Global Rigid Packaging Container Market

Market Size in USD Billion

USD

232.23 Billion

USD

319.06 Billion

2024

2032

USD

232.23 Billion

USD

319.06 Billion

2024

2032

| 2025 - 2032 | |

| USD 232.23 Billion | |

| USD 319.06 Billion | |

| % | |

|

Rigid Packaging Containers Market Size

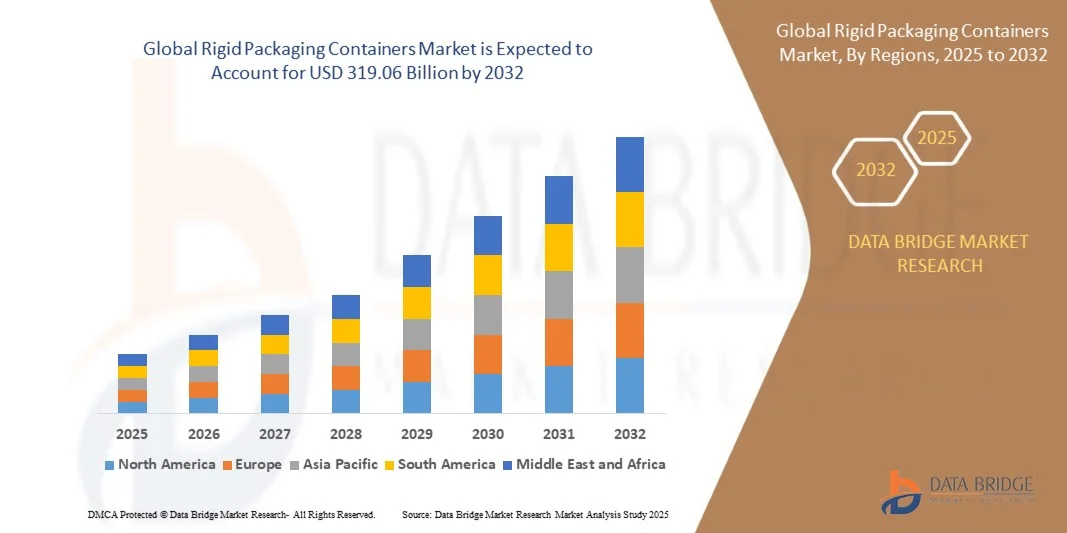

- The global rigid packaging containers market size was valued at USD 232.23 billion in 2024 and is expected to reach USD 319.06 billion by 2032, at a CAGR of 4.05% during the forecast period

- The market growth is largely fueled by the increasing demand for durable, sustainable, and recyclable packaging solutions across the food, beverage, healthcare, and personal care industries. The shift toward rigid packaging containers is driven by their superior protection, extended shelf life, and ability to maintain product integrity during transportation and storage, making them a preferred choice among manufacturers and consumers

- Furthermore, rising consumer awareness of environmental sustainability and the global emphasis on reducing plastic waste are accelerating the adoption of eco-friendly rigid packaging materials such as metal, glass, and bio-based plastics. These factors are encouraging manufacturers to invest in lightweight, recyclable, and reusable rigid containers, thereby supporting market expansion

Rigid Packaging Containers Market Analysis

- Rigid packaging containers, including bottles, jars, cans, and drums, play a vital role in preserving product quality and ensuring safe distribution across diverse end-use sectors such as food, beverages, pharmaceuticals, and industrial goods. Their structural strength, tamper resistance, and aesthetic appeal make them a preferred packaging solution for both consumer and industrial applications

- The growing demand for rigid packaging containers is primarily driven by the rapid expansion of the packaged food and beverage industry, increasing e-commerce activities, and the global movement toward sustainable packaging alternatives. As manufacturers continue to innovate with recyclable materials and efficient designs, the market is poised for steady growth over the forecast period

- Asia-Pacific dominated the rigid packaging containers market with a share of 44.43% in 2024, due to expanding food and beverage production, rapid industrialization, and the strong presence of packaging manufacturers

- North America is expected to be the fastest growing region in the rigid packaging containers market during the forecast period due to increasing consumption of packaged foods, beverages, and healthcare products

- Plastic segment dominated the market with a market share of 65.2% in 2024, due to its versatility, cost-effectiveness, and suitability for mass production. Plastic containers are widely used across industries owing to their lightweight nature, flexibility in design, and durability. Moreover, advancements in high-density polyethylene (HDPE) and polyethylene terephthalate (PET) have enabled manufacturers to produce impact-resistant and transparent packaging with lower environmental impact

Report Scope and Rigid Packaging Containers Market Segmentation

|

Attributes |

Rigid Packaging Containers Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Rigid Packaging Containers Market Trends

“Rising Shift Toward Sustainable and Recyclable Rigid Packaging”

- The global rigid packaging containers market is undergoing a notable transformation driven by the growing shift toward sustainable, recyclable, and lightweight packaging solutions. Manufacturers and brand owners are increasingly prioritizing circular economy principles and eco-friendly materials to meet consumer preferences and comply with environmental regulations

- For instance, Amcor plc and Berry Global Inc. have introduced recyclable PET and post-consumer recycled (PCR) plastic-based rigid containers for food, beverage, and personal care applications. These developments highlight how leading producers are aligning product innovation with the global demand for sustainable and closed-loop packaging systems

- Advancements in material science, including the development of bio-based plastics, compostable polymers, and lightweight metal containers, are further revolutionizing the rigid packaging segment. These innovations enhance functionality while reducing carbon footprints and material waste in manufacturing and disposal stages

- The rising focus on extended shelf life and product safety is accelerating the adoption of high-barrier rigid containers with improved sealing and moisture resistance. These properties ensure product integrity across global supply chains, especially for ready-to-eat foods and sensitive beverages

- Sustainability commitments from global companies in the FMCG, pharmaceutical, and personal care industries are spurring investments in recyclable plastics and mono-material packaging. This transition is supported by stricter environmental mandates encouraging reduced plastic waste and enhanced recyclability across packaging formats

- As consumers and regulators continue to emphasize environmental preservation, the rigid packaging industry is moving toward hybrid sustainability models combining design efficiency, recycled content, and resource conservation. These emerging approaches are expected to redefine the future of rigid container production and waste management across industries

Rigid Packaging Containers Market Dynamics

Driver

“Increasing Demand from the Food and Beverage Sector”

- The expanding food and beverage industry remains a major driver of the rigid packaging containers market. The need for durable, tamper-resistant, and contamination-free packaging solutions for both perishable and non-perishable products continues to fuel the demand for rigid plastics, metals, and glass containers

- For instance, Crown Holdings Inc. and Silgan Holdings Inc. have developed lightweight, high-barrier cans and jars to meet the rising demand for processed foods, carbonated beverages, and dairy products. These innovations combine visual appeal, durability, and extended shelf life to address consumer expectations and logistical requirements

- The surge in convenience foods, ready-to-drink beverages, and e-commerce-based grocery delivery has amplified the demand for rigid packaging formats that offer protection and stackability. Rigid containers support efficient product handling, reduce damage during transit, and provide branding opportunities through advanced labeling and printing technologies

- Increasing emphasis on hygienic packaging in the post-pandemic environment has reinforced demand for resilient, moisture-resistant materials that ensure safety and freshness. Food producers are adopting rigid containers due to their compatibility with automated filling lines and recyclability, offering productivity and sustainability benefits simultaneously

- As global food production and urban consumption patterns expand, rigid packaging containers will remain indispensable for ensuring product safety, convenience, and compliance with evolving food safety standards. This enduring demand is expected to maintain the market’s strong growth trajectory

Restraint/Challenge

“High Cost of Raw Materials and Production”

- Fluctuating raw material costs, particularly for plastics, metals, and glass, represent a persistent challenge for the rigid packaging containers market. Price volatility in petrochemical feedstocks directly impacts the cost of producing rigid polymers such as PET, PP, and HDPE used extensively in consumer packaging

- For instance, packaging manufacturers such as Amcor and DS Smith have reported margin pressures due to rising energy and resin costs in recent years. These fluctuations also complicate pricing strategies and long-term supply agreements with clients in competitive packaging segments

- In addition, the high energy consumption associated with metal smelting, glass forming, and plastic molding processes significantly elevates production costs. This is particularly critical for companies transitioning to eco-friendly or bio-based materials, which often require specialized, cost-intensive processing technologies

- Transportation and logistics costs for heavy and bulky rigid packaging further add to the total cost of ownership, limiting adoption among cost-sensitive small and medium enterprises. Moreover, compliance with environmental regulations regarding emissions and recyclability increases expenses related to material certification and waste management

- The long-term stability of raw material supply, investments in lightweight design, and enhanced recycling infrastructure are essential to mitigating cost challenges. Achieving production efficiency through automation and renewable energy use will play a key role in maintaining competitiveness and ensuring sustainable growth in the rigid packaging container market

Rigid Packaging Containers Market Scope

The market is segmented on the basis of product type, material, capacity, and end use.

- By Product Type

On the basis of product type, the rigid packaging containers market is segmented into bottles & jars, cans, jerry cans, drums, kegs, and clamshells. The bottles & jars segment dominated the market with the largest revenue share in 2024, driven by their widespread usage across food, beverage, and personal care industries. Their strong barrier properties, recyclability, and compatibility with diverse closure systems make them a preferred choice for both liquid and semi-solid packaging. Bottles & jars also offer excellent brand visibility and ease of handling, which further enhances their adoption among manufacturers emphasizing premium packaging designs.

The cans segment is anticipated to witness the fastest growth rate from 2025 to 2032, propelled by increasing demand in the beverage and food sectors for lightweight, durable, and tamper-resistant packaging solutions. Metal cans provide superior protection against contamination and have a long shelf life, making them ideal for carbonated drinks and processed foods. The growing popularity of recyclable aluminum cans, driven by sustainability trends and circular economy initiatives, further supports their rapid market expansion.

- By Material

On the basis of material, the rigid packaging containers market is segmented into plastic and metal. The plastic segment dominated the market with a share of 65.2% in 2024 due to its versatility, cost-effectiveness, and suitability for mass production. Plastic containers are widely used across industries owing to their lightweight nature, flexibility in design, and durability. Moreover, advancements in high-density polyethylene (HDPE) and polyethylene terephthalate (PET) have enabled manufacturers to produce impact-resistant and transparent packaging with lower environmental impact.

The metal segment is projected to record the fastest CAGR from 2025 to 2032, driven by rising preference for recyclable and sustainable packaging materials. Metal containers offer exceptional strength, chemical resistance, and temperature tolerance, making them suitable for food preservation, healthcare, and industrial uses. The resurgence of aluminum packaging, backed by initiatives for eco-friendly alternatives to plastics, is a major factor accelerating segment growth.

- By Capacity

On the basis of capacity, the rigid packaging containers market is segmented into up to 5 litre, 5 to 20 litre, 20 to 50 litre, and 50 litre & above. The up to 5 litre segment dominated the market in 2024 due to high consumption in food, beverage, and personal care applications. These small-sized containers are preferred for consumer goods packaging as they offer portability, convenience, and portion control. The segment’s dominance is also reinforced by the extensive use of compact rigid bottles and jars for retail packaging and e-commerce deliveries.

The 20 to 50 litre segment is anticipated to witness the fastest growth rate from 2025 to 2032, driven by growing industrial and commercial demand for bulk packaging solutions. This capacity range is widely used in chemicals, lubricants, and cleaning products due to its balance between storage efficiency and handling convenience. Increasing adoption of reusable rigid drums and intermediate containers for cost-effective logistics is expected to further propel segment growth.

- By End Use

On the basis of end use, the rigid packaging containers market is segmented into food, beverages, homecare products, personal care products, healthcare products, electronics & electrical, industrial goods, and others. The food segment dominated the market in 2024, driven by the rising demand for durable, hygienic, and tamper-proof packaging for perishable and processed foods. Rigid containers ensure product safety and freshness while supporting branding through attractive designs and labeling. The growth of packaged and ready-to-eat food products further sustains high demand in this segment.

The beverages segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by the increasing consumption of bottled water, soft drinks, and alcoholic beverages. Rigid containers such as bottles, cans, and kegs provide superior barrier protection, ensuring product integrity and extended shelf life. The segment also benefits from innovations in lightweight and recyclable rigid packaging solutions, which align with consumer preference for sustainable beverage packaging.

Rigid Packaging Containers Market Regional Analysis

- Asia-Pacific dominated the rigid packaging containers market with the largest revenue share of 44.43% in 2024, driven by expanding food and beverage production, rapid industrialization, and the strong presence of packaging manufacturers

- The region’s cost-efficient manufacturing capabilities, rising consumption of packaged goods, and growing urban population are accelerating market expansion

- Increasing adoption of recyclable plastic and metal packaging materials, supported by government initiatives promoting sustainability, further strengthens regional growth

China Rigid Packaging Containers Market Insight

China held the largest share in the Asia-Pacific rigid packaging containers market in 2024 due to its massive food, beverage, and personal care industries, along with high packaging production capacity. The country’s robust manufacturing infrastructure, technological advancements in molding and extrusion processes, and strong export base are driving market dominance. Rising investments in sustainable packaging solutions and the adoption of lightweight rigid containers for e-commerce and FMCG applications are enhancing market development.

India Rigid Packaging Containers Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, fueled by surging demand for packaged food and beverages, rapid retail sector expansion, and government support for domestic manufacturing under the “Make in India” initiative. Growing urbanization, a rise in disposable incomes, and increased consumer awareness of product safety and hygiene are further stimulating demand for rigid packaging containers. In addition, the expansion of pharmaceutical and personal care industries is contributing to sustained market growth.

Europe Rigid Packaging Containers Market Insight

The Europe rigid packaging containers market is expanding steadily, supported by high adoption of recyclable materials, stringent sustainability regulations, and a well-developed food and beverage industry. The region’s focus on reducing plastic waste and promoting circular economy practices is driving the shift toward reusable and eco-friendly rigid packaging. Rising demand for premium packaging designs and strong consumer preference for durable and visually appealing containers are contributing to continued market expansion.

Germany Rigid Packaging Containers Market Insight

Germany’s market is driven by its strong industrial base, advanced packaging technologies, and focus on sustainable production practices. The country’s high-quality manufacturing standards and adoption of metal and glass rigid containers in beverages and pharmaceuticals are key growth drivers. Investments in automation, material innovation, and closed-loop recycling systems are further enhancing Germany’s leadership in the European packaging sector.

U.K. Rigid Packaging Containers Market Insight

The U.K. market benefits from growing demand for sustainable and lightweight packaging solutions across food, beverage, and healthcare sectors. Increased awareness of environmental impact, coupled with innovations in biodegradable rigid materials, is supporting market growth. The country’s emphasis on eco-friendly packaging and efforts to minimize plastic waste post-Brexit are encouraging manufacturers to invest in advanced rigid packaging technologies.

North America Rigid Packaging Containers Market Insight

North America is projected to grow at the fastest CAGR from 2025 to 2032, driven by increasing consumption of packaged foods, beverages, and healthcare products. High adoption of innovative packaging formats, strong retail infrastructure, and rising focus on recyclable rigid materials are supporting regional expansion. The growing influence of sustainability-driven consumer preferences and manufacturer initiatives toward lightweight packaging solutions are propelling market growth.

U.S. Rigid Packaging Containers Market Insight

The U.S. accounted for the largest share in the North America market in 2024, supported by robust demand from food processing, healthcare, and personal care sectors. The presence of major packaging manufacturers, technological advancements in plastic and metal molding, and increasing integration of recycled materials in packaging production are key factors driving dominance. The country’s strong emphasis on sustainable packaging and extensive distribution networks further reinforce its leading position in the regional market.

Rigid Packaging Containers Market Share

The rigid packaging containers industry is primarily led by well-established companies, including:

- DS Smith (U.K.)

- Georgia-Pacific (U.S.)

- Holmen (Sweden)

- PLASTIPAL HOLDINGS, INC (U.S.)

- Reynolds (U.S.)

- Tetra Pak International S.A. (Switzerland)

- Crown (U.S.)

- Sonoco Products Company (U.S.)

- Ardagh Group S.A. (Luxembourg)

- Dow (U.S.)

- Amcor plc (Switzerland)

- Ball Corporation (U.S.)

- Bemis Company, Inc. (U.S.)

- Berry Global Inc. (U.S.)

- MeadWestvaco Corporation (U.S.)

- Silgan Holdings Inc. (U.S.)

- Coveris (U.K.)

- Sealed Air (U.S.)

- RESILUX NV (Belgium)

- Mondi (U.K.)

Latest Developments in Global Rigid Packaging Containers Market

- In September 2025, a memorandum of understanding (MoU) was signed between Harcourt Butler Technical University (India) and Mercury Industries Limited to jointly research and develop innovations in metal and plastic rigid packaging, including paint cans, drums, food cans, and plastic containers. This collaboration aims to advance material science, coatings, and design optimization in rigid packaging, strengthening India’s manufacturing competitiveness. The initiative highlights the growing emphasis on R&D and academia–industry partnerships to enhance product performance and sustainability in the rigid packaging sector

- In May 2025, Avantium partnered with The Bottle Collective to develop next-generation fibre-based rigid bottles using plant-derived PEF polymers for food, beverage, and pharmaceutical applications. This partnership marks a major step toward sustainable rigid packaging by replacing fossil-based plastics with bio-based alternatives. It is expected to accelerate the adoption of circular packaging solutions, reduce carbon footprint, and set new standards for eco-friendly rigid containers across global markets

- In April 2025, LyondellBasell Industries N.V. introduced Pro-fax EP649U, a high-performance polypropylene impact copolymer tailored for thin-walled injection-moulded rigid packaging. The new grade offers improved flow and compatibility with recycled and renewable content, addressing the demand for lightweight and sustainable packaging. This product launch enhances the company’s portfolio in advanced polymer solutions and supports brand owners aiming for high-efficiency, lower-emission rigid containers

- In November 2024, Amcor Plc announced the acquisition of Berry Global Group in an US $8.4 billion all-stock deal, forming one of the world’s largest rigid packaging and closures companies. The merger strengthens Amcor’s global scale, diversifies its rigid packaging offerings, and enhances pricing power across consumer and industrial markets. This consolidation marks a major shift in the competitive landscape, with larger integrated players gaining stronger positions in the global rigid packaging industry

- In June 2024, Sonoco Products Company completed the acquisition of Eviosys Packaging for approximately US $3.9 billion, expanding its portfolio in rigid metal containers for food and aerosol applications. This acquisition enhances Sonoco’s presence in high-barrier and specialty rigid packaging segments, aligning with rising demand for durable, recyclable, and premium packaging. The deal underscores increasing market focus on sustainability and innovation in rigid metal packaging solutions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Rigid Packaging Container Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Rigid Packaging Container Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Rigid Packaging Container Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.