the global transition toward low-impact and resource-efficient industrial packaging solutions

- In 2022, Sonoco completed the acquisition of Ball Metalpack, significantly expanding its presence in the metal rigid industrial packaging segment, particularly in steel containers and aerosol cans used across chemical and lubricant industries. The acquisition improved manufacturing scale, operational efficiency, and product availability across North America, strengthening Sonoco’s competitive positioning. It also enhanced its ability to serve high-strength and durable packaging requirements in industrial applications. Overall, this consolidation reinforced the trend toward larger integrated players in the metal rigid packaging market

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Rigid Industrial Packaging Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Rigid Industrial Packaging Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Rigid Industrial Packaging Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.